This article is written by Tiger Research. Despite the downturn in the cryptocurrency market, the tokenized stock market continues to grow. It is divided into fully collateralized spot futures and perpetual futures, with perpetual futures receiving the most attention and a series of new strategies emerging.

Key Points Summary

- While the stock market continues to hit new highs, both the market capitalization and trading volume of cryptocurrencies have declined. As the two trends diverge, the tokenized stock market has realized growth through building open positions in perpetual futures contracts.

- The market is divided into fully collateralized spot futures and perpetual futures. Perpetual futures are noteworthy because they can trade stocks that are not available on local exchanges 24 hours a day and can utilize leverage.

- After the regular trading hours, price trends will become leading indicators for the next day's spot opening price, which can predict not only the direction of price movements but also the magnitude of price fluctuations.

- Two retail trades, one delta-neutral trade, earn premiums as funding through spot trades and engage in cross-exchange arbitrage by exploiting price gaps.

- The same structure also applies to businesses such as market makers, regional oracles, token issuance, and basis hedging funds. Although on a smaller scale, opportunities for investment and business are emerging with the participation of institutional investors.

1. The Stock Market is Absorbing Cryptocurrency Liquidity

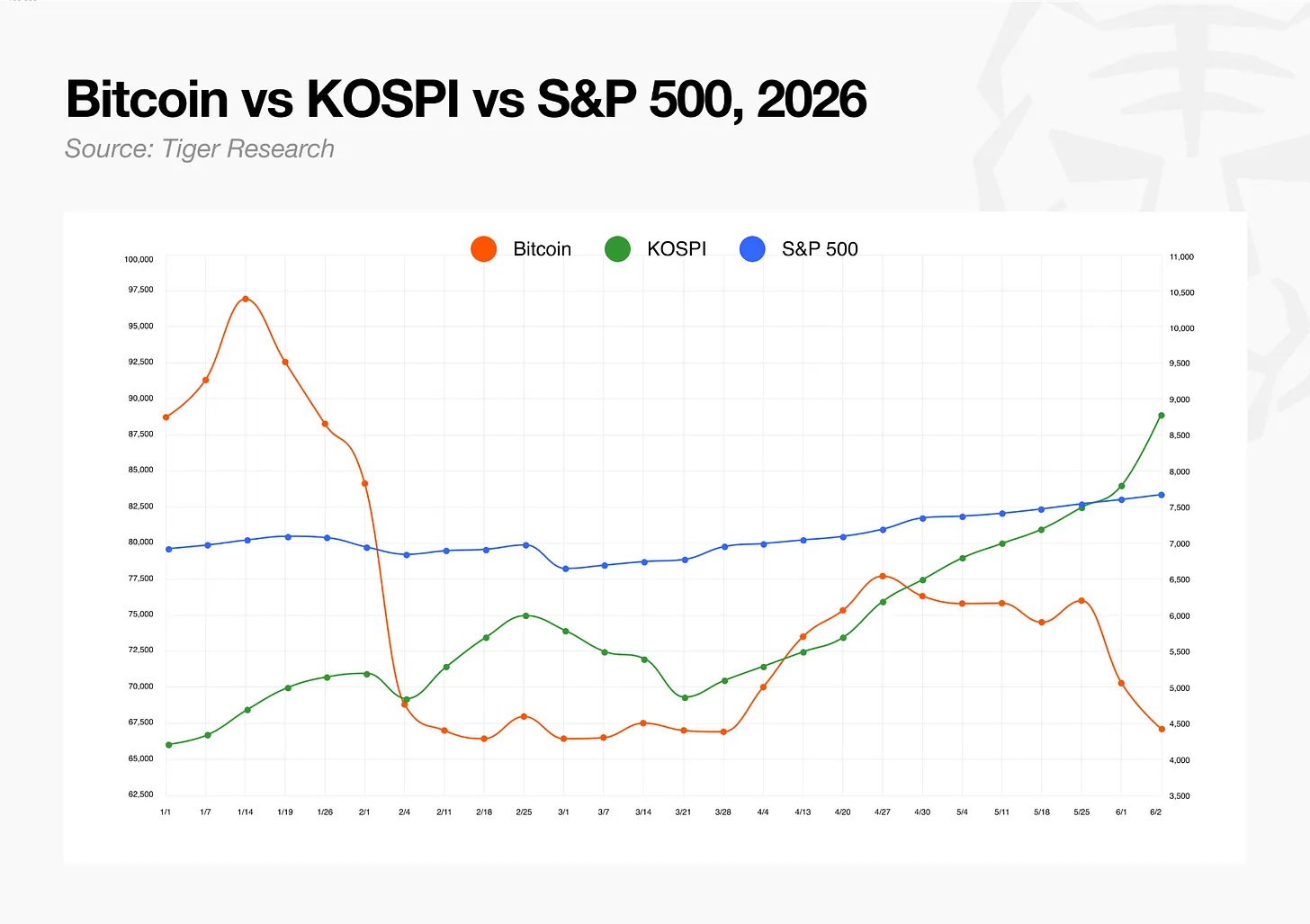

In the first quarter of 2026, the total market capitalization of cryptocurrencies fell by 20.4%, and centralized exchange spot trading volume dropped by 39.1%. Bitcoin has been declining since it hit an all-time high in October 2025.

The stock market's trend stands in stark contrast. The S&P 500 easily surpassed its annual target, and the Korea Composite Stock Price Index (KOSPI) also benefited from a rally in the semiconductor industry, doubling this year. Meanwhile, the total market capitalization of cryptocurrencies has significantly fallen, while the stock markets in most countries have hit historic highs. These two paths have never been so distinctly different.

2. Collateral Segmentation Market, Funds Flowing to Criminals

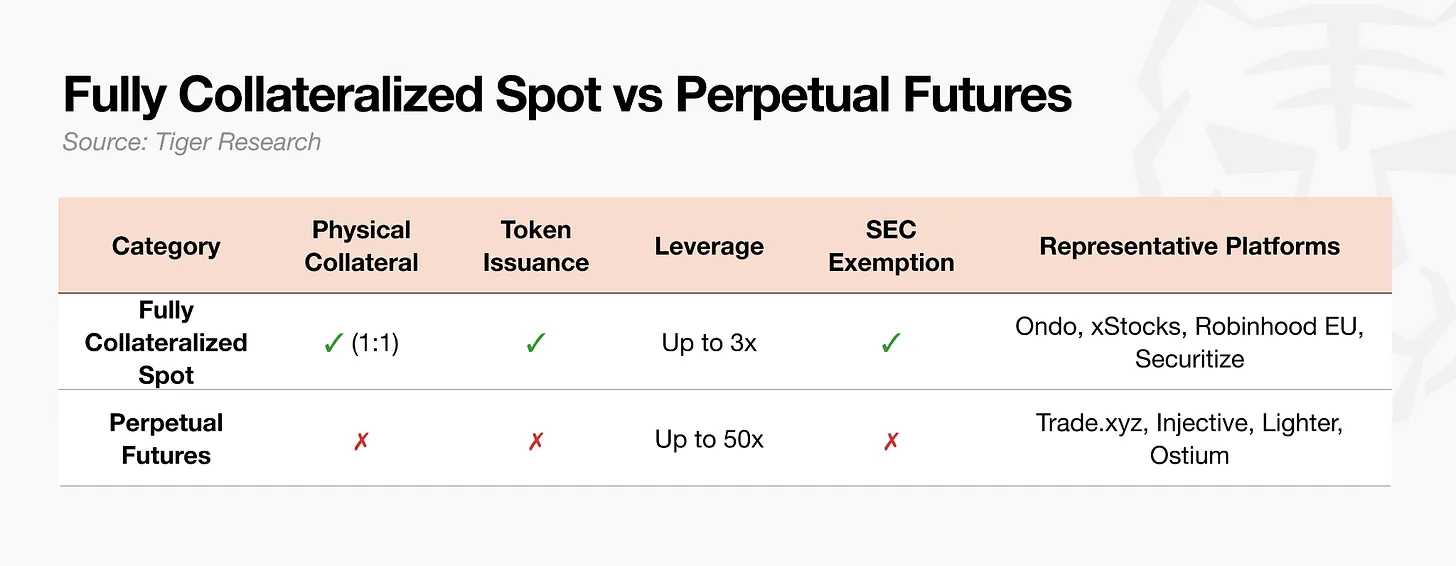

The tokenized stock market is divided into two parts based on collateral structure.

Fully collateralized spot trading deposits real stocks on a 1:1 basis, then issues tokens. Investors hold the stocks themselves or their legal claims. The details of issuance vary by platform, but the underlying assets are always present.

Perpetual futures operate differently. They do not hold any actual stocks. Traders pay margin and open a contract that tracks prices, so there are no claimable underlying assets. Margins are typically paid in stablecoins, and an increasing number of platforms now also accept other assets such as Ethereum (ETH).

Perpetual contracts are attractive because they retain the advantages of spot trading, provide around-the-clock trading of stocks that cannot be traded on local exchanges, and offer higher leverage. Some fully collateralized spot products on Kraken xStocks offer up to 3 times margin, while perpetual contract leverage can be as high as 20 times, depending on the product. Since there is no need to hold the underlying assets, and prices are tracked only through oracle data sources, the listing speed is fast and the range of tradable stock codes is wide.

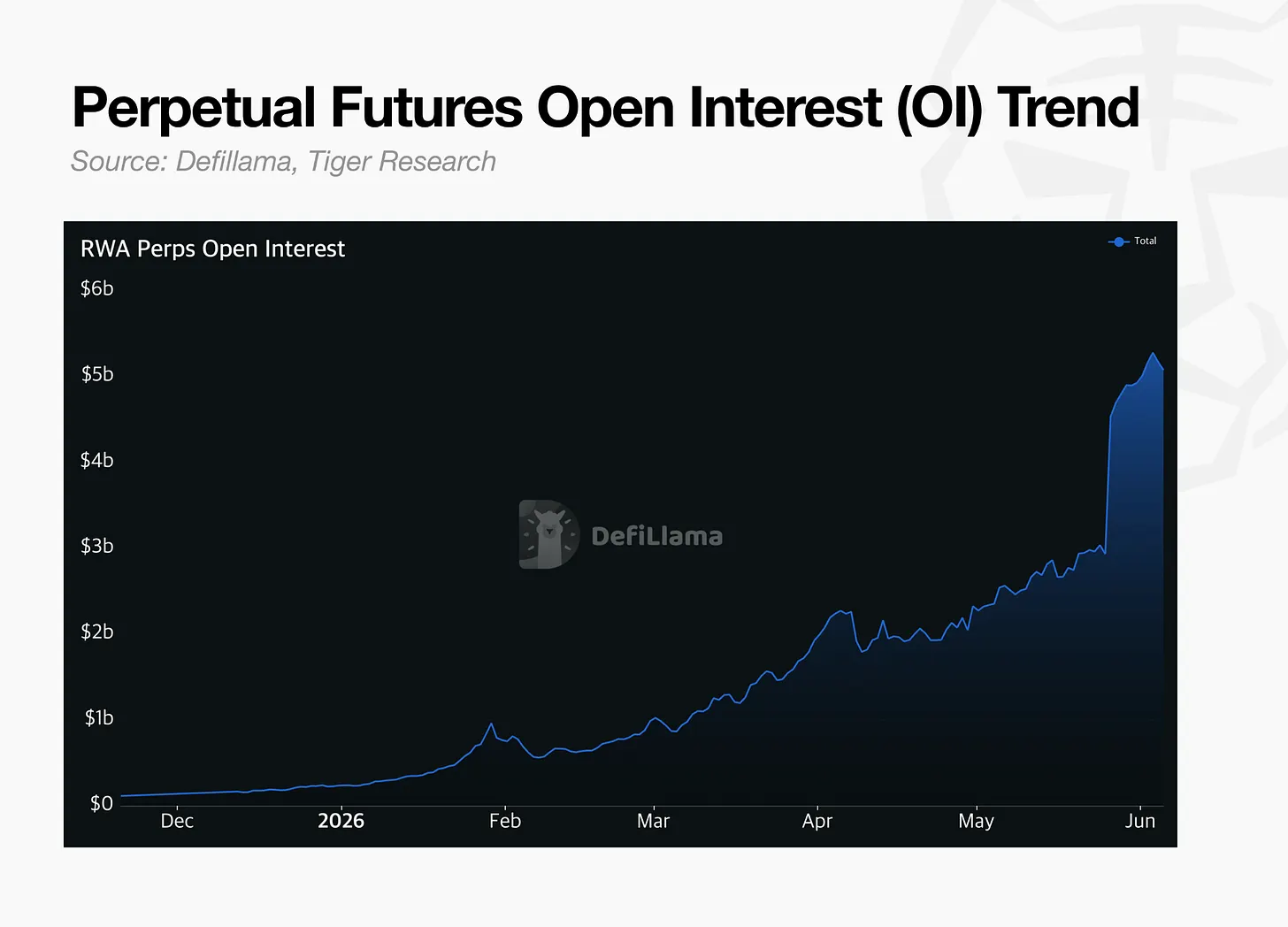

Compared to the traditional market, it is still small in scale. The average daily turnover of the U.S. stock market is about $1.1 trillion. The open interest of stock options (i.e., the total of currently valid contracts) amounts to $2.25 billion. It is difficult to make a direct comparison due to different measuring indicators, but it is clear that this market is still in its early stages.

The direction is clear. Open interest (OI) is growing each quarter, and regulators are beginning to see it as a market. The U.S. Securities and Exchange Commission (SEC) has categorized such contracts as innovative financial products, and the Commodity Futures Trading Commission (CFTC) is publicly reviewing its institutionalized operations in the U.S. Initially falling outside regulatory oversight, this contract is now rapidly entering the regulatory framework.

3. 24-Hour Market and Physical Market

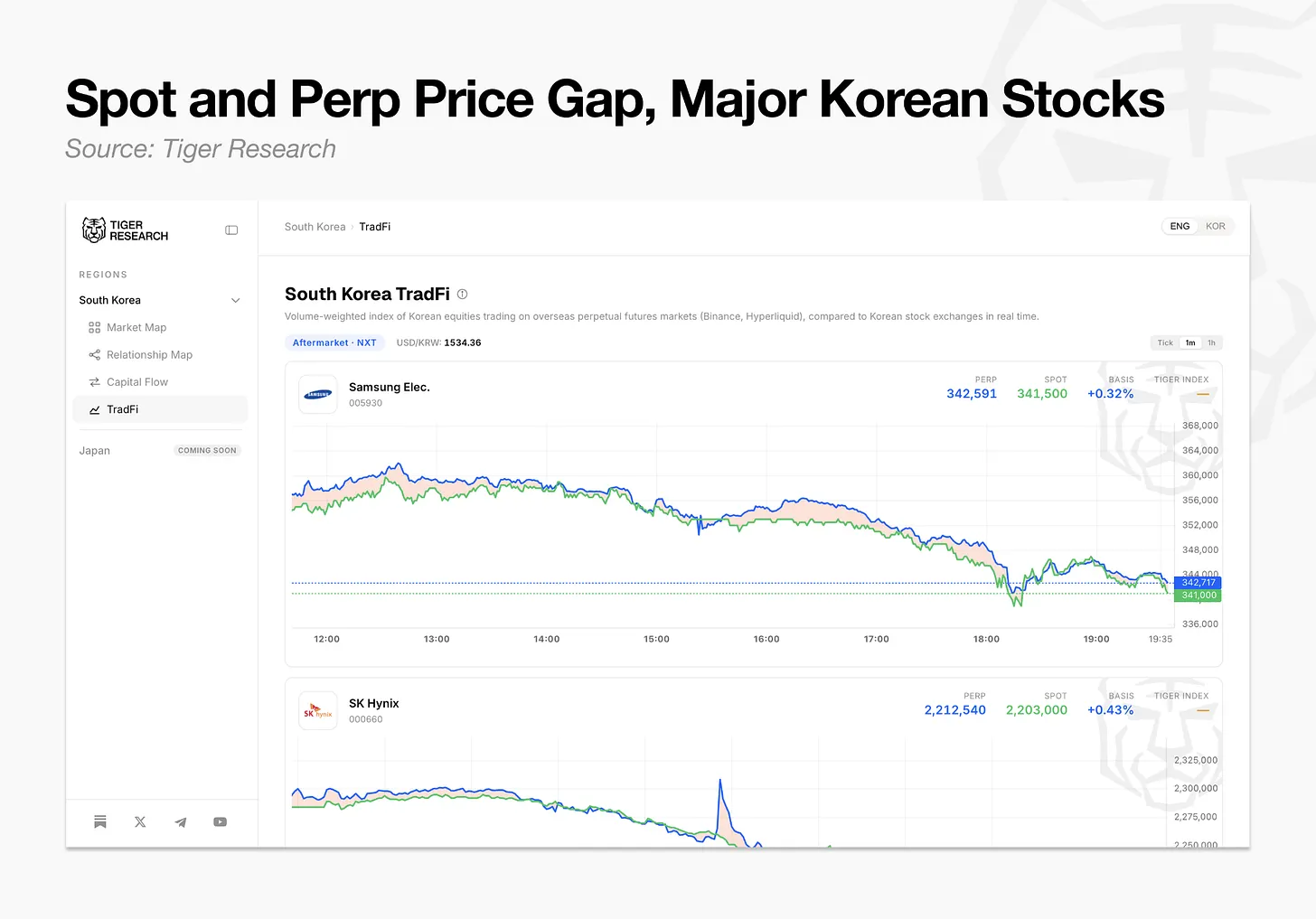

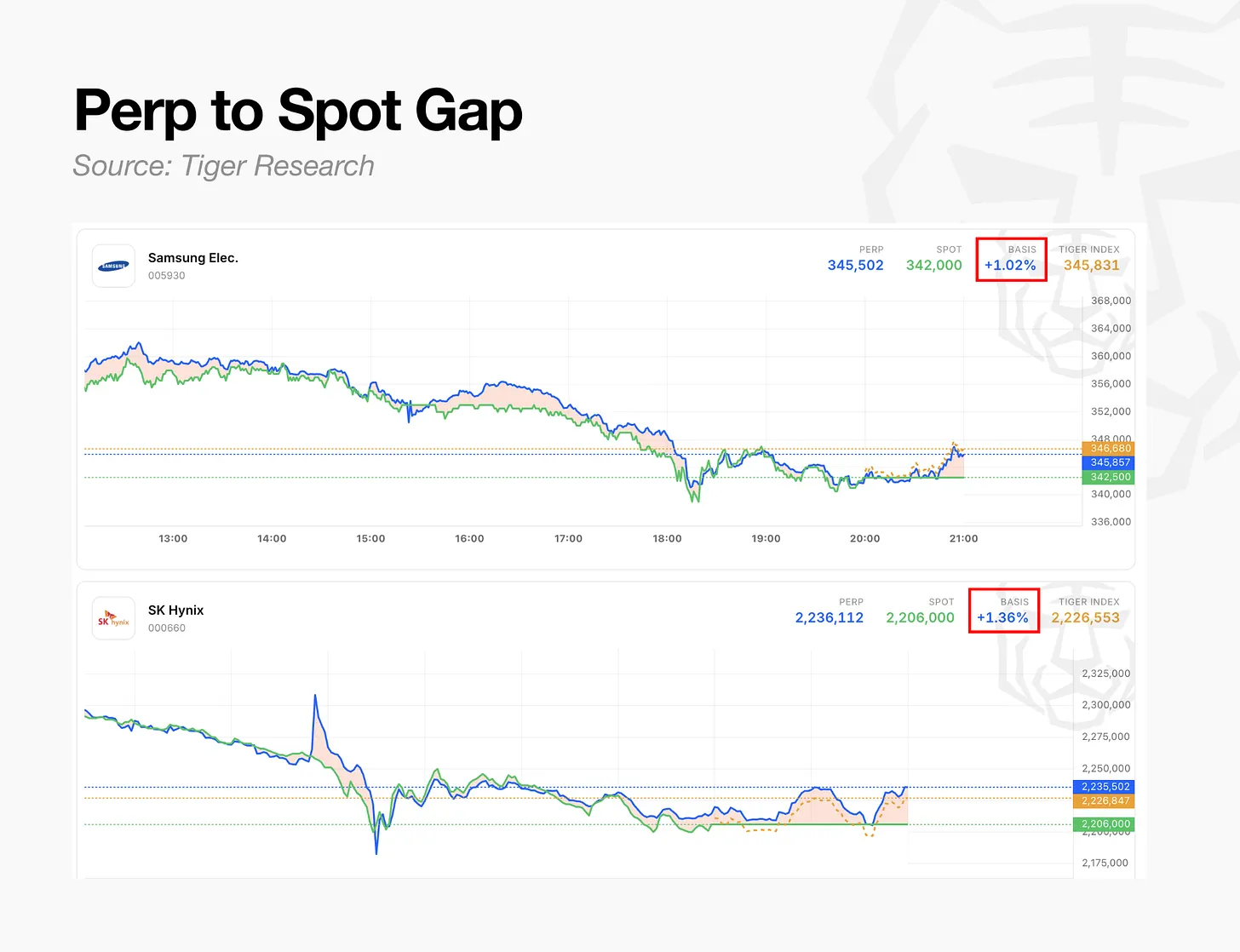

Tiger Research has tracked this change and provided a tool to compare real-time prices of Korean stocks in the overseas perpetual contract market with the domestic spot prices of the Korea Exchange (KRX). This tool aggregates the prices from perpetual contract exchanges supporting stocks such as Samsung Electronics, SK Hynix, and Hyundai Motor, using a volume-weighted average method and displays them alongside the domestic spot prices for each stock.

The current data reveals three patterns.

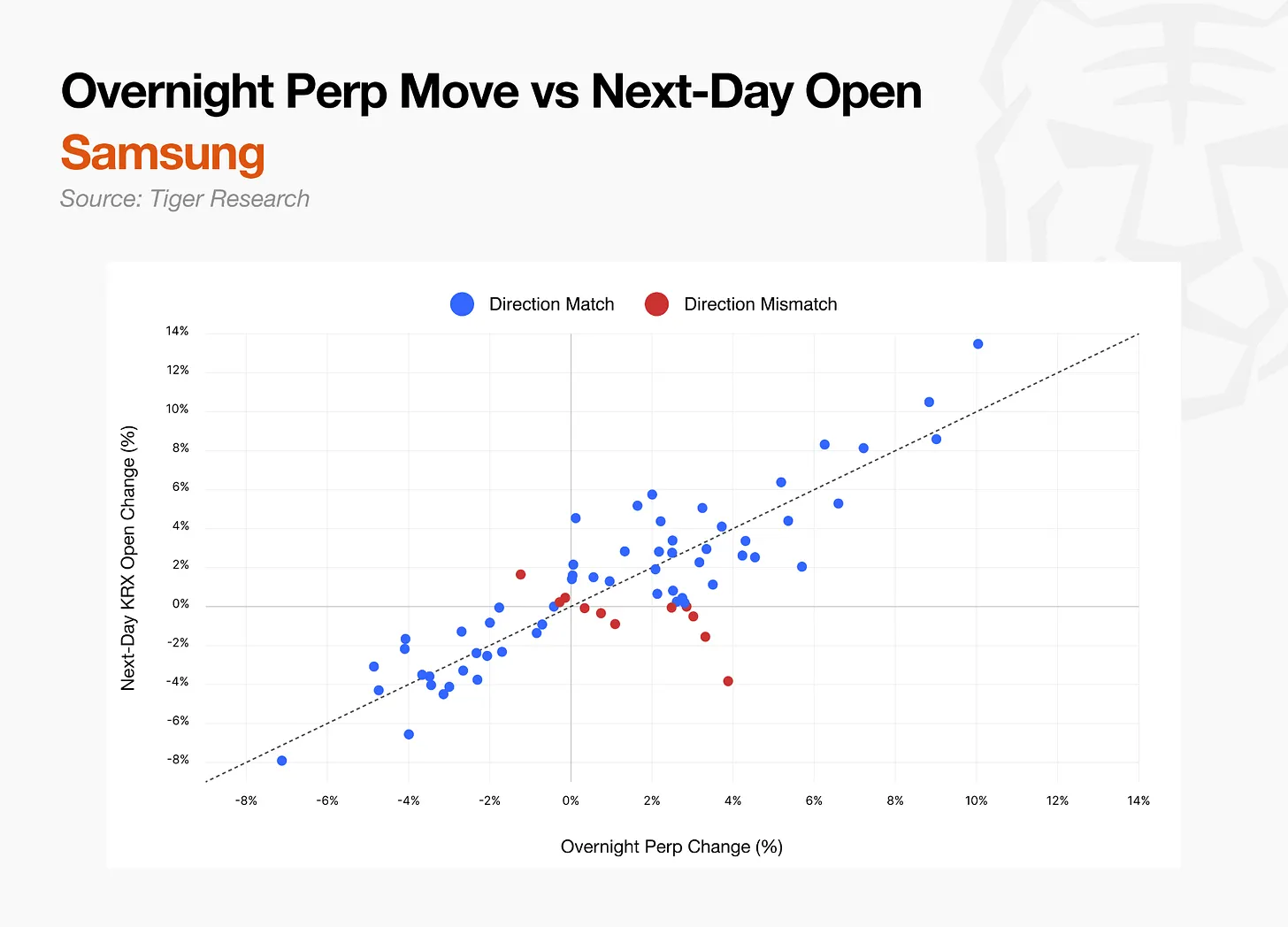

3.1. Criminal Activity Predicts Overnight Trends for the Next Opening

The Korean stock market closes during the night. The U.S. stock market is volatile, and the Nvidia report shows that the exchange rate fluctuates too, but the Korean stock market does not resume trading until the next morning. Criminals conduct trades during the night.

This raises a question. What price do criminals reference after the spot trading closes?

The answer is that they do not follow established market prices. During trading hours, criminals extract spot prices from institutional data. After trading hours, the criminals' own trades directly determine the prices. They do not replicate the spot market prices that have already ended but discover new prices based on overnight news and macroeconomic variables.

The data confirms this. On days when the stock price rises after the closing, the probability of Samsung Electronics and SK Hynix opening higher on the next trading day is 82% and 95%, respectively. When the stock price falls after closing, the probabilities for Samsung Electronics and SK Hynix opening lower the next trading day are 96% and 78%, respectively. The consistency of the trends for both is about 85%, with a correlation coefficient between 0.85 and 0.89.

The extent of the increase also correlates with stock price trends. An overnight increase of 3% in stock prices leads to an opening price increase of about 3%. The regression coefficients between the price increase of Samsung Electronics and the actual opening gap is 0.93, and for SK Hynix, it is 1.00, which can almost predict the magnitude of the rise.

The weekend trend is even sharper. From Friday's close to Monday's open, the predicted stock price trends for Samsung Electronics match the actual opening price on Monday with a rate of 93%, while for SK Hynix, this ratio is 87%, as predicted stock price trends will first absorb two days of global market volatility factors.

By observing the overnight futures prices, one can gain advanced knowledge of the early morning opening price trends.

3.2. Delta-Neutral Trading of Spot Premiums

Perpetual contracts do not have an expiration date. To prevent the price from deviating too far from the reference price, longs and shorts periodically exchange costs, known as funding rates.

For example, when the price is above the reference price, the profitable longs need to pay premiums to the losing shorts. The higher the premium, the more premium paid. When one side profits beyond the reference price, they must pay corresponding fees. To avoid this portion of fees, traders adjust strategies, and the final price will fall back to near the reference price.

Data shows that the trading price of Korean stock futures is higher than that of spot prices, with Samsung Electronics averaging a daily premium of 0.15% and SK Hynix at 0.23%. Selling futures means earning this premium as funding in each trading cycle.

The strategy is as follows: Buy KRX spot during the day while simultaneously selling an equal amount of option contracts. If the stock rises, spot gains increase, and option contracts incur losses; if the stock falls, the opposite occurs. The two offset each other, so regardless of stock trends, the final result approaches zero. In return, funds come from the sold option contracts. This position profits solely from the option fees without needing to bet on direction. This method of eliminating directional risk is called delta-neutral trading.

The premium does not last long. The spot gap typically narrows by half in about 40 minutes. It is applicable during high volatility phases with expanded premiums but requires continuous monitoring.

3.3. Arbitrage Using Inter-Exchange Price Gaps

At the same time, different exchanges show price differences for perpetual contracts of the same stock. Data from June 2026 shows that Binance's perpetual contract price for Samsung Electronics is, on average, 0.93% higher than that of Hyperliquid. The contract price for SK Hynix is 1.03% higher, with peaks reaching 2.3%.

Positions cannot be transferred between different exchanges. Traders need to establish opposing positions simultaneously on both exchanges, shorting on the exchange with the higher price and going long on the exchange with the lower price, so that directional profits and losses offset each other. As the two prices converge, the initial price gap translates into profit. Short positions on the exchange with the higher price can also gain funding, thus increasing returns.

Exchanges that enter later often maintain a higher price because arbitrage funds flow in less. As more exchanges are launched, this price gap is likely to repeatedly occur in the early stages. At night and on weekends, when spot trading is closed, each exchange sets prices independently, further widening the price gap.

4. Market Changes and Emerging Opportunities

A significant challenge in this market lies in its decentralization, which presents both risks and opportunities. Due to cryptocurrencies of the same name being dispersed across existing exchanges in Korea and platforms like Hyperliquid, Binance, and Lighter, liquidity is segmented. Price differences exist between different trading platforms, making it difficult to determine which cryptocurrency is truly traded, while the price disparity offers room for confusion and manipulation. Overlaying leverage in a poorly liquid environment can lead to chain liquidations. This is both an opportunity and a risk.

The openings listed above are for retail. The same structure also provides opportunities for other commercial uses.

Market Makers: The trading price difference for the same stock across different exchanges ranges from 0.15% to 0.75%, and the price gap during the night widens further. In the early market with scarce arbitrage funds, the price gap will remain persistently large. Due to the lack of liquidity and multiple exchanges managing dispersed liquidity, market-making demands are expected to continue growing.

Regional Oracles: Criminals discover prices during the closure of spot trading; their accuracy depends on the oracle. Currently, oracles that provide accurate prices for assets in Asian time zones, such as Korea, Japan, and Taiwan, are still under development.

Tokenized Issuance: The currently listed Korean companies are limited to Samsung Electronics, SK Hynix, and Hyundai Motor. The market needs an intermediary to list and manage KOSPI 200 index constituents and major Asian companies.

Basis Hedge Funds: Investors convert premiums above spot prices into funding every hour. Funds specifically collecting basis and funding gaps from various exchanges operate faster than traditional basis trading, although the market size remains too small to fully absorb.

Compared to traditional markets, the illegal trading market is smaller in scale, but its importance cannot be overlooked. It is the first to discover prices, operates 24/7, and is rapidly moving towards institutionalization. There are enormous opportunities in both investment and commercial aspects.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。