This article is written by Tiger Research. The DeFi ecosystem already has all the core financial primitives: swaps, lending, yield, derivatives, all of which are available. What is truly missing is the execution layer that allows ordinary users to smoothly use these products. Countless teams have previously attempted to eliminate wallet thresholds and cross-chain friction but have failed to go far. This article explores where these attempts went wrong.

Key Points

- The DeFi infrastructure has matured, but user-friendly applications that retain users are still absent. Traditional fintech companies like Robinhood are constrained by regulations and cannot enter the realm of self-custody and high-leverage products.

- defi.app launched in February 2025, accumulating a trading volume of $44 billion and 1.06 million registered users. The no Gas fee, cross-chain seamless operation interface has been validated by the market.

- Rocket Perps charges fees much higher than mainstream DEXs, but 80% of the platform's total revenue is directed toward the $HOME token buyback in accordance with the DIP-004 governance proposal.

- If defi.app wants to sustain long-term growth, it must go beyond short-term user acquisition and establish a daily habit for users based on trust.

1. Why No One Has Captured the DeFi Execution Layer

Ethereum launched in 2015, and the development of DeFi has spanned ten years, yet mainstream adoption remains stagnant. The core barrier is not the products themselves but the friction of user experience.

A 2023 survey by Consensys/YouGov indicated that 93% of global respondents have heard of cryptocurrency, yet only 8% claim familiarity with Web3 or DeFi. There has been no significant change since then.

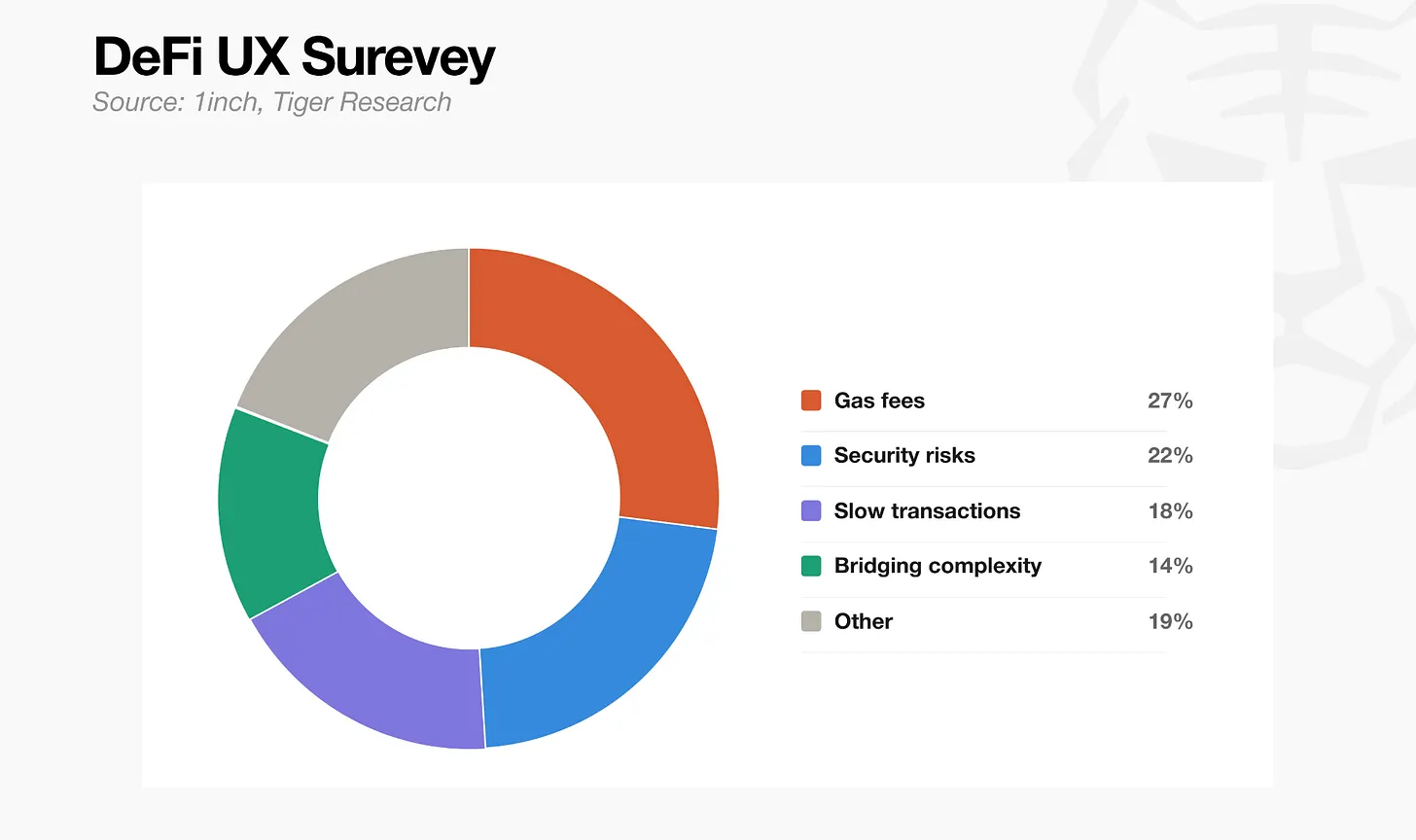

A January 2025 1inch survey summarized DeFi's main pain points as: Gas fees (27%), security risks (22%), slow transaction speeds (18%), complexity of cross-chain operations (14%). These are all experience friction, not defects of the products themselves.

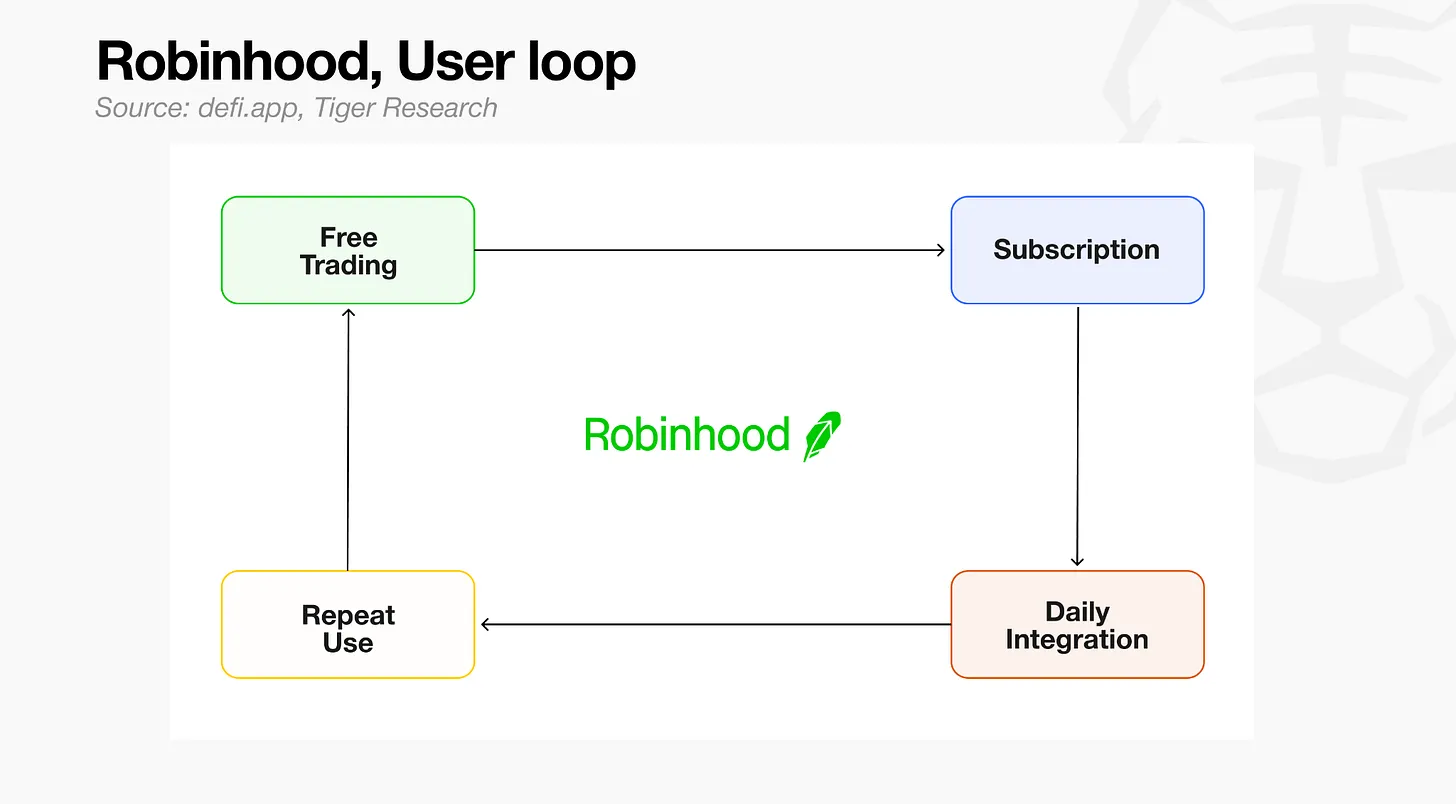

Robinhood's success in traditional finance relied on turning stock trading into a process easily completed on a mobile phone during an era of prevalent broker commissions and cumbersome account opening processes. With a low enough barrier, anyone is willing to give it a try.

The user demand in DeFi is structurally different, covering high-leverage derivatives, on-chain yields, and self-custodied assets. These areas are precisely those that regulated fintech companies legally cannot touch. Robinhood has begun to dabble in some crypto spot trading, but self-custody and unlicensed high-leverage products remain firmly outside its regulatory boundaries.

The goal of the DeFi execution layer is not to replicate Robinhood's business but to create Robinhood-level experiences in areas where Robinhood cannot enter.

2. Where Previous Attempts Failed

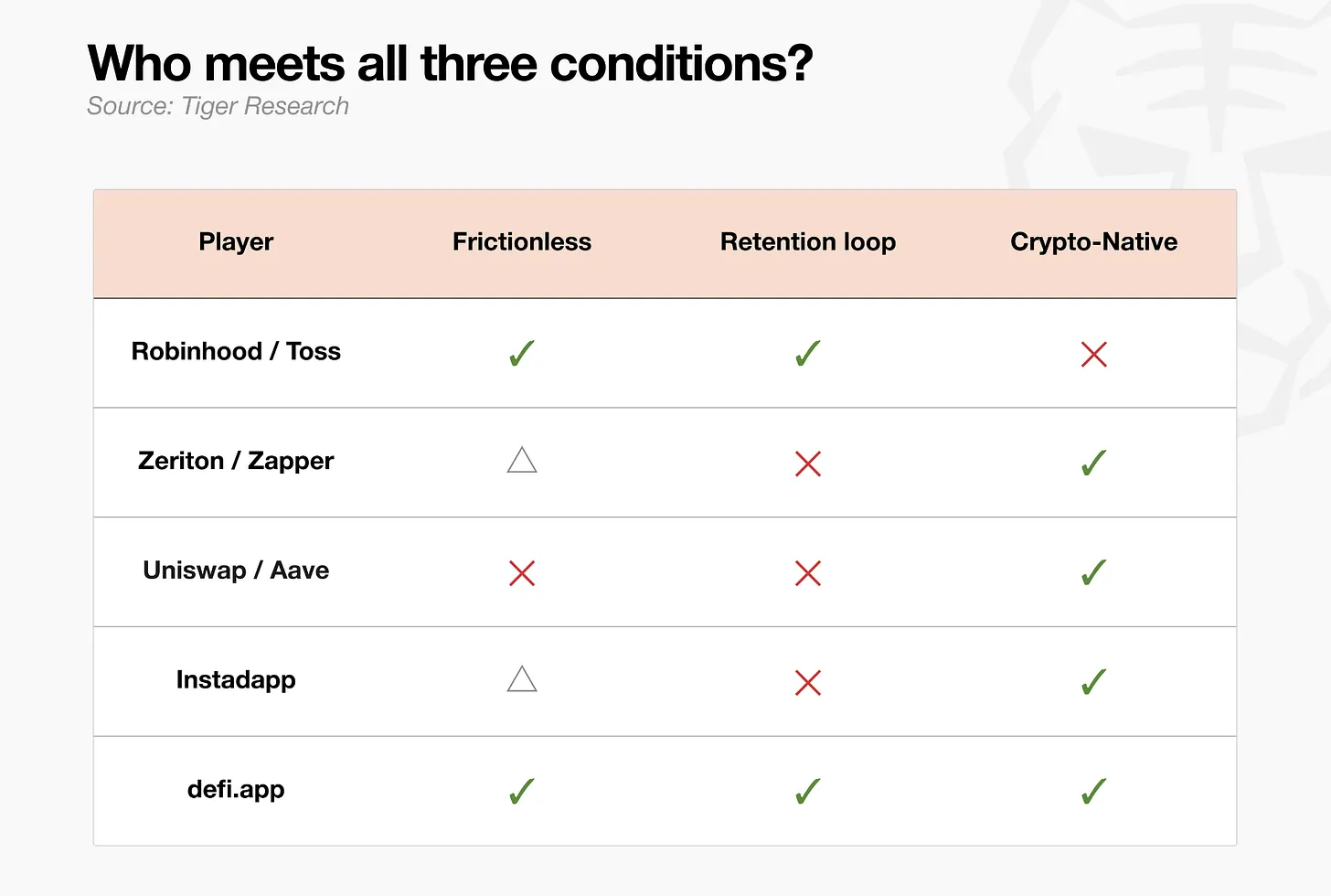

Zerion, Zapper, and Instadapp (Avocado) have all tried to lower the entry barriers of DeFi through aggregation dashboards and smart account technologies. The direction was correct, but the retention rates are disappointing.

There is only one root cause of failure: the absence of a lasting retention loop. Once token or point incentives end, users shift focus to the next reward cycle. The technical hurdles have been passed, but without incentives, users cannot be retained, which is far from the fintech industry's benchmark of a 9.2% D30 retention rate.

Reducing friction and cultivating a daily revisit habit are two different design problems. Robinhood retains users not just through zero commissions, but through push notifications, spending analytics, and daily rewards. These elements combined create a mechanism for users to want to return. Existing DeFi applications generally lack this product design capability.

Reflecting on these failures, to capture this market, platforms must simultaneously satisfy three conditions.

First, a frictionless entry: Users should not perceive the existence of cross-chain, Gas fees, and bridges. Second, a retention loop: Mechanisms must drive users to continue returning even after incentives exit. Third, complete support for self-custody and high-leverage products that regulated fintech cannot provide.

Platforms that achieve all three points will set the standard in this market.

3. The Path of defi.app: What the Data Shows

defi.app integrates swaps, yields, and perpetual contracts into a single interface. With the Gas abstraction based on EIP-4337 smart accounts, users need not manage Gas separately. Cross-ecosystem transactions between EVM and Solana are automatically routed to the optimal path through aggregators like 1inch and Jupiter. The core logic of the product is: financial functionalities are readily accessible, while the technical complexities of Web3 are hidden.

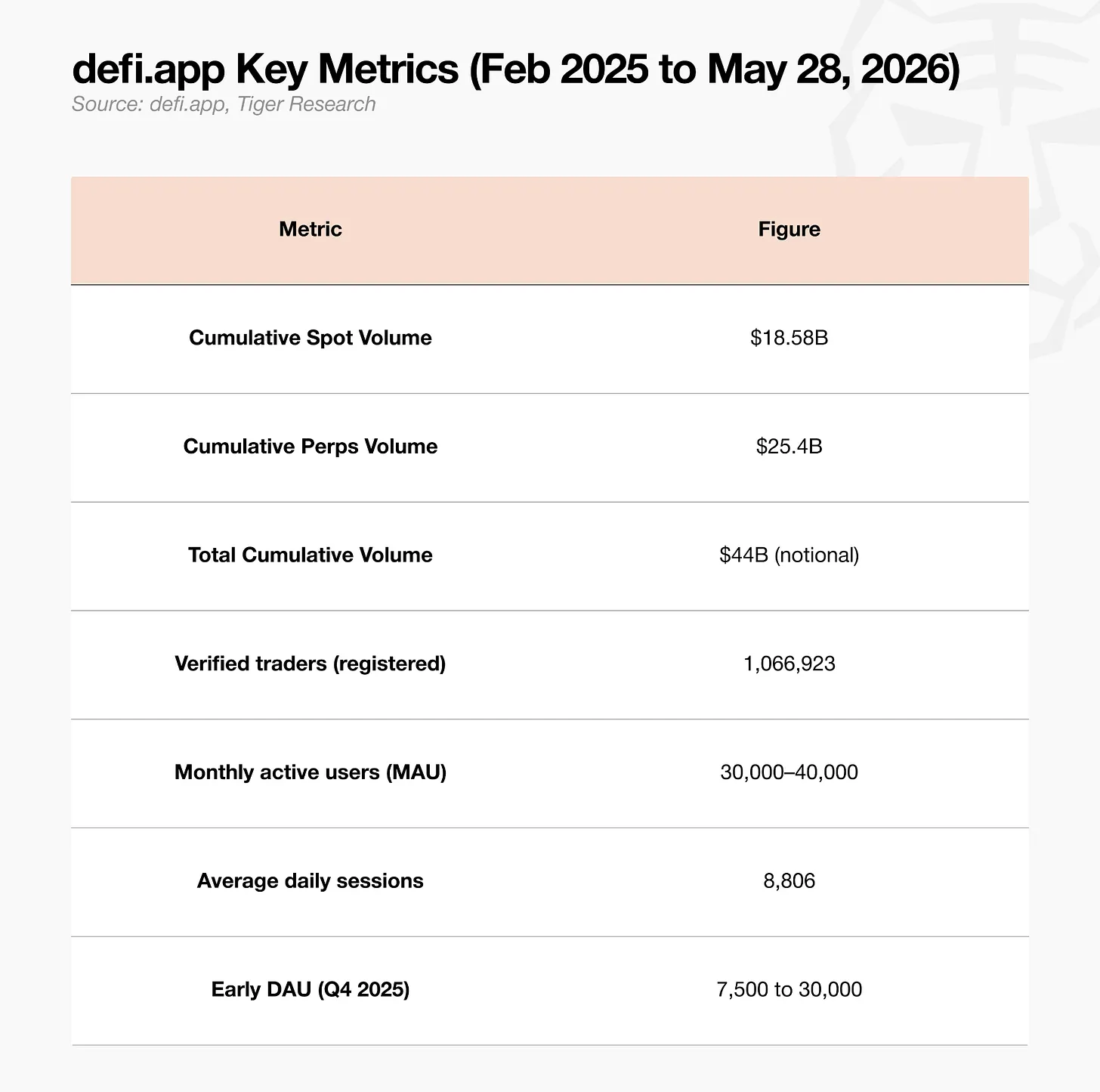

The core data since launch is as follows.

With 1.06 million registered users, it indicates that the user acquisition capabilities of defi.app are genuine. Monthly active users (MAU) have maintained between 30,000 to 40,000, while daily active users (DAU) have grown by about 3000% since launch. This means that before Rocket Perps officially goes live, the platform already has a substantial retention foundation. The current question is: how far can the official launch on June 4 push this foundation?

4. Rocket Perps: Linking Participation, Revenue, and Token Value

Previously, the focus of defi.app was on eliminating friction and constructing retention loops, but comparisons with traditional fintech performed shadowing. Many services were integrated, but the third condition—cryptonative coverage—remained unmet.

Rocket Perps is the answer provided by defi.app.

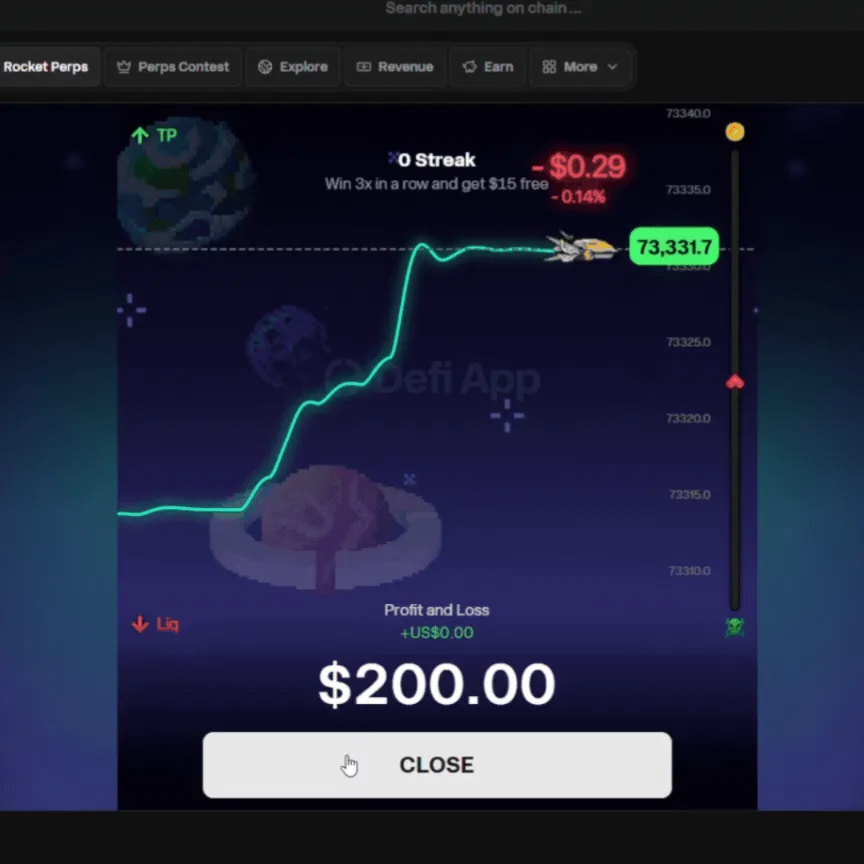

This is a perpetual contract product with a maximum leverage of 1000 times, wrapped in a pixel art arcade game style. Based on Aark Digital's oracle infrastructure, positions can be executed instantly without requiring counterparty matching. Players accumulate XP by clicking on flying asteroids, which can be redeemed for $HOME token rewards. The game mechanics are tied to trading behavior, driving users to return repeatedly.

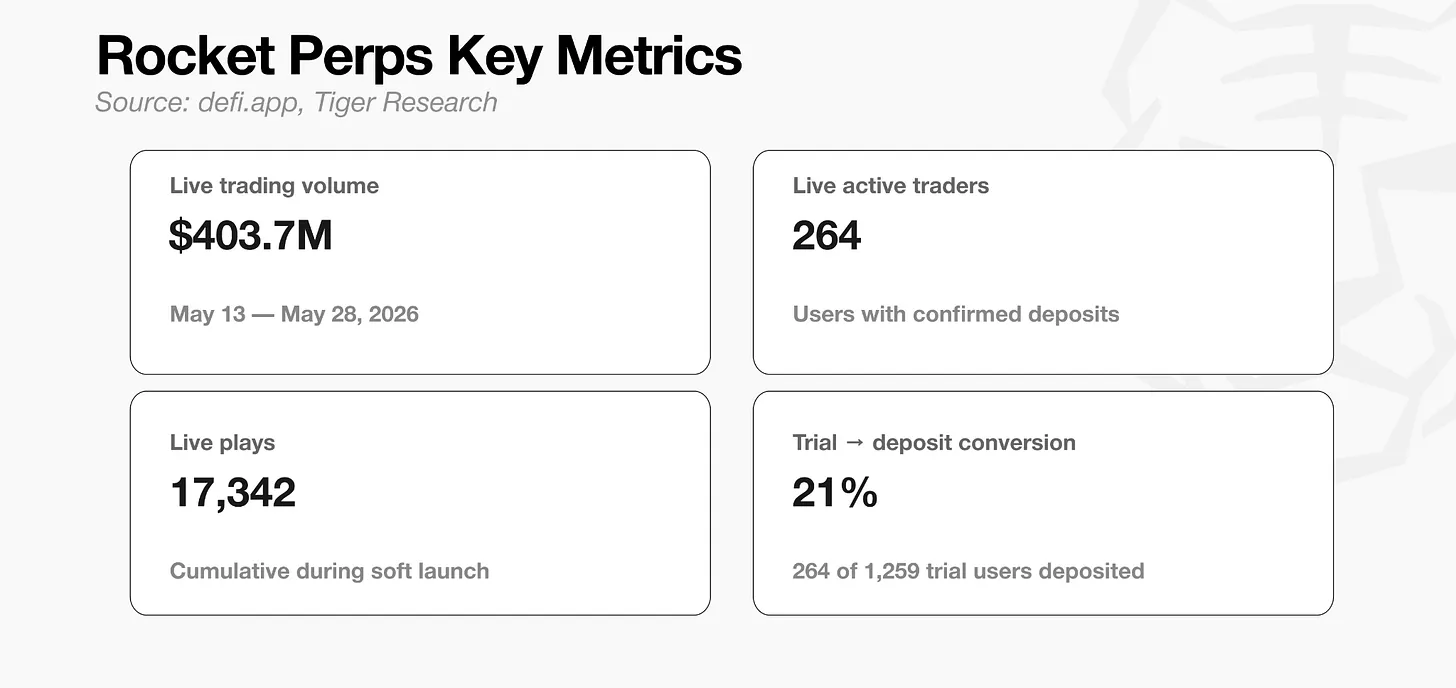

The data during the soft launch phase (from May 13 to May 28, 2026) is as follows.

Within two weeks, 264 users generated over $400 million in trading volume. High-leverage products inherently possess such capital density, and this group of users comprises early adopters with a very high risk tolerance. Whether scalability can be achieved during the public phase still needs to be verified.

While 1000x leverage may seem aggressive at first glance, it precisely hits the psychological profile of crypto market participants. This group notably features a willingness to exchange high risk for high returns. Rocket Perps transforms this preference into a product, grounded in territories inaccessible to regulated fintech.

The fee structure deserves special mention. Opening a position incurs a 4% margin fee, while profitable closings are charged a tiered maximum of 50% of profits. Compared to the usual 0.02% to 0.07% fees of mainstream perpetual DEXs, the difference is stark. However, this is not a mistake; 80% of the platform's total income is injected into the $HOME buyback according to the DIP-004 governance proposal; the fee pricing is a proactive choice to serve ecological goals. For users treating it as a high-confidence trading tool rather than a hedging instrument, this premium is unlikely to be a barrier.

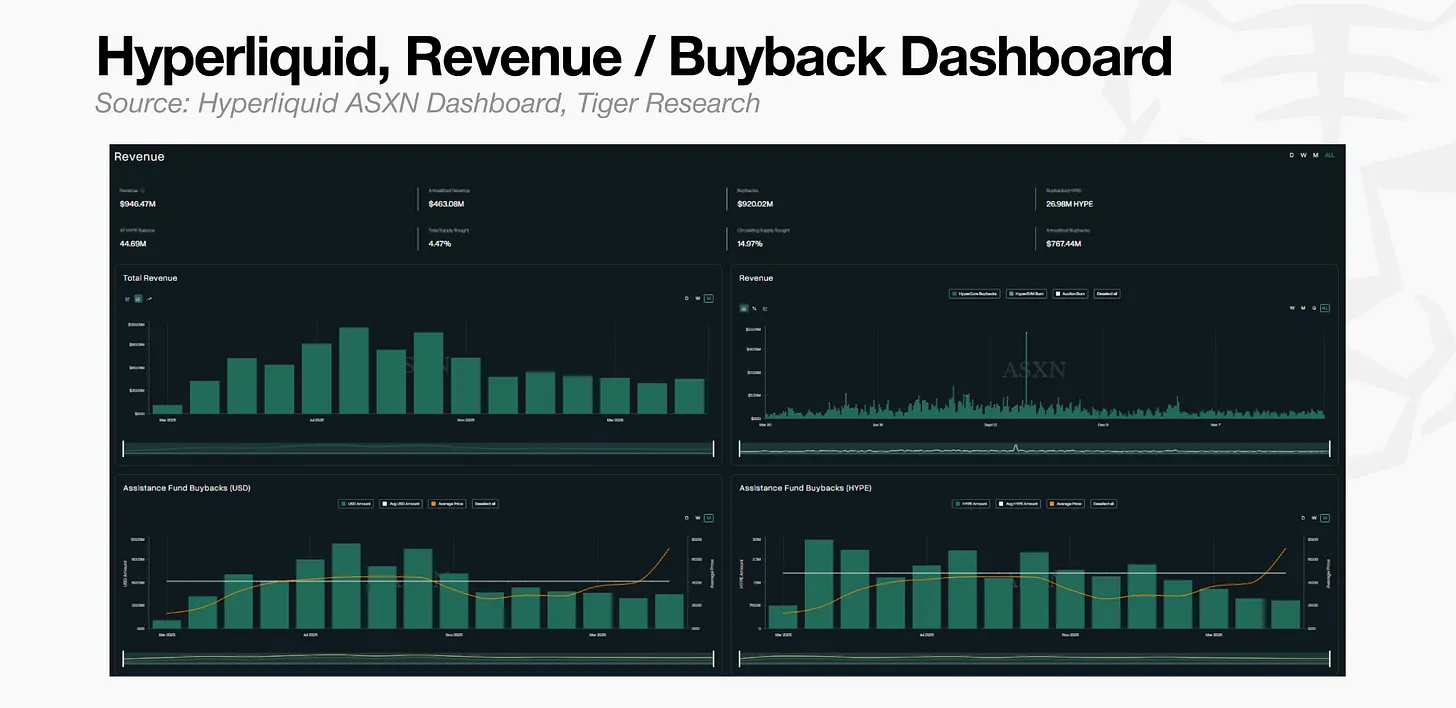

Hyperliquid is the clearest precedent of this logic. 97% of transaction fees are used for HYPE token buybacks, and each transaction is instantly verifiable on-chain, requiring no official statement; the data speaks for itself. If defi.app can present the same positive loop on-chain, the cost premium paid by users will be offset by the strong incentives to remain on the platform.

5. Challenges that defi.app Must Overcome

5.1 Retention Verification and Trust Building

The 264 users in the soft launch were high-risk traders who opted in. The public launch on June 4 will be the first real test of retention capabilities for average users. Whether the current 30,000 to 40,000 MAUs can achieve meaningful expansion from this foundation is the core question.

Robinhood faced a similar dilemma in its early days. After the meme stock frenzy subsided in 2021, MAUs saw a sharp decline from their peak. The response was to introduce credit card, banking services, and social features, giving users reasons to open the app even on non-trading days. The conclusion is that regardless of market conditions, retaining users requires independent daily usage scenarios.

defi.app faces the same question. Continuously launching features that resonate with the intuitions of cryptonative traders can attract users, but keeping them requires making the platform a "worthwhile investment" place. Both aspects must progress simultaneously. Only when retained users make defi.app a part of their daily asset management will the platform truly become a comprehensive application.

5.2 On-Chain Transparency of Buybacks

For today's investors assessing the value of $HOME, the most persuasive point is that 80% of the platform's total revenue will be directed toward the governance-approved buyback plan. However, crypto investors have been hurt by similar promises before and have a very low tolerance. Even a minor discrepancy between promises and actual on-chain execution can erode trust faster than anticipated.

Hyperliquid's solution is the cleanest. As soon as transaction fees are generated, buybacks are executed automatically and verifiable on-chain, requiring no further explanation.

The commitment of 80% from defi.app is powerful enough on its own. If they can publish the buyback execution wallet address simultaneously with the public launch of Rocket Perps and launch a real-time income dashboard, it will have the foundation for replicating Hyperliquid's trust flywheel.

6. Conclusion

Robinhood changed the financial experience but has never crossed the regulatory boundary. Self-custody, high leverage, and unlicensed yields remain out of reach. DeFi has built a financial system beyond this boundary but struggles to retain users. The infrastructure is complete, yet the habitual loop of daily revisits is missing.

The goal of defi.app precisely falls into this gap: to create a user experience in the territory where Robinhood cannot enter that DeFi has yet to accomplish.

The path advances along three lines: eliminating friction through Gas and bridge abstraction; providing reasons for users to keep returning with features like Rocket Perps; and linking fee injections to the real platform use with the $HOME buyback plan.

The team at defi.app understands what brings users into the crypto market. For the volatility-embracing cryptonative users, Rocket Perps serves as a powerful entry point and a reason to return repeatedly. Beyond short-term user acquisition, the deeper question is: can the platform help users form the habit of opening the app daily—earning yields through Earn, accumulating XP through games, returning not just for incentives but because this app has become one of their ways to manage assets?

When this condition is met, defi.app will not just be another DeFi application. It will represent the first true market standard on the track where Robinhood cannot enter.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。