Author:RootData

Introduction

With the rise of on-chain perpetual DEXs like Hyperliquid and Aster, we also see a new phenomenon worth noting: more and more new projects first complete a round of liquidity accumulation on on-chain perpetual DEXs like Aster or Hyperliquid before launching perpetual contracts on centralized exchanges (CEXs). Whether on-chain perpetual DEXs are becoming a "pre-testing ground" for the market-making of new coins on CEXs has become a core topic of industry discussion.

This potential structural change has raised a series of questions: Is there an inherent correlation between the quality of on-chain liquidity and subsequent CEX positions (Open Interest, OI)? Do different types of projects exhibit differences in on-chain layout strategies? Has the participation logic and strategic focus of market makers thereby undergone a systematic shift?

This report combines derivative data from CoinGlass and asset data from RootData, attempting to answer the above questions from a data perspective, providing references for project parties, market makers, and exchanges.

1. OI Performance Comparison: On-Chain Pre-Listing vs Direct CEX Listing

This analysis is based on CoinGlass's OI data from January 1 to May 20, 2026, focusing on newly listed tokens within 2026. The research sample is divided into two categories: one category includes projects that first listed on the Aster platform and subsequently launched on Binance, while the other category includes projects that directly listed on Binance without prior listing on Aster, totaling 55 valid samples. To eliminate interference from extreme outliers, this analysis uses the median as the core statistical measure, and the OI data pertains to the derivative contracts linked to the tokens' listings on Binance, facilitating a comparison of market liquidity and capital attention differences between the two types of projects after they go live on a leading exchange.

First-Day Performance: Looking at the first-day performance on Binance, the median OI for the Aster then Binance group was $2.08 million, while the direct Binance group was $298,900, making the former 6.96 times the latter. This difference may reflect that projects with prior Aster listings tend to garner relatively higher initial capital attention upon their Binance launch; the exposure from the pre-listing platform might have helped accumulate a certain amount of early market enthusiasm and user base, leading to more favorable initial liquidity performance compared to those that launched directly.

Peak Capital: From the perspective of peak capital, the median OI for the Aster then Binance group reached $6.1619 million, while the direct Binance group was $1.5716 million, making the former 3.92 times the latter. This data comparison indicates that pre-listed projects have a relatively higher scale of funding backing in derivative markets, possibly due to the market recognition stemming from preliminary groundwork and initial selection of projects.

Short-Term Capital Retention: In terms of short-term capital retention, the median OI for the Aster then Binance group within 7 days of launch was $3.239 million, while the direct Binance group was $785,200, making the former 4.13 times the latter. This suggests that the capital interest of projects with prior listings tends to have better sustainability within the first week of launch, whereas those that launch directly see a faster pace of decline in initial interest; this difference may relate to early user stickiness and the level of market consensus accumulation.

Long-Term Capital Resilience: Regarding long-term capital resilience, the median OI for the Aster then Binance group within 30 days of launch was $3.0734 million, while the direct Binance group was $894,700, making the former 3.44 times the latter. It can be seen that projects pre-listed on Aster have certain advantages in long-term capital consensus, as the decline in market enthusiasm is relatively slower, while projects listed directly are more likely to experience a rapid loss of capital interest.

Capital Growth Cycle: In terms of capital growth cycles, the median number of days from launch to peak for the Aster then Binance group was 27.00 days, while the direct Binance group was 5.50 days, making the former 4.91 times the latter. This difference indicates that projects that pre-list have relatively longer capital growth cycles, with a more gradual uplift in enthusiasm; direct listings tend to release capital interest in a concentrated manner, reaching peaks earlier and potentially experiencing greater short-term capital fluctuations, highlighting distinct performance characteristics in both models.

Overall, based on the median OI data from these 55 valid samples, within the observation period from January to May 2026, projects listed on Aster before launching on Binance outperformed those that directly listed on Binance in terms of initial scale, peak level, short-term retention, and long-term resilience of derivative OI. This on-chain perpetual DEX pre-listing strategy may have facilitated early market warming, user retention, and consensus accumulation, positively impacting subsequent capital performance on leading CEXs.

Note: This analysis is based solely on a single time frame and OI metrics, with limited samples and dimensions, and does not incorporate factors such as fundamentals, teams, and market environment. The conclusion reflects only temporary characteristics and is not a definitive judgment, requiring further data for validation.

2. What Types of Projects Are More Likely to Adopt On-Chain Layouts?

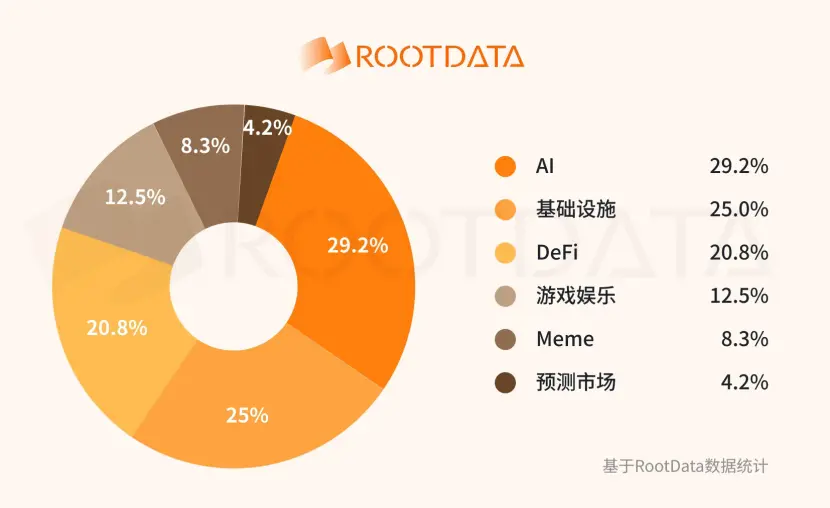

Based on RootData data, we compiled statistics on new coins in 2026 that first launched on the Aster chain before listing on any mainstream CEX. After excluding TradFi type tokens, we found that among this batch of projects that launched on on-chain perpetual DEXs, AI, infrastructure, and DeFi categories are the absolute core groups, collectively accounting for over 75%. Among them, AI projects account for nearly 30%, infrastructure types account for 25%, and DeFi types exceed 20%, establishing them as the mainstream preferred types for on-chain pre-listing projects.

Additionally, there are gaming, meme, and prediction market projects that have also opted for on-chain pre-listing layouts. These projects are all native blockchain paths, with their core value and development logic closely tied to the on-chain ecosystem. In the early stages, there is often a necessity for contract testing, functional validation, community cold starting, and low-cost trial and error; the on-chain environments like Aster precisely match these needs, making it a standard pre-listing path before entering mainstream CEX.

3. Why Is the Main Battlefield for Market Making Shifting?

The on-chain perpetual DEX market is gradually evolving from being a "complementary trading venue" to an "pre-heating layer" and "testing ground" for new coins before entering mainstream markets. This shift is not an incidental phenomenon brought about by the rise of a single platform, but rather the result of the collaboration between exchange risk control, market maker behavior, and the maturity of on-chain markets.

On one hand, CEX risk control continues to tighten, raising the threshold for new coins to directly enter the contract market. In March 2026, Binance explicitly prohibited profit-sharing and guaranteed yield agreements for market makers, requiring projects to fully disclose the identity of market makers and contract terms, while establishing a mechanism for a black list of violations. Subsequently, Bitget launched a "Market Integrity and Token Accountability Framework" in May 2026, focusing on monitoring irregular transactions, on-chain data, and position concentration, granting the platform authority to suspend trading and enforce delistings; HTX implemented a market maker elimination system beginning in June 2026, degrading or eliminating underperforming market makers through monthly quantitative assessments. This indicates that projects lacking real liquidity validation are naturally at a disadvantage within the risk control evaluation systems of CEXs. Compared to directly bearing the risks of being listed, exchanges prefer to first observe the actual trading activity, position structure, and price stability of projects within on-chain markets.

Market makers are also actively migrating on-chain, changing the "first battlefield" for new coin liquidity. According to Kaiko's monitoring, liquidity reserves of market makers on CEXs declined by 47% year-on-year in Q3 2025; TradingView data shows that in the first nine months of 2025, the average daily order amount of the top ten market makers on CEXs decreased by approximately $6.2 billion. Among them, leading market-making institutions like Jump and Wintermute transferred over 30% of their liquidity to on-chain derivative platforms like Hyperliquid and Aevo. This means that market makers no longer see CEXs as the starting point for deploying new coin liquidity, but are more inclined to conduct trial trading, accumulation, and initial pricing on-chain before spreading to centralized markets.

Moreover, more importantly, on-chain perpetual DEXs have already grown to a market scale capable of assuming this role. According to CoinGlass data, in April 2026, Hyperliquid's open interest (OI) market share was approximately 6.8%, ranking seventh in the global perpetual contract market, surpassing some mainstream CEXs, and becoming the only decentralized derivative platform to enter the industry's top ten. When the trading depth, OI scale, and price discovery capability of on-chain perpetual DEXs are approaching those of some second-tier CEXs, they no longer serve merely as retail speculation markets but begin to be recognized as liquidity "pre-certification" venues by projects, market makers, and exchanges alike.

Conclusion and Outlook

Based on the analysis of samples from January to May 2026, new coins that completed liquidity accumulation on on-chain perpetual DEXs like Aster before launching on mainstream CEXs exhibited significantly better OI performance on the first day, first week, and throughout the entire period compared to projects that launched directly on CEXs. The amplification of enthusiasm and advantages of capital retention brought by on-chain pre-listing are particularly prominent.

These projects that initially launched on on-chain perpetual DEXs predominantly belong to native blockchain sectors such as AI, infrastructure, and DeFi, fitting their core needs for early contract testing, community cold starts, and low-cost trial and error. Concurrently, tightening CEX risk controls, the migration of market makers to on-chain, and the maturity of on-chain DEXs collectively propel on-chain pre-listing to become an important reference path within the industry.

Looking ahead to the second half of 2026, the influence of on-chain perpetual DEXs within the new coin issuance ecosystem is likely to continue to strengthen, and on-chain warming may become a standard choice for more new coins, further reshaping the issuance pathway from chain to CEX.

The synergistic value of CoinGlass derivative data and RootData asset tagging will also provide more comprehensive decision-making references for project parties, exchanges, and market makers, promoting on-chain data to become an important basis for coin assessment and market-making strategies. Overall, the linkage between on-chain and CEXs will grow increasingly closer, though the industry landscape will still have the potential for diverse changes, necessitating continuous monitoring and validation with a broader range of samples.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。