The median margin of liquidated positions was only $31, with 3x leverage, almost entirely consisting of retail investors.

Written by: ChandlerZ, Foresight News

On the evening of May 28, the SPACEX - USDH perpetual contract on Hyperliquid experienced a severe flash crash, with its price plummeting from $2277 to a low of $1254 within 30 minutes, a drop of nearly 45%, before rebounding to around $2169.

This crash led to the liquidation of 405 users and 1393 positions, with a total liquidation amount of $1.51 million.

Data shows that the total trading volume of this contract in the past 24 hours was only approximately $4.87 million, with less than $2.9 million in open interest, indicating extremely low market depth. A large sell order nearly directly pierced through liquidity, triggering a cascading drop. The liquidated users were primarily retail investors, with a median margin of only about $31 and commonly using approximately 3x leverage.

The Hyperliquid ecosystem perpetual contract platform Ventuals later responded on Twitter, stating that the team had noticed the flash crash event in the SPACEX market. The cause of the incident was that a data provider for off-chain data, one of the oracle price components, returned erroneous data, causing significant fluctuations in the oracle price and the mark price of the market, which in turn triggered forced liquidation for some users. The team has since taken measures to prevent similar situations from occurring again. Additionally, they are assessing the impact of this event on affected users to develop an appropriate compensation plan. Affected users will receive compensation within the next 48 hours.

A Fragile Pricing Chain

SPACEX - USDH is a crypto perpetual contract named "SpaceX Valuation" launched by Hyperliquid, allowing users to bet on market valuation changes before SpaceX's IPO, but it does not represent real stock and does not confer any shareholder rights.

On Ventuals, 1 SPACEX represents a $1 billion valuation for SpaceX, meaning if the SPACEX price is $420.69, the market values SpaceX at $420.69 billion.

The core challenge of such contracts is how to price a privately-held company?

Ventuals' solution is to break down pricing into two parts, with one-third of the weight coming from off-chain private market data provider Notice, whose pricing model incorporates funding rounds, 409A valuations, mutual fund markings, secondary market transactions and quotes, as well as comparable publicly listed companies. Two-thirds of the weight comes from the contract's own marked price's exponentially weighted moving average over the past 2 hours. Notice data is polled at least once per minute, and the oracle price is updated every 3 seconds.

This design can ideally balance external information with on-chain price discovery, but it has a fatal single point of failure. If the data returned by Notice is inherently incorrect, then one-third of the external anchor becomes a force pulling the price in the wrong direction. The remaining two-thirds of the on-chain average can hedge this error when liquidity is sufficient, but with a daily trading volume of only $4.87 million for the SPACEX contract, the on-chain price itself is fragile. The combination of two weak components led to the flash crash of the price.

Zero Arbitrage, Fragmented Low Liquidity

The SPACEX flash crash exposed issues not only with Ventuals. The entire class of pre-IPO synthetic products faces the same predicament in its pricing mechanism, namely the absence of a unified spot market and no cross-platform arbitrage channel.

In traditional finance, price differences for the same stock on the NYSE and NASDAQ are nearly nonexistent because high-frequency market makers trade at millisecond levels. However, in the pre-IPO synthetic product market, such arbitrage is structurally impossible because each platform's contract is issued as an asset or derivative based on its own rules and cannot hedge across platforms.

SPACEX on Hyperliquid and SPCX on Binance track the same company, but there is no mechanism to ensure price consistency between them. As a result, each platform forms its own closed pricing pool, with liquidity dispersed across various disconnected venues, each much shallower than the overall pool. Ventuals' SPACEX has a daily trading volume of $4.87 million; if the existing liquidity on platforms were concentrated in one place, the depth would be entirely different, but fragmentation exposes every platform to risks of low liquidity.

The essence of pre-IPO synthetic products is that a group of people bets around a number without a publicly available price benchmark. Price discovery on each platform only reflects the consensus of that small group of traders on that platform, with no rigid connection to the true valuation of the company.

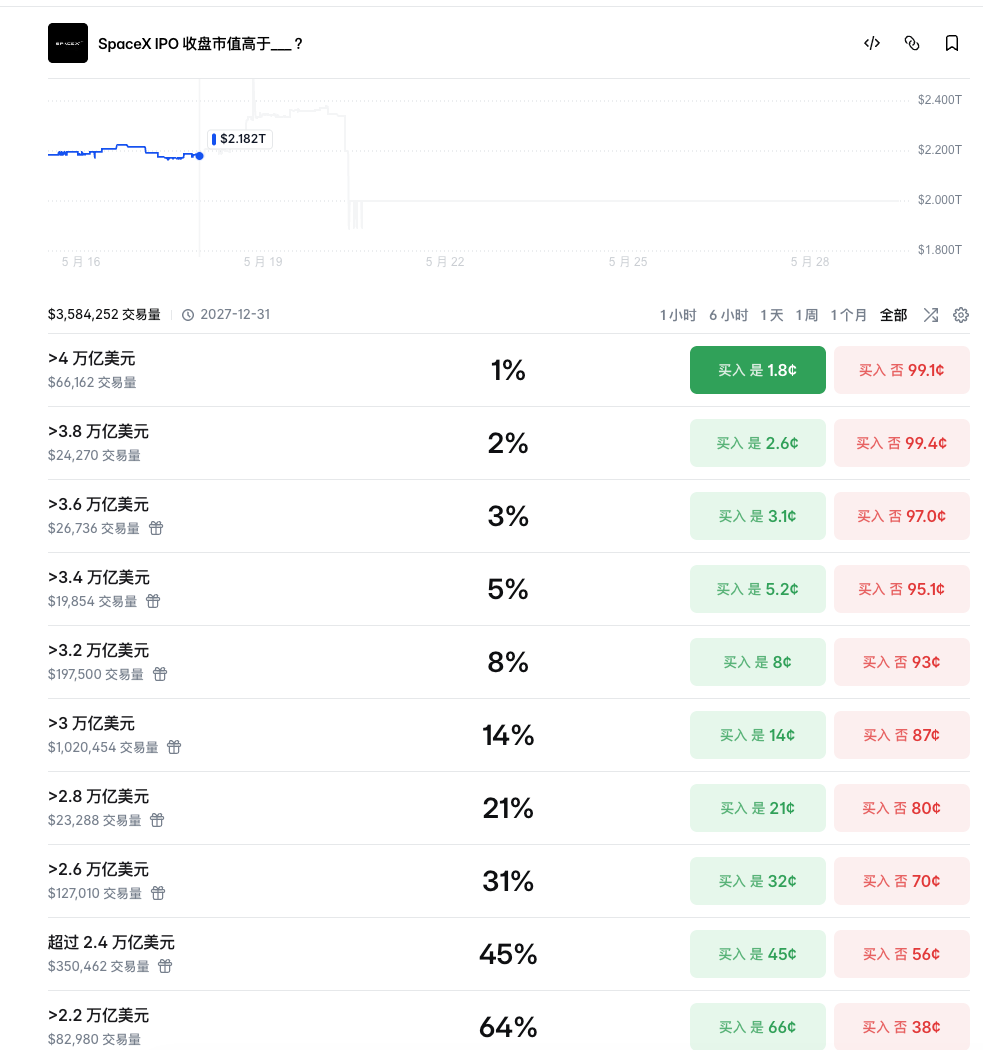

Sources of data similar to Notice come from private market information, which has low update frequency, narrow coverage, and lack of transparency. No one really knows how much SpaceX is worth, and the valuation distribution for SpaceX's IPO on Polymarket is similarly scattered, with a 45% probability in the range over $2.4 trillion and a 31% probability in the range over $2.6 trillion.

The Mystery Will Soon Be Revealed

On April 1, SpaceX submitted a confidential S-1 filing to the SEC, targeting a Nasdaq pricing on June 11 and trading to begin on June 12, with a valuation range of $1.75 trillion to $2 trillion.

The Ventuals documentation describes the settlement mechanism of the contracts: after the market opens on the first day of the IPO, the funding rate is set to zero, and the oracle price is locked to the mark price, while the valuation calculated based on real-time stock prices is introduced as an external price constraint. After the market closes, the mark price is overwritten to reflect the valuation based on the closing price, and all open positions are forcibly settled at that price.

This means that on the day of the IPO, all holders of SPACEX contracts will be settled at the real stock price. If there is a significant gap between the on-chain price and the Nasdaq pricing, the moment of settlement will be a large-scale one-way liquidation. Analysts estimate that the current gap is about 60%, and convergence is unlikely to occur smoothly because, prior to the IPO, there is no way to hedge the on-chain positions with SpaceX's real stock; the arbitrage mechanism is structurally broken. The convergence is likely to occur sharply in the last 72 hours.

This flash crash in prices resulted from an oracle data error, while the convergence on the day of the IPO will result from real price calibration, with the impact depending on the total scale of open positions across multiple platforms at that time. As SpaceX gets closer to the IPO, the inflow of speculative capital will increase, and fragmented liquidity and distorted pricing will simultaneously expand.

The user group with a median margin of $31 will not disappear; they will return, bringing more $31.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。