What exactly supports the valuation of 2 trillion?

Written by: Su Yang

Edited by: Xu Qingyang

On May 20 local time in the United States, SpaceX officially submitted its S-1 filing to the U.S. Securities and Exchange Commission (SEC), initiating the Nasdaq IPO process, with the stock code set as "SPCX." The company plans to raise $70 billion to $80 billion through this IPO, with a target valuation reaching $1.75 trillion to $2 trillion. It is expected to be listed on Nasdaq on June 12.

This is the largest IPO in human history and marks Musk's debut in the public market with absolute control. After the listing, he still holds 85.1% of the voting rights, while public shareholders have almost no voice.

As early as April 1 of this year, SpaceX had submitted an S-1 registration statement draft in a confidential manner to the SEC, internally codenamed "Project Apex," marking the first formal legal step in the IPO process.

According to the prospectus, investment bank Goldman Sachs leads the underwriting position, with Morgan Stanley, Bank of America, and 16 other underwriters acting as co-managers to jointly participate in this issuance.

This submission of the prospectus is also SpaceX's first public disclosure of its financial cards—Starlink is the cash cow, xAI is the money-burning black hole, and Musk has forcefully rewritten a space company into a "AI + aerospace" super narrative. So, what exactly supports the valuation of 2 trillion?

01 Starlink earns $11.4 billion annually, AI business loses $6.4 billion in a single quarter

SpaceX's financial data presents a "stark contrast" scenario.

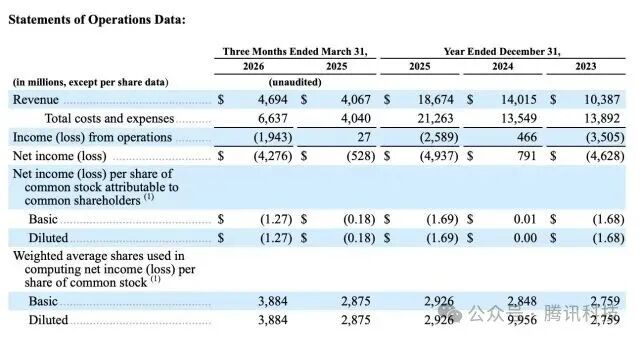

Key financial data of SpaceX

For the entire year of 2025, SpaceX achieved consolidated revenue of $18.67 billion and adjusted EBITDA of $6.584 billion, but the operating loss reached $2.589 billion, with a net loss nearing $4.94 billion. Nearly all losses came from the AI business—xAI lost $6.4 billion in 2025, while Starlink contributed $4.4 billion in operating profit during the same period. The money earned from the sky was all burned by the large models on the ground.

In the first quarter of 2026, the company generated revenue of $4.694 billion, with adjusted EBITDA of $1.127 billion and an operating loss of $1.943 billion.

Breaking down the business, the connectivity business, namely Starlink, contributed $3.26 billion, accounting for nearly 70% of revenue, making it the absolute powerhouse; AI business (xAI) revenue was $818 million; space operations (including rocket launches and government contracts) revenue was $619 million.

Core business financial data of SpaceX

From the balance sheet perspective, as of March 31, 2026, SpaceX held cash and cash equivalents of $15.9 billion, marketable securities of $7.8 billion, total assets of $102.1 billion, and total liabilities of $60.5 billion, of which debt and finance leases account for about $30.3 billion.

Even with billions in cash on hand, facing annual capital expenditures exceeding $20 billion, the company's cash flow pressure remains immense.

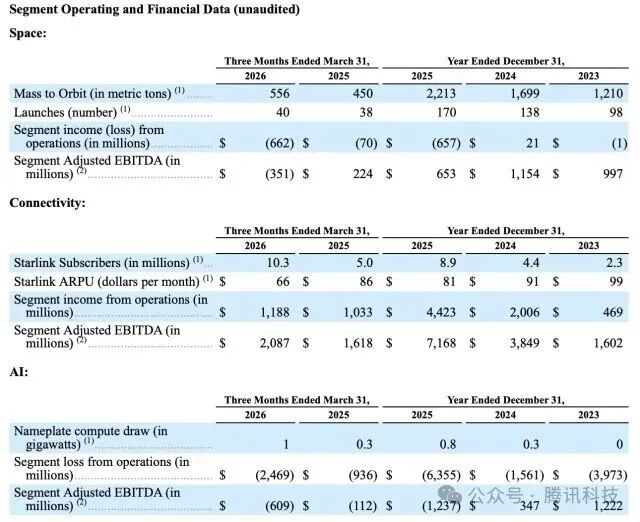

The operational data of Starlink is equally remarkable.

Highlights of SpaceX's space business

The prospectus shows that as of March 31, 2026, the number of Starlink users had reached 10.3 million, up from only 8.9 million at the end of 2025, with a net increase of 1.4 million users in one quarter. About 9,600 satellites are operating in orbit, with Starlink's adjusted EBITDA reaching $7.2 billion, an EBITDA profit margin as high as 63%, which is a 22 percentage point increase from 41% in 2023, with free cash flow around $3 billion, making it the only segment of SpaceX generating positive cash flow.

However, Starlink's average monthly revenue per user fell from $99 in 2023 to $81 in 2025, and then to $66 in the first quarter of 2026, a drop of over 30% in two and a half years.

This represents a typical logic of exchanging price for scale—SpaceX rapidly expanded user numbers through proactive price cuts, but the larger the scale, the more individual users' payment ability has declined. If ARPU continues to decline, to meet the market's expected long-term revenue targets, the growth rate of user scale must consistently outpace the decline in prices.

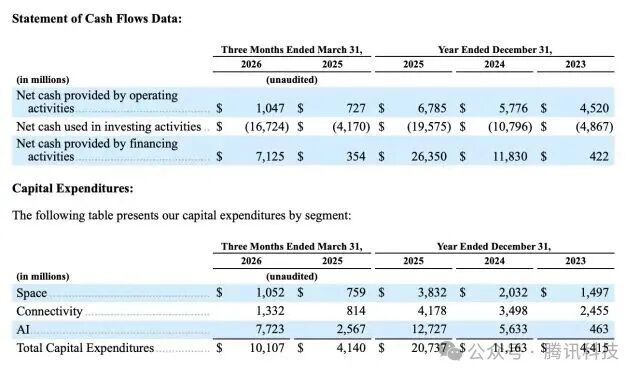

SpaceX's total capital expenditures in 2025 reached $20.7 billion, exceeding the total revenue for the year, of which the AI department's expenditure reached $12.7 billion, surpassing the total of aerospace and satellite businesses.

SpaceX's capital expenditures and cash flow

xAI burns about $1 billion on average each month, with an annual cash consumption of around $14 billion. For reference, OpenAI and Anthropic burned approximately $9 billion and $4 billion, respectively, in 2025, while SpaceX's AI segment alone exceeded the combined total of the two. Spending is aggressive, but in terms of revenue scale and growth, xAI is also far behind its two major competitors.

What's more concerning is the valuation multiples.

SpaceX's target valuation for this IPO is between $1.75 trillion to $2 trillion, which corresponds to about 266 times EBITDA. In comparison, Meta's valuation multiple is 16 times, Alphabet's is 25 times, Nvidia's is 36 times, and even Tesla, known for its high valuation, is only at 119 times.

SpaceX enters the public market with a valuation multiple more than twice that of Tesla, raising the first question of whether it is a case of value discovery or a narrative bubble, which will be the first test for the market post-listing.

The prospectus also clearly states: there are no plans to distribute dividends to Class A shareholders in the foreseeable future. This means investors can only bet on the stock price increase—this is purely a growth stock without a safety net.

02 85% voting rights: Musk's "one-man dynasty"

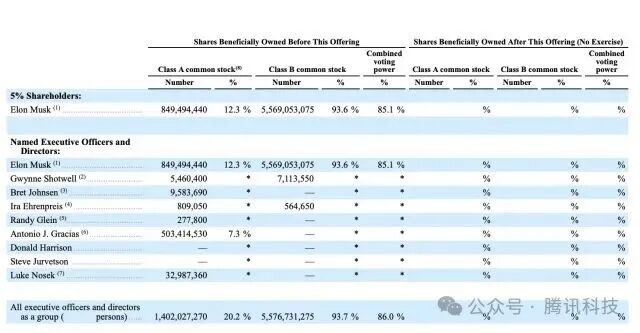

SpaceX employs a multi-class share structure. The company issues Class A common stock (1 vote per share) for public investors, while Class B common stock (10 votes per share) is held by Musk and insiders.

Shareholding status of management and directors

According to the data from the prospectus, Musk holds about 42.5% of SpaceX's equity, but with Class B super voting rights, he controls approximately 84% to 85.1% of the total voting power. This means that after the listing, regardless of how many shares public investors purchase, Musk alone can determine the composition of the board, major mergers, and even amend the company's articles of association.

The prospectus also discloses that Musk will continue to serve as CEO, CTO, and chairman of the board and has the authority to unilaterally dismiss or fill Class B director positions. SpaceX will also apply for a "controlled company" exemption, which frees it from the governance rule requiring a majority of independent directors.

Aside from Musk, the prospectus reveals that no other shareholders hold more than 5%. However, SpaceX's shareholder list still includes prominent institutions: Alphabet (the parent company of Google), as an early strategic investor, currently holds about 5%; Fidelity holds about 2%; Silicon Valley venture capital firms Valor Equity Partners, Founders Fund, Sequoia Capital, etc., collectively hold about 10% of the shares; and there are also appearances from hedge funds like D1 Capital, Darsana, and sovereign capital from the Middle East. SpaceX has also established a large-scale stock option pool for employees to incentivize its core tech team.

In Silicon Valley, multi-class share structures are quite common. According to a governance survey published by Fenwick in 2025, 27.3% of the top 150 technology companies in Silicon Valley still adopt multi-class share structures, a ratio far exceeding the 10.1% among S&P 100 constituents. However, companies design them differently.

But SpaceX has applied this control mechanism to an unprecedented degree—85% of the voting rights concentrated in one hand, making it extraordinarily prominent when facing other tech giants.

Looking back at Tesla, another publicly listed company owned by Musk, the situation is quite different. Tesla implements a "one share, one vote" principle without super voting rights, so Musk frequently faces challenges and questions from activist shareholders.

03 xAI merger: a "narrative engine" with a valuation of 2.5 trillion

COLOSSUS II facility in Memphis, Tennessee

In February of this year, SpaceX completed its acquisition of xAI with a total valuation of $1.25 trillion, of which xAI was valued at $250 billion. Before the merger, SpaceX's independent valuation was about $1 trillion, with the AI narrative adding about $250 billion in premium.

This transaction resulted in two immediate effects. One is revenue increment; in the first quarter of 2026, the AI business already contributed $818 million in revenue. The other is narrative enhancement—SpaceX transformed from a "space company" into a composite of "AI + aerospace."

Wall Street's valuation expectation for SpaceX has also been raised from $1.25 trillion all the way to between $1.75 trillion and $2 trillion.

The prospectus also discloses even crazier forward plans. SpaceX intends to deploy its first orbital AI computing modules before the end of this decade, operating AI computing facilities in space.

Highlights of xAI business

Musk's judgment is that producing AI computing power in space is cheaper than on Earth.

Meanwhile, SpaceX has also mentioned its "space mining" business for extracting metal resources from near-Earth asteroids. These plans currently have no revenue and not even technological prototypes, but they constitute some of the sexiest pages in the prospectus and also the parts with the greatest valuation disparities.

04 Terafab, Cursor acquisition, and financial business: Musk's "ecosystem revolution"

The prospectus also conceals several easily overlooked layouts.

Among them, SpaceX and Tesla jointly announced the Terafab project, aimed at integrating all stages of semiconductor production within the same system to produce two types of chips: one optimized for Tesla's fully autonomous driving system, Optimus humanoid robot, and Robotaxi fleet, and the other being high-power space chips resistant to radiation.

According to publicly available information, the total investment for the project can reach as high as $119 billion, employing Intel's 14A process, targeting to allocate 80% of computing power capacity to AI data centers in space.

Additionally, SpaceX plans to acquire Cursor post-IPO using Class A common stock as consideration, with the implied equity value of the transaction being $60 billion. SpaceX has secured exclusive rights to acquire Cursor at a $60 billion valuation, with the deal able to proceed 30 days after the IPO, and a breakup fee of up to $10 billion. Several core engineering team members from Cursor have previously joined xAI.

The company also plans to launch a financial product covering payment, banking, and other services, extending into the financial services sector.

The common feature of these businesses is that they are all in the early stages, require significant cash burn, and depend on SpaceX's financing capabilities and Musk's storytelling abilities.

05 Market divides: investment banks and skepticism coexist

The lineup of underwriters has seen an unexpected reversal, which in fact reflects the divisions on Wall Street.

Morgan Stanley, which has long closely collaborated with Musk, was edged out by Goldman Sachs from the top underwriting position, a result that surprised some market participants, given that Morgan Stanley previously led the IPOs for Tesla and the financing for Twitter’s acquisition.

Jay Ritter, a scholar at the University of Florida and the "Mr. IPO," clearly stated that if SpaceX's valuation reaches $2 trillion, he would choose to short the stock once it begins trading. Ritter further pointed out that new stocks with revenue exceeding $100 million after inflation adjustment and a price-to-sales ratio exceeding 40 times average significantly underperform the market in the three years following their IPO.

Greater concern stems from losses in the AI business—xAI lost $6.4 billion in 2025, while Starlink's $4.4 billion profit cannot fill this gap. If AI continues to burn money without commercial success, SpaceX's overall profitability pressure will sharply increase.

Analyst James Picariello from BNP Paribas stated that SpaceX's IPO will "divide" the base of retail investors supporting Musk, putting pressure on Tesla's stock price.

UBS analyst Joseph Spak, in earlier comments, reminded clients that big investments in hardware AI may just be the beginning. Meanwhile, questions have also arisen among some institutional investors about whether Musk can effectively manage his responsibilities across Tesla, SpaceX, xAI, X, and other companies.

06 Conclusion

June 12 will be a referendum to test the "Musk premium."

Starlink provides a solid cash cow, xAI offers a sexy narrative, and Musk provides absolute control. The good side is extremely high decision-making efficiency; the downside is the absence of brakes.

Goldman Sachs calls this IPO a once-in-a-lifetime opportunity, while some analysts compare it to buying a lottery ticket—the grand prize is Mars, and the consolation prize is Earth.

Cook handed Apple over to Ternus, a successor from a hardware engineering background, while Musk has no intention of handing SpaceX over to anyone—going public just means more passengers without voting rights, with only him remaining in the cockpit.

What can we say? It's very Musk.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。