$30 billion RWA assets, with only 9% circulating in DeFi.

Written by: Gino Matos

Translated by: Chopper, Foresight News

DeFiLlama data shows that the current on-chain tokenized real-world assets (RWA) scale has approached $30 billion, but only $2.47 billion is shown as the active value of locked funds in DeFi (TVL), which refers to the amount of funds actually deposited into third-party DeFi platform pools and participates in the ecosystem's operation.

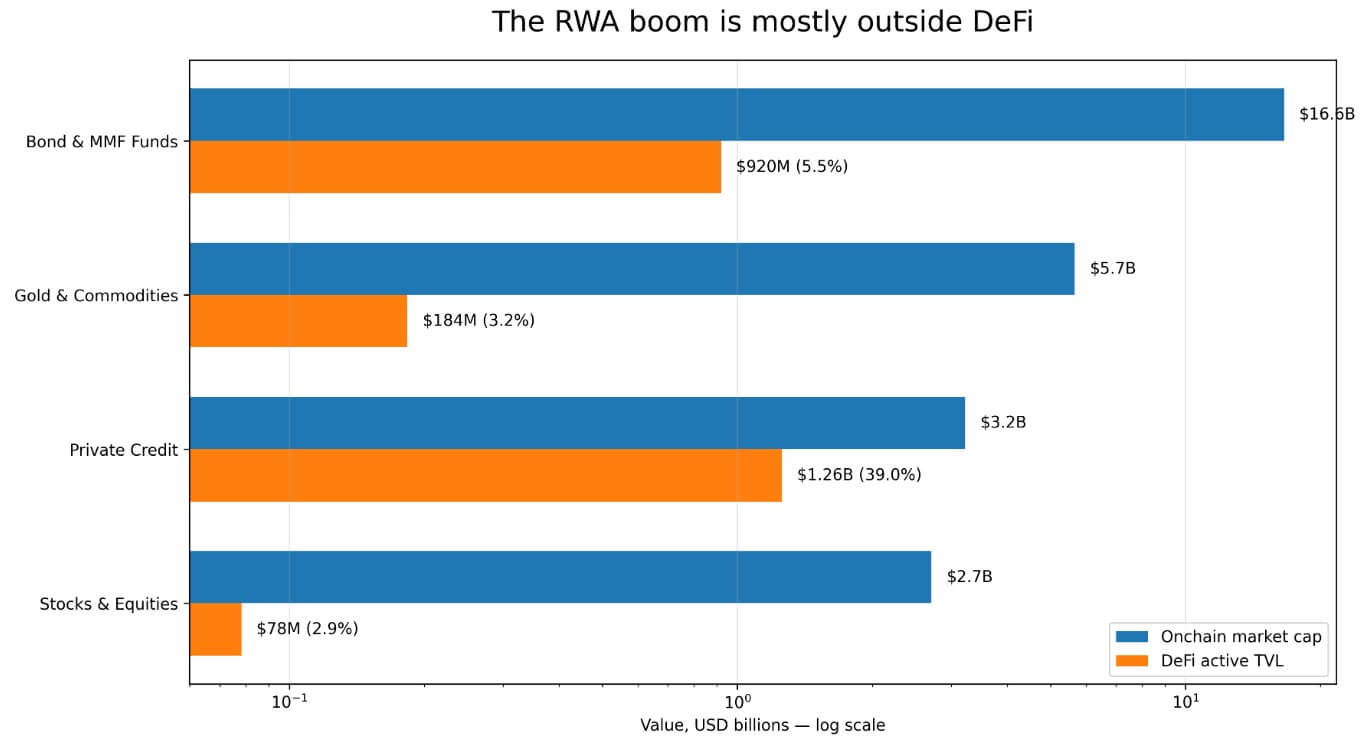

The vast majority of RWA assets remain outside scenarios such as lending markets and collateral vaults that can achieve free combinations and interactions of crypto assets. Bonds and money market funds are the largest category of RWA, with a total on-chain scale exceeding $16.6 billion, but the effective locked funds flowing into the DeFi ecosystem are only $920 million. Gold and commodities have an on-chain scale of $5.7 billion, with an effective circulation in DeFi of only $18.36 million; equity assets have an on-chain scale of $2.7 billion, with funds entering the DeFi market being only $7.827 million.

Only the private credit sector shows a bright performance: with an on-chain scale of $3.226 billion, the effective locked scale in DeFi is $1.257 billion, resulting in a penetration rate of 39%. The reason behind this is that projects like Maple Finance and Centrifuge positioned their products as lending financial tools from the design phase, naturally adapting to DeFi application scenarios.

In contrast, tokenized products like U.S. Treasury funds, gold assets, and equity assets are designed more to serve institutional holding needs from the issuance stage, and the overall architecture fits traditional compliant fund operation models.

The distribution of on-chain market capitalization and active DeFi TVL across four RWA categories

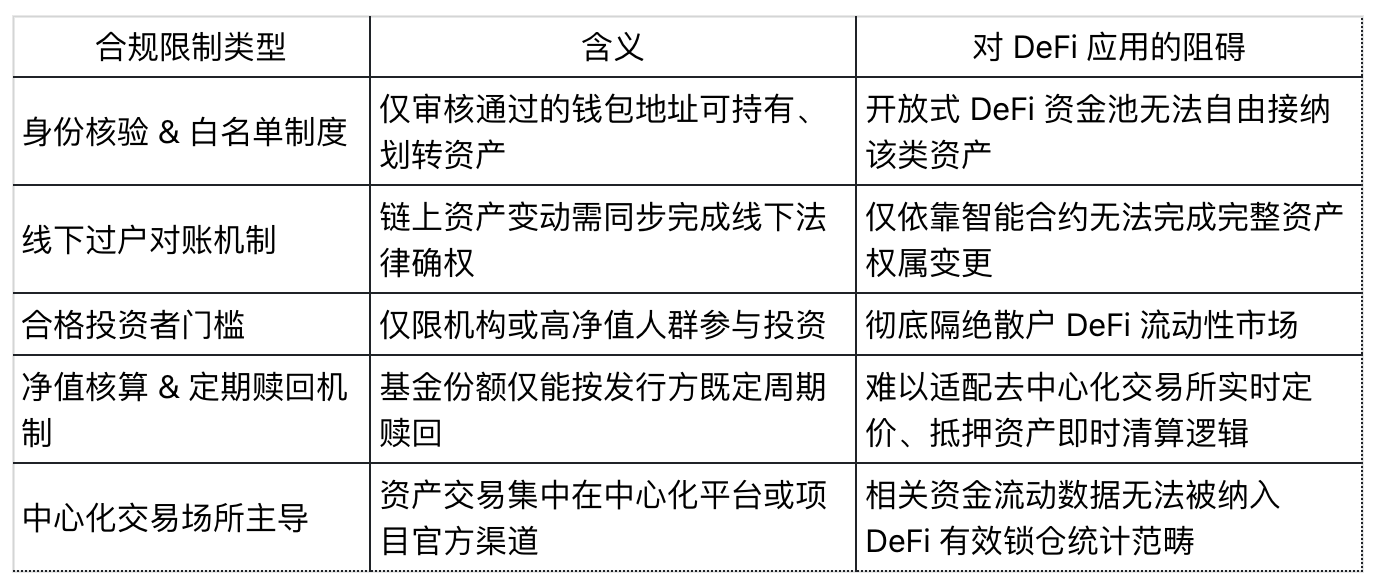

Licensing structure becomes the biggest barrier to DeFi composability

DeFiLlama classifies BlackRock's money market fund product BUIDL as a licensed fund, with an effective locked scale in the DeFi ecosystem of only $18.9 million.

The International Organization of Securities Commissions (IOSCO) pointed out in its final report on financial asset tokenization published in November 2025 that BUIDL has created a permissioned system on public blockchains for issuance, custody, secondary transactions between qualified investors, dividend distribution, and redemption.

Potential investors must pass a whitelist review through the Securitize platform, and the on-chain asset transfer actions must be completed with information verification by offline transfer registration institutions to have complete legal effect.

This also means that BUIDL essentially relies on a compliant holding infrastructure built on the underlying blockchain channels, focusing on custody of institutional assets and offline accounting reconciliation needs. Its smart contracts only support interactions with addresses within the whitelist; without the compliance wrapping layer for transit, it cannot be directly deposited into open DeFi protocols like Aave and Uniswap, which have no entry barriers.

In February 2026, BlackRock completed ecosystem collaboration between BUIDL and Uniswap, allowing part of the assets to enter the trading pool. However, the asset admission authority is still controlled by Securitize, limited to qualified institutional investors with a net asset value of no less than $5 million, and ordinary market participants still cannot get involved.

IOSCO found that the vast majority of tokenized money market funds on the market still adopt a similar operating model, and these assets have yet to realize the high liquidity value in the secondary market previously expected by the industry.

RedStone stated in its tokenization industry report released in March 2026 that the most challenging part of implementing asset tokenization is coordinating compliance reviews, identity verification, trading permission restrictions, risk control screening, and corporate rights distribution across different jurisdictions and public chain ecosystems. Looking at the current market, Morpho and Aave Horizon are among the few true cases that have unlocked the application of RWA assets in DeFi.

In short, every compliance access restriction set by project parties further raises the threshold for assets to enter the DeFi ecosystem. Tokenized products like U.S. Treasury tokens, money market funds, etc., are inherently designed to meet the regulatory requirements of licensed institutional investors, actively adding various permission constraints.

Gold and commodity assets also present another layer of reality. CoinGecko data shows that in the first quarter of 2026, the tokenized gold spot trading volume reached $90.7 billion, surpassing the total for 2025, but the vast majority of these trades occur on centralized exchanges. The previously mentioned $18.36 million effective locked scale in DeFi only represents a very small portion of the circulating volume within the ecosystem; the massive trading volume in centralized markets is completely outside DeFiLlama's data statistics.

Positive expectations: High-adaptation products have already set examples

At the beginning of 2026, the locked scale of USDY under Ondo exceeded $1 billion, now achieving full coverage across nine public chain ecosystems. Launched in September 2025, Ondo's global market segment focuses on tokenized U.S. stocks and ETF assets for overseas investors, supporting free asset transfers from the design stage, which can be directly used as collateral in DeFi; the corresponding asset locked scale has reached $650 million, with cumulative trading volume exceeding $12 billion.

According to RedStone statistics, RWA asset deposits on the Morpho platform exceed $620 million, while the related asset total on Aave Horizon reaches $423.5 million. Both lending protocols have successfully implemented mature applications for RWA collateral lending.

These successful cases fully demonstrate that as long as the asset issuance stage adheres to the design philosophy of free circulation without permissions, RWA assets can indeed achieve composability within the DeFi ecosystem.

DWF Labs, at an industry roundtable held in April 2026, in collaboration with projects like Centrifuge, Falcon Finance, and xStocks, jointly proposed the view that the RWA sector has already differentiated into two major development tracks: one prioritizing compliance with asset ownership and taking a strict licensed control route; the other balancing compliance issuance standards while enabling secondary market circulation, with ecosystem composability as the core design direction.

Graham Nelson, the project lead of Centrifuge, stated that the stringent whitelist access mechanism means that each participant in the liquidity pool must complete individual qualification reviews, directly blocking the path for assets to enter open DeFi.

Meanwhile, the DeRWA solution launched by Centrifuge encompasses compliant wrapping of underlying primary issuance assets, while relaxing the restrictions on secondary market asset circulation to break down barriers. Artem Tolkachev from Falcon Finance also mentioned that ecosystem composability and flexible exit mechanisms are the key bridges connecting real-world assets with liquidity in the crypto market.

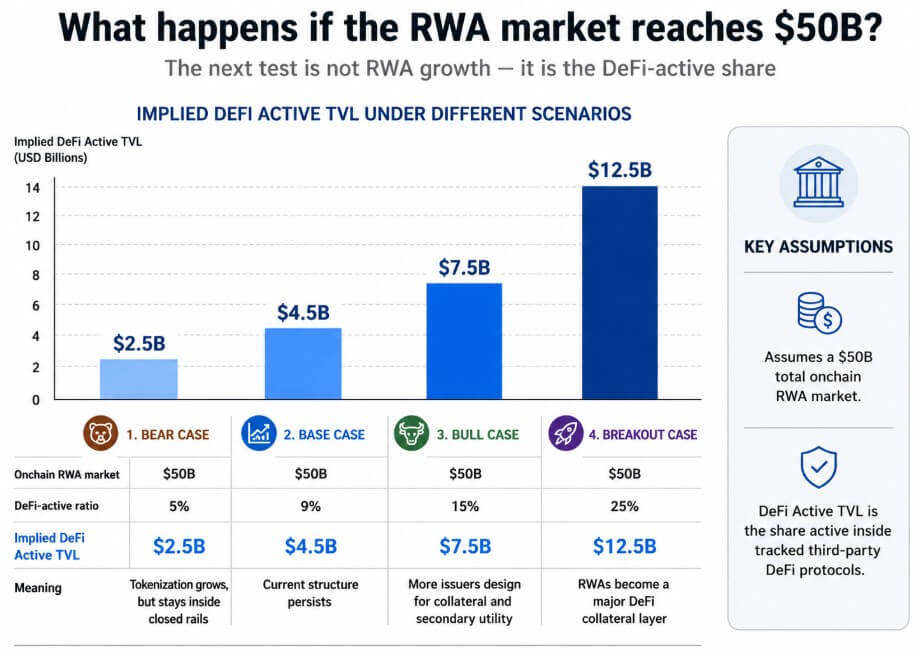

The industry holds an optimistic view that as the overall on-chain RWA asset scale approaches $50 billion, if most projects in the sector shift towards compatibility with DeFi design ideas, the penetration rate of RWA assets in the DeFi ecosystem may break through the current low level of 9%.

Negative realities: Industry growth may be trapped in the traditional financial system

Standard Chartered predicts that the global scale of tokenized assets will reach $2 trillion by 2028, but at the same time warns that this industry boom will likely be confined within the traditional banking financial system, with very limited growth dividends for the open crypto market.

IOSCO's survey in November 2025 also confirmed this point. Due to the entry barriers of distributed ledger technology itself and liquidity shortcomings, the current distribution and circulation of tokenized assets and secondary market trading still heavily rely on traditional financial infrastructure.

The European Central Bank further pointed out in its research report on the tokenization industry released in April 2026 that a unified industry standard for asset tokenization has not yet been formed globally, making it easy to produce isolated asset islands. Different asset systems have their own compliance rules, clearing underpinnings, and admission mechanisms, ultimately leading to liquidity being highly concentrated in closed circles, making it difficult to circulate.

The DeFi penetration rates for bonds and money market funds are only 5.5%, for gold commodities 3.2%, and for equity assets 2.9%, with these data sets intuitively confirming this ecological fragmentation pattern.

The vast majority of U.S. Treasury token and money fund products on the market generally set minimum investment thresholds, mandatory identity verification, offline asset reconciliation cycles, and fixed redemption window periods linked to asset net values, all of which directly conflict with the operation logic of decentralized exchanges that emphasize real-time pricing and no-threshold collateral vaults. These constraints are hard requirements from regulatory perspectives and are also an inevitable choice for asset issuers to actively adapt to compliant environments.

Two markets, one industry label

The total on-chain RWA scale of $30 billion, along with the $2.47 billion effective circulation scale in DeFi, seems to belong to the same RWA sector but actually corresponds to two completely separate markets:

- Compliant on-chain financial markets: primarily involving money market funds, U.S. Treasury funds, and institutional custody assets, where asset circulation relies on offline transfer institutions for confirmation and verification, fully complying with traditional financial regulatory rules;

- DeFi composable ecological markets: where assets can be freely deposited into lending protocols, act as no-threshold collateral, and connect to various automated financial yield strategies for free circulation.

The above figure predicts the implied values of active DeFi TVL in four scenarios within a $50 billion RWA market, ranging from 5% to 25%

With Morpho's over $620 million RWA deposits and USDY circulating across nine blockchains, the results are enough to prove that the second type of market possesses genuine development potential.

To drive the DeFi penetration rate of RWA assets beyond 9%, asset issuers must abandon the design ideas centered on compliance systems, like BlackRock's BUIDL, and instead adopt an underlying architecture that supports free circulation without thresholds.

Currently, $28.56 billion of on-chain RWA assets belong to the licensed control sector, which also means that the current tokenized real-world assets are overall more similar to compliant on-chain traditional financial products rather than general collateral assets that adapt to open DeFi ecosystems.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。