This month in South Korea, if you are neither an SK Hynix employee nor an SK Hynix shareholder, you are very likely a "suffering person".

Following the release of the huge profits in the quarterly report, investment banks that thrive on excitement not only actively revised upward the profit forecasts for Hynix this year but also raised expectations for year-end bonuses for Hynix employees. By applying the principle of allocating 10% of operating profit as a bonus pool, they calculated that this year’s average year-end dividend for employees could be several million RMB, while also putting the capitalists at Samsung near the fire of injustice.

After that, everything related to Hynix's IP received fervent support.

Hynix's work uniform became a priority pass in the South Korean dating market; real estate agents in the headquarters city of Icheon welcomed a dream-like quarter, with property volumes and prices rising along many areas along the Hynix commuter bus route; related China-South Korea semiconductor ETFs also surged to a 30% premium, frequently halting trading temporarily.

Even the Hong Kong stock market, which has long been criticized for its lack of technology content, saw a surge.

As of May 13, 2026, the South China East Ying SK Hynix daily 2x leveraged ETF (07709.HK) listed on the Hong Kong Stock Exchange has an asset scale nearing 60 billion HKD, surpassing the Tesla 2x leveraged ETF (TSLL.NASDAQ) that has long held the top spot in the US stock market and became the largest one-stock leveraged derivative product globally.

No matter how niche an investment product is, once the market rises to this extent, anyone just surfing the internet, even only watching some tech and digital bloggers' updates, can hardly escape seeing enthusiastic netizens posting—"Why don't you buy the 2x leveraged Hynix?"

Deadly Leverage

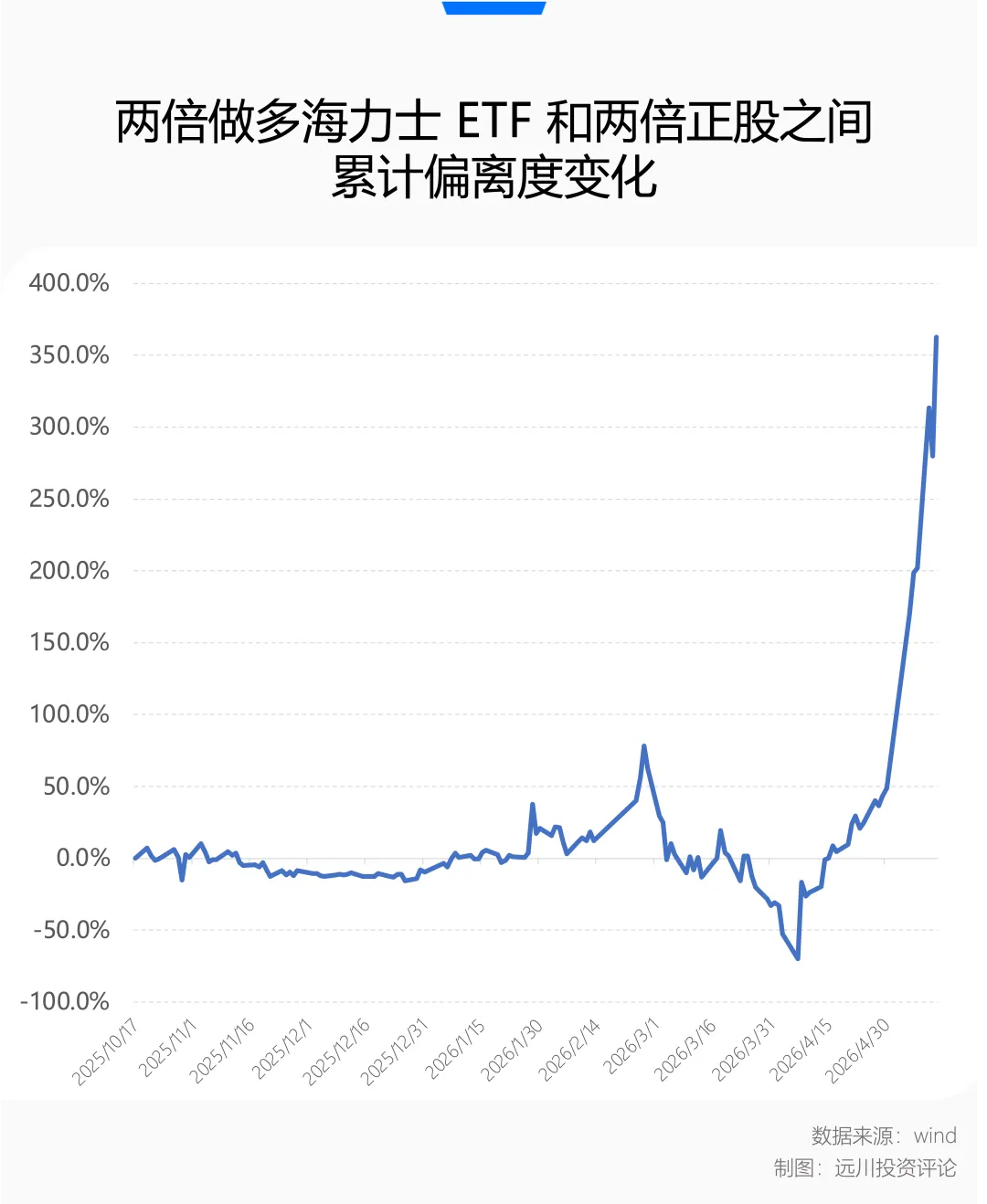

On October 16, 2025, when the 2x leveraged Hynix ETF was just listed on the Hong Kong Stock Exchange, its issuance scale was less than 5 billion HKD. If calculated based on the closing price on May 13, 2026, in just 7 months, the net value of this leveraged ETF product increased by 1011.58%, with its scale soaring more than 13 times.

The “first stock in hotel robotics,” Cloudwise Technology, which listed on the same day in Hong Kong, has made a steep climb with a market value that is still less than 4 times its IPO value.

You might say this demonstrates the terrifying efficiency of 2x leverage. The underlying stock of SK Hynix listed on the Korean market has accumulated an increase of "only" 324.49% from October 17 of last year to May 13 of this year; under the support of a unilateral main upward trend, this leveraged ETF's deviation even exceeded the theoretical twofold return by an excess return of 362%. Faced with such a violent monetary expansion, it seems more appropriate to describe it as "threefold leverage."

However, looking back at the past 7 months, this excess on paper is actually temporary.

Just two months ago, the Strait of Hormuz fell into a Schrödinger's blockade, and the global market plunged into panic due to the sudden interruption of oil and gas supply. Amid the abrupt swings and rapidly changing circumstances, the market did not see a traditional unilateral decline but fell into a state of schizophrenia in this atypical geopolitical conflict.

During the day, there were trades based on the logic of "three wars breaking out, supply chain disruptions," but in the evening, due to ambiguous statements from the White House press secretary, the market could quickly switch to a frenzy over "de-escalation of conflicts, returning to tech lines.” The ambiguity and uncertainty of this evolving path were amplified by the rapid dissemination on social media, translating to violent sell-offs in tech stocks within capital markets or frenzied buying on pullbacks.

While common sense tells us that wars will eventually end, the token consumption in the AI industry is also accelerating daily; however, when market volatility becomes too intense, the twists and turns cannot be overlooked.

More people began to feel the volatility loss of this leveraged ETF product at this time.

From the real trading data between March and April 2026, Hynix's stock price experienced significant downward volatility. The decline itself is problematic, but the multiple violent rebounds exceeding 10% along the way worsened the situation.

For the daily rebalancing 2x leveraged Hynix ETF, enduring unilateral declines might be bearable, but the true meat grinder is the high volatility downturn; at its worst, it fell over 50% more than the underlying stock.

Excluding other trading fees and management costs, the product's design of daily rebalancing implies that in a unilateral rising market, yesterday's profits automatically become today's "principal," allowing for continued doubling leveraged gains on that basis, yielding more excess positive returns. Conversely, if there's a unilateral plunge, the shrinking daily calculation base means the actual loss will also be less than the theoretical twofold.

However, once it enters a volatile market characterized by alternating rises and falls, the leveraged ETF reveals its ugly side.

The 2x leveraged Hynix ETF repeatedly undergoes “whipsawing”—after a significant increase yesterday, adjusting the positions right before a big drop today results in more losses, then adjusting again will cause more losses on the rebounding day due to the base being damaged.

The cyclic friction caused by alternating rises and falls can lead to a real net value retracement far exceeding twice the drop in the underlying stock, resulting in significant negative volatility loss, eating into investors' principal.

However, with the market now returning to the AI mainline, fervent capital is once again pouring in, leading to joy amidst unilateral surges.

As Hynix’s market value hits new highs repeatedly, when hundreds of billions in leveraged ETF products ignite frenzied trading, the market inevitably revisits the daily question: does this round of industrial revolution truly have no cycle?

Silicon-based Cycle Stocks

One point that must be acknowledged is that from the timing of its listing, the 2x leveraged Hynix ETF is indeed blessed with "one life, two fortunes, three feng shui".

For a considerable period prior, storage was not the absolute focus of the secondary market's bullish stance on the AI mainline. After all, since humanity boarded the express train to the information age in the 1990s, storage has often been a battlefield where many corpses lie after the flames of profit. The horror of cycles far outweighed the fantasy of growth.

Storage chips (especially traditional DRAM and NAND) are highly standardized commodities. The memory bars produced by various manufacturers have almost no differences in physical performance, except for the labels attached, making them the pork shares in silicon. The entire industry has long been caught in a brutal cyclical loop:

Shortage leads to price increases → Giants frantically expand production → Overcapacity → Price collapse → Losses lead to production cuts → Shortage again.

Each upward phase is topped with the super optimistic expectation of a "super cycle," and every downward phase is marked by brutal price wars and losses in the billions, resulting in many corpses.

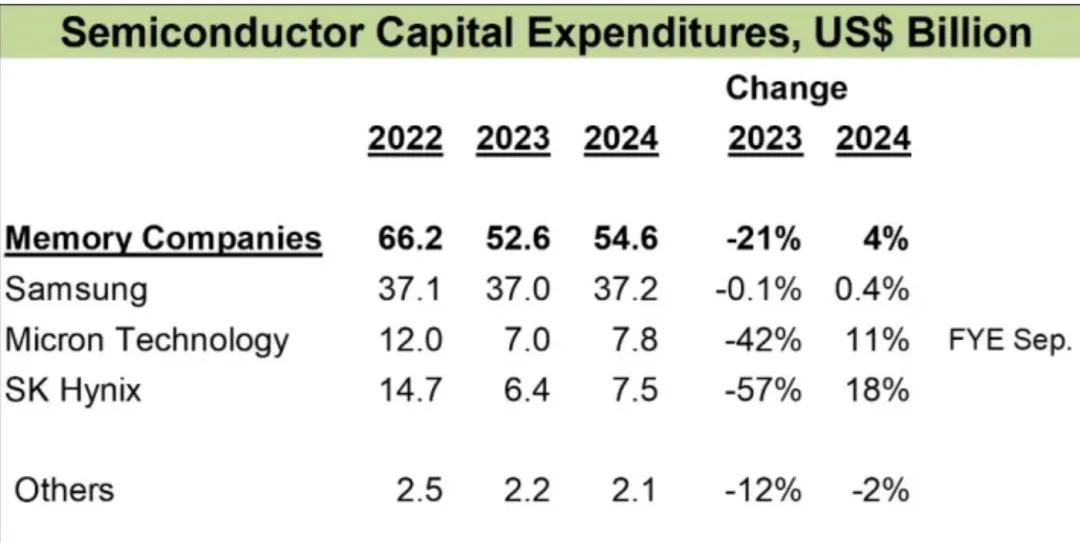

After experiencing the most severe semiconductor winter from 2022 to 2023, the surviving three storage giants—Micron, Samsung, and Hynix have tacitly agreed to cut capital expenditures, no longer maliciously expanding production and harming each other.

Image source: IC Insights

Then the AI narrative appeared, reenacting shortages and price hikes, effectively turning everyone’s operation into a money-printing machine.

Especially since the second half of last year, the competitive focus on the AI industry side has shifted from "training" to "inference," moving the demand focus from "computing power" to "storage capacity" while the supply bottlenecks shifted from bandwidth to capacity, making the widespread shortage of storage the hottest trading narrative.

At this point, if anyone still mentions, "Wasn't it said that the endpoint of AI is power?" they are likely to have missed the boat.

After the third quarter of 2025, the news from the AI industry has almost all been about the shortage of storage chips; one moment it's the giants announcing HBM orders backlog to beyond 2027, and the next, informing customers that DDR5 is also in short supply, so sorry, we are raising prices across the board for both high-end and low-end products.

As a major supplier of NVIDIA's HBM, Hynix has gained immense first-mover advantage and market share, and the timely launch of the 2x leveraged Hynix ETF has seamlessly coincided with memory prices rising above gold, with one box being able to exchange for a set of houses in Shanghai during the good times.

So, can hopping on the AI express make one escape the gravitational pull of cycles? The key isn’t to reach conclusions now but to find where changes might occur.

Hynix has established a dominant position under the barriers of HBM yield, achieving a historical peak gross profit margin of about 79% in Q1 2026, even surpassing NVIDIA's profitability during the same period.

Human nature tells us that extreme excess profits will inevitably attract a surge of production capacity expansion desires. The tacit agreement among storage giants to "cut production" seems untrustworthy in the face of absolute windfall profits.

Thus, whether Samsung or Micron will achieve breakthroughs in yield that could discount the narrative of HBM scarcity and widen the divergences between bulls and bears, leading to sector volatility, is a variable that needs continuous tracking.

In addition to changes on the supply side, the debates on the demand side have not entirely dissipated due to the accelerated popularization of agents or the increase in token consumption.

Ultimately, Hynix’s frenzy is built on NVIDIA’s frenzy; and NVIDIA’s frenzy is grounded in the downstream giants' annual capital expenditures in AI in the hundreds of billions of dollars.

The marginal changes in Capex remain the greatest attraction in the secondary market, embodying all anxieties and pride surrounding AI.

Conclusion

Whether to buy or not to buy the 2x leveraged Hynix ETF, it will inevitably become a subtle footnote for us when we look back on this history in the future.

In this era, bulls and bears often refer to two things—the bulls in AI industry faith, and the bears in macro geopolitical concerns.

People habitually turn to historical books, trying to find parallels in the internet frenzy of the millennium or even earlier macro upheavals. But every wave of technological revolution evolves differently, and what is “different” this time is the unprecedented speed of industrial revolution disruption.

AI is reshaping global productivity and production relations at an unprecedented acceleration. This extreme “speed” breaks the long penetration and fermentation processes present in traditional technology cycles. It does not give the market time to slowly digest valuations, nor does it grant the “old guard” any opportunity to take a moment to receive the flood of liquidity.

Whether it's industry giants or secondary market funds, they’re forced to complete their positioning and pricing within a very short time window, making the unit of stock price rises into multiples; hence, seasoned AI practitioners already assume that in this era, six months is already considered long-term.

However, the storm in the Strait of Hormuz has placed this round of technological revolution under the commonality of all past technology cycles: industry determines the ending and return rate, while macro impacts the path and volatility—what caused the massive negative deviation of the 2x leveraged Hynix ETF was not the interruption of the AI process, but the extreme swings in global macro expectations during that month.

And the soft underbelly of the real world is not merely the 33 kilometers at the narrowest part of the Strait of Hormuz.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。