Citi stated that at a pace of approximately 3 to 4 months per cycle, it is more likely to see Gemini 3.2 or 3.5 at I/O, while there is also a possibility of Gemini 4.0, but the probability is relatively low.

Written by: Zhao Ying

Source: Wall Street View

The biggest suspense at Google I/O is not whether Gemini 4.0 will make an appearance, but whether Google can prove that Gemini is transforming model capabilities into revenue growth in search, advertising, shopping, and cloud business.

Google has two key events in the coming week, with Google I/O on May 19 focusing on products and models, and Google Marketing Live on May 21 more directly addressing advertising and commercialization. The market's focus is shifting from "what model is released" to "how AI capabilities can enter daily business processes."

According to a report from Citi Research's Ronald Josey on May 12, the Gemini model is still at the forefront, AI tools are driving global query growth, UCP is transforming business, and Google Cloud's backlog has nearly doubled to $462 billion quarter over quarter. Citi maintains a "buy" rating on Alphabet with a target price of $447.

This means that any model updates at I/O are only the first layer of signals. What truly affects valuation is whether AI search can expand commercial queries, whether AI Max can become the new default tool for advertising budgets, whether agent-based shopping can connect transaction links, and whether the cloud business can continue to benefit from Gemini, TPU, and enterprise AI demand.

Gemini 4.0 is possible, but not the only focus

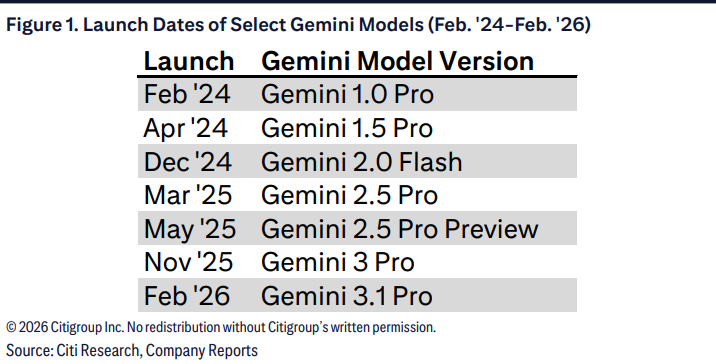

In terms of release pace, Gemini 4.0 is not impossible. Over the past two years, Google has successively launched Gemini 1.0 Pro, 1.5 Pro, 2.0 Flash, 2.5 Pro, 3 Pro, and 3.1 Pro, with Gemini 3.1 Pro being released in February 2026. At a rhythm of approximately every 3 to 4 months, it is more likely to see Gemini 3.2 or 3.5 at I/O, while there is also a possibility of Gemini 4.0, but the probability is relatively low.

For investors, the model number itself is not a decisive factor. What is more important is whether the Gemini ecosystem continues to expand, including Genie 3, Gemma 4, Gemini Robotics ER-1.6, and the path of Gemini entering more core services after Gmail and Maps.

Google may also update Gemini Health, Android XR smart glasses, and travel scenario integrations around services like Google Canvas. If these products can form a unified entry point, it will strengthen Gemini's role as an operational layer, rather than just a chat or generative tool.

As of the end of the first quarter of 2026, Google product suite subscription users reached 350 million. The next thing to observe is whether the expansion of Gemini functions will drive subscription revenue or serve more for advertising monetization. If AI search enhances the experience but weakens ad display, market reaction may be limited; if it allows more queries to have commercial intent, the growth space for the advertising business will be reassessed.

The key to AI search is turning queries into actionable intent

Search remains the core of Google's valuation. The most noteworthy change at I/O will be how AI-O, AI-M, and the Gemini search experience are integrated, as well as Chrome's role within this framework.

Google's management mentioned in the first quarter earnings call that longer and more complex queries from AI-O, AI-M, and Gemini provide more intent-based data. This directly relates to ad value. Users are now inputting not just short keywords, but budgets, scenarios, preferences, and constraints, allowing Google to gain more granular demand signals.

Traditionally, about 20% of queries have commercial attributes. If AI search allows more queries to become identifiable, matchable, and actionable commercial intent, the ceiling for search advertising could rise. For advertisers, the question is not whether AI capabilities are advanced, but whether they can generate more conversions under the same CPA (cost per acquisition).

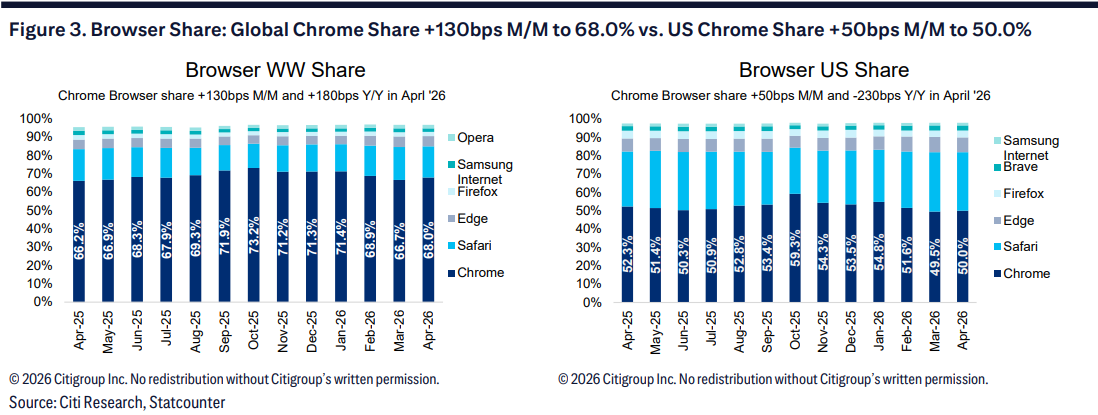

In the first quarter, Google's query volume hit a record high. In April 2026, Google’s global search share was 90.0%, an increase of 10 basis points quarter over quarter. Chrome's global share was 68.0%, up 130 basis points. If these entry points continue to expand, the commercialization foundation for AI search will be more solid.

Google Marketing Live will test AI advertising monetization

If Google I/O answers "where AI capabilities are," Google Marketing Live answers "how AI makes money."

Currently, AI-driven ad campaigns account for more than 30% of search ad spending, covering tools like AI Max, P-Max, and Demand Generation. Advertisers can create and modify campaigns through prompts, Ads Advisor provides agent-based assistance, Smart Bidding Exploration brings about 27% more conversions in search campaigns, and Campaign Total Budgets reduce manual budget adjustments by about 66%, while Journey Aware Bidding is still in the testing phase.

AI Max will be the key observation point at GML. This tool completed beta testing in April 2026 and plans to fully replace Dynamic Search Ads by September 2026. Early results show that the complete feature set of AI Max brings 14% more conversions; through broader search term matching, it delivers 7% more conversions at a similar CPA.

Google is also advancing vertical optimizations for AI Max for Shopping and Search Campaigns for Travel. If these tools become the new default configuration for search budgets, the impact of AI on the advertising business will shift from "feature upgrades" to "campaign system reconstruction."

Agent-based shopping targets transaction closure

Google's shopping business is extending from product discovery entry to deeper transaction links. UCP, Direct Offers, Agentic Checkout, and agent-based shopping experiences in Google Shopping and Chrome will be common observation points at I/O and GML.

This change is not simply about adding shopping buttons but reducing friction from search, comparison, selection to checkout. Google has recently expanded partnerships with several major e-commerce companies, as well as Meta, Microsoft, Stripe, and has since added Klarna and Affirm. If payment, installment, checkout, and ad placement can be linked, Google's commercial role in Shopping will become more significant.

Chrome is also becoming more important. In April 2026, Chrome's global share was 68.0%, with a U.S. share of 50.0%. If agent-based shopping, personalized recommendations, and checkout processes are embedded in Chrome, Google will gain new commercial entry points beyond search.

This is also one of the reasons investors are focusing on I/O. If Gemini can push "searching answers" to "executing actions," Google's pricing power in shopping and advertising may be enhanced.

Cloud business and TPU are raising Alphabet's valuation weight

Alphabet's core valuation in the past has been based on search advertising, but Google Cloud is becoming a more important variable.

In the first quarter, Google Cloud revenue reached $20.028 billion, a year-on-year increase of 63.4%; the backlog reached $462.3 billion, nearly doubling quarter over quarter, and increasing 400.3% year on year. During the same period, token consumption grew 60% quarter over quarter. These indicators show that enterprise AI demand is entering the orders and usage of the cloud business.

Calculations show that Google Cloud revenue is expected to increase from $58.705 billion in 2025 to $94.529 billion in 2026, then to $146.521 billion in 2027 and $209.525 billion in 2028. The corresponding growth rates are expected to be 61.0% in 2026, 55.0% in 2027, and 43.0% in 2028. The share of cloud business in total revenue is also expected to rise from 14.6% in 2025 to 19.5% in 2026, reaching 30.6% by 2028.

Profit margins are also improving. Google Cloud's operating profit margin is expected to reach 23.7% in 2025, 33.8% in 2026, 35.0% in 2027, and 35.5% in 2028. This means that cloud business is no longer just a high-growth segment, but is beginning to support Alphabet's overall profit margin.

At I/O, Gemini Code Assist, the "vibe coding" tool in Google AI Studio, and TPU sales strategies are also worth paying attention to. TPU-related revenue is expected to start contributing in the second half of 2026 and significantly amplify in 2027. For the market, this represents that Google Cloud is forming a more complete link between models, chips, infrastructure, and enterprise AI tools.

YouTube and AI creative tools provide another growth line

The YouTube Brandcast on May 13 is a precursor to I/O and GML. Points of observation include YouTube engagement, Shorts growth, Demand Gen tool updates, and YouTube Premium/Music subscription adoption after its price increase in April 2026.

The advertising creative side is also being redone by AI. Gemini Omni is positioned at the end-to-end creative orchestration stage, with both generation and editing possibly integrated into the advertising process. Lyria 3 has already generated over 150 million songs. Demand Gen ads with video enhancements bring 16% higher conversion rates.

The commercial significance of these tools lies in reducing the costs of ad production and iteration. In the past, advertisers needed to handle materials, placement, budgets, and bidding separately; now Google is attempting to integrate these stages into one automated system. As long as improvements in conversion rates continue, the motivation for advertisers to transition to AI placement processes will strengthen.

Valuation bet: Can AI support higher multiples

Citi's target price of $447 is based on approximately 30 times the GAAP EPS of $14.75 in 2027. Based on the closing price of $387.35 on May 12, the expected stock price return is 15.4%, plus a 0.2% dividend yield, giving a total expected return of 15.6%.

Alphabet is currently valued at about 26 times the GAAP EPS in 2027. A 30 times valuation is above the market and higher than Google's own historical valuation range. This premium requires two conditions to be met simultaneously: search queries continue to grow, and AI does not weaken the advertising base; Google Cloud continues to accelerate under Gemini demand, TPU demand, and enterprise AI adoption.

Revenue models show that Alphabet's total revenue is expected to grow from $402.836 billion in 2025 to $484.620 billion in 2026, a year-on-year increase of 20.3%; $579.560 billion in 2027, a year-on-year increase of 19.6%; $684.904 billion in 2028, a year-on-year increase of 18.2%. Google Search and Other revenue is expected to be $260.170 billion in 2026, a year-on-year increase of 15.9%; total advertising revenue is expected to be $333.057 billion in 2026, a year-on-year increase of 13.0%.

Risks are also clear. Advertising budgets may be weighed down by economic factors and consumer spending, AI competition might impact Google more than expected, internet advertising spending may decline faster, and antitrust, data, and privacy regulations may still suppress valuations.

Therefore, whether Gemini 4.0 will be released will attract attention, but it is not the only answer. The next two release events will truly test whether the AI capabilities demonstrated by Google can become a growth engine for search, advertising, shopping, and cloud business.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。