Author: Memento Research

Translated by: Deep Tide TechFlow

Deep Tide Outlook: The cryptocurrency financing data for the first four months of 2026 reveals a harsh reality: funding for gaming and DePIN tracks is nearly exhausted, while the amounts taken by two prediction market companies, Kalshi and Polymarket, exceed the total of all DeFi projects for the year. Even more concerning is that the number of mergers and acquisitions has reached the level of seed rounds, indicating that capital is shifting from betting on new ideas to acquiring existing leaders.

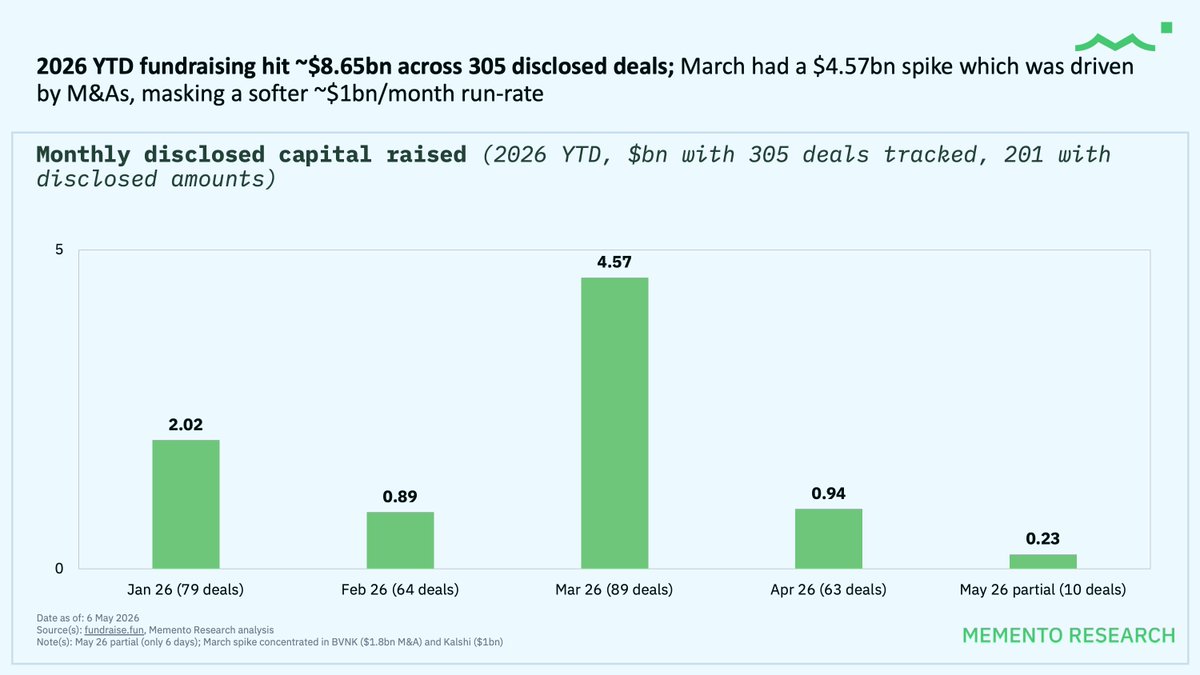

Financing Overview: March's Surge is an Illusion

From January 1 to May 6, 2026, the cryptocurrency industry completed a total of 305 financings, amounting to $8.65 billion. However, the $4.57 billion "surge" in March was actually just due to two massive acquisitions: $1.8 billion from BVNK and $1 billion from Kalshi.

Excluding these two, the real financing rate is about $1 billion per month, weaker than at the end of 2025.

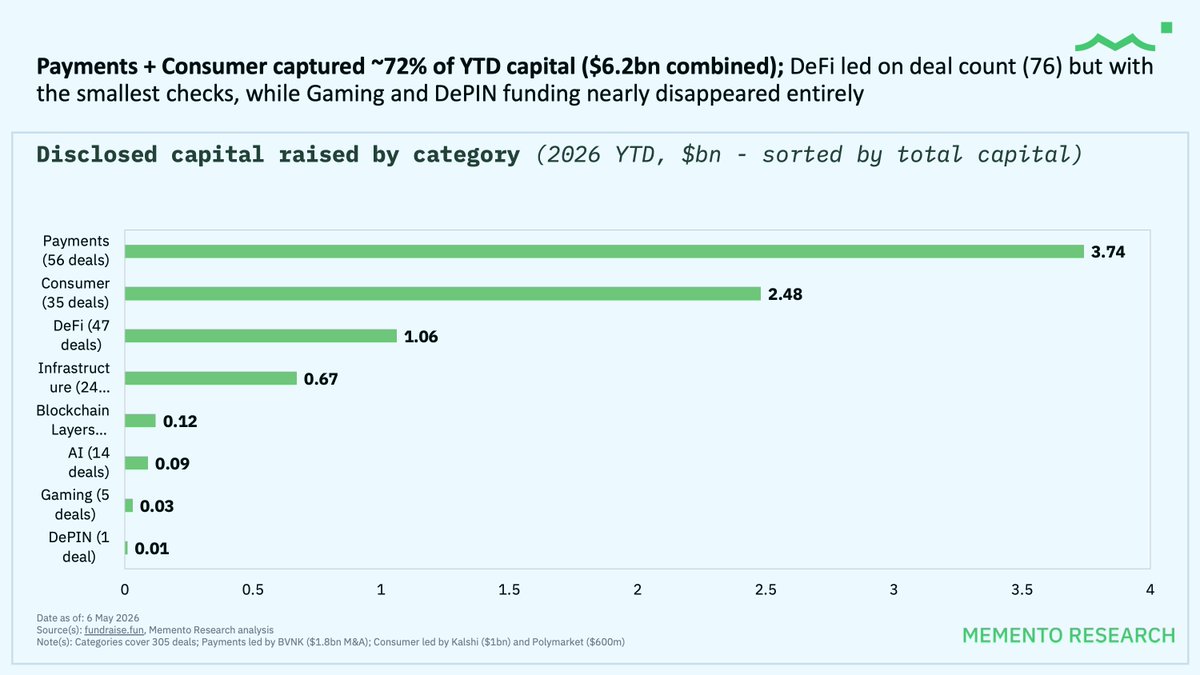

Flow of Funds: Payment and Consumption Take 72%

By sector:

Payments: $3.74 billion (56 deals)

Consumption: $2.48 billion (35 deals)

DeFi: $1.06 billion (47 deals, the most transactions)

The combined total for the payment and consumption sectors accounts for 72% of the annual funding. Financing for gaming and DePIN has nearly disappeared.

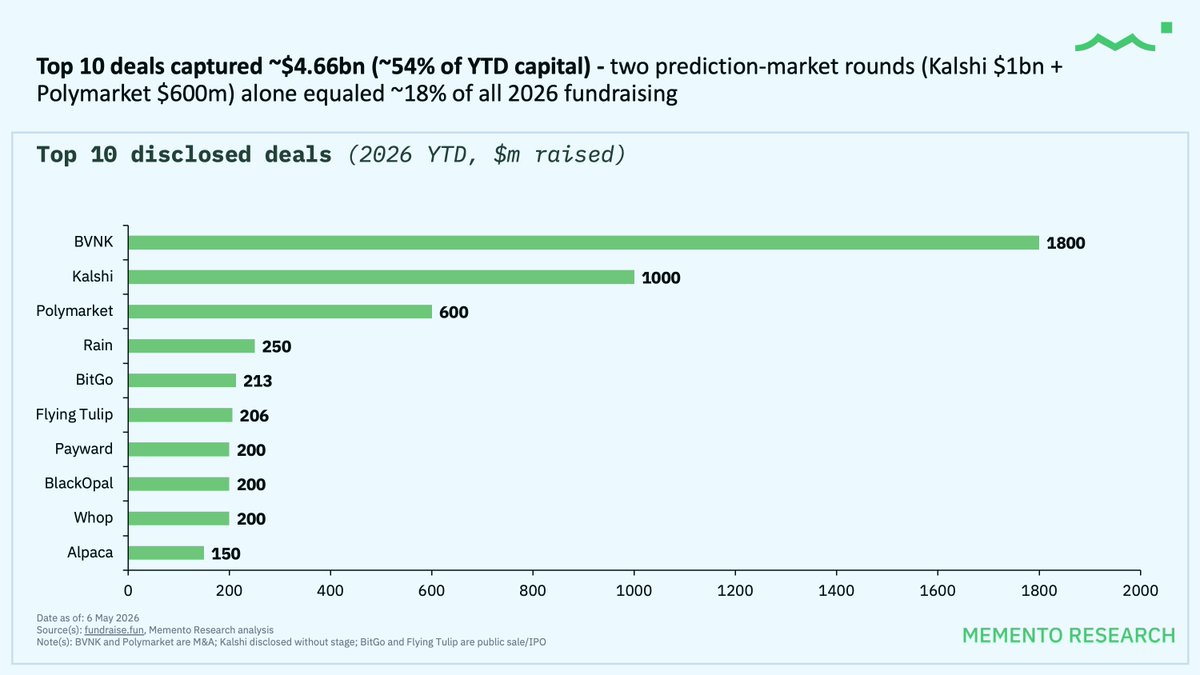

Prediction Markets Dominate the Consumption Sector

The amounts received by two prediction market companies account for 18% of annual financing:

Kalshi: $1 billion

Polymarket: $600 million

These two total $1.6 billion, surpassing the total of all 47 DeFi financings combined.

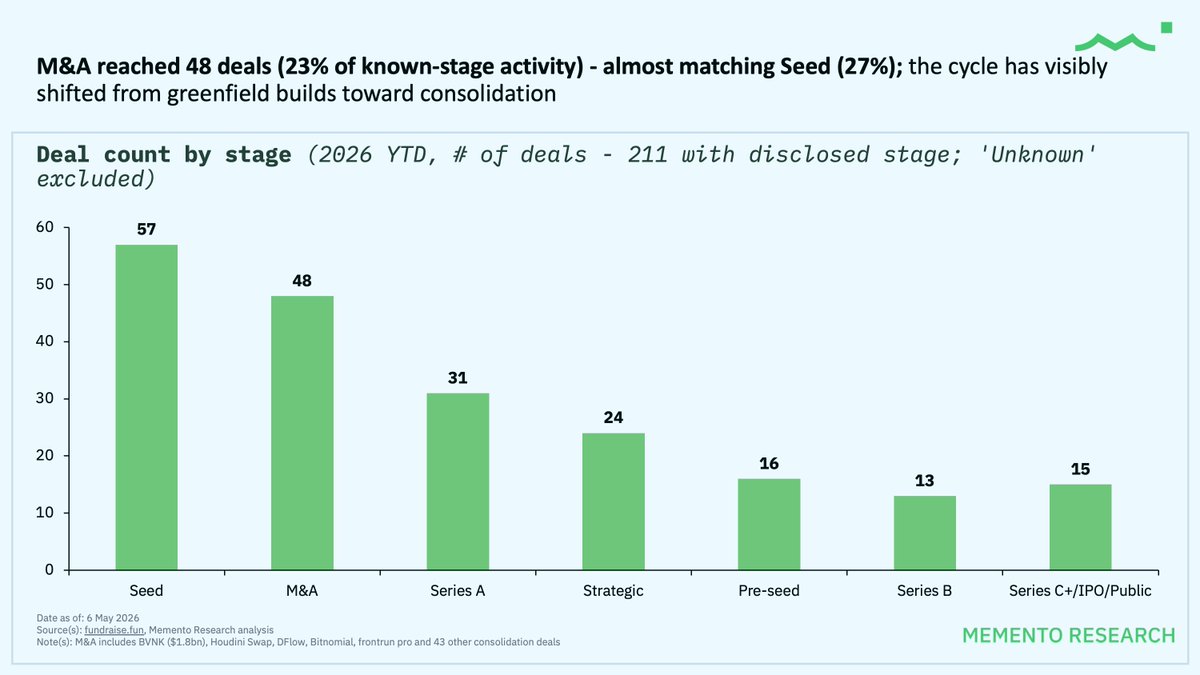

Mergers and Acquisitions Become Mainstream

The number of merger and acquisition deals reached 48 (accounting for 23% of known stage deals), nearly catching up with seed rounds' 57 (27%). This cycle has shifted from the early stages of investing in new ideas to acquiring industry leaders.

Investment Institution Ranking Reshuffled

The most active funds in 2026:

Coinbase Ventures: 18 deals (ranked second from 2021-26)

Tether: 13 deals (new leading investor)

Animoca Brands: 11 deals (ranked first from 2021-26)

GSR: 11 deals

a16z: 7 deals (a significant drop compared to about 200 deals from 2021-26)

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。