Ethena has built a system that relies on user consensus and trust, and the outcome of the fee switching mechanism will directly determine how much of this trust can be retained.

Written by: Thejaswini M A

Translated by: Saoirse, Foresight News

Value creation and value capture are two different things. Value creation involves building products and services that the market truly needs; value capture is about keeping a portion of the revenue paid by the market for oneself.

Most of the time, people assume that these two complement each other: you create valuable products, charge users, and keep a portion of the revenue, which is the most common business model for companies.

But few mention that many historically influential giant companies focused entirely on value creation in their early growth stages, deliberately giving up on value realization. They provided products almost for free, and whether they could eventually achieve profitability was entirely based on one premise: that market size and channel share would one day convert into pricing power. Some companies eventually saw that day come.

Amazon Web Services (AWS) operates with nearly zero profit for years, as Amazon has long seen: once a company deeply embeds cloud infrastructure into its business, it will not easily switch. Stripe, after handling billions in payment transactions, gradually rolled out new products and earned substantial profits based on its solid industry position. What we are discussing today is a business model that almost retains no revenue in its early stages.

Previous articles talked about the Morpho protocol: it generated a total of $256 million in fees yet retained almost none for itself. The reason lies in the infrastructure trap—when many institutions rely on your ecosystem to build their businesses, charging suddenly poses huge risks, and it itself did not actively choose to give up profits.

So, when can market size turn into pricing power? When should it stop giving away profits and start retaining revenue? Companies that excel at this model usually have clear plans; those without clear answers find themselves in tricky situations.

Now, Ethena finds itself in such a predicament.

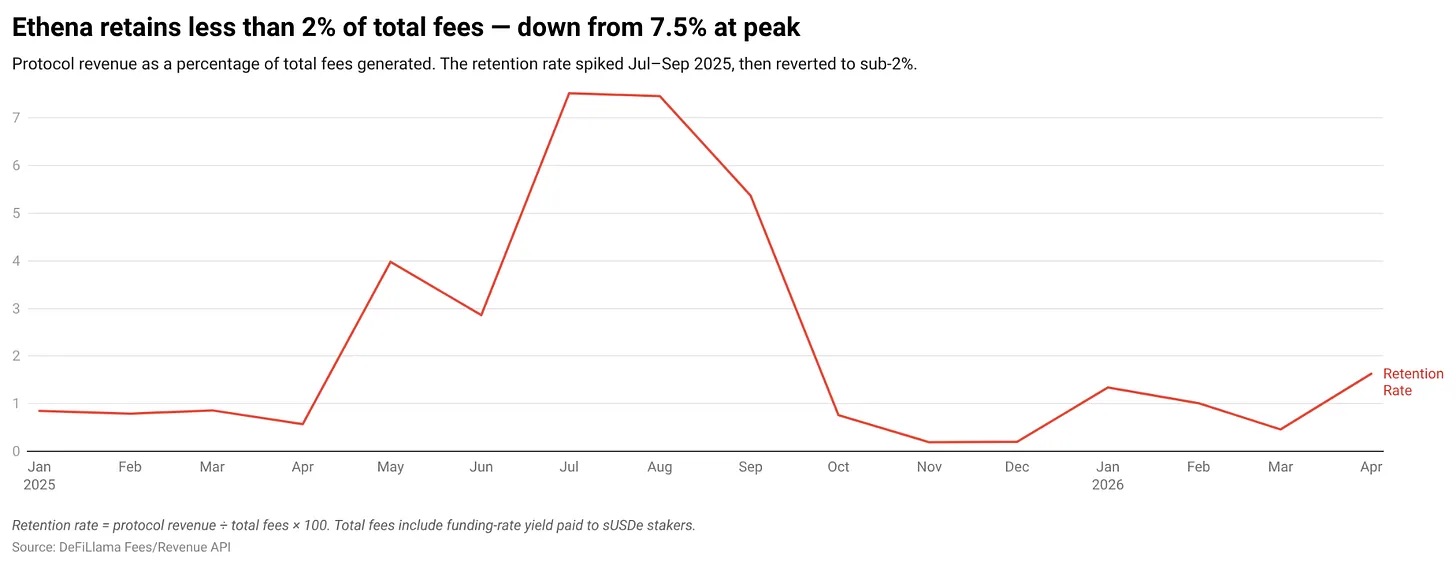

It has built the world's third-largest stablecoin. In the last 16 months, the protocol generated $470 million in fees, but the team retained only $13.8 million, resulting in a retention rate of just 2.93%. This means for every $100 earned by the protocol, only $3 remains with it. The rest of the profits are distributed to sUSDe holders as designed.

Ethena's predicament differs from Morpho's, and this article will deeply analyze the reasons.

Ethena's Product Underlying Logic

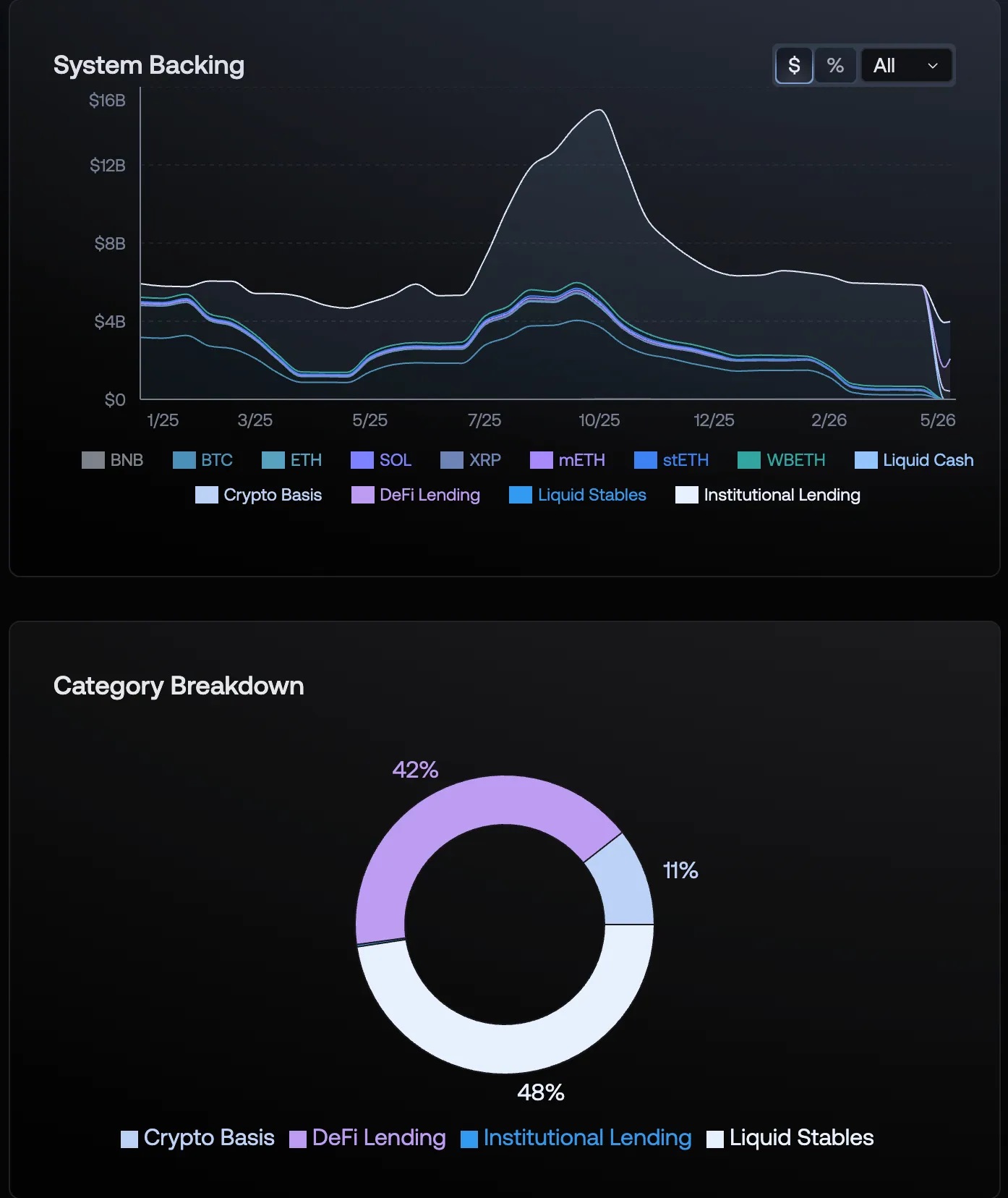

First, let’s talk about the product Ethena has created: USDe is a synthetic dollar stablecoin supported by no bank reserves. For every $1 USDe minted, Ethena allocates crypto assets as collateral and opens a corresponding short position in the perpetual contract market. In simple terms, it is about going long in the spot market and shorting in the perpetual market, maintaining a net position that is generally neutral and stable regardless of Bitcoin and other cryptocurrencies' price fluctuations.

The protocol's revenue mainly comes from three parts: funding fees paid by long traders to shorts in the perpetual contract market, Ethereum staking rewards from the collateral assets, and interest generated by reserve liquidity stablecoins.

All these revenues flow to holders of sUSDe who stake USDe; Ethena only takes a tiny portion to add to the reserve fund and charges a small minting and redemption fee, while all other revenues are distributed externally.

In 2024, the funding rates for perpetual contracts are expected to maintain at an annualized rate of 8%–11%. During that time, the protocol was just getting started, the market was overall bullish, and leveraged long traders were willing to pay high costs to hold positions. For sUSDe holders, this was an excellent investment opportunity, with annualized returns reaching as high as 18%. USDe's scale skyrocketed from zero to $6 billion in just ten months.

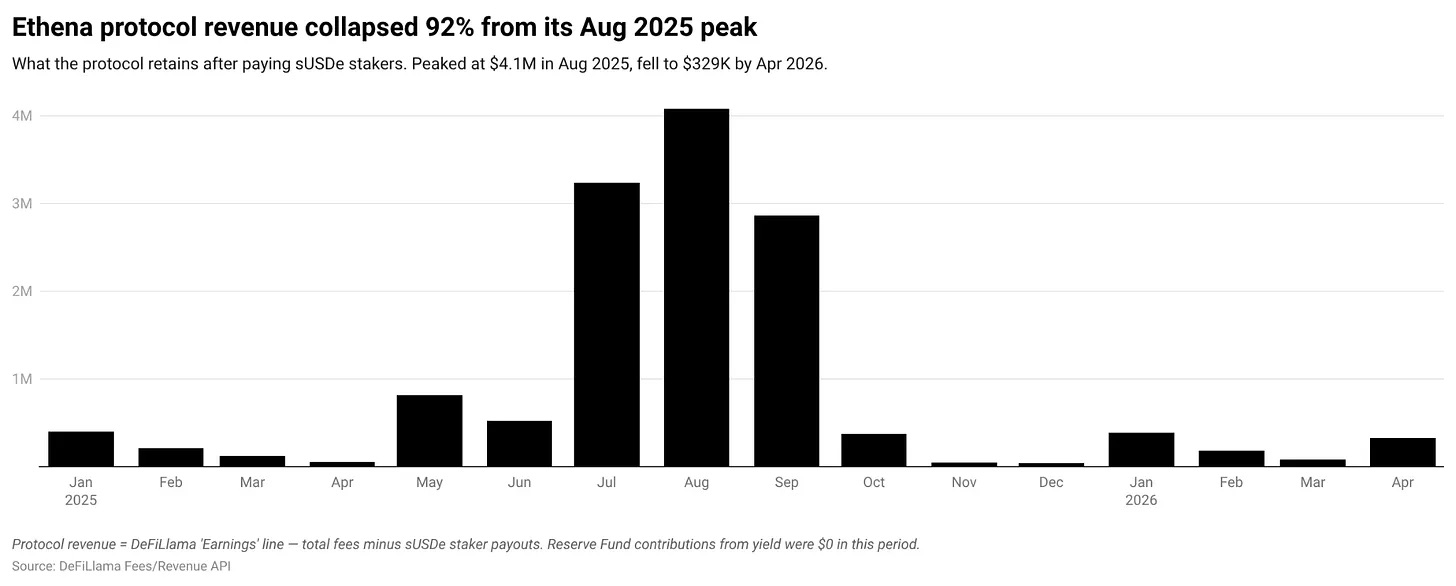

By August 2025, Ethena's total monthly fees reached $54.7 million, with the protocol retaining $4.08 million, setting a revenue peak, and everything seemed to be developing smoothly.

Ethena's protocol revenue plummeted by 92% from its peak in August 2025

A turning point occurred in October. The crash on October 10th resulted in the largest single-day leveraged liquidation event in the crypto market in years, with over $19 billion in leveraged positions vanishing in an instant. USDe briefly deviated from the $1 peg on Binance, though it recovered within a few hours, this incident was reported by the media, but beneath this market turmoil, deeper hidden dangers lurked for stablecoins.

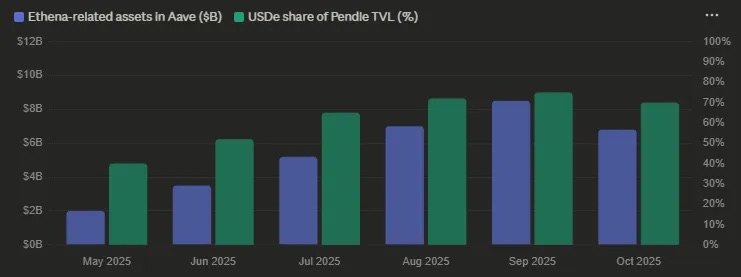

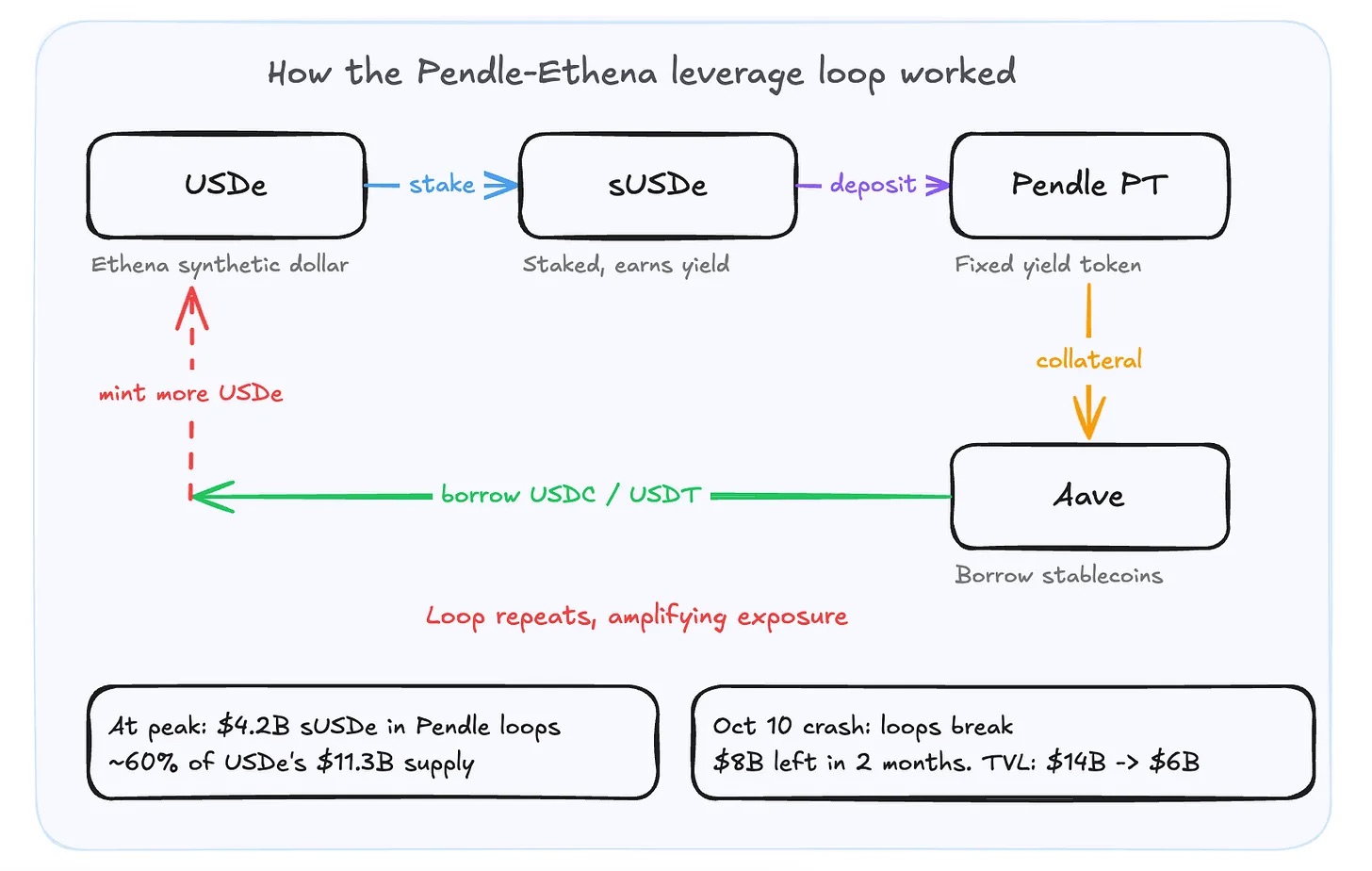

At its peak, over $4.2 billion sUSDe was locked in the Pendle protocol, accounting for about 60% of USDe's total circulation of $11.3 billion. Users locked sUSDe to secure fixed income through structured yield products and could also borrow against their positions on Aave.

Asset size changes related to Ethena in Aave and Pendle protocols from May to October 2025

These types of players are profit-seeking speculators relying on high leverage for arbitrage; they only want to take advantage of the high annualized yield of sUSDe. Once the market turns, and the arbitrage logic collapses, they immediately exit. After the October crash, this leveraged arbitrage chain was completely severed, with over $8 billion in funds fleeing in just two months, and $5.7 billion lost in October alone.

The Pendle-Ethena leveraged cyclic arbitrage model is also the core reason for the sharp decline in USDe funds during the October 2025 market crash

Those who chose to stay generally did not use leverage. The staking ratio of USDe (the proportion of positions converted to sUSDe) fell from a peak of 60% to about 47% by the start of 2026, with user loyalty remaining virtually unchanged. Only the effect of the overall shrinking supply led to a reduction in staking scale from $8.4 billion to $3.3 billion. Long-term users who really recognize the value of income-generating dollar assets chose to remain, while purely profit-driven speculators exited entirely.

However, for Ethena, the October crash directly shattered its growth strategy reliant on expansion of distribution through scale.

The model of this protocol is: to distribute almost all revenue to sUSDe users while itself only profits from minting and redemption fees, which is a minuscule proportion of the overall business.

In the first quarter of 2026, Ethena's total fees reached $65 million, yet the quarterly net profit was only $614,000. During the same period, Tether's net profit reached $5.2 billion. Both are stablecoin issuers, yet their profitability levels are drastically different. It is critical to note: total revenue for the protocol does not equal the actual profits that Ethena pockets.

Ethena's protocol revenue retention rate

Meanwhile, the underlying collateral asset structure of USDe also underwent dramatic changes: in early 2025, perpetual contract positions accounted for 93% of USDe's collateral assets; by early 2026, perpetual contracts comprised only 11%, with the remaining 89% consisting of high liquidity stablecoins and lending positions.

Ethena has completely transformed from its original delta-neutral arbitrage trading protocol into a tool akin to U.S. Treasury yield distribution, transmitting treasury-like returns to sUSDe holders. Currently, the annualized yield of sUSDe is merely about 3.5%, comparable to that of high-quality money market funds, no longer requiring complicated delta-neutral hedging mechanisms.

The significant structural change of the underlying collateral assets of the Ethena protocol perfectly confirms what we previously discussed about "transforming from leveraged arbitrage to low-risk tools"

Years ago, an annualized yield of 18% was the core advantage of USDe over traditional stablecoins like USDC; now, with yields reduced to just 3.5%, this advantage has significantly diminished, while the complex underlying product mechanism has turned into a potential risk hazard.

On the regulatory front, there was also a blow: in March 2025, the Federal Financial Supervisory Authority of Germany (BaFin) classified USDe as an unregistered security, ordering Ethena's German subsidiary to shut down and giving EU users 42 days to redeem their assets. Ethena subsequently responded, stating that at the time of the ban, its German entity had neither whitelist users nor direct customers, and most USDe issuance occurred before the effective date of the EU's Markets in Crypto-assets Regulation (MiCA). This outflow of funds was not primarily due to EU regulations leading to capital withdrawal; the core reason was still the collapse of the Pendle leveraged arbitrage chain.

The Dilemma of the Fee Switching Mechanism

Ethena plans to initiate a fee switching mechanism: reallocating 10%–20% of the protocol's revenue from sUSDe users to sENA token stakers.

Revenue distribution has strict priorities: first, it must fully replenish the protocol's reserve fund; second, it must ensure that sUSDe yields remain at a market competitive level as determined by the risk committee; only after both conditions are met will the remaining revenue be distributed to ENA stakers. The risk committee has the authority to set and adjust revenue benchmarks autonomously, and until governance voting is enacted, there is no fixed bottom line for revenue distribution. In simple terms: ENA stakers can only share in the remaining "residual revenue."

Currently, with market interest rates low, the protocol has no surplus residual revenue available for distribution, making the fee switching mechanism effectively meaningless.

This allocable revenue originates from the same fund pool used to distribute sUSDe yields. In times of peak revenue with funding rates as high as 15%, even a slight reduction of 2 percentage points in sUSDe yields would go unnoticed by users; however, now that sUSDe yields are just 3.5%, and the risk benchmark is set at around 4.5%, which triggers the revenue protection threshold, no revenue can flow to ENA holders.

For Ethena to realize profitability through the fee switch, it must rely on higher funding rates for perpetual contracts; however, high funding rates only occur in a crypto derivatives bull market—precisely the same market environment that spurred the Pendle leveraged arbitrage and ultimately led to an outflow of $8 billion in funds. This means that Ethena's profitability realization logic is tied to the same market conditions as its stable scaling risk.

Comparing the Trust Logic of Two Stablecoins

Tether's trust logic: builds user trust through long-term institutional credibility. After going through multiple industry cycles without ever experiencing principal losses, the market has gradually formed a consensus: the risk of holding it is far lower than arbitrarily switching to other stablecoins. Tether retains almost all profits; users are fully aware of this yet remain steadfast, and this loyalty stems from years of risk-free operational records.

On the other hand, Ethena takes the route of loyalty tied to interests: distributing the vast majority of revenues to users, with almost no profit retained by the protocol, aligning user and platform interests completely, not relying on endorsements or concealment, but building trust through symbiotic benefits.

However, this symbiosis model has a fatal flaw: once the protocol begins to retain revenue for itself and realize value, the symbiotic relationship will instantly shatter.

When Ethena starts to self-retain revenue, the originally win-win relationship transforms into a purely commercial transaction. Those users who remained purely due to completely binding interests will immediately feel the disconnection. Only then can they see clearly whether users truly recognize the product itself or merely accept the mechanism for high yields. Tether has never touted a common interest with users from the beginning, thus it will never fall into such contradictions; however, Ethena’s fee switching mechanism is precisely what is breaking the hard-earned trust binding with users.

Ethena has established a system that relies on user consensus and trust, while the result of implementing the fee switching mechanism will directly determine how much of that trust can be retained.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。