Author: Odin

Translation: Deep Tide TechFlow

Deep Tide Introduction: Global VCs are shouting "invest in people, not projects," but the data from the University of Chicago reveals a harsh truth: investors make the worst decisions when they overly rely on the founder's education.

This worship of education causes the industry to lose hundreds of millions of dollars each year. Ironically, the ones who truly invest in people, like Thiel and YC, do not look at resumes at all, but rather the complex whole created by the founders and their ideas. For cryptocurrency investors, this reminds us to be wary of those institutions that only do pattern matching based on prestigious educational backgrounds.

A long time ago, eight researchers from Shockley Semiconductor walked into the office of a young banker in San Francisco, Arthur Rock. This "rebellious eight" proposed an idea: they wanted to start a competitor company. Rock saw something in them, perhaps a special kind of talent with nowhere to apply it, and he set out to help them raise funds, founding Fairchild Semiconductor—this company is widely considered to have planted the seeds of Silicon Valley. This is the story of how Rock, the first believer of the team, became the first modern venture capitalist.

Rock's decades-long belief was that supporting talent is at the core of venture capital. He loved to say that an excellent management team can find good opportunities even if they need to jump out of the current market they occupy.

His peers had different views. Tom Perkins of Kleiner Perkins focused on technology, asking whether it was proprietary and whether it was clearly superior to alternatives. Don Valentine, who founded Sequoia after marketing at Fairchild, was obsessed with the market. In the mid-1980s, when Sequoia considered an early investment in Cisco, most of his peers rejected it; the founding team was considered weak. Valentine invested anyway, reasoning that the market for networks was so huge that even a mediocre team could sell a lot of equipment.

These three inspired three different philosophies of American venture capital; but Rock triumphed in the cultural war. "Venture capital is a people business" is not only a great slogan but also places the founders at the center of the story. If you are selling capital to founders, this is exactly what they want to hear.

But is it really that simple? What does the so-called "people business" actually look like?

Normative Conformity

Today, almost every venture capital firm claims to prioritize founders.

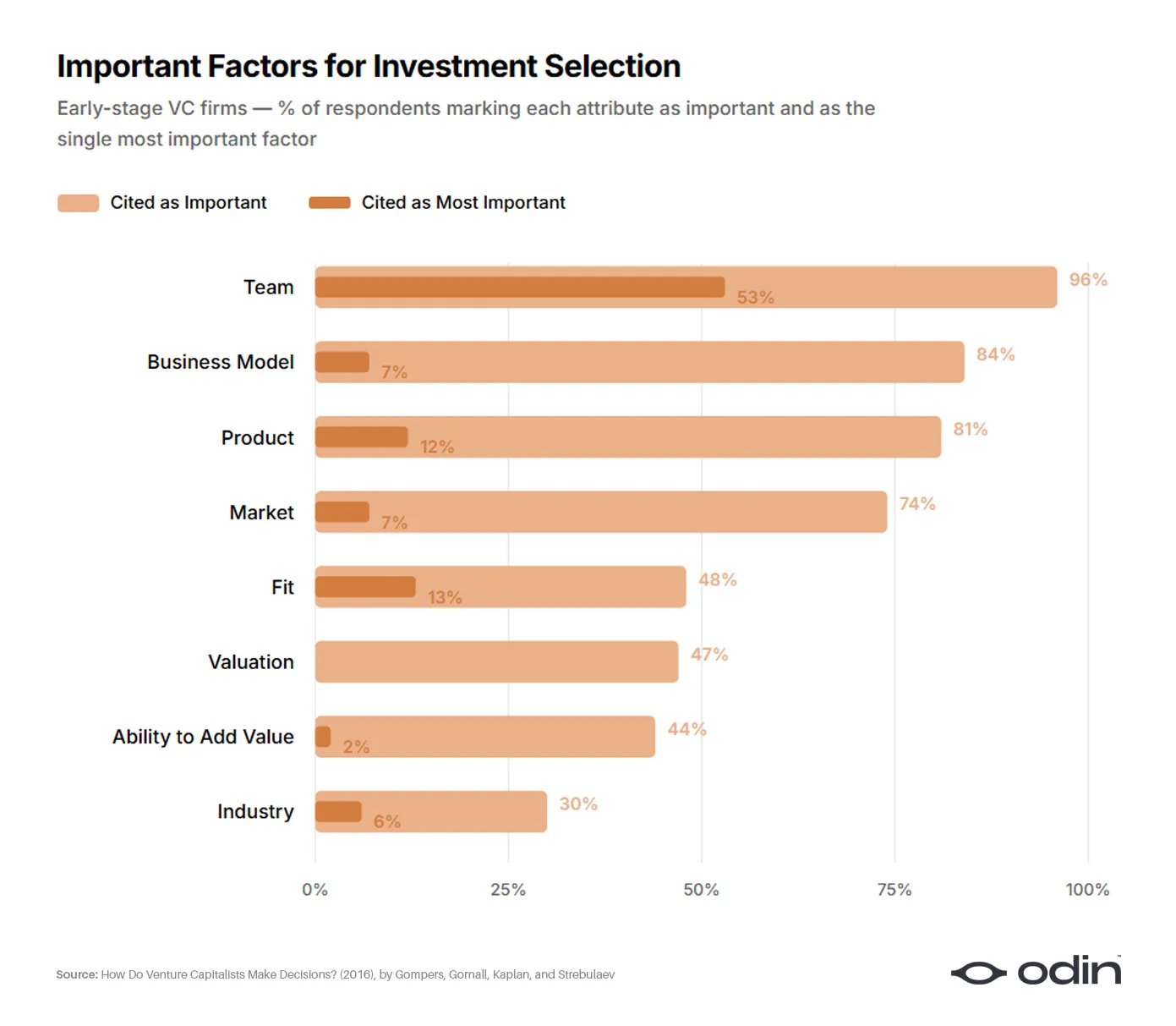

In 2016, four economists (Paul Gompers, William Gornall, Steven Kaplan, and Ilya Strebulaev) surveyed 885 venture capitalists from 681 firms to understand how they make decisions. This study is the most thorough analysis of industry decision-making, seemingly providing a final conclusion on Perkins and Valentine's philosophies.

About 53% of early-stage respondents listed the founders as the most important single factor in deal selection. Business models and products (Perkins' traditional domain) were chosen by about 10%. Markets and industries (Valentine's focus) were selected by about 6%. The rest were scattered across valuation, fit with the fund, and the investors' own ability to add value.

"96% (92%) of venture capital firms believe the team is an important factor, and 56% (55%) believe the team is the most important factor for success (failure). The team is the most important for all sub-samples, but especially important for early and IT venture capital."

—— "How Do Venture Capitalists Make Decisions?" by Gompers, Gornall, Kaplan, and Strebulaev

Looking at other responses from the survey, 9% of investors admitted they do not use any financial metrics, with this ratio rising to 17% among early-stage investors. An industry so reliant on qualitative judgments should be reflecting on its criteria for judgment and how to track outcomes.

Unfortunately, the answer remains a vague commitment—to invest in "the best founders"—but fails to clarify what that means or why.

"The findings indicate that venture capitalists are not good at introspecting their decision-making processes. Even in controlled experiments that significantly reduce the amount of information considered, venture capitalists lack a deep understanding of how they make decisions."

—— "Lack of Insight: Do Venture Capitalists Really Understand Their Decision-Making Processes?" by Andrew Zacharakis and G. Dale Meyer

Thus, the founder-first venture capital approach has fostered a pandemic of lazy thinking, permeated by biases and elitism. This, in turn, is reflected in declining performance as well as frequent fraud and negligence scandals.

A Billion-Dollar Blind Spot

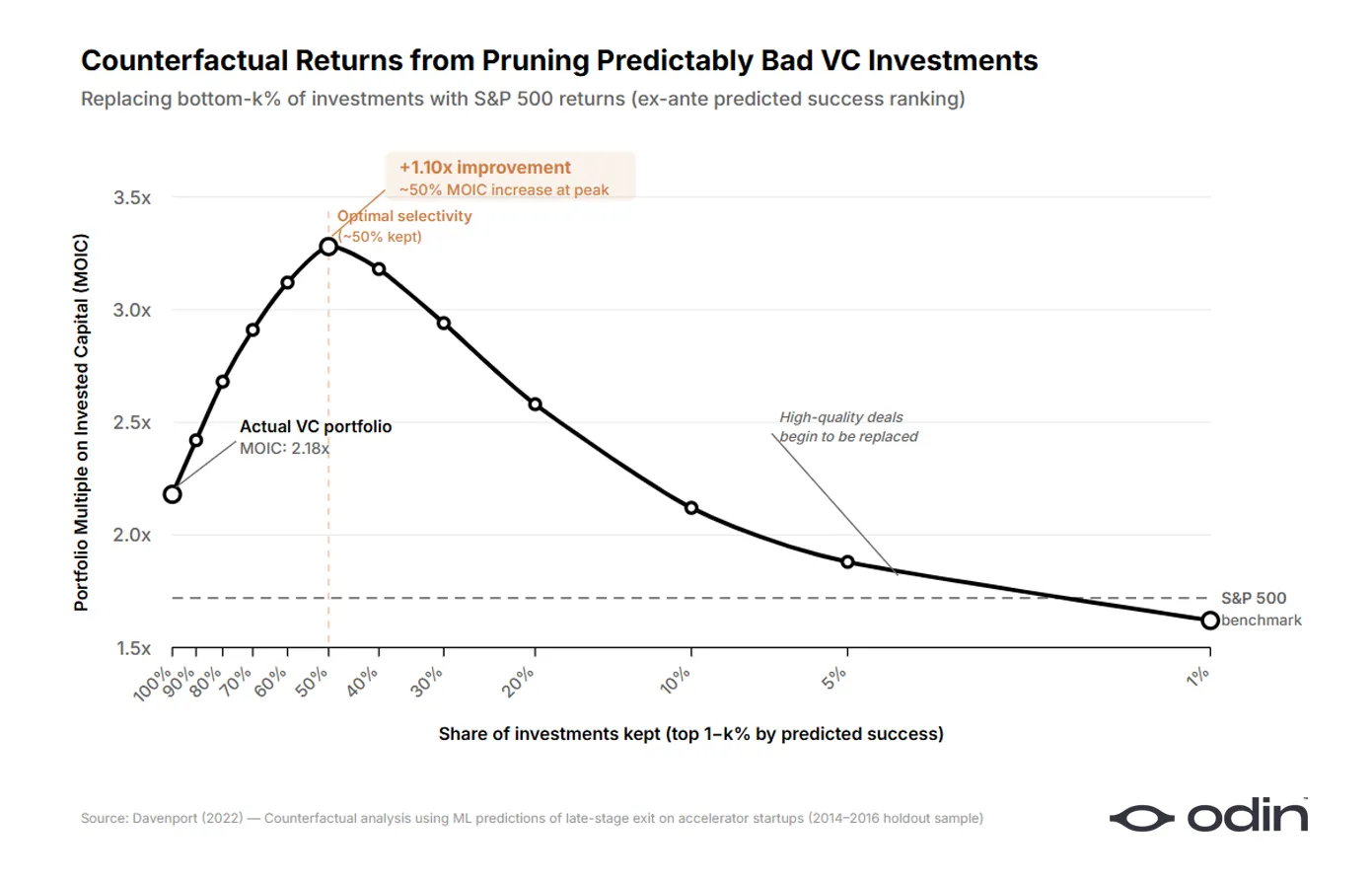

In 2022, Diag Davenport, an economist at the University of Chicago Booth School of Business, tagged the losses caused by this oversimplified attitude to the industry.

Davenport built a machine learning model on a dataset of over 16,000 startups, representing over $9 billion in committed capital. He trained the model using only the information available to investors at decision-making time and asked: How many of the investments that venture capitalists actually made could have been identified in advance as worse than if the same money had been invested in standard public market alternatives? The answer was about half.

By removing the worst half of the investments and reallocating capital to public market options, Davenport discovered that venture capital returns in the sample could have been 7 to 41 percentage points higher. In the data he handled, this equated to over $900 million in avoidable losses. The cost of poor investments, expressed as a spread relative to external options, was about 1000 basis points.

Davenport trained two parallel algorithms, one predicting which startups would become the best investments and the other predicting which would become the worst investments. When he compared the signals relied on by each model, a strange pattern emerged. The algorithm built on good outcomes relied on product characteristics, while the algorithm built on bad outcomes heavily relied on founder backgrounds. When investors made good decisions, they looked more closely at the ideas. When they made bad decisions, they seemed to look more closely at the teams.

To test for over-weighting, Davenport built a separate model using only founder education data and asked: Would two companies that appeared equally promising under the full model receive different investment outcomes based on their performances under the education-only model? The model indicated that investors systematically over-weighted education, and they did so most severely on the startups that performed the worst later.

"Investors seem to be convinced that a founder-centric world model is correct. This may lead investors to ignore predictive characteristics, and the feedback loop of never noticing or learning persists, which is consistent with the model and evidence presented by Hanna et al. (2014)."

—— "Predictable Bad Investments: Evidence from Venture Capitalists" by Diag Davenport

Davenport's paper is part of an increasing number of studies reaching similar conclusions, indicating that investors over-weight superficial founder attributes, leading to predictable bad investments (omission errors) and predictable missed opportunities (omission errors).

This has a structural explanation; in venture capital, "success" is more easily measured by incremental financing rather than distant exits, and if investment decisions become a simple tick-box exercise, the friction in fundraising will decrease.

The industry at some point convinced itself that the ability to raise capital was itself an ideal founder trait, and this logic became recursive. Investors began to do pattern matching on the founder prototypes most likely to raise the next round, making that prototype easier to fund and reinforcing the pattern. Thus, the quality of returns generally declined while the speed of capital (and fee income) accelerated.

This cycle is explained by economist Daniel Kahneman, who described that even complex professionals can be tempted if simple, coherent ideas align with the right incentives—even if they lead to apparently bad outcomes.

"The statistical evidence of our failures should shake our confidence in judgments of specific candidates, but it does not. It should also temper our predictions, but it does not. We know as a general fact that our predictions are almost no better than random guessing, yet we continue to feel and act as if each specific prediction is valid."

—— "Don't Blink! The Dangers of Confidence" by Daniel Kahneman

The Paradox of Great Investors

This creates an interesting puzzle. The data shows that over-weighting founder attributes leads to worse investment decisions, especially in the worst-performing deals. Yet, some of the most successful companies in the industry are also the most aggressive in prioritizing founders.

Founders Fund has spent twenty years supporting unusual people before others are willing. Peter Thiel also created the Thiel Fellowship for young entrepreneurs without college degrees, which has produced incredible success stories.

Y Combinator has operated for twenty years based on identifying exceptional founders. In fact, the program has proven to reduce elitism in venture capital by providing alternative sources of signals for investors.

If founder-first thinking were merely systematic pathology, the firms most committed to it should be the worst performers. Instead, they are the best.

The answer is actually quite direct. When great investors say "founder first," they mean something far more complex than the shallow interpretation offered by the entire industry.

The Great Man Fallacy

The desire to simplify founder success into a predictable list of attributes is a modern manifestation of the Great Man theory; the belief that history is shaped by outstanding individuals with intrinsic greatness, ignoring how success itself forges these qualities.

"A successful company with a strong performance record? The leaders appear visionary, charismatic, and possess strong communication skills. A company that is struggling? The same leader appears indecisive, misleading, or even arrogant."

—— "The Halo Effect," Phil Rosenzweig

For instance, entrepreneurs like Elon Musk have shaped investors' expectations for hard-tech founders through many stories about his cross-disciplinary fluency, discipline, and determination. Thus, this is what they seek in first-time founders, not realizing that Musk developed these attributes over time, they are depriving others of the opportunity to do the same.

Also consider Thiel's investment in Mark Zuckerberg, the Harvard dropout. Today, this is often cited as an example of Thiel's early ability to identify exceptional founders. Yet, contemporary records show that Thiel was drawn to Facebook itself, the early traction, and Zuckerberg's particular way of framing the online identity issue.

If Zuckerberg were starting a flower delivery startup, would Thiel recognize anything in him? It's hard to imagine. The idea of how a college social network should operate and the particular form Zuckerberg had already given it was the magic Thiel was searching for.

Indeed, when Peter Thiel was asked by Andrew Ross Sorkin at the DealBook summit how he evaluates founders, his answer resonated with the Facebook example.

"I don't separate the idea, the business strategy, and the technology from the person too much. It's all some kind of complex packaged deal."

—— Peter Thiel, Co-founder of Founders Fund

He said he could not evaluate the quality of the founder without assessing the quality of the idea the founder was working on. He cannot assess the idea without understanding how the founder is shaping it. The two are inseparable.

Problems Worth Solving

The academic community has also developed a complementary argument. In a paper published in 2022 in the Journal of Business Entrepreneurship Design, Mattia Bianchi from the Stockholm School of Economics and Roberto Verganti from the Politecnico di Milano argue that entrepreneurship has long been systematically misunderstood as an activity of solving problems, while in fact, it primarily is an activity of discovering problems.

Within their framework, the most important creative act of the founder is to identify and define a problem worth solving. Everything else, whether it's a pitch deck, market entry strategy, or product roadmap, derives from the quality of this initial definition.

"Viewing problem discovery as a design act rather than mere discovery expands the potential impact of design practice—from creatively generating solutions to creatively generating the problems themselves. Redefining problems in speculative ways is another lever for breakthrough innovation, as unconventional problem statements can open unforeseen pathways to solutions."—— Bianchi and Verganti, "Entrepreneurs as Designers of Problems Worth Solving"

If this framework is correct, then the core dichotomy of horse and jockey is misguided. Evaluating founders should involve looking at the problems they choose to tackle and the specific frameworks they utilize to understand these problems. Ideas also cannot be evaluated in isolation, as they reflect the founders' material expression of their beliefs about what the world will look like a decade from now. The two interpret each other, and any investors claiming to evaluate them separately surely would not do well on either.

“You Will Know Them by Their Fruits”

Nabeel Hyatt of Spark Capital articulates this combinatory approach well. When asked how to distinguish between true executors and those founders who merely superficially meet many criteria, his answer was surprisingly straightforward.

"The way we distinguish between snake oil salesmen and true executors is by looking at what they have built. I’ve never evaluated a company and said 'this person should get a $15 million check' just because I've seen the product or used the website. You look at the product and then get to know the people behind the product by evaluating the product."—— Nabeel Hyatt, General Partner at Spark Capital

The product is an embodiment of the founder's ambition, profoundly reflecting their judgment, priorities, and the problems they choose to solve.

An investor who says, "I invest in people" but does not closely study the product is either investing in superficial patterns or investing in charm and personal charisma. These are precisely the habits that can reliably generate predictable bad investments.

Sam Altman expressed the same idea in slightly different language during a 2016 summit with Khosla Ventures’ Keith Rabois, discussing his heuristic method of application screening:

"The hardest quality we seek to identify is determination. There are a few other themes we focus on: clarity of vision, communication skills, and the non-obvious brilliance of the idea, which we scrutinize very carefully. These are things you can't always judge correctly, but you can often get quite a bit of data, and they're not as difficult to gauge as determination."—— Sam Altman, former President of Y Combinator

He did not mention the brilliance of the founders. He spoke about the brilliance of the idea, defined as "non-obvious," indicating that the founder chose a novel problem. There is also the clarity of vision, suggesting one should look at how they perceive and articulate that problem. Of course, there is also their determination to invest in that process.

In Bianchi and Verganti's language, he is talking about founders as designers of problems worth solving.

The Whole Ocean in a Drop of Water

When investors say they invest in people, it may mean two things.

The first is the belief that attributes such as background, resume, charisma, and past fundraising success convey signals more effectively than the founder's choice of what to spend time on. Essentially, this position sees founders as interchangeable commodities that can be stacked and ranked. This is the version most directly refuted by Davenport’s data.

The second, rarer version, is the belief that the objects being evaluated are a unique alchemical mix of people and ideas. The investor's job is to assemble a complete picture: the choice of problems, the form of solutions, the character of the team. Only then can they fully perceive the opportunities before them.

The two are easily confused because they use the same vocabulary. Both express a language that supports and celebrates human potential. The first is lazy and is fully rewarded by industry norms. The second is difficult, often misunderstood, but clearly the path to higher quality investments.

The argument is not that investors should abandon qualitative team analysis and revert to Perkins and Valentine’s approach. The conclusion is simply that teams cannot be effectively assessed divorced from the context of what they are doing, and attempting to do so is precisely where investors fall into problematic pattern matching.

This is why the atomic unit of entrepreneurship is neither the founder nor the idea, but the unity of both. Venture capitalists must stand far enough back to see both at once and evaluate them as a single entity.

Rather than getting tangled in the old question of horse versus jockey, the investor's job is to identify the centaur.

Note: A paper from 2009 provided empirical evidence for prioritizing ideas over people when assessing companies by analyzing how many companies had changed their leadership teams or core products at the time of their IPO. However, this covered a period where VCs often brought in new executives before the IPO, which seems no longer relevant.

Use Odin to operate your venture capital firm on your phone.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。