1. From "Temporary Statement" to "Formal Rules": The Open Letter Chooses the Current Policy Window

Although the SEC’s Market and Trading Division’s statement provides a green light for certain software user interfaces, its legal effectiveness remains non-binding guidance, unable to provide developers with long-term legal certainty. The open letter explicitly calls for the initiation of a formal rule-making process, essentially hoping to transform the current policy stance into regulatory text that can be cited by courts and is less likely to be overturned by a single committee through the announcement and comment process under the Administrative Procedure Act framework. Currently, the SEC, under the leadership of Chairman Paul Atkins, maintains an open attitude towards digital asset innovation, contrasting sharply with the repressive stance during former Chairman Gary Gensler's period—this represents the best policy window for solidifying rules. Once the rule-making process is initiated, validators, oracle providers, RPC providers, and cloud service providers will have the opportunity to be explicitly excluded from the definition of "broker," thereby eliminating the most significant legal uncertainties in their business models.

2. For Exchanges and Wallet Service Providers: Reducing Compliance Friction Costs for Non-Custodial Businesses

For publicly traded companies operating cryptocurrency trading platforms or self-custodian wallets, their non-custodial interfaces have long faced the regulatory gray area of "whether the interface constitutes brokerage activity." If the rule-making requested by the open letter can clarify that subjects "that only provide software interfaces without controlling customer private keys" do not need to register as broker-dealers, it will significantly reduce the compliance costs and legal risks for such companies in the DeFi space. Currently, various exchanges' wallet products and third-party DeFi aggregation interfaces are facing uncertainties about whether they need to register with the SEC; the establishment of formal rules will release quantifiable compliance capital for these business lines. Each week of rule-making delay means additional legal expenses and investors' risk discounting of non-custodial business.

3. Infrastructure Service Providers: The "Exemption from Registration" Dividend for Validators, Oracles, and Cloud Services

One of the most groundbreaking demands in the open letter is to explicitly exclude validators, API and RPC providers, oracle operators, and cloud services from the definition of "broker." This means that under the final rules, enterprises running Ethereum or Solana validation nodes, operators providing oracle data, and cloud service providers supplying RPC endpoints for DeFi applications will not have to worry about being classified as broker-dealers simply for processing on-chain data or validating transactions. For technology infrastructure companies listed on Nasdaq or the New York Stock Exchange, this rule will clear compliance barriers for them to provide node services or cloud services to the crypto market. The formal establishment of this rule will give rise to a more predictable enterprise-level DeFi infrastructure market.

The Deep Resonance of SEC Policy Shift and Infrastructure Demands: From "Temporary Clearance" to "Permanent Rules"

Yesterday's open letter and the prior temporary statement from the SEC's Market and Trading Division form a progressive relationship in policy progression. Although the temporary statement gave the green light to certain user interfaces, its fragility lies in the lack of support from the rule-making record, as the next SEC leadership can overturn it at any time. The deeper demand of the open letter is precisely to elevate this temporary "no action" stance to a formal regulation verified through the notice and comment process—this is not about changing the substantive content of the policy but about changing the durability and defensibility of the policy. For validators, oracle providers, RPC providers, and exchanges’ non-custodial wallet businesses, the initiation of the formal rule-making process will be the most critical policy anchor for eliminating legal uncertainties in the second half of 2026; while the current temporary green light relying on the personal policy stance of the SEC chairman still faces the vulnerability test after the future committee composition changes.

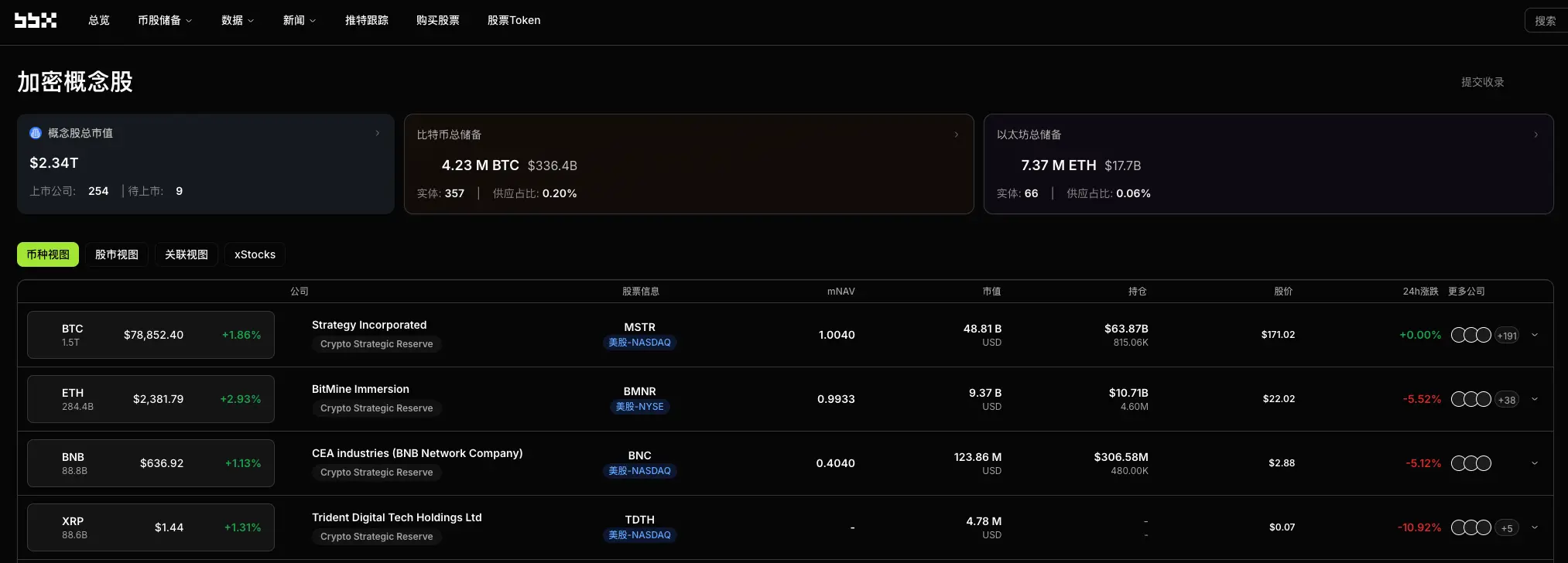

Data Source:https://bbx.com/ Crypto Concept Stock Information Database, organized based on yesterday's announcements from global listed companies and SEC/TSE disclosure documents.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。