Written by: Tulip King

Translated by: Saoirse, Foresight News

You may have already noticed that after inflating the valuations of private enterprises to several trillion dollars, venture capital firms are finally ready to cash out and exit. But their only dilemma is finding enough liquidity for their exit.

Let’s be clear: I am not accusing the San Francisco venture capital circle of engaging in illegal activities. What I criticize is that their actions are extremely unethical and have destroyed the original social contract of capitalism.

The Original Agreement

The baby boomer generation is the last group to benefit from the era's dividends.

The United States does not have a European-style high welfare state system, nor should it have needed one. The original social agreement was that the stock market is the welfare system for Americans. Traditional fixed-income pensions exited, replaced by personal contribution accounts; the pension system was overtaken by 401k plans; social security could only serve as a safety net, and no one expected to rely solely on social security for retirement.

The underlying rule was that every ordinary worker would become a shareholder; the dividends from capital appreciation would also rise alongside ordinary workers. It didn’t matter if wage growth stalled or the wealth gap widened, because everyone’s retirement account would be compounding in the background, and everyone would ride the same train of wealth, with a final outcome that would not be too bad.

This is also why America’s wealth gap could be politically tolerated. You could accept that the boss earns four hundred times your income, as long as your retirement account and the boss’s assets rise along the same curve. Passive index funds are the purest embodiment of this agreement. Supermarket cashiers, teachers, and plumbers could enjoy the market returns brought by professional capital discovering value, sharing dividends securely. At that time, the capital market belonged to a public dividend pool for everyone.

But for this agreement to hold, certain preconditions must be met: the public market must be a place where real value is created; the dividends from wealth appreciation must benefit the public; every new capital growth must be incorporated into holdings by index funds. These conditions used to be long-standing but have now all become invalid.

This is everything they have stolen from you.

When companies remain private until their valuations reach trillions of dollars before going public, the public market no longer creates value, only cashes out value. Everything happening in today’s stock market is merely wealth distribution, not compounding growth. The profits from the growth stage of companies that should have flowed to ordinary retirement funds now all fall into the hands of pre-IPO equity holders. After Figma went public, its valuation was halved within weeks compared to its private valuation; Klarna's valuation plummeted by 90%. And all of this is precisely the outcome designed by this system.

The industry has also noticed that ordinary retail investors are isolated from the dividends, so they threw out a set of rhetoric: democratizing investment, widening investment channels, bridging the wealth gap, and allowing retail investors to enter the private equity market. But the reality is exactly the opposite: they merely allowed retail investors the right to take over the chips accumulated at low prices by insiders when the companies were worth only a fraction of what they are now, at the peak of a decade-long private bull market. The private venture capital products aimed at retail investors are not genuine investment opportunities; they are merely tools for distributing high-priced internal chips. Even Naval's own promotional logic confirms this point.

(Note: Naval Ravikant is the number one spokesperson for democratizing private equity in Silicon Valley's venture capital circle, and the author of this article explicitly points out that his advocacy for ordinary people's private equity investment is a media push for venture capital to achieve high-level exits and capture retail liquidity.)

A Carefully Designed Exit Strategy

The cryptocurrency circle has always been the first to grasp this harvesting strategy.

Early crypto project foundations held a large amount of locked native tokens, and retail purchasing power had already dried up. As the unlocking period approached, there were no buyers.

So they devised a plan: to package these unloved locked tokens as compliant equity assets, allowing traditional financial institutions to enter and purchase. Tokens that retail investors would not directly buy suddenly transformed into stocks, which institutional investors could buy compliantly, and retail investors could also enter through brokers to take over. The chips were successfully distributed, the U.S. Securities and Exchange Commission permitted it all, and the project parties successfully cashed out, while the ones taking over were, from the start, the ones being harvested.

By the way, Naval entered the crypto space early and is well aware of this.

After the San Francisco venture capital circle witnessed the success of this play, they directly scaled it to the trillion-dollar capital market. Private venture capital products for retail investors became the first channel, while NASDAQ’s revision of listing rules became the second channel.

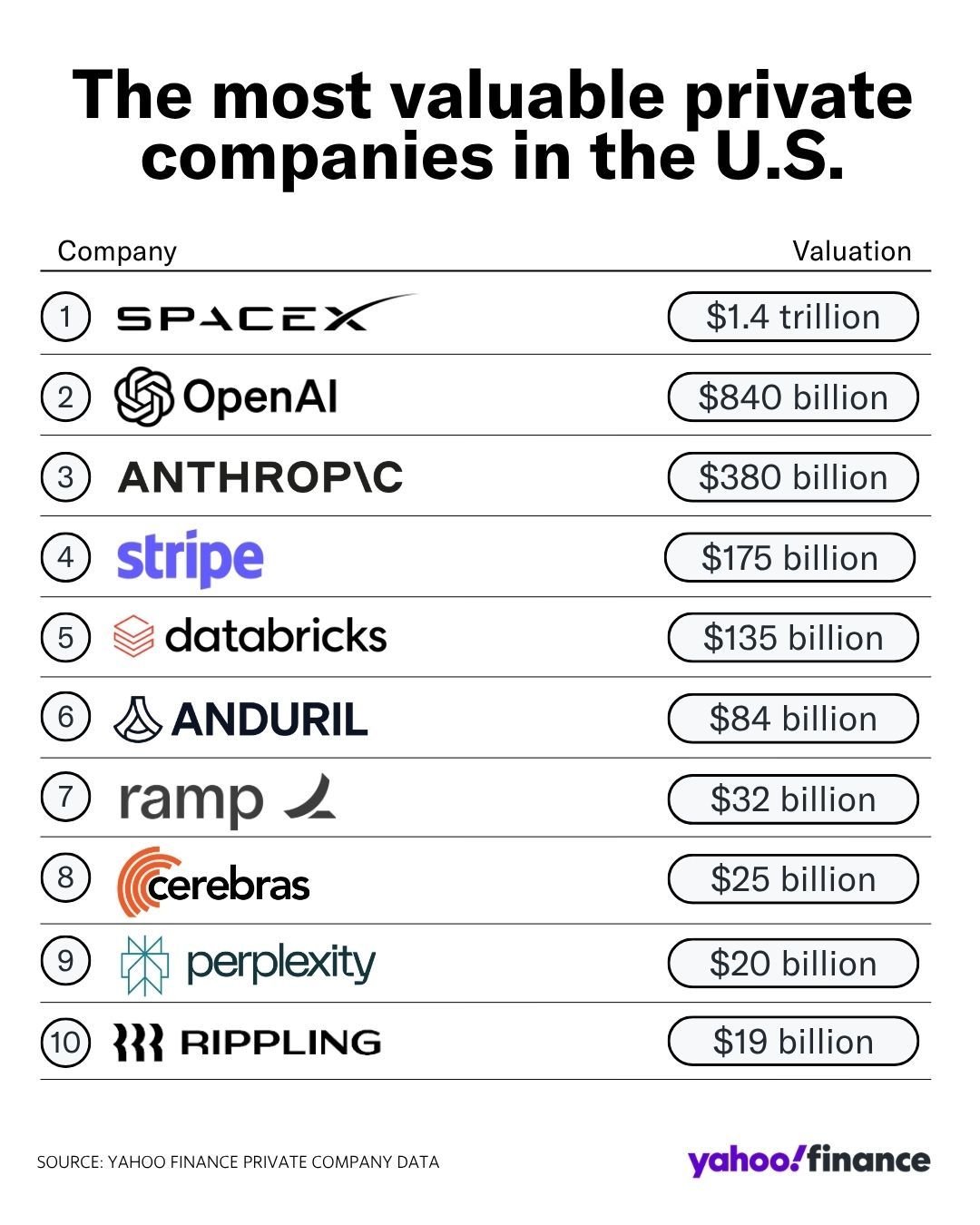

NASDAQ's planned new regulations state that companies with very few publicly circulating shares will have their index weights amplified by five times, updated during each quarterly index adjustment. Taking SpaceX as an example: when this company goes public, only 5% of its shares will be circulating, with a total valuation of $1.75 trillion. According to the new regulations, passive index funds are required to purchase that stock based on a weight of $438 billion; this operation will be executed 15 days after listing, completely bypassing market value assessment. The internal equity lockup period will precisely align with the next index adjustment date; at that time, the weight will be maximized, and passive funds will make large purchases unconditionally, while insiders legally cash out. SpaceX plans to go public mid-year, and the end of the year coincides with index adjustments, making the entire process seamlessly fitting.

Originally, index funds served as a protective umbrella for ordinary retail investors against internal capital harvesting; now they have become tools for capital to cash out. Your retirement savings are being harvested by this mechanism.

The tactics of the crypto circle and the venture capital circle are completely consistent: insiders first hold low-priced positions in markets inaccessible to retail investors; assets appreciate; the purchasing power of the original market cannot support high-level selling; then they create a newly packaged vehicle to connect with another batch of funds—specifically, pensions and passive index funds that rely on rule-based blind buying without considering prices; internal capital successfully escapes, and new retail investors take over the high-priced chips. The entire process is completely legal because the packaging design itself is compliant; regulatory agencies are largely ineffective because this institutional harvesting does not count as a violation within the rules.

The Final Consequences

Current various chaos all stem from this: Sam Altman facing public backlash, self-driving vehicles being maliciously damaged, and data centers encountering public protests. Ordinary people initiating resistance do not understand the theory of exit liquidity, but they feel directly that the world is divided into two classes: early entrants and later takers; the speed at which the class divide is expanding far exceeds what can be compensated by personal struggle, talent, and opportunity.

The elite tech class has demonstrated through reality that the public capital of ordinary people is being continuously harvested to create excess wealth for already advantaged groups.

The K-shaped wealth divide will become increasingly extreme. What follows will not be a normal market correction since the premise of a market correction is that participants still believe the current rules are fair.

Today, the public’s resistance and conflict have essentially evolved into political contradictions at the societal level.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。