Authorship: Rust, the Uncle Who Does Not Understand the Classics

The vast majority of people analyzing business models have never understood one thing: a great organization is essentially an extension of a great person.

A few days ago, the famous AI blogger Dwarkesh Patel invited Jensen Huang for nearly two hours of discussion.

This interview was different from previous ones. Dwarkesh's questions were sharp: "NVIDIA is just a software company; it relies on TSMC for chips, buys memory from Samsung, and hands assembly work to Taiwanese ODMs. If software is being commoditized by AI, how can you avoid being commoditized? TPU has trained Claude and Gemini—what if GPUs are replaceable? Anthropic has given its largest compute order to Google—how do you explain that? Why not do cloud yourself? Why still sell chips to China?"

Jensen Huang faced the onslaught, almost losing control during the segment about China. He told Dwarkesh, "You are not talking to someone who gives up as soon as they wake up."

But the true essence of the entire conversation, which can answer Dwarkesh's question—Can NVIDIA's moat be sustained?—might be hidden in Huang's repeated statement:

Do as much as needed, as little as possible.

Translated, this conveys a more colloquial meaning: do what you must do and do it to the utmost; minimize what is optional.

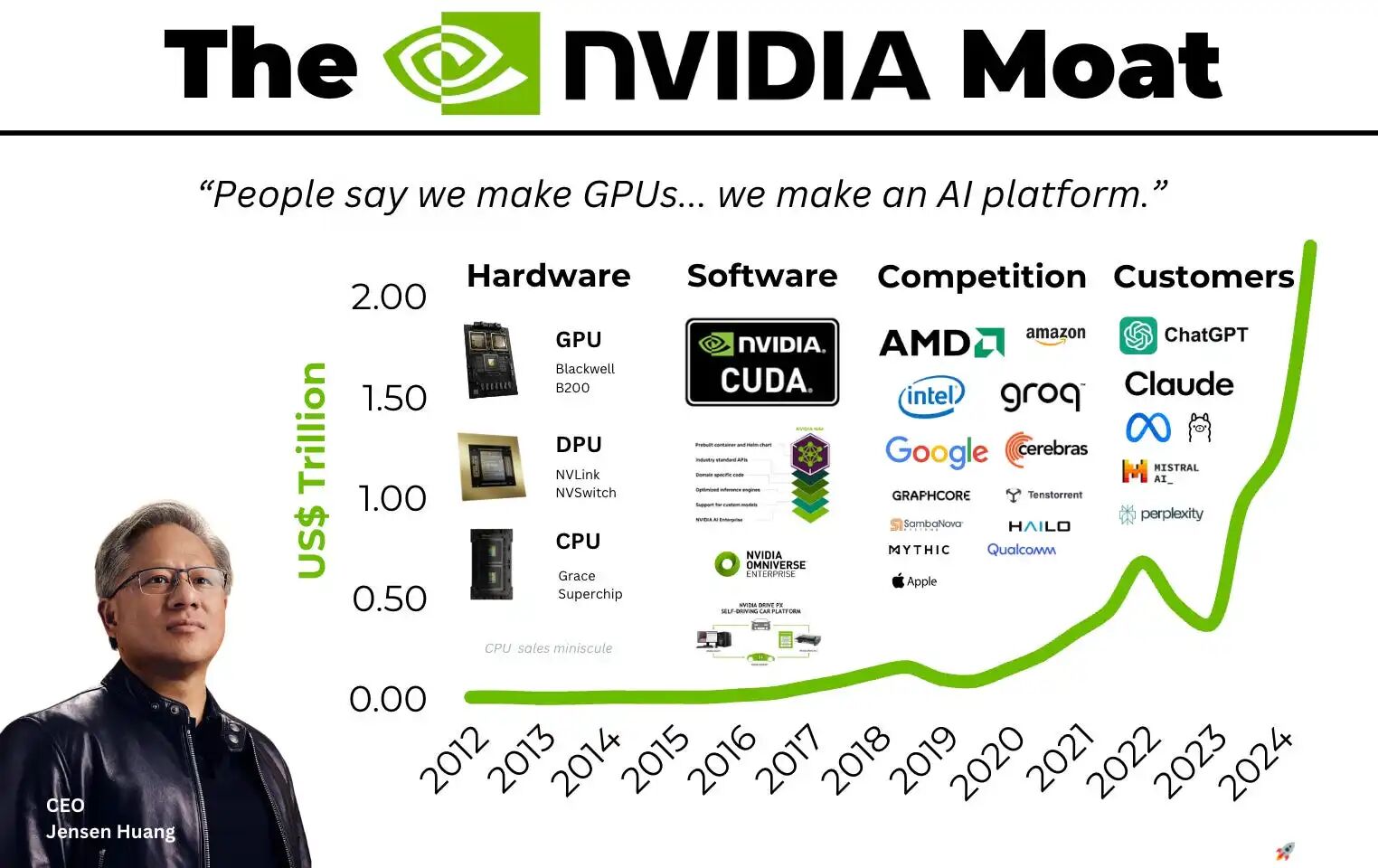

For a $4 trillion company, at the core of all its moat analysis, supply chain discussions, and ecological flywheel metaphors, what truly holds everything together is this phrase. NVIDIA's moat is Jensen Huang's extreme business philosophy.

I. Why One Sentence Can Support $4 Trillion

Huang's statement may sound unremarkable, like an inspirational quote on a coffee mug or a PowerPoint slide from the first day of an MBA class.

But if you savor it, it locks in two things at once: do what you must with utmost effort, and resolutely avoid what you should not do. Both ends must hold; if either end falters, the whole structure collapses.

Strategic master Michael Porter made it clear in his 1996 article "What is Strategy": the essence of strategy is choosing what not to do. Without trade-offs, there is no strategy. Things everyone can do are not called strategy; they are called operations.

Most companies fail not due to lack of effort but because they try to want too much at once. They want market share, profit, new stories, old businesses, vertical integration, and platform ecosystems. Each item seems reasonable when viewed individually, but when combined, they lead to slow suicide.

Porter cited a grisly example. In 1993, Continental Airlines launched Continental Lite, trying to be both a low-cost airline and a traditional airline. As a result, low-priced seats couldn't support frequent flyer points, and traditional routes couldn't support quick boarding. Trying to do both, they ended up achieving neither; the CEO stepped down, and hundreds of millions of dollars were wasted.

"Without trade-offs, there is no choice; without choice, there is no strategy." These are Porter's exact words. Any good idea that everyone can execute will be quickly replicated, and in the end, everyone competes solely on operational efficiency.

The brilliance of Huang's statement lies not in "doing less," but in nailing both ends down at the same time. He is not saying, "NVIDIA is very disciplined." He is saying: I have already drawn the red line in advance, identifying which things only NVIDIA can do and must do; and which things, even if NVIDIA can do, it will not do, leaving them for others.

This constraint is proactive. It changes the organization’s daily question from "Should we do this?" to "How well can we do this?" The former drains decision-making power, while the latter allows for compound growth.

The internet as we know it is being brought to an end by AI, along with its underlying logic of making money online.

Two Americans looking at AI in China see the same thing.

II. NVIDIA Once Died for "Doing More"

In 1995, NVIDIA launched its first chip, the NV1.

It was a "chip that wanted to do everything." 2D graphics, 3D graphics, audio processing, and game controller interfaces all packed into one silicon chip. The architecture used quadrilateral rendering, which was different from the triangular rendering everyone else was using. Huang and his team thought this was more "elegant."

As a result, Microsoft launched DirectX, which only supported triangles. Overnight, the industry standards turned against NVIDIA.

250,000 NV1 chips were shipped to Diamond Multimedia. 249,000 were returned.

By spring 1996, NVIDIA had only 30 days of cash left and couldn’t afford to turn on all the lights in the office. Huang flew to Tokyo to meet Sega's president, Hisashi Yuujirou, and personally told him: “We chose the wrong technical route, your NV2 project is beyond saving, can you please let us keep the $5 million we paid?”

Such words are usually hard for an ordinary CEO to utter. Sega agreed.

Huang returned to Silicon Valley, slashed the team from 100 to 40 people, and gave up all ambitions, putting the remaining resources into a chip that only does one thing. This chip was called RIVA 128, compatible with mainstream triangle graphics, not doing audio, not doing controllers, not doing fantasies.

In August 1997, RIVA 128 was shipped, with only one month's salary left in the bank. It sold a million units in four months.

29 years later, Huang is still using that unofficial motto: "We are 30 days away from bankruptcy."

This is not just a cultural slogan; it is a wound that is all too real. The mistake with the NV1 was not that the technology was insufficient; it was that they wanted to do too much. When you try to meet all standards simultaneously, you cannot excel at any one of them.

A company that engraved "almost died from greed" into its entrepreneurial memory instinctively asks during any decision: "Does this have to be done by me?"

III. CUDA: Do What "No One Else Will Do"

In 2006, NVIDIA launched CUDA.

For ten consecutive years, analysts in every earnings conference call asked the same question: When will this thing become profitable? Wall Street repeatedly reminded Huang that his gross margin was being dragged down by CUDA, and the stock price was suffering because of it.

Huang's answer remained unchanged over the decade: If we don’t do it, no one else will.

The other side of the phrase "Do as much as needed, as little as possible" is fully realized here in CUDA. It is not just about "cutting out the excess." It also involves the more difficult matter of doing what must be done in years when no one believes you can succeed.

CUDA was not pursued because it was likely to be profitable. It was because NVIDIA was the only company willing to lose money for ten years to make it happen. This is precisely why it has become a moat today.

Huang clarified this further in the interview. He distinguished between two types of things:

The first type is what no one else will do if NVIDIA does not do it. Accelerated computing platforms, CUDA, NVLink, CUDA-X libraries, cuLitho computing lithography. Huang's exact words were: "If we don’t do it, I am completely certain no one will." These types need to be pursued with heavy investment, bearing losses.

The second type is what others will naturally do if NVIDIA does not do it. Cloud computing is a typical example. If you don’t do it, AWS will do it, Azure will do it, OCI will do it. Therefore, NVIDIA's choice is to invest in CoreWeave, Nscale, and Nebius, rather than becoming a massive cloud provider themselves.

In 2024, NVIDIA will have hundreds of billions of dollars on its balance sheet. Theoretically, this is enough to establish a cloud, engage in finance, and create models. But Huang made it clear: We are not a financial intermediary; our business model needs to be as simple as possible, supporting the ecosystem and allowing others to do what they can do.

Behind this lies a counterintuitive principle of capital allocation: always concentrate the most scarce resources (the founder's attention, the organization’s top talents) on the one thing that only you can do in the world. Other things should either be invested in others or simply ignored.

Most companies miscalculate this. They see others making money and feel they should also take a share; they see cash on hand and feel they must invest it. But what Huang sees is another matter: NVIDIA’s rhythm of releasing a new architecture every year—Vera Rubin → Vera Rubin Ultra → Feynman— is like clockwork. This in itself is a moat. To maintain this rhythm, the founder's attention that can be spared is zero.

Another counterintuitive point: Huang said in the interview that he never "picks winners." Among the 60 early 3D graphics companies, the least favored was NVIDIA. "I am humble enough to recognize that." So he doesn't bet on a single model company; he invests in all major foundational model companies. OpenAI, Anthropic, and xAI are all on the list.

Not picking winners is because the cost of picking wrong is too high. Another deeper logic: a company that supports everyone else will, in turn, become a company that everyone cannot do without.

Using AI, you’ve tracked down 5,000 impressive individuals, but your world is narrow.

The collapse of the middle management: two thousand years of management history culminates in an AI cycle.

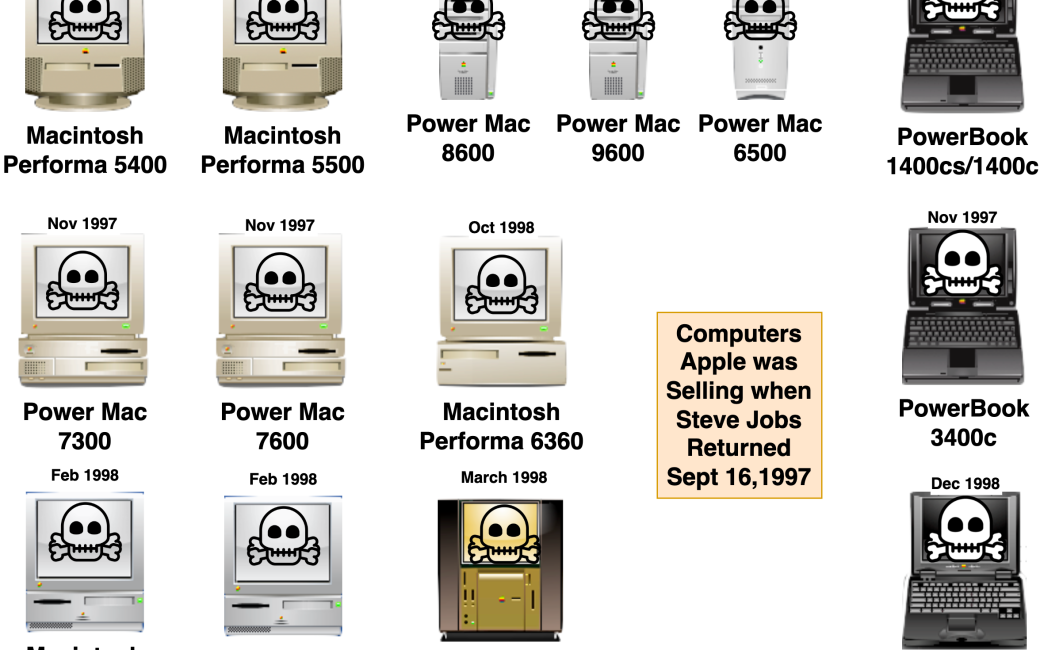

Jobs' product line when he returned to Apple in 1997.

IV. The Same Philosophy, Two Extreme Interpretations

"Do as much as needed, as little as possible" is not a set action. It is a way of thinking. The key lies in how you define "must."

We can look at two extreme examples.

TSMC: Drawing the Red Line of "Must Not Do" as Strictly as Possible

When Morris Chang founded TSMC in 1987, he established a rule: never compete with customers.

Before that, the semiconductor industry only had the IDM model. Intel, Motorola, and Texas Instruments designed and produced their chips; nobody did pure foundry. Chang's bet was that a large number of design companies would emerge, and they would need a manufacturing partner that would never compete with them for business.

This rule seems like a conscious abandonment of a significant chunk of profit. The profit from designing chips is very high; why not do it?

But precisely this "conscious abandonment" red line made TSMC a partner that Apple, NVIDIA, AMD, and Qualcomm all dared to trust. Would you dare hand your design over to Intel for manufacturing? Intel also makes CPUs; would you trust them? Hand it over to Samsung? Samsung makes phones and DRAM too; would you trust them?

TSMC's credibility does not stem from what it does right; it stems from what it promises not to do.

"We never compete with our customers." This sentence is worth two trillion dollars.

Decades ago, Chang realized one thing: a moat is sometimes not about what you can do, but about what you commit not to do.

Musk: Pushing the Boundary of "Must Do It Ourselves" as Far as Possible

On the surface, Musk's approach seems completely opposite to TSMC and NVIDIA.

SpaceX manufactures 80% of its rocket parts in-house. Tesla is vertically integrated across batteries, motors, software, and charging networks. In 2026, Musk is still promoting TeraFab, aiming to manufacture chips himself. This is not about "doing less," but about "doing more."

However, if you look closely at his logic, the core is the same.

In 2002, Musk wanted to buy Russian second-hand intercontinental ballistic missiles to modify for rockets, and the price was quoted at $20 million each. He used first principles to calculate: the raw materials for a rocket—titanium, copper, carbon fiber, aerospace-grade aluminum—total only 2% of the rocket’s selling price in the commodities market.

This 2% and the 98% gap is Musk's famous "idiot factor."

In Musk's definition, this is "must do it ourselves." Because if not done in-house, he would never reach Mars. The pricing logic of the space industry is built on bureaucracy, not physics. His definition of "must" is much broader than Huang’s, yet the decision-making logic is completely consistent.

Anything that I cannot accomplish without doing it myself, I won’t let anyone else handle. Anything that does not affect the core mission, I won’t touch.

Tesla does not have 4S stores (the dealership network is unnecessary), does not run TV ads (the brand relies on product self-promotion), and did not produce low-end models until the Model 3 (insisting on first making high-end products before moving downmarket). SpaceX does not go public (not letting short-term financial pressures distort decisions).

Each decision to "not do" is aimed at allowing the "must do" to be done to greater extremes.

This is two directions of the same philosophy

Chang is the "I vow not to do" type, trading an absolute red line for total trust in the ecosystem.

Musk is the "I must do it myself" type, using first principles to calculate "what can only be accomplished by myself."

Huang stands between the two but defines his "must" most exquisitely: only do the conversion from "electronic to Token," and only focus on that layer. Everything upstream goes to TSMC, SK Hynix, Samsung, ASML; everything downstream goes to AWS, Azure, CoreWeave, OpenAI, Anthropic. Every participating entity in the ecological layers can earn money, and each is willing to place advance orders for NVIDIA's next generation of architecture.

In 1997, when Jobs returned to the nearly bankrupt Apple, the first thing he did was this. He reduced 350 SKUs to 10. Retained two rows and two columns of four products: professional desktop, professional portable, consumer desktop, consumer portable.

Later, Jobs had a saying: "I am as proud of what we do not do as I am of what we do."

This is four ways of saying the same thing.

Retiring at 65 has gradually become an illusion; being 35 and 85 is becoming the new normal.

Stop being friends with time; in the age of AI, "space" is your friend for getting rich.

V. Why is this Simple Philosophy So Difficult to Learn?

The reasoning is so clear. Why can most companies not learn it?

First level of difficulty: Selections let immediate opportunities slip away.

You see competitors entering a new market, you have cash on hand, and you have a team. Your sales tell you that this opportunity has a "window of only 6 months." How can you not be tempted?

But Porter already said: in organizations, "not choosing" is more easily forgiven than "choosing wrong." Making a mistake is a personal responsibility, but missing an opportunity is due to market changes. Thus, most managers tend to do a bit of everything; it does not matter if nothing is done splendidly, at least nothing is missed.

The endpoint of this decision-making model is mediocrity.

Second level of difficulty: Judging "what is essential" requires a nearly brutal clarity.

In 1995, Huang judged NV1 as "must do it," and he was wrong; they nearly died. In 2006, he judged CUDA as "must do it," and he was right; it won the future.

This kind of judgment does not have a formula. It requires three things: an understanding of the underlying physical laws of the industry, foresight into the direction of ecological evolution, and honesty about one’s true capability limits.

Most people deceive themselves on the third point. Every VP believes their department can do everything, and every CEO thinks "adding one more business to try can’t hurt." The clarity of the third point usually only appears during two moments: when a company has only 30 days left until bankruptcy, and when a founder has experienced a company being 30 days from bankruptcy.

Third level of difficulty: "Reducing the excess" contradicts the inherent power of the organization.

Large organizations naturally expand outward. Each department wants to grow bigger, every new executive wants to leave "their business," and annual budget meetings tend to add projects rather than reduce them. A company must proactively relinquish a piece of business, even if objectively it has reasons to hand over to ecosystem partners, fighting not just external competitors but also all the internal power inertia.

This is also why this philosophy can almost only be executed by founders. Professional managers cannot fight against the organization’s expansion instinct; their reward function is "do more things."

Fourth level of difficulty: You must accept that others earn money that should be yours.

NVIDIA lets CoreWeave earn the profits from turning GPUs into leasing services, allows SK Hynix to earn profits from HBM memory, and allows TSMC to earn fees from advanced process foundry.

Every item in the accounts is "could have been mine," but Huang understands one thing: if I go after that money, I lose the focus to earn the money that truly belongs to me.

This is a form of counterintuitive restraint. It is hardest in the startup phase since every penny is tempting. It becomes easier during the maturity phase because you finally become large enough not to care about the gross profits of single business units.

Not understanding the classics: AI consumes not only software but also the entire internet.

Stop learning from Buffett: the main battlefield for getting rich has shifted, but no one has told you.

Dwarkesh's entire focus was on one question, which was the title of the interview.

VI. The Redistribution of Capabilities is Built on Clear Restraint

In Dwarkesh's interview, you will find that nearly all of his questions essentially ask the same thing: what allows NVIDIA's moat to continue? The threats from TPU, the betrayal of Anthropic, China's pursuit, large customers’ self-research, ASIC’s 65% gross margins... each one like a knife.

Dwarkesh's question actually captures a real phenomenon: NVIDIA indeed does not have a "moat" in the traditional sense; it does not have its own factories, its own memory, its own cloud, or its own models.

But Huang's answers rendered this question ineffective.

Huang's answers ultimately converge to one point: the moat is not in any single technology, in any supply chain contract, or in a commitment of $250 billion upstream. The moat lies in NVIDIA's continuous clarity regarding "what it should do and what it should not do."

It is not because NVIDIA possesses any secret assets, but because it thinks about "moat" in a different way. The real moat is not how much you can control, but: what will the world lose when you are absent?

If CUDA disappears, the entire AI training ecosystem would fall into chaos. If NVIDIA's chip roadmap disappears, the world's largest data centers would be unable to plan their infrastructure investments. If NVIDIA's ability to gather supply chain participants at the GTC events disappears, the entire industry's information alignment would fracture.

These are the real moats.

NVIDIA is able to achieve all of this precisely because it does not attempt to do everything. It concentrates all its efforts on that core area of "if I do not do it, no one else will," and allows the entire ecosystem to revolve around it.

Do as much as needed, as little as possible. This is not conservatism; it is a multiplicative mindset.

In an era of increasingly refined division of labor, what is most powerful is not total control but a clear understanding of which segment you pertain to, and then executing that segment to the point that no one can replace you.

Do what you must do to the utmost. Reduce what is optional to the minimum.

The most challenging aspect of this era is not the lack of capability; it is the abundance of opportunities.

AI makes every capability accessible. Writing, drawing, analyzing, programming, filming, translating—things that used to require professional training can now be accomplished with a prompt delivering a decent version. "Doing a bit of everything" has become hugely tempting. Every content creator, every entrepreneur, every worker faces the same allure: since the marginal cost is so low, wouldn’t not doing one more thing be a loss?

It is precisely in such an era that the weight of the phrase "Do as much as needed, as little as possible" begins to become unusual.

Capabilities are being redistributed, but how much is allocated does not depend on how much you can seize, but rather on how much you are willing to let go.

Your time, attention, and resources are being fragmented daily by the illusion of "doing one more thing won’t hurt." What truly determines how far you go is never what you have done.

It is whether you have the courage to eliminate, one by one, the things that should not be done. 【Understanding】

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。