Written by: Grandpa Zuo Web3

Liquidity exchanges for yield, understand RWA path in one article

The world feels the same temperature, both on-chain and off-chain are pursuing liquidity. Looking east, the stock market is competing for bank wealth management, looking west, AI giants are scrambling for money to save themselves.

After 2008, banks were trapped in institutional cages, but "private credit" became an important source of corporate loans.

After 2018, PE, BDC (Business Development Company), and private credit took away $300 billion from banks, most of which flowed to internet giants represented by SaaS.

Subsequently, during the pandemic in 2020, the global financial market completely split, and everyone needed to find their own anchors again. The Chinese stock market embraced hard tech concepts while the American stock market went all-in on AI; simply having targets is useless without corresponding liquidity organizational methods.

Liquidity first comes from monetary easing; China implemented three cuts in reserve requirements in 2020, and the Federal Reserve restarted QE and ultra-low interest rates, leading to "everyone buying funds," which once made Zhang Kun a Weibo celebrity.

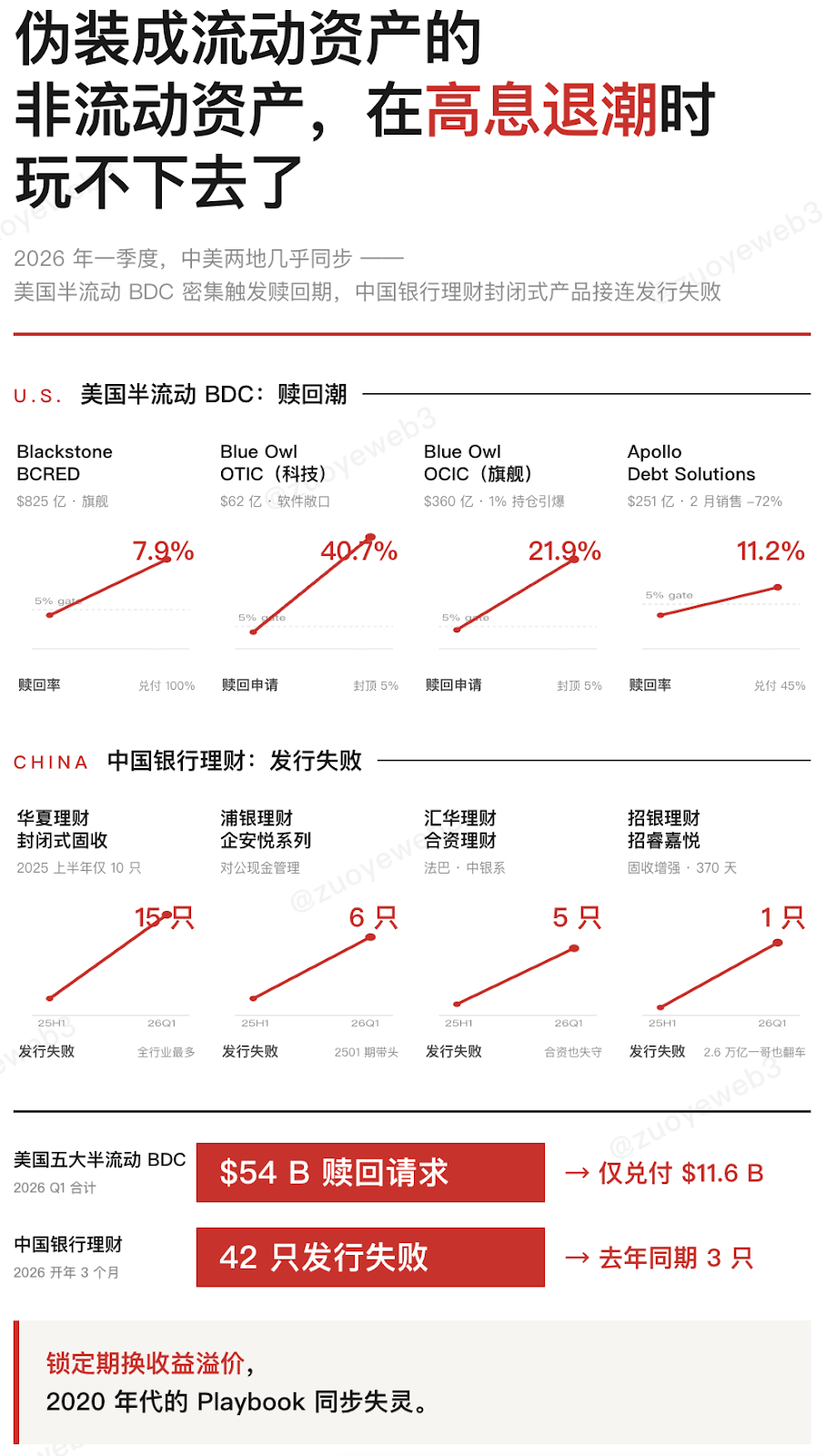

But in 2026, the sound of cannons in the Gulf shattered the illusions; the user mentality changed. Compared to future yields, accessible cash became more important, seeking liquidity became the grand backdrop for the current wave of RWA.

Wall Street started the on-chain process, needing to convert a variety of products’ AUM into trading volume; otherwise, repayment pressure would directly collapse them.

Assets are not money; liquidity has trading value. This is the significant meaning of RWAfi — being on-chain is a liability, and only when traded does it become an asset.

Image Explanation: Liquidity is more important than yield; image source: @zuoyeweb3

Or to say, the market is reassessing the pricing of "liquidity premium." The redemption wave in American private credit and the sluggish issuance of Chinese banks' closed-end income products both demonstrate that liquidity is vying for the position of yield.

This transmission or shadow shows that the global financial market needs to look for new connectors. Document No. 42 leaves a gap for "domestic assets + overseas issuance," and the clear legislation is likely a way out for income arrangements, with mutual understanding, fighting but not breaking.

Undoubtedly, blockchain will definitely be the future of global finance, but on-chain finance in the U.S. is Canton, while on-chain finance in China is digital RMB. Global finance is the territory of Ethereum and Solana; the more opposition there is, the more the need for peace hotels.

Seeking liquidity globally is the ultimate significance of this round of RWAfi.

For profit, seeking quality assets

What has happened will not be forgotten; it's just hard to remember.

Many people's impression of RWA still lingers on the early memories of "everything on-chain." However, Aave co-founder Stani has a special affection for putting photovoltaics on-chain. On one hand, he warns that DeFi might become a passive position for private credit liquidity; on the other hand, he passionately encourages DeFi to rush towards solar energy and other $30 trillion abundant assets.

Unfortunately, the current mainstream practices in DeFi are precisely "private credit" and all electronic asset types, including U.S. Treasuries, U.S. stocks, CLOs (Collateralized Loan Obligations), and even OnRe packaging real-world reinsurance business on-chain to attract on-chain liquidity for income.

Physical types of RWA have already become a thing of the past; the re-linking of entities in the energy sector can only be said to hold promise for the future.

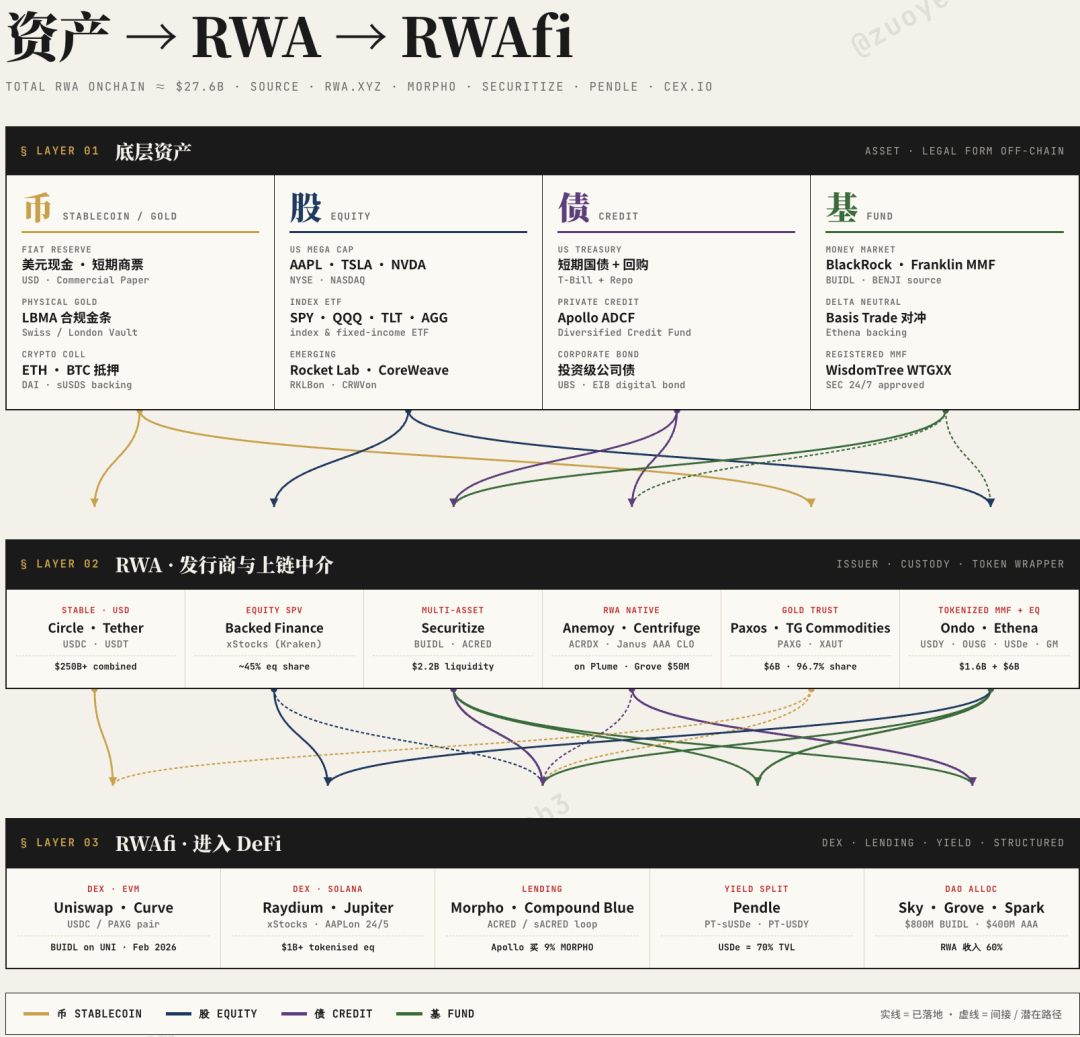

Image Explanation: Panorama of RWA equity and debt funds; image source: @zuoyeweb3

In summary, RWA is a type of asset based on assets, which is very rare. ETH is based on people's use, BNB is based on Binance's trading volume, and BTC is based on decentralized narratives.

This is where the problem lies. RWA project parties seem eager to bring liquidity by putting certain assets on-chain, but just like "antiques were luxury goods at the time," high-quality projects off-chain do not lack liquidity; being on-chain does not equal liquidity.

Being on-chain is a technical category, while liquidity is a financial category, and they should not be confused.

Only in one situation can being on-chain bring liquidity: when the action of going on-chain meets the expected reach of liquidity, for instance, wealth management products that can only be bought by institutional-level clients off-chain can be issued as stablecoin vaults accessible to retail investors.

Accordingly, the framework of RWA can be understood in three layers, from top to bottom being the asset (Asset) layer, tokenized RWA assets, and liquidity RWAfi.

- Assets

- RWA: Asset-based assets

- RWAfi: Liquidity-bearing asset-based assets

Image Explanation: Three-layer division of RWA; image source: @zuoyeweb3

Excluding physical assets and photovoltaics, the types of assets in the real world can be divided into four categories: stablecoins, stocks, debt, and funds. The stablecoins anchored to the U.S. dollar, such as USDT/USDC, and U.S. stocks are the most familiar to people.

However, it can be predicted that debt and fund types will have stronger development potential because both currently lack liquidity, and merely switching the purchasing process of institutional clients to on-chain does not allow retail investors to participate directly.

A typical example is the tokenized fund GUSDT and GHKDT sold by Hashkey, where users can neither trade nor withdraw; overall, it lags behind the U.S. market by one version.

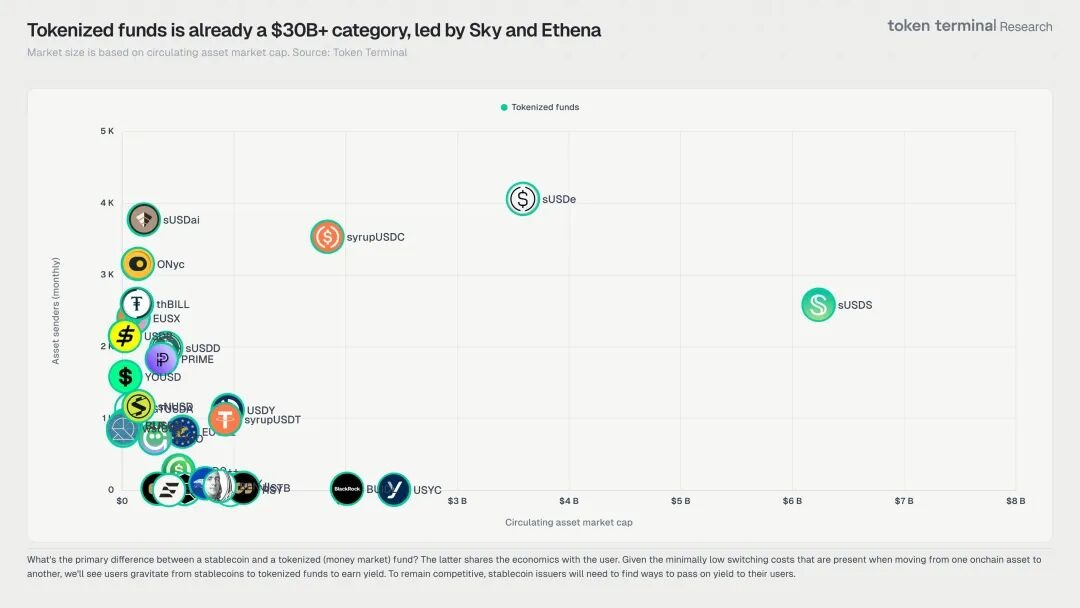

At least in BlackRock's view, tokenized funds will disrupt Wall Street just as the internet disrupted the postal system. This principle is not complicated; tokenized funds target the global market and will eliminate existing national boundaries.

Of course, currencies, stocks, debts, and funds can be infinitely subdivided. For example, stablecoins can be divided into anchoring objects (dollar > crypto assets) or types (dollar > non-dollar), and debt can be split by issuer (government > local > enterprise) or by collateral (CLO underlining loans > CDO underlining real estate).

But none of this is important; there is no need to research the institutional differences between the U.S., South Shenzhen, and Singapore extensively; countless research reports cover this. These details are not the core concerns of capital operations and inflows and outflows.

Just keep an eye on the technical service providers that help link real assets on-chain, especially the practices of U.S.-based Securites, SuperState, Canton, and Ondo. They will help us clear all obstacles.

After the SEC released guidelines explaining the applicability of securities law to tokenized products, Securites welcomed Nasdaq's former Spot Bitcoin ETF listing head Giang Bui and former SEC official Brett Redfearn joining.

Beyond the revolving door of politics and business, traditional finance also participates.

Traditional asset management company Invesco purchased SuperState's $USTB tokenized treasury product, while Circle's USYC product even surpassed BlackRock's BUIDL and other giants in terms of issuance.

Moreover, the Canton chain, backed by Goldman Sachs, can "defeat" Ethereum in undertaking DTCC's on-chain experiment.

In terms of technical paradigm, the RWA intermediate layer has completely degraded into a color-filling game for institutions, and while competing for the four major product lines of RWA, clear spheres of influence have yet to emerge.

However, at the RWAfi level, DeFi shows a more tolerant acceptance attitude. For them, allowing more assets to be liquid is also beneficial to themselves.

But for RWA to leap to RWAfi, initial liquidity needs to be artificially created; if it merely enters the existing stack as a base asset, it still faces the dilemma of "no one cares."

Where does liquidity come from?

On-chain liquidity becomes high premium products.

If RWA is prepared to seek liquidity from DeFi, then a 10% yield is the baseline; compared to less than 4% from U.S. Treasuries, it is practically impossible for existing RWA to make up the gap, let alone achieve higher returns, as retail investors have little motivation to buy in.

Therefore, sand will be mixed in to raise the yield.

- Implied extraction costs of funds, or time constraints, such as Ethena's sUSDe redemption period has just changed from 7 days to dynamic, with underlying assets including more non-U.S. Treasury assets. Essentially, it involves leveraging user funds, but without the high volatility of perpetual contracts.

- Containing more subsidy components, such as self-token sales revenue, which is essentially a controllable "funding scheme," with underlying assets including U.S. Treasuries ensuring minimum repayments, attracting liquidity with high interest, and then locking it in, allowing project parties to earn scale income from funding.

However, practices from 2025/26, from Huma to Pharos and products like Bitway, show that the gap between off-chain and on-chain always exists. Non-real-time third-party audits merely add legitimacy to "illiquid" rather than enhance on-chain liquidity.

Although they all appear to be income-bearing stablecoins, each protocol's underlying structure remains difficult to analyze.

Image Explanation: Tokenized funds; image source: @tokenterminal

Furthermore, by adding leverage to TradFi, they also create seemingly on-chain liquidity, with Hyperliquid's Trade.xyz being the most typical case, which expands into the RWAfi field by increasing trading leverage for oil and precious metals.

However, we must recognize that the liquidity generated by trading and the illiquidity of private credit are two sides of the same crisis. This principle is not complicated; any mature market requires three elements:

- Low-cost funds

- High-leverage strategies

- Large-scale markets

Warren Buffett uses insurance float and extremely long-term time leverage to dominate the U.S. financial market; similarly, the U.S. banking industry's resistance to stablecoin income mechanisms is also a desire to monopolize customers' demand deposits.

However, the cost of funds needed to sustain existence in the crypto industry’s perpetual contracts is very high, which is also the price of being perpetual; otherwise, the delta-neutral mechanism wouldn't come into play, but now Ethena is partially abandoning fee arbitrage strategies.

Even projects like Saturn and APyx have started to use MicroStrategy stocks ($MSTR) as underlying assets to build on-chain income products, indicating a crisis in crypto trading.

While praising the increase in trading volume for Trade.xyz, let us not forget the crisis signals after Binance greatly lowered VIP standards.

In summary, the current problem lies in relying on U.S. Treasuries + token subsidies + market-making strategies to fill the 10% and U.S. Treasury gap, even hoping to push higher, with bizarre fundraising efforts on Phraos and Gaib chains targeting third-world markets.

Thus, payment, fund, and bond markets that are not directly leveraged trading are more critical for RWAfi development, such as payment companies' residual funds and Galaxy's CLO loans using BTC as collateral.

Especially the latter, Galaxy's VC investment in Arch Lending allows users to borrow stablecoins with over-collateralized BTC, while Galaxy packages Arch's debts into CLO products, and Sky injects capital through Grove to obtain corresponding yields. In this process:

- Users: No need to sell BTC, avoiding capital gains tax.

- Arch: Obtains institutional-level "low-cost funds" without needing to sell coins to support scale expansion.

- Galaxy: Expands a "large-scale market," as CLO products underlining BTC are easier to be accepted by DeFi protocols.

- Sky/Grove: "High-leverage strategies," expecting returns on RWA assets beyond U.S. Treasuries to be higher.

Of course, things will not be perfect; the success of this case is not unrelated to Galaxy's multiple interests. But looking at the entire RWAfi market, this is a better and safer strategy to raise yield.

Galaxy's CLO products underpinning BTC as collateral was mentioned earlier, and we should also consider the path of U.S. stocks as collateral in DeFi.

U.S. Treasuries, U.S. dollars, and U.S. stocks, as currently the strongest financial assets in the world, are not developing at the same pace. U.S. Treasuries and dollars support the surge of dollar stablecoins and TMMF (tokenized money market funds), but the tokenization of U.S. stocks is only just beginning.

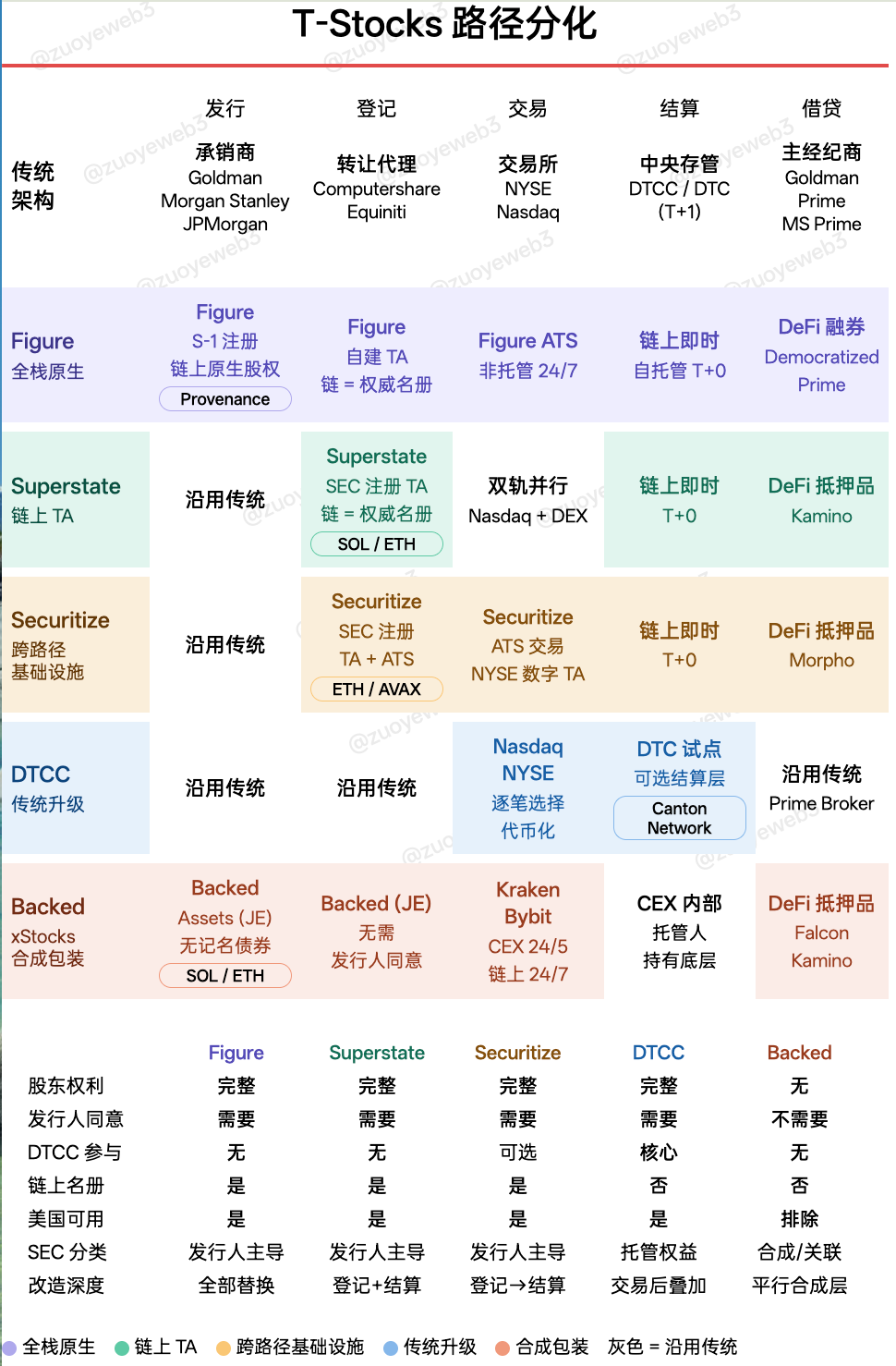

Image Explanation: T-Stocks path differentiation; image source: @zuoyeweb3

Beyond the conventional processes of issuing, managing, custodian, auditing, clearing, etc., U.S. stock leveraged trading categories are also extraordinarily rich. Based on the rules of long and short-term holding, from margin trading by brokers to leveraged ETF products and more flexible options, they can basically meet all kinds of retail needs.

If scaled to institutional or professional investors, futures are already close to the perpetual contract concept commonly used in the crypto circle.

Additionally, even if highly concentrated in the "seven sisters," U.S. stocks themselves also possess more abundant liquidity. Technologies like T+0 are unrelated to asset issuance, no longer over-discussed, and DeFi's opportunity exists in becoming a lending service provider.

It's not the stocks seeking liquidity on-chain, but rather DeFi actively including U.S. stock assets.

There is an unconventional assumption here: DeFi is indeed desperately lacking high-quality assets to expand market size. Otherwise, BTCFi wouldn’t be repeatedly reinvented, but major holders prioritize protecting capital, and the gap remains unfilled.

Projects like Kamino and Morpho vaults can use U.S. stocks under the guarantee of SuperState as more flexible reallocation assets, bridging the bids of TradFi and DeFi.

Comparatively, U.S. Treasuries are the cornerstone of risk-free yields, while U.S. stocks are more volatile assets with stronger liquidity.

In summary, blockchain cannot only serve as a technical facility for TradFi; it needs to reverse-utilize TradFi assets to expand itself.

Conclusion

The road to large-scale markets.

Due to space limitations, there will be no extensive discussion on stablecoins. On one hand, stablecoins have already grown to a large-scale market with the most abundant liquidity. On the other hand, stablecoin income, foreign exchange (non-dollar stablecoins), and the stability of assets anchored on-chain are all evolving, and will be dealt with separately in future writings.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。