Author: a16z

Translation: Deep Tide TechFlow

Deep Tide Insights: MIT claims that 95% of corporate generative AI pilots fail to convert, but a16z uses firsthand data from portfolio companies to directly contradict this assertion. 29% of Fortune 500 and 19% of Global 2000 are already paying customers of leading AI startups, and programming tools are increasing the efficiency of the best engineers by 10 to 20 times. This 23,928-word report is based on internal data, revealing which AI scenarios truly generate value and which are still concept hype.

There are many speculations about how much progress AI has made in large enterprises, but most existing information consists only of self-reported AI usage or surveys capturing qualitative buyer sentiments rather than hard data. Furthermore, a few existing studies assert that AI performs poorly in enterprises, the most notable being MIT's study claiming that 95% of generative AI pilots failed to convert.

Based on our internal data and conversations with corporate executives, we found this statistic difficult to believe. We have been closely tracking where AI sees the most adoption and where ROI is most clear, compiling hard data on what actually works in enterprise AI.

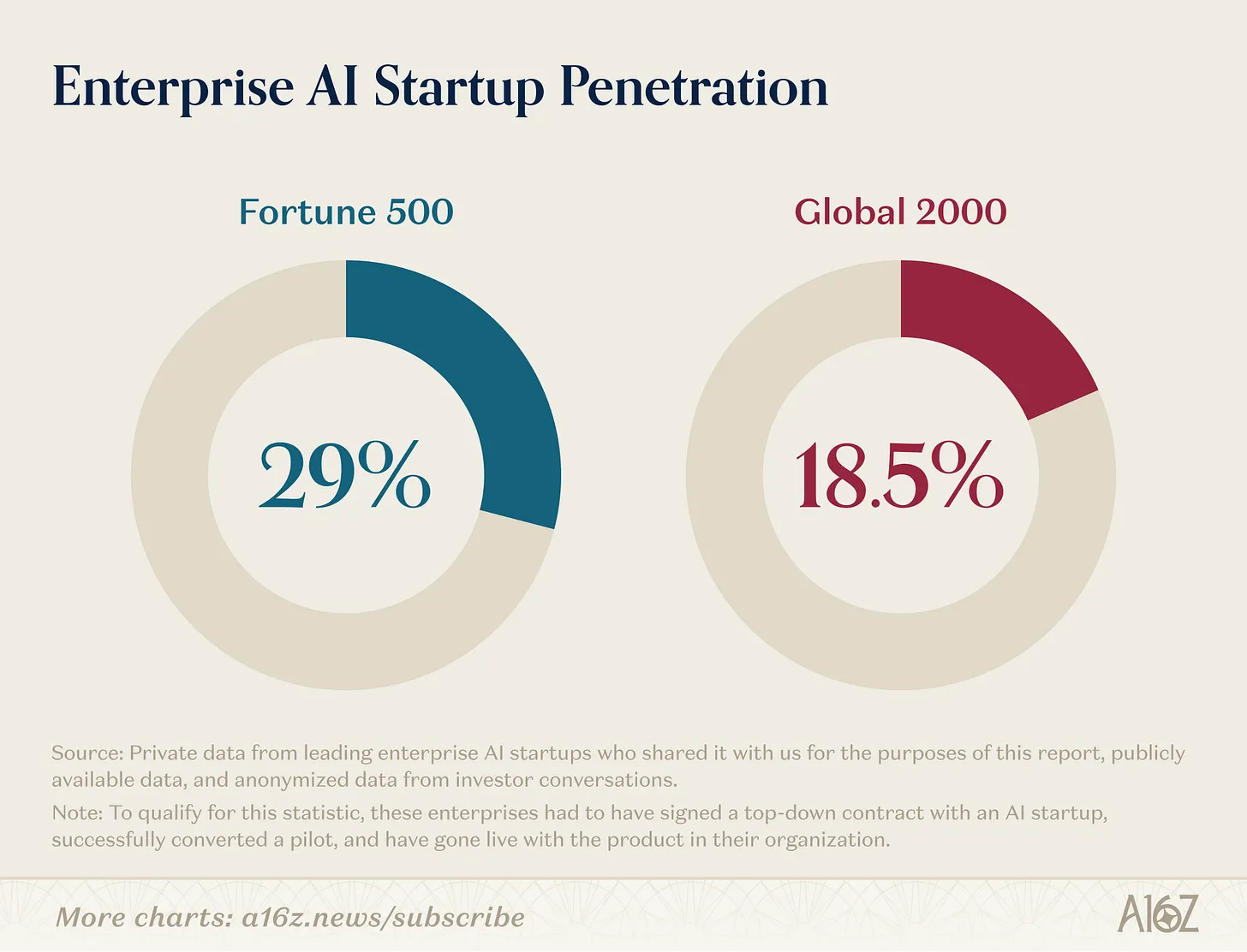

AI Penetration Rate in Enterprises

According to our analysis, 29% of Fortune 500 and approximately 19% of Global 2000 are active paying customers of leading AI startups.

To meet this statistic, these companies must have signed top-down contracts with AI startups, successfully converted pilots, and deployed products within their organizations.

Reaching such a penetration level in such a short time is remarkable, as Fortune 500 companies are not known for being technology early adopters. Historically, many startups had to first sell to other startups to gain early momentum, and it would take years before they could sign their first enterprise contracts, needing more revenue and time to ultimately sign clients of Fortune 500 scale.

AI has disrupted this norm. When OpenAI launched ChatGPT in November 2022, it instantly showcased the potential of AI to consumers and businesses alike. This unleashed a storm of interest in AI that previous generations of technology had never sparked, with large enterprises more willing than ever to place early bets on new products. The result: just over three years later, nearly one-third of Fortune 500 and one-fifth of Global 2000 have real enterprise AI deployments within their organizations.

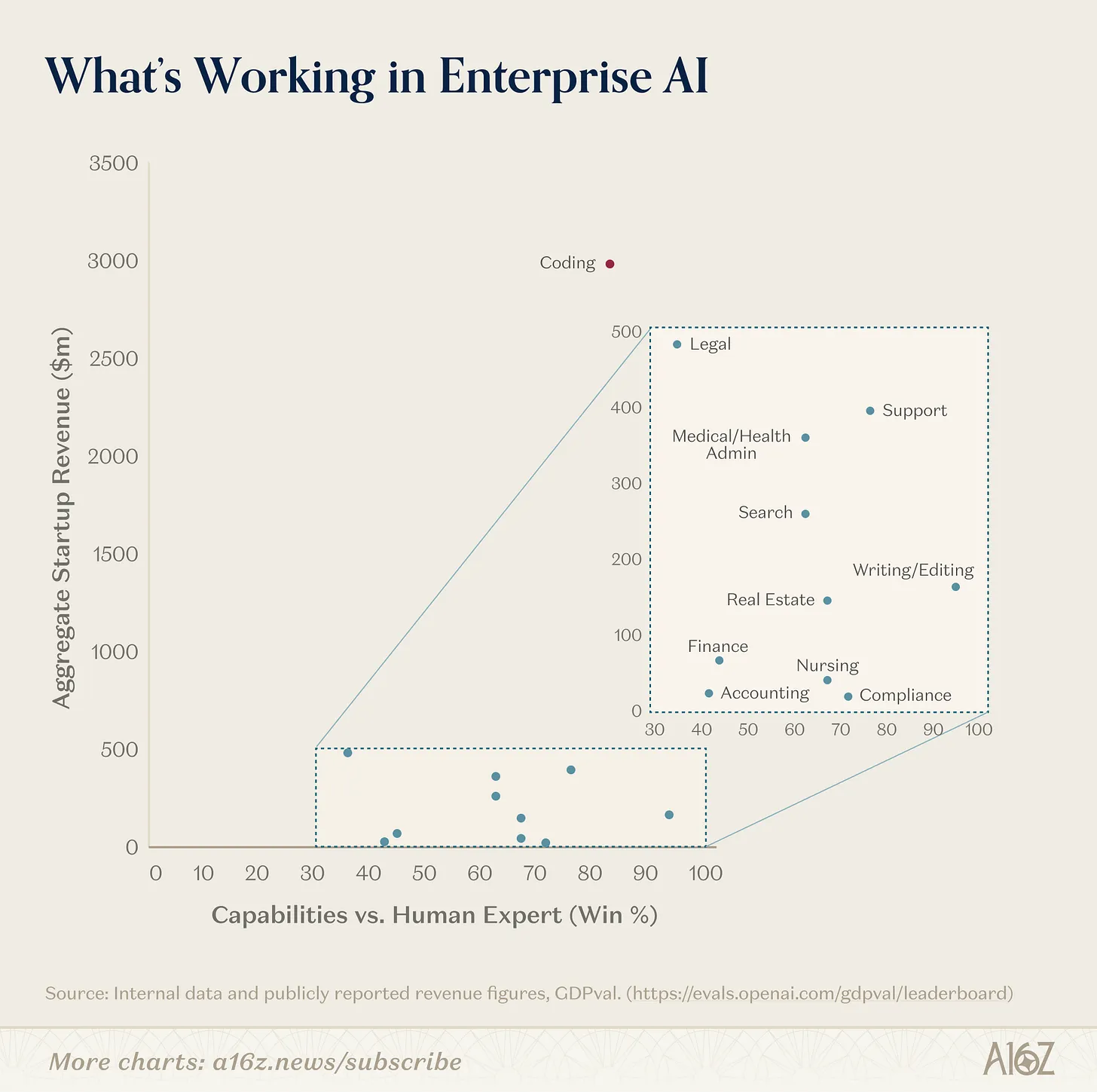

What Works in Enterprise AI

Where is this adoption happening the fastest, and how does it map to the types of work that models are inherently better at doing?

We found that the most indicative assessment method is to layer the revenue momentum of various use cases onto the theoretical capabilities defined by GDPval, which is a well-known benchmark from OpenAI that assesses model capabilities on tasks of real-world economic value. For us, these two factors summarize not only how well models can perform but also how much value they are currently proving to deliver. This makes them very illustrative of where AI adoption is today, where it may head, and where AI remains unadopted despite model capability maturity.

Where is Enterprise AI Providing the Most Value Today?

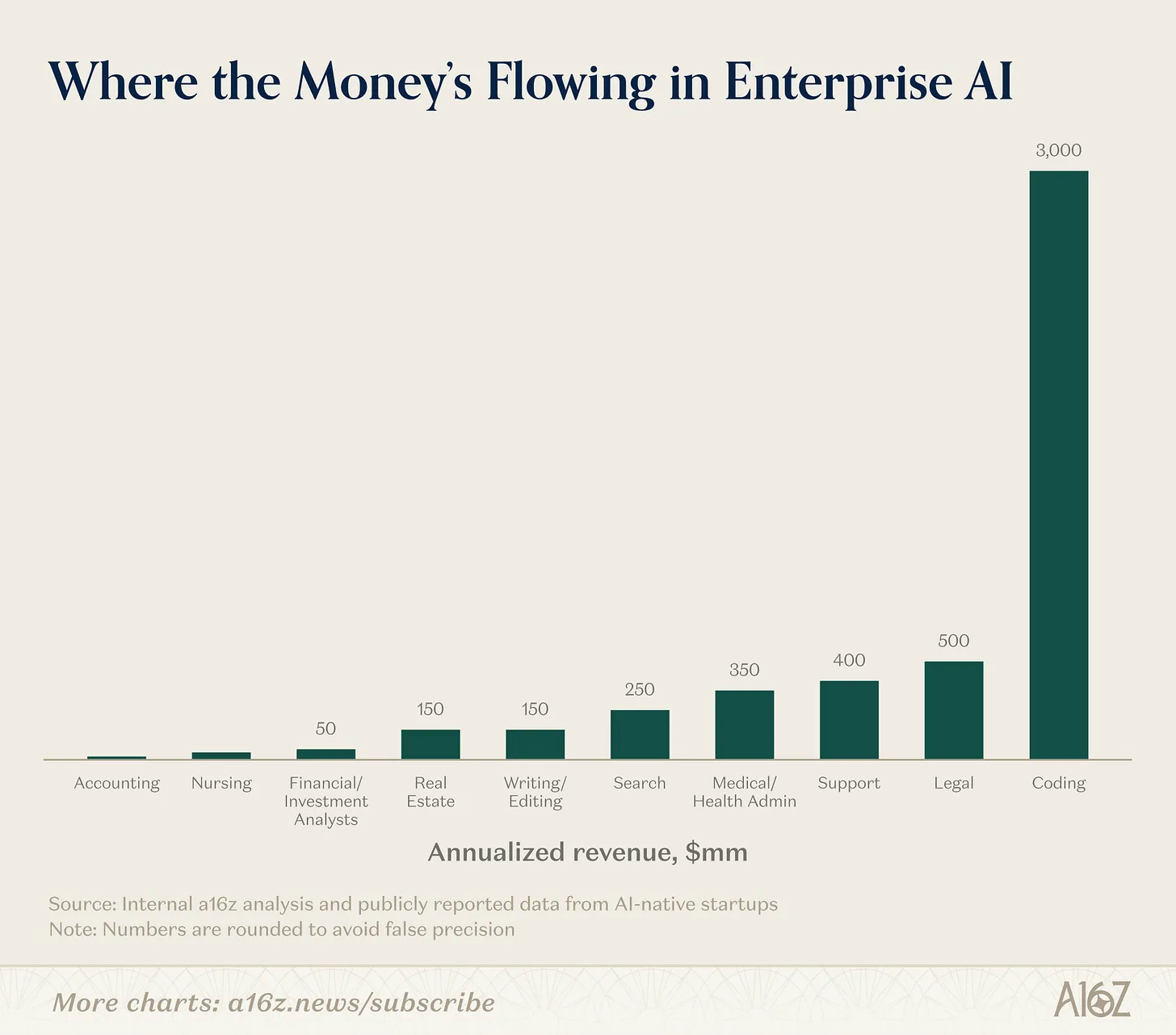

In terms of revenue momentum, corporate adoption of AI is dominated by a set of clear use cases and industries. Programming, support, and search so far represent the bulk of use cases (with programming even an order of magnitude outlier within this group), while the tech, legal, and healthcare sectors are the most eager to adopt AI.

Programming: Programming is the leading use case for AI, nearly reaching an order of magnitude. This is evident in the explosive growth reported by companies like Cursor and the super-fast growth of tools like Claude Code and Codex. These growth rates are exceeding nearly everyone's most optimistic predictions, and to this point, the vast majority of Fortune 500/Global 2000 adopting AI tools have been in coding.

In many ways, programming represents the ideal use case for AI, across both technical capabilities and enterprise market acceptance. Code is data-intensive, meaning there is ample high-quality code online for models to train on. It is also text-based, making it easy for models to parse. It is precise and unambiguous, with strict syntax and predictable outcomes. Crucially, it is verifiable: anyone can run it and know if it works, creating a tight feedback loop for models to learn and improve.

From a business perspective, it is also a great application. We have consistently heard from portfolio companies that the productivity levels of their best engineers have increased by 10 to 20 times with AI coding tools. Hiring engineers has always been challenging and expensive, so anything that increases their productivity has a clear ROI—the significant lift that AI coding tools provide creates a huge incentive for adoption. Engineers also tend to be early adopters seeking the best tools, as programming is a more solitary task compared to most corporate work; they find the best tools and adopt them without being encumbered by the coordination and bureaucracy that plagues many other functions within a company.

Additionally, programming tools do not need to complete the task 100% end-to-end to provide added value, as any acceleration (e.g., finding bugs, generating boilerplate code) still saves time and is useful. Given that programming has tightly knit people-in-the-loop workflows, developers still oversee the development process today; these tools provide space for human judgement to review, edit, and iterate while accelerating output. This both increases corporate confidence and smoothens the path to adoption.

Programming capabilities are improving exponentially, with every lab clearly focused on winning code as a use case. This has profound implications. Code is upstream of all other applications because it is a core building block of any software, hence the acceleration of AI on code should ripple out to accelerate every other domain. The lowered barriers to building in these domains unlock new opportunities that can be solved with AI, but the same accessibility makes it more critical than ever for startups to build lasting competitive advantages.

Support: Support sits at the opposite end of the spectrum, contrasting with code. While software engineering typically garners the most investment and attention within organizations, support is often overlooked. The work in support organizations is back-end, entry-level work that is often outsourced to offshore companies or business process outsourcers (BPO), as companies find it too cumbersome and complex to manage themselves.

AI has proven to excel at managing this work for several reasons. First, much of the nature of support interactions is time-bound with constrained intents (e.g., issuing refunds), providing agents with clearly defined problems to handle. Support is also one of the few functions where the tasks involved are clearly defined. Support teams are large and highly fluid, requiring new representatives to be trained quickly and in a standardized manner. To this end, they have clearly articulated standard operating procedures (SOP) that guide each representative's work. These SOP create clear rules and guidelines that an AI agent can mimic. This sets it apart from most other corporate work, which typically lasts longer, is less clearly defined, and involves more stakeholders beyond the customer and service representative.

Support is also one of the clearest enterprise functions to demonstrate ROI. Support operates on quantifiable metrics: the number of tickets answered, customers' CSAT (satisfaction) scores, and resolution rates. The status quo pitted against any A/B tests of AI agents yields favorable results for AI agents: they answer more tickets, improve resolution rates, and elevate consumer satisfaction scores—all at lower costs. Since most support is already outsourced to BPOs, adopting AI solutions requires limited change management, making the path to adoption easier.

Support does not need to be 100% accurate to be useful, as it has natural exits to humans (e.g., "I'm transferring you to a manager"). This allows sales cycles to move faster and makes piloting AI support agents relatively low risk; in the worst case, 100% of cases will simply escalate and be resolved by a human.

Finally, support is inherently transactional. Customers do not care who is on the other end, which means support does not require any human relationships that are difficult for AI to replicate. These characteristics explain why companies like Decagon and Sierra are growing so rapidly, as well as more vertically-specific support participants like Salient and HappyRobot.

Search: The last category with a clear enterprise market pull is search. The primary use case of ChatGPT itself is search, so the impact of search may profoundly intertwine with revenue and usage for ChatGPT, where it may be greatly underestimated.

AI search as a category is so expansive that it has enabled many independent, large startups to emerge. One of the primary pain points inside many enterprises is enabling employees to easily locate and extract relevant information across disparate collections in their systems. Glean thrives as a leading startup vendor for this use case. Many large industries also operate based on very specific industry information (both internal and external), with companies like Harvey (starting in legal search) and OpenEvidence (starting in medical search) thriving by building core products around this.

Industries

Technology: The most common industry adopting AI so far is the tech industry. ChatGPT itself reports that 27% of business users come from tech, with many early customers of companies like Cursor, Decagon, and Glean being tech firms. Given that tech is almost always an early adopter and is the industry that birthed the AI wave, this is not surprising at all.

What is more surprising is that markets not historically considered as early adopters have proven to be eager this time.

Legal: The legal industry is surprisingly one of the leading sectors in AI. Law has historically been seen as a difficult market for software, with long timelines and buyers less technically savvy.

This is because traditional enterprise software offers limited value to lawyers: static workflow tools do not accelerate the unstructured, nuanced work that lawyers typically do. But AI has clarified the value proposition for technology to lawyers. AI excels at parsing dense text, reasoning over large bodies of text, and summarizing and drafting responses—all of which are tasks lawyers often perform. AI now frequently serves as a co-pilot to enhance individual lawyers' productivity, but it has started to expand beyond that: in some cases, it can actually generate revenue by allowing firms to handle more cases (as in the case of Eve, which specializes in plaintiff law).

The results are evident. Harvey reported about $200 million in annual recurring revenue (ARR) within three years of its founding, and companies like Eve have over 450 clients and are reaching a $1 billion valuation this fall.

Healthcare: Healthcare is another market responding to AI in ways that traditional software never did. Companies like Abridge, Ambience Healthcare, OpenEvidence, and Tennr are growing rapidly based on discrete use cases such as medical records, medical search, or back-office automation of Byzantine rules on how healthcare is delivered and paid.

Healthcare has historically been slower to adopt software because 1) high-skilled and complex work does not map well to problems traditional workflow software can solve, and 2) the dominance of systems like Epic in recording EHR has squeezed out entirely new software vendors. However, with AI, companies are able to take on discrete manual labor tasks that circumvent system records by either replacing administrative work (e.g., medical record clerks) or enhancing higher-value work that doctors are doing. This work is unique enough that it does not require tearing down and replacing EHRs, allowing these firms to scale quickly without needing to displace existing software vendors.

A Few Notes on Analysis

These estimates are best guesses. It may underestimate the revenue generated in each category and overstate model capabilities.

We may have underestimated revenue because:

The revenue analysis is purely based on which sectors and use cases succeeded enough to create large, standalone enterprise AI businesses, excluding the long tail of use cases that other startups are addressing.

Many of these markets also have significant non-startup participants generating substantial revenues (e.g., Codex/Claude Code in code, CoCounsel from Thomson Reuters in legal), but we focused the analysis on independent startup participants.

Many of the tasks articulated in our analysis may be integrated into the core products of model companies (e.g., search from ChatGPT and OpenAI), but have not been broken out and included in this analysis.

This analysis focuses on enterprise businesses rather than consumer or professional consumer businesses. There are successful businesses (e.g., Replit and Gamma in application generation and design) with a considerable number of business users, but they are currently mainly focused on consumers or professional consumers. Given that this analysis focuses on enterprise AI and where enterprises are getting value, we excluded consumer-dominated businesses.

In terms of capabilities, measuring AI's impact on different sectors of the economy is exceedingly difficult, although many economists are trying. The nature of work is inherently poorly defined and long-tailed, making it very hard to automate completely. It is also unclear today how much value enterprises can extract from partial automation—if AI can only do 50% of a human task, the importance of non-automatable tasks may increase as they become bottlenecks, raising their relative value. Thus, we may be overestimating the current state of capabilities since every incremental 1% of capability does not translate to 1% of economic value, but noting relative capabilities and how they improve with each new model release remains highly illustrative.

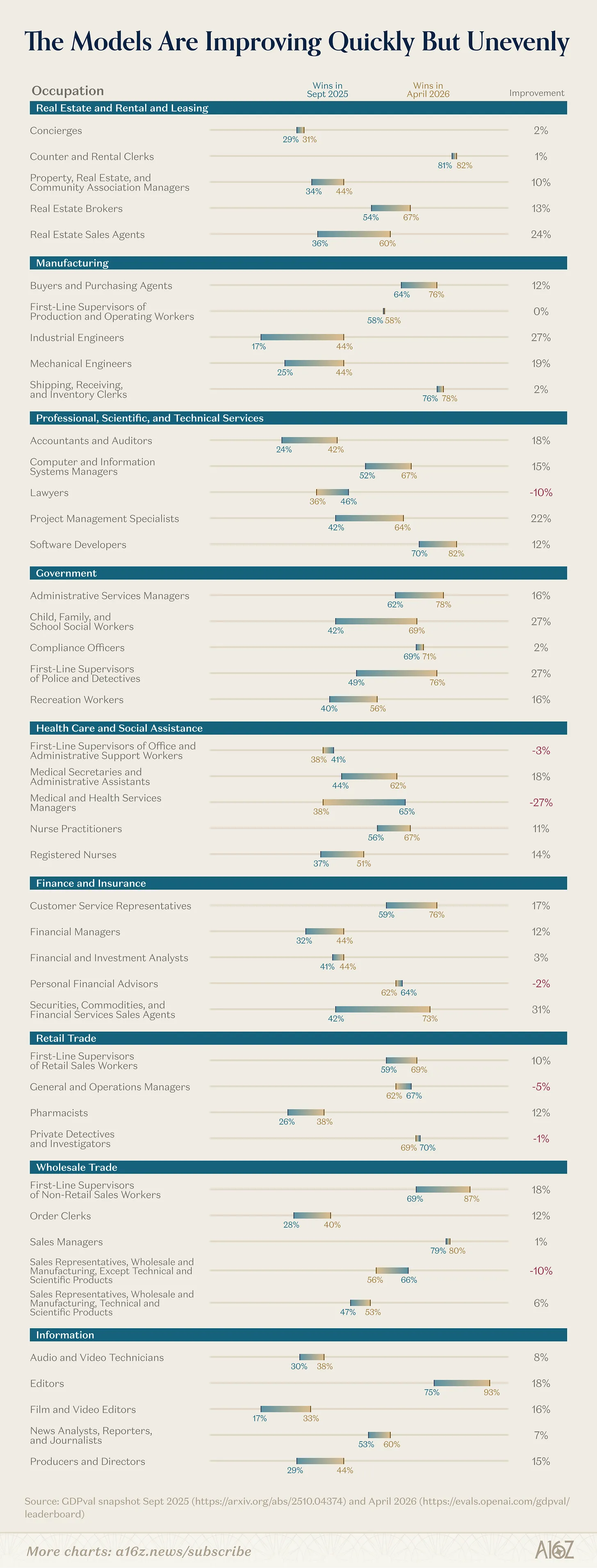

AI is Entering All Markets

This analysis measures the win rates of top evaluative models against human experts through GDPval benchmarking. Based on this, it is clear that since the fall of 2025, models have significantly improved in economically valuable work.

So why haven't we seen industries ranked high in this evaluation exhibit the same type of revenue momentum as others?

Industries that have enthusiastically adopted AI so far share several similarities: they are text-based, involve mechanistic and repetitive work, have humans in the loop involved to inject human judgement, have limited regulation, and possess clear verifiable end outputs (e.g., running code, resolved support tickets). Many industries do not have these attributes. They either deal with the physical world, heavily rely on interpersonal relationships, have significant coordination costs across multiple stakeholders, impose regulatory or compliance obstacles, or lack verifiable outcomes. While revenue momentum and model capabilities are clearly correlated, in fields where model capabilities theoretically sit below 50% win rates relative to humans (as is the case in law), companies like Harvey are still able to rapidly gain market share through co-pilot products to enhance individual legal work and then sustain improvements to their core products as models evolve.

The most notable finding here is that model capabilities are improving rapidly. Several areas have shown tremendous improvement over the past four months—accounting and auditing showing nearly a 20% jump in GDPval, and even areas like policing/detective work showing nearly a 30% improvement. We expect these jumps to lead to compelling new products and companies emerging in their respective fields. Furthermore, model companies have clearly stated their intentions to enhance the core capabilities for economically valuable work, performing core work on spreadsheets and financial workflows, using computers to deal with legacy systems and the tricky work in the industry, and making meaningful improvements on long-duration tasks. This opens up an entire class of new work that cannot be easily cut into small, digestible chunks.

Insights for Builders

Understanding where enterprises derive value and how they think about ROI—and which sectors are clearly seeing pull versus which are coming up—enables us to think more clearly about the opportunities for AI builders.

Serving buyers in technology, law, and healthcare is now clearly fertile ground, but we do not believe there will be a "winner" in every category. For example, in the legal domain, there are many types of lawyers—corporate counsel, law firms, patent lawyers, plaintiff lawyers, etc.—all with different workflows and distinct needs that companies can address. This is also true for healthcare, given the patchwork of different types of doctors, healthcare facilities, and so on.

Beyond these sectors, another fruitful way to think is about where capabilities are strengthening but where there are not yet breakthrough companies in revenue. Many current businesses were built before model capabilities truly unlocked products, but they have established enough technological infrastructure and customer/market awareness that they are best positioned when the unlock arrives.

Finally, it is important to focus on where labs are concentrating their latest research efforts on aspects of economically valuable work. With rapid improvements in long-term agents, serious investments in computer use, and research into reliable interfaces for non-text modalities (e.g., spreadsheets, presentations), an entire class of new startups will soon have the enabling infrastructure needed to generate meaningful enterprise value.

Data Methodology: This data is compiled from leading enterprise AI startups, including private data shared with us by companies for the purpose of this report, as well as publicly available data and anonymized data analyzed from the thousands of conversations we have had with startups and large enterprises at a16z.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。