Written by: Bu Shuqing

Source: Wall Street Journal

The U.S. Treasury market is facing potential selling pressure from overseas official investors, which has heightened market alertness.

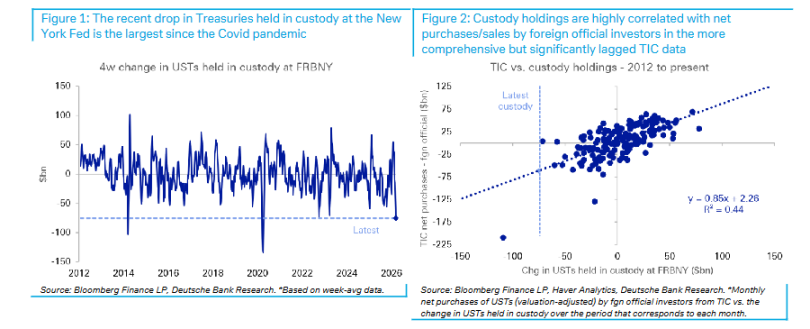

According to the Wind Trading Desk, a research report released by Deutsche Bank on March 23 shows that the holdings of U.S. Treasuries by foreign official accounts managed by the New York Fed have sharply decreased by $75 billion in the past four weeks, marking the largest monthly decline since the impact of the COVID-19 pandemic in 2020. Based on historical data models, this change indicates that the actual net selling of U.S. Treasuries by foreign official investors amounts to about $60 billion, also a record since the pandemic.

The above data corroborates the recent market trend of sharply rising U.S. Treasury yields, especially the abnormal increase in belly yields—while foreign official investors' holdings are precisely concentrated in that maturity segment. Deutsche Bank warns that if overseas demand continues to shrink, the "convenience yield" advantage of U.S. Treasuries will be eroded, posing substantial upward risks for long-end yields.

Custody Data Reveals Selling Signals

The most authoritative data source for tracking the movements of foreign official investors in U.S. Treasuries is the U.S. Treasury's TIC (Treasury International Capital) report, but this data has significant lags—the March data is not expected to be released until mid-May at the earliest.

As an alternative indicator, the H.4.1 report released by the New York Fed every Thursday includes a memorandum entry that records the face value of securities held in custody for foreign official and international accounts, with a lag of only one day. Deutsche Bank strategists Matthew Raskin, Steven Zeng, and Andrew Fu noted in the report that the latest H.4.1 data shows that, based on four-week averages, the holdings of U.S. Treasuries in foreign official accounts decreased by $75 billion, which not only represents the largest drop since March 2020 but also the second-largest decline in a single cycle in nearly a decade.

It is noteworthy that, unlike a similar situation in March 2023, the scale of FIMA repos did not rise concurrently this time, indicating that this round of reductions constitutes direct sales or non-renewals at maturity, rather than liquidity provision through repo operations with the Federal Reserve. Foreign reverse repos, foreign official deposits, and FIMA securities lending have also shown little change in the past month.

Custody Data Highly Correlated with TIC Data

To what extent do custody position data represent the overall changes in U.S. Treasury holdings by foreign official investors? Deutsche Bank has systematically validated this.

The report shows that over the past 15 years, the changes in custody positions have had a significantly notable correlation with the net purchasing volume of foreign officials in TIC data, explaining about 50% of the variations in the latter. Even when narrowing the sample to the period since 2019, to exclude potential interferences from reserve management model changes, the relationship remains robust.

Based on this historical relationship, the $75 billion decline in custody holdings corresponds to a net selling scale of about $60 billion by foreign officials. Deutsche Bank points out that this would be the largest net selling scale by foreign official accounts since the COVID-19 pandemic, with comparable cases only traceable back to December 2018.

Change in Fund Flows Against the Background of Foreign Exchange Interventions

The decline in U.S. Treasury holdings aligns closely with the market dynamics recently observed by Deutsche Bank's foreign exchange strategy team.

According to a previous report by Deutsche Bank's foreign exchange strategy team, against the backdrop of the outbreak of the Iran war and soaring oil prices, the dollar failed to strengthen as expected, partly due to massive foreign exchange interventions by several Asian central banks. Meanwhile, high-frequency ETF monitoring data from the team also shows a significant slowdown in foreign investment in dollar-denominated assets.

These two clues, together, point to one conclusion: Foreign official investors are reducing their allocation to dollar assets, and the selling of U.S. Treasuries is a direct reflection of this trend.

Continued Selling May Push Long-End Yields Up by More than 100 Basis Points

Deutsche Bank's analysis reveals a structural concern: U.S. Treasury yields have long benefited from the "convenience yield" brought about by the dollar's status as a reserve currency, and this advantage is now under pressure.

The report cites prior research by Deutsche Bank, indicating that the current 10-year U.S. Treasury yields are over 100 basis points lower than what is implied by the U.S. net international investment position (NIIP). Additionally, recent academic working papers estimate that the dollar's reserve currency status keeps U.S. long-term rates about 90 basis points below "normal levels."

Deutsche Bank warns that once foreign demand experiences sustained decline, the aforementioned convenience yield will face pressures to revert, and there will be substantial upward space for U.S. Treasury term premiums and overall yields, which will directly impact investors holding U.S. Treasuries.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。