Author: James | Snapcrackle

Translation: Shen Chao TechFlow

Shen Chao's Introduction: Most people's understanding of Tether is stuck three to five years ago—either as a stablecoin issuer or as a potential scam.

Neither framework explains its current true nature: 300 employees, annual profits exceeding $10 billion, holding more U.S. government bonds than Germany, and acquiring publicly listed agricultural companies.

This article is currently the most comprehensive dissection; by the end, you will find that it is no longer just a cryptocurrency company.

The full text is as follows:

The Billion-Dollar Machine That No One Updates Their Understanding About

A woman walks into a mobile phone recharge booth to buy phone credit. This recharge booth belongs to Tether.

In North Carolina, a former White House official is operating a federally regulated stablecoin supported by U.S. government bonds, which is also Tether.

A listed agricultural group has just replaced its board of directors, taking control of a company that didn’t exist twelve years ago. Still Tether.

Most people's understanding of Tether has lagged behind by three to five years.

Crypto media still treats it as a stablecoin issuer with trust issues. Mainstream media still considers it a possible scam. Neither framework offers an explanation for what Tether has actually become while everyone is still arguing over the old version.

What I discovered is a company with over $10 billion in profits last year, only 300 employees (planning to add another 150), and holding more U.S. government bonds than Germany—quietly building a tech group entirely funded by others' dollar interest.

This article is long. It has to be this way. The scale at which Tether operates requires you to hold several thoughts in your head simultaneously, some of which are contradictory.

Background

Tether reported over $13 billion in profits in 2024 and over $10 billion in 2025. About 300 employees, no external investors, and no transfer fees for USDT transactions in the secondary market (detailed later).

For reference: each employee generates about $33 million in profit per year.

Tether does not make money from ordinary USDT transfers like card networks do. There are issuance fees for direct minting and redemption (in some cases 0.1%, with minimum amounts), but that contributes zero to Tether's revenue from billions of point-to-point and exchange transfers that make up daily USDT transaction volume. At the company's inception in 2014, they discussed whether to charge 1 to 10 basis points per transaction like Visa and Mastercard.

They chose zero. Tether CEO Paolo Ardoino said in an interview that it was a deliberate decision to prioritize adoption over revenue.

The result is a business model that looks nothing like a payment company, although its functions mimic one. Tether makes money in a way similar to money market funds: absorbing dollars, investing in short-term U.S. Treasury bills, and keeping the earnings. The difference is that money market funds return most of their earnings to investors, while Tether keeps all of it.

As of December 31, 2025, Tether holds $122 billion in direct U.S. Treasury positions and an overall exposure of $141 billion in government bonds (including indirect positions through money market funds and repurchase agreements). At an approximately 5% Federal Reserve interest rate, just this item can generate around $6-7 billion in baseline earnings, aside from other income.

The rest comes from gold (end-of-year reserves of 127.5 tons, with Ardoino indicating that positions will increase to about 140 tons by early 2026), Bitcoin (96,184 coins), and an ever-growing portfolio of venture capital and commodity positions.

Tether estimates that by early 2026, global users will exceed 550 million, using a combination of on-chain wallet data and estimates from centralized platforms. This is not a verified independent number of individuals, but even after significant discounts, the scale is enormous. In 2025, USDT, valued at $13.3 trillion, flowed on-chain, with $156 billion below $1,000 in payments, which suggests real economic activity rather than mere trading.

McKinsey did a reality check on these figures—estimating that identifiable stablecoin real payment activities (B2B, remittances, settlements, card-linked spending) would annualize around $390 billion in 2025, far smaller than the raw figure for on-chain flow. There is a significant gap between "on-chain value transfer" and "actual goods and services payments."

Most of the balance sheet data comes from BDO's assurance report (including reasonable assurance business at year-end), but Tether still has not released fully audited financial statements in the way that typical publicly listed companies do. (This will be discussed in detail later.) However, the scale has been sufficiently corroborated by third-party data (on-chain analysis, Treasury market data, and counterparty confirmations from Cantor Fitzgerald), and to completely deny this would be absurd.

Money-Making Machine

The simplest way to understand Tether's economic model: imagine you operate a savings account for hundreds of millions of people, most of whom live in countries where their national currency is constantly depreciating. They deposit dollars, and you invest those dollars in the safest, most liquid tool on the planet (short-term U.S. Treasury bills), then give them a token that trades at $1 across every crypto exchange globally.

You keep all the interest.

Your customers don't mind because they weren’t earning interest on their own dollars anyway.

In Nigeria, the local financial system might only be 20% efficient; just holding a stable dollar is far more valuable than a 4% annual yield. In Argentina, where inflation rates have exceeded 100% in recent years, being able to hold something that does not depreciate is, in itself, a product. The earnings are Tether's revenue, but no one perceives it as such.

Ardoino has directly addressed this dynamic. In a podcast, he bluntly stated: the efficiency of the American financial system is already at 90%, and stablecoins only push it to 95%. In emerging markets with efficiencies of only 10-30%, USDT pushes it to 50%. He is not interested in the 5% profit margins of the U.S.; he is interested in the 30-40% profit margins everywhere else.

The usage pattern also tells an interesting story, and I guess this story will continue to evolve. Tether's Q4 2025 market report indicates that 63.6% of the value of transferred USDT in that quarter was single-asset transfers (pure dollar flows, not part of multi-token DeFi trading), with about 67% of the market cap remaining in low-turnover "savings" wallets. These two metrics do not measure the same thing, but together, they paint a picture of a product being used as currency rather than as a trading tool.

BIS researchers have independent support, finding that the use of stablecoins is more strongly correlated with remittance costs and trading demand than Bitcoin or Ethereum, especially in emerging and developing economies. (Not surprising to anyone.)

Standard Chartered predicts that stablecoin savings in emerging markets could increase significantly by 2028, believing that stablecoins effectively provide people with synthetic dollar bank accounts, which helps hundreds of millions of unbanked individuals. The value proposition is not yield, but escape from domestic currency depreciation and friction.

Tether spent less than $10 million on global marketing between 2020 and 2024, which is less than a Super Bowl advertisement.

Growth is organic and driven by crises. Ardoino said they even didn’t understand why market cap skyrocketed in 2020 until they did internal analysis years later: when COVID lockdowns shut down the physical black market for buying real dollars for residents in emerging economies, tech-savvy youth introduced USDT to their parents on smartphones. The global dollar black market shifted to Tether's track and hasn’t returned.

The issue of interest rate sensitivity is the most critical analytical issue regarding Tether's business, and the 2025 numbers provide genuine data. Profit fell from over $13 billion in 2024 to around $10 billion in 2025, a drop of about 23%. Tether's own disclosures show that government bonds and repurchase agreements contributed about $7 billion to 2024's profit. A rough model: a 200 basis point drop in direct Treasury yields on $122 billion could reduce annual interest income by about $2.4 billion. This matters, but it is not life-or-death, especially considering the hard asset hedges (gold and Bitcoin holdings often appreciate in a lowering interest rate environment). But it does mean that the earnings narrative part is a function of the interest rate cycle; Ardoino knows this. He explicitly described R&D investments in AI, energy, and telecommunications as hedges against eventual rate cuts.

What’s in (and not in) the Vault

Tether publishes quarterly attestations written by BDO Italia (one of the Big Five accounting firms). The quarterly reports provide a limited assurance under the ISAE 3000 framework. Year-end reports (including Q4 2024 and Q4 2025) are stricter: reasonable assurance engagement with stricter testing. But both differ from fully audited financial statements in the sense of publicly listed companies. BDO reviews Tether's statements regarding its reserves and reports any significant misrepresentation. It does not produce the comprehensive financial audit that institutional allocators typically require.

As of December 31, 2025, BDO’s reasonable assurance report confirmed: total assets exceeding $192.8 billion and total liabilities of $186.5 billion (with $186.4 billion related to issued tokens), with excess reserves of about $6.3 billion.

The Brookings Institution found that stablecoin issuers have become meaningful marginal buyers of U.S. Treasury bonds, actually ranking just behind a few foreign jurisdictions in a recent period. Tether alone holds more U.S. government bonds than Germany, the UAE, Spain, or Australia. This is no longer a crypto story. Tether has become part of the pipeline for short-term U.S. government debt demand.

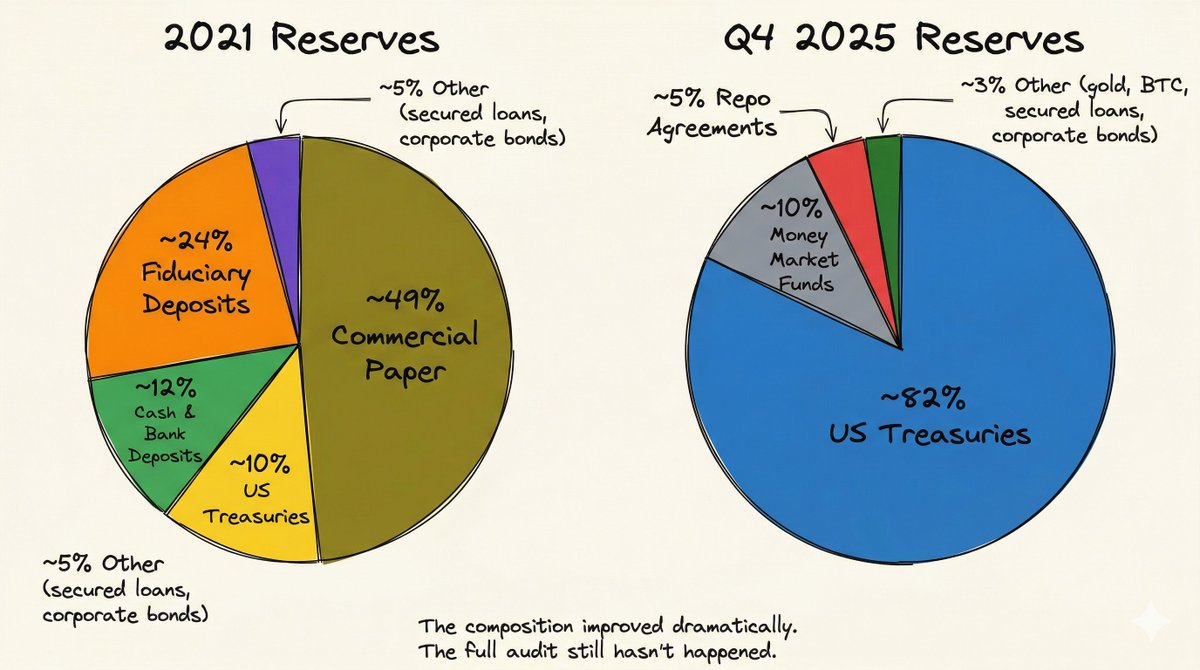

The composition of reserves also tells a story. According to the attestation documents and supplementary disclosures, approximately 82% is U.S. Treasury bonds, 10% is money market funds, 5% is repurchase agreements, with the remainder being gold, Bitcoin, secured loans, and corporate bonds.

In 2021, 49% of the reserves were commercial paper, with actual cash comprising about 3%.

This is a real transformation driven by regulatory pressure, well documented in the records. But the trust deficit is real and verifiable. A brief history:

In 2019, the New York Attorney General found that Bitfinex (Tether's sister exchange) had misappropriated $850 million from Tether's reserves to cover losses, with funds of the involved payment processor being seized by authorities. Tether settled for $18.5 million. The CFTC separately fined Tether $41 million for claiming that USDT was "fully backed" during the period when it "was not fully backed." At some point, Tether quietly changed the wording on its website from "100% backed by U.S. dollars" to "100% backed by our reserves, which may include affiliated entities."

Regarding the auditing issues, Ardoino has been more candid and defensive than most reports suggest. In a CNBC interview, when pressed why the Big Four have not audited Tether, he admitted: "They haven't even started looking at our numbers." He attributed the delay to the "reputational risks" created by the previous U.S. administration, which made major accounting firms cautious about engaging with crypto businesses. He then pointed out that Silicon Valley Bank, Silvergate, Credit Suisse, and Wirecard all had clean audits before their collapse.

In early 2025, Tether hired a new CFO specializing in "controversial audits" from LetterOne, signaling that they are preparing personnel for a final Big Four engagement. But "final" carries a lot of weight in that sentence.

Image: Tether Reserves

Tether's cash and bank deposits are close to zero.

The Q1 2025 attestation shows cash of $64 million (accounting for 0.04% of total assets). Treasury bills are the most liquid instruments on Earth, and Cantor Fitzgerald could convert positions to cash the same day. The risk argument is that, in severe stress events, Tether needs the Treasury bill market to function normally and needs Cantor to execute quickly.

In 2022, coordinated short-sellers triggered $7 billion in USDT redemptions within 48 hours, reaching $25 billion within 20 days. Tether fulfilled every redemption. But at that time, the circulation was $80 billion. At $186 billion in scale, stress testing has yet to be run.

S&P downgraded its stability rating to the lowest ("5") at the end of 2025, citing that exposure to high-risk assets (Bitcoin, gold, corporate bonds, secured loans) increased from 17% last year to 24% of reserves. Ardoino publicly responded: "We wear your disdain proudly." You interpret it as you see fit.

USA₮: The American Brand

On January 27, 2026, Tether launched USA₮, a federally regulated dollar-backed stablecoin designed for the U.S. market. The product is structured under the GENIUS Act (signed into law on July 18, 2025), even though the law's implementation timetable is phased and the full regulatory framework is still being established.

USA₮ is issued by Anchorage Digital Bank, the first federally chartered crypto bank in the U.S., operating under OCC supervision. Cantor Fitzgerald serves as the reserve custodian and primary dealer of choice. Bo Hines, the former executive director of the President's Advisory Council on Financial Technology (White House cryptocurrency committee), serves as CEO of Tether USA₮, headquartered in Charlotte, North Carolina.

This is not Tether rebranding USDT. This is a structurally independent product, with different issuers, regulatory frameworks, and reserve requirements. Anchorage and Cantor are shareholders of U.S. entities and will share revenues, although specific economic terms have not yet been publicly finalized.

The strategic logic is a bifurcation. USD₮ remains an offshore product issued from El Salvador, serving hundreds of millions of global users, especially in emerging markets. USA₮ is an onshore product designed for U.S. institutional settlement, issued by a state-chartered bank under federal supervision.

Bo Hines described the relationship between the two as "mutually beneficial," adding that "Ultimately it’s still Tether." However, the competitive dynamics faced by the two products are entirely different.

In the U.S., Ardoino anticipates that stablecoin profitability will "squeeze to the bottom." As bank-issued stablecoins enter the market under the GENIUS Act, they will compete by sharing profits with holders, effectively turning into tokenized money market funds. USA₮ cannot win on profitability; it must win on programmability, institutional services, and Tether's distribution advantage.

Offshore, USD₮ faces little competition (holders earn zero returns) because its users have no better alternatives. The product itself is a stable dollar. This is a monopoly position that is hard to attack.

Hines is also confident that the U.S. Treasury will eventually establish a "mutually beneficial standard" under the GENIUS Act, allowing offshore USD₮ to achieve legal recognition in the U.S. Tether operates two structurally independent businesses under one brand.

A pessimistic scenario, which is rarely articulated clearly: by launching a highly regulated, transparent U.S. product, Tether implicitly acknowledges that the standards for offshore USD₮ are not the same. If the institutional market begins to view the two products as agents of each other's reputations, the opacity surrounding USD₮ could end up tainting USA₮.

The Group

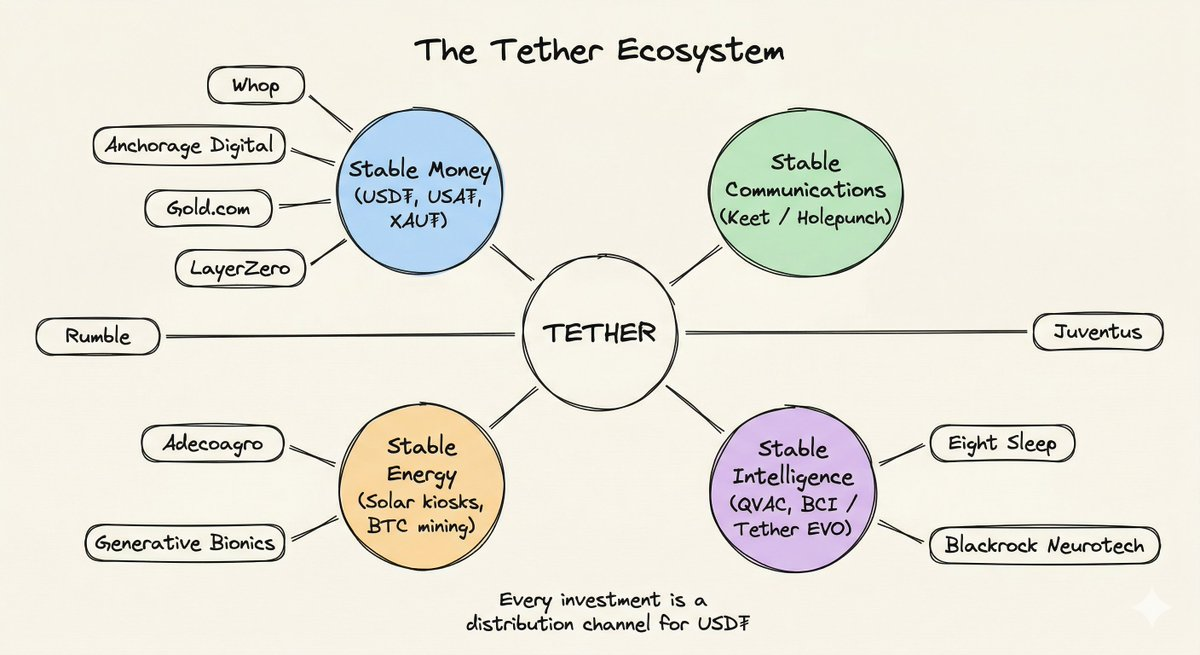

I found the way Tether's portfolio is structured makes it look like a list of random bets. But it's not.

Tether's proprietary investment department manages over $20 billion (isolated from USDT reserves and funded by profits and excess capital). Ardoino stated in July 2025 that they have invested in over 120 companies. Recent deployments include: $200 million in Whop (an internet marketplace with 18.4 million users), $150 million in Gold.com (12% stake), $100 million in Anchorage Digital, $50 million in Eight Sleep, and small holdings in LayerZero, Ark Labs, and Axiym.

Ardoino calls the overarching theme "stable company," with four pillars: stable currency (USD₮), stable communication (Keet, a peer-to-peer instant messaging app), stable energy (African solar booths, Bitcoin mining), and stable intelligence (QVAC, a decentralized AI platform).

Peeling away the branding, one sees a distribution strategy disguised as a group. Each investment is evaluated as a channel to embed USD₮ deeper into global commerce. Whop’s 18.4 million users will receive an integration of WDK (Tether's Wallet Development Kit). Rumble's 51-70 million users will gain access to a native wallet supporting Bitcoin, USD₮, USA₮, and Tether gold. In mid-March, USA₮ held a branding event in Times Square, with 25,000 people scanning QR codes, downloading Rumble wallets, and claiming $10 in USA₮.

This is how the ecosystem operates: portfolio investments fund distribution channels, and distribution channels guide stablecoin users.

The group's narrative has changed within months. Tether is no longer just writing checks and integrating wallets; it is starting to gain operational control.

In 2025, Tether acquired a 70% controlling interest in Adecoagro (a major agricultural company in South America). They completely revamped the board, appointing Juan Sartori (Tether's head of special projects) as executive chairman (not hiding it). This is not a venture capital bet but a takeover of a public agricultural group.

This pattern repeats. After investing $150 million in Gold.com in February, Tether gained board nomination rights, and Sartori was appointed to the Gold.com board on March 16. They hold a minority stake in Juventus Football Club and recently acquired 30.4% of the Italian media company Be Water. Each time, the trajectory is: investment → board seat → operational influence.

What is most unusual is that Tether has been acquiring small shops, stalls, and mobile credit purchase chains across Latin America, Africa, and Asia.

These are the physical locations where locals traditionally buy prepaid phone credit. By owning this infrastructure, Tether controls the literal cash-to-crypto entry in emerging markets, completely bypassing the banking system. Control over tangible assets is a fascinating strategic move, creating a broader moat for Tether.

Whether you see this as visionary infrastructure building or as over-expansion depends on whether you believe a company with 300 employees is capable of managing a $20 billion portfolio spanning stablecoins, gold, Bitcoin mining, AI, robotics, brain-computer interfaces, sleep technology, agriculture, football clubs, media companies, and video platforms.

Ardoino's framing in interviews: Tether provides capital and distribution, allowing portfolio companies to operate on their own. But the takeover of the Adecoagro board and Sartori's appointment tells another story. This increasingly looks less like a strategic fund and more like an operational group powered by a stablecoin engine. The CIO transition announced this week (Richard Heathcote moving to an advisory role, replaced by his deputy Zachary Lyons) suggests that the investment operations are maturing into something that requires more institutional structure, not less.

Platform Layer

The underlying infrastructure products are things that may keep Tether's technology sticky, no matter what happens with the token itself.

WDK (Wallet Development Kit): open-source, non-custodial wallet infrastructure. The strategic goal is to become the default financial layer for every internet-connected device. The most specific example Ardoino provided: a smart fridge holding $50 in USDT managing its grocery budget autonomously and paying independently (yes, he was serious). More practically, WDK has already integrated with Whop and is being embedded into the Rumble wallet. Its most interesting feature is cross-chain routing: automatically transferring users' USD₮ to the blockchain with the lowest transaction fees at any given moment, forcing L1s to compete on cost to capture Tether's volume.

QVAC: Tether's decentralized AI platform. Launched in May 2025, it already shipped products: Genesis I (a 41 billion token synthetic dataset for STEM-focused AI training), QVAC Workbench (a local AI app supporting local model inference on mobile and desktop devices), and QVAC Health (a privacy-focused health app aggregating wearable device data without sending anything to the cloud). The SDK supports Llama, Qwen, and Whisper models running fully on devices. No user adoption data has been released yet.

Hadron: Tether's tokenization platform, launched in November 2024. It supports USA₮ issuance and tokenization of stocks, bonds, commodities, and funds. Integration with Chainalysis and Crystal Intelligence provides institutional-level compliance tools. In November 2025, strategic agreements were made with KraneShares and Bitfinex Securities targeting tokenized exchange-traded products. But like QVAC, there are no published adoption metrics except for Tether's own products.

Keet / Holepunch: a peer-to-peer instant messaging app built on a rewritten BitTorrent architecture, serverless, with no central infrastructure. Ardoino claims a chat room called "Keet News" has over 12,000 daily active users streaming media with zero servers. Since there is no infrastructure to maintain, he theorizes it could, in theory, scale to a billion users at nearly zero cost.

The platform products are real (the code is open-source, applications can be downloaded, SDKs are documented). But none have independent usage metrics, revenue data, or third-party validation. Everything I can verify comes from Tether's own announcements. The platform layer is a bet on the future, not a verified means of revenue diversification. The question is whether the integration of WDK with Whop (18.4 million users) and Rumble (51 to 70 million users) will yield real adoption.

Risks

Interest rate sensitivity has already manifested in the numbers. A continued decline in Federal Reserve interest rates will directly compress Tether's core revenue. Gold and Bitcoin hedges partially offset this impact but introduce new volatility (in a January 2026 sell-off, gold fell 20% within three days).

TRON Reliance: about 44% of USDT supply (around $82 billion) is on TRON. The chain dominates retail transfers, processing about 65% of all USDT transactions below $1,000. Tether's countermeasure is WDK's cross-chain routing, but this concentration is a reality that exists before widespread deployment.

The audit gap persists. Institutional buyers will discount everything else until the Big Four release a complete audit. The hiring of a "controversial audit" CFO signals intentions.

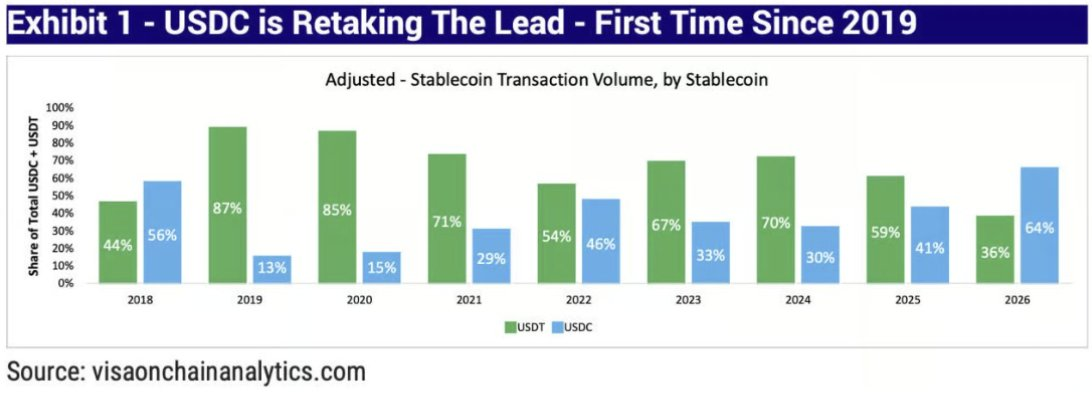

The competitive landscape with Circle is more complex than either party might admit. On adjusted trading volume, USDC has surpassed USDT for the first time since 2019. Visa's on-chain analysis shows a reversal: USDT's share of stablecoin trading volume fell from 87% in 2019 to 36% in 2026, while USDC rose from 13% to 64%.

Institutions, AI agents, payment providers, and DeFi protocols are all choosing USDC. Circle has gone public on the New York Stock Exchange, gaining regulatory clarity in the U.S. In 2025, USDC supply grew by 73%, while USDT grew by 36%.

But the volume reversal does not translate into a profit threat. Circle gives away about 60% of its revenue to distribution partners (with Coinbase alone receiving over $900 million in 2024). Tether organically owns its distribution network, and now is also purchasing more on a physical level (convenience stores, stalls, Rumble, Whop).

Tether's profit in 2025 exceeds $10 billion. Circle's total revenue for 2024 was about $1.7 billion. USDC is a product for institutional routing; USDT is a money-making product. They are playing entirely different games, and Tether's game is an order of magnitude higher in profitability.

There are also group issues: a company that simultaneously manages a $190 billion stablecoin reserve, acquires football clubs, invests in brain-computer interfaces, builds an AI platform, and operates solar booths in Africa—are they creating resilience, or setting the stage for operational accidents?

Stablecoin Infrastructure

If you operate in emerging markets, USD₮ remains the dominant settlement tool priced in dollars, with a significant lead. Its distribution network (estimated at over 550 million users, with physical entrances, exchange integrations) is unparalleled.

If you are a U.S. institution, USA₮ gives you a federally regulated tool to enter Tether's ecosystem. But it has just started and is in direct competition with the existing institutional relationships of USDC. The reason to choose USA₮ over USDC today is Tether's global liquidity network. The opposition reason is Circle's longer compliance record.

If you are a bank considering issuing your own stablecoin, Bo Hines has a sharp observation: "Banks are beginning to realize that, given other banks' unwillingness to settle with their own products, issuing their own stablecoin may not be the best idea." Neutral, unbiased incumbents win the interbank settlement game. That is Tether's position.

If you are observing the platform layer (Hadron, WDK, QVAC), a honest assessment is: these are early infrastructure bets backed by real technology but have yet to generate meaningful impact (this is expected).

In 2026, Tether's correct frame of reference may not be Circle or Paxos, but rather a combination more akin to Berkshire Hathaway (retained earnings diversifying funding for the conglomerate, with 95% of profits retained) and Visa (an all-participant settlement track because they are neutral and ubiquitous).

When I started writing this article, I thought I was writing about a stablecoin company; I ended up writing about a company attempting to build parallel financial infrastructure for half a world that has been forgotten by the existing system. The reserve issue is real. But its ambition, and the speed at which it executes with 300 people and zero external capital, is something I have never encountered in this space.

If Tether realizes even half of what Ardoino has built, the rest of the industry will spend the next decade catching up.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。