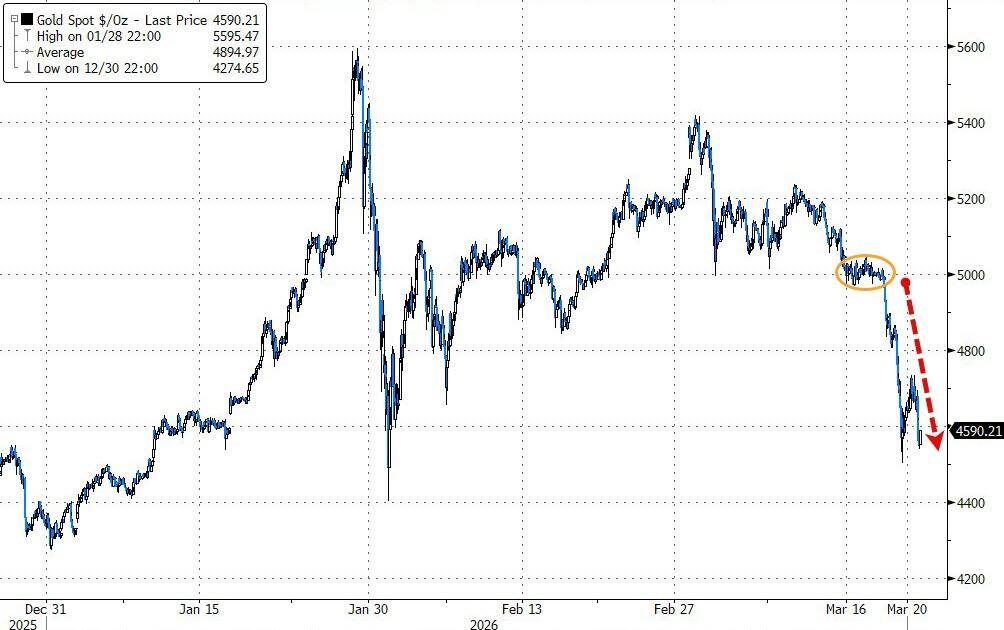

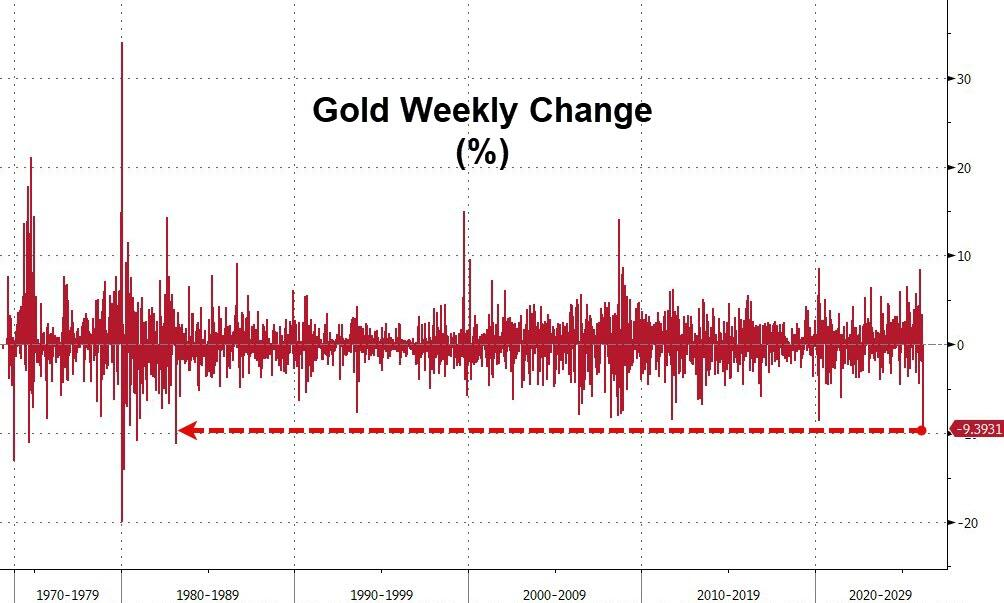

Gold faced its worst weekly decline in 43 years this week, with the echoes of history sending shivers through the market.

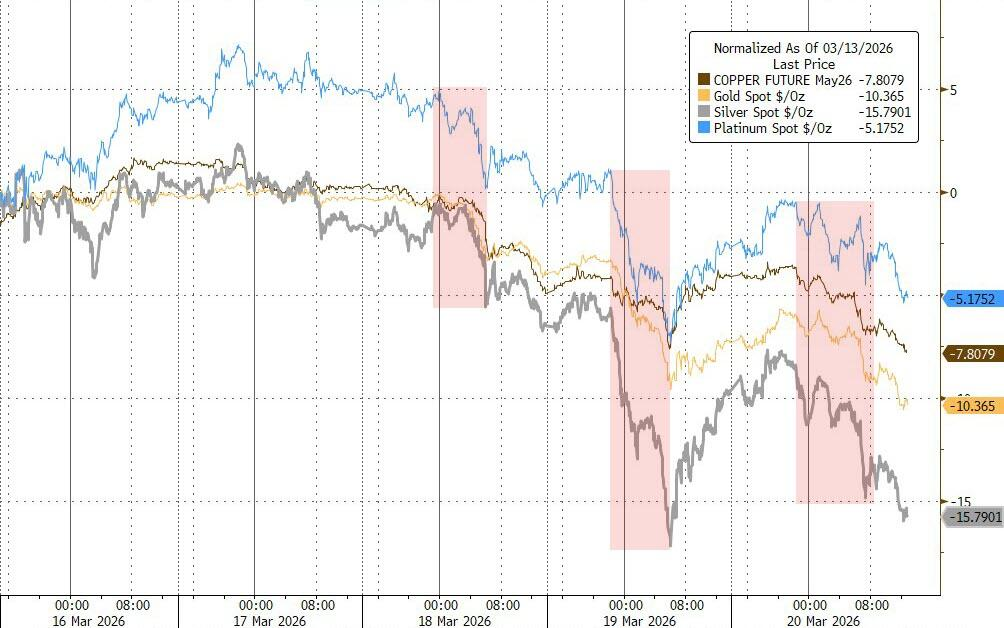

This week, gold's decline set a record for the largest weekly drop since March 1983, with spot gold prices falling for eight consecutive trading days, marking the longest consecutive drop since October 2023. Meanwhile, silver fell more than 15% this week, and both palladium and platinum also declined.

The trigger for this round of sharp decline was the escalating conflict in the Middle East, which increased energy prices and suppressed expectations for interest rate cuts. Market bets on the Federal Reserve raising interest rates have risen to 50%, intensifying the wave of selling in precious metals.

What makes the market more vigilant is that the current situation is strikingly similar to the historic collapse in March 1983, which was triggered by a massive sell-off of gold by oil-producing countries in the Middle East—at that time, OPEC members, facing a sharp drop in oil revenues, were forced to liquidate gold reserves for cash, causing gold prices to plummet by over $100 within a few days.

It is noteworthy that, according to historical data, this week's decline in gold is the most severe since the "sell gold to raise funds" storm 43 years ago.

Expectations for interest rate cuts collapse, gold's safe-haven logic fails

Since the attacks by the United States and Israel on Iran last month, gold has fallen for several consecutive weeks, which sharply contrasts with the traditional role of "safe-haven assets."

The reason is that war brings not easing expectations, but inflationary pressures. Currently, the market's prediction of the Federal Reserve's policy path has undergone a fundamental reversal.

Traders are currently betting on a 50% probability of the Federal Reserve raising rates before October. Rising energy prices increase inflation expectations, and gold, as a non-yielding asset, becomes significantly less attractive in an environment of rising real interest rates.

Meanwhile, signs of tightening dollar liquidity have emerged in the current market. Cross-currency basis swaps began to widen significantly this week, indicating a degree of dollar financing pressure.

This phenomenon may explain the deeper logic behind gold's sell-off—when dollar liquidity tightens, gold is often one of the assets that investors prioritize for liquidation.

It is worth noting that the times of the most severe declines in the metals market this week were concentrated during Asian and European trading sessions, which aligns with the pattern of dollar shortage pressure first emerging in the offshore market.

Technical stop-loss triggers, self-reinforcing sell-off

As the decline continued, gold's technical indicators deteriorated significantly, with the 14-day Relative Strength Index (RSI) falling below 30, entering a region considered by some traders to be oversold.

Rhona O'Connell, an analyst at StoneX Financial, pointed out that this round of gold correction is the result of profit-taking and liquidity clearing acting together. She stated that gold prices had previously attracted significant buying above $5,200, leading the market to accumulate notable vulnerability to a correction.

Once prices began to decline, numerous investors' stop-loss orders were automatically triggered, rapidly creating a self-reinforcing spiral of selling. Technical signals such as moving averages further exacerbated the downward pressure.

Meanwhile, passive selling triggered by declining stock markets also affected gold.

O'Connell noted that forced liquidations related to stock assets may have dragged down gold prices, while the slowdown in central bank gold purchases and the continuous capital outflow from gold ETFs further suppressed market sentiment. According to Bloomberg data, gold ETFs have recorded net outflows for three consecutive weeks, with holdings decreasing by more than 60 tons over these three weeks.

The ghost of the 1983 Middle East "sell gold to raise funds"

The current situation inevitably reminds market participants of the gold crash triggered by the oil crisis 43 years ago.

Historical data show that around February 21, 1983, British and Norwegian oil producers were the first to lower prices, putting pressure on OPEC to follow suit, sharply exacerbating the oversupply situation in the global oil market. Faced with a significant shrinkage in oil revenues, Middle Eastern oil-producing countries (mainly OPEC members) were forced to sell gold reserves in bulk to raise cash, which triggered a collapse in gold prices.

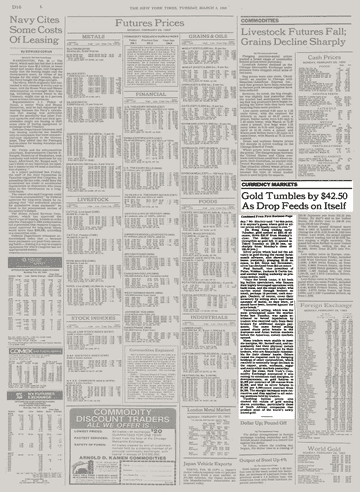

Reports from The New York Times at the time confirmed this assessment. According to a March 1, 1983, report in The New York Times, traders clearly stated that the sell-off of gold by Middle Eastern oil-producing countries was a direct trigger for the plunge in gold prices, and warned that if oil revenues continued to decline, these Arab countries might sell more gold. At that time, gold prices fell over $105 from their highs in less than a week, with a maximum single-day drop of $42.5, the largest in nearly three years.

According to The New York Times reports at the time, the funds obtained from the Middle Eastern sell-offs immediately flowed into Eurodollars and other short-term investment instruments, causing short-end interest rates to soften and subsequently sending warning signals to the global gold market. Since February 21 coincided with the U.S. Presidents Day holiday, the New York market was closed, and the impact only fully manifested in the following week, leading to a chain of forced liquidations that also affected commodity markets such as copper, grains, soybeans, and sugar.

ZeroHedge pointed out that the gold crash in 1983 marked the beginning of a multi-year bear market cycle in the oil market—characterized by OPEC's disintegration of discipline and continuous loss of market share, leading to sustained pressure on oil prices throughout the 1980s.

Stagflation clouds loom, can gold stabilize?

Despite suffering a heavy blow this week, gold has still risen about 4% since the beginning of the year. Gold prices touched nearly $5,600 per ounce in late January this year, supported by investor enthusiasm, a gold purchase spree by central banks, and concerns over Trump's intervention in the Federal Reserve's independence.

However, the current macro environment has significantly deteriorated. According to Bloomberg, Goldman Sachs economist Joseph Briggs expects that rising energy prices will drag down global GDP by 0.3 percentage points over the next year and push overall inflation up by 0.5 to 0.6 percentage points. The rising risk of stagflation severely compresses the policy space for central banks.

Goldman Sachs analyst Chris Hussey noted that the blockade of the Strait of Hormuz has entered its fourth week, and hopes for a quick resolution to the conflict are fading. If the conflict continues, the longer high oil prices persist, the harder it will be for the stock and bond markets to maintain the narrative of "seeing through short-term pain," further exposing the vulnerability of global assets.

For gold, the trend of real interest rates will be a key variable. If the conflict drags on and inflation expectations continue to rise, the path for the Federal Reserve's interest rate hikes will become increasingly clear, and the pressure on gold may persist; however, if there are signs of easing in geopolitical situations, whether suppressed safe-haven demand can be released again remains the biggest suspense in the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。