In less than a month, Goldman Sachs has made a rare strategic U-turn—from actively promoting the HALO concept to investors, to actively shorting constituents that have "overheated," reflecting concerns over the crowdedness of heavy asset trading.

On Tuesday, Faris Mourad, head of Goldman Sachs' thematic trading team, introduced a short basket, GSXUHALT, in the latest report, specifically targeting American companies that are asset-intensive but have zero or even negative profit growth expectations, while their stock prices have surged significantly with the HALO trend. Goldman Sachs believes that the market's enthusiasm for heavy asset stocks has shown indiscriminate characteristics, with the price increases of some individual stocks severely disconnected from their fundamentals.

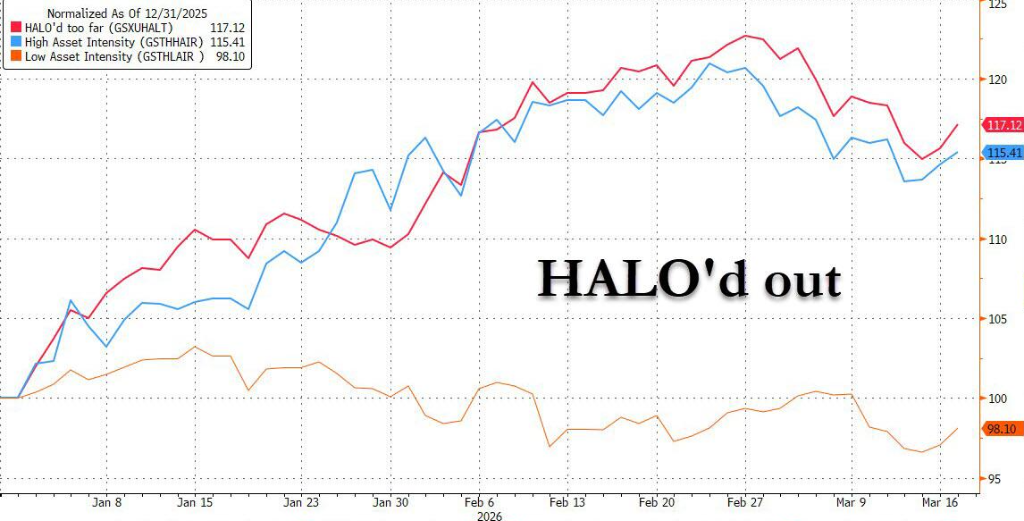

The direct implication of this shift for the market is that the honeymoon period for HALO trading may be over. Goldman Sachs data shows that the GSXUHALT basket began to decline after peaking at the end of February, and the bank recommends that investors pair this short position with thematic long opportunities they are optimistic about.

One Month Ago: Goldman Sachs Promotes HALO, Heavy Asset Narrative Sweeps Wall Street

Let’s return to February 24, when Goldman Sachs' Global Investment Research Department released a report "The HALO Effect: Heavy Assets and Low Obsolescence in the Age of AI", alongside major banks like JPMorgan, actively promoting the HALO concept to investors—which combines Heavy Assets with Low Obsolescence.

At that time, the logic was clear and compelling: the rapid rise of AI is creating a dual impact on light asset industries. On one hand, AI has disrupted profitability expectations in industries like software and IT services, leading the market to reassess the terminal value of these sectors; on the other hand, tech giants have embarked on an unprecedented capital expenditure cycle to maintain their competitive advantage in computational power—according to Goldman Sachs data, the five largest tech companies in the U.S. are expected to spend about $1.5 trillion on capital expenditures between 2023 and 2026, with spending in 2026 alone expected to exceed $650 billion, surpassing their historical total before the AI era.

Goldman Sachs' data at the time was equally impressive: since 2025, its heavy asset portfolio (GSSTCAPI) had cumulatively outperformed the light asset portfolio (GSSTCAPL) by 35%. At the macro level, higher real interest rates, geopolitical fragmentation, and supply chain restructuring are believed to collectively constitute structural tailwinds for heavy asset stocks.

Sharp Turn: Market Indiscriminate Pursuit, Some Heavy Asset Stocks' Price Increases Have Lost Fundamental Support

However, just a month later, Goldman Sachs' stance had shifted significantly.

Mourad pointed out in the latest report that the companies included in the GSXUHALT basket are those that have risen alongside the overall heavy asset market but have no profit growth expectations, with returns significantly lagging behind those high-quality HALO targets. In other words, while the market chases "AI insulation" attributes, funds have indiscriminately flowed into all heavy asset stocks without distinguishing between quality.

Data confirms this judgment: the price increase of the GSXUHALT basket has actually surpassed that of the high-quality high asset density basket (GSTHHAIR), meaning low return, no growth heavy asset stocks have outperformed those with real competitive barriers. Meanwhile, the stock price movements of the basket were synchronized with profit expectations until the end of last year, after which there was a clear divergence.

When selecting components for GSXUHALT, Goldman Sachs chose companies from the Russell 1000 index with the highest asset density industry, while eliminating all targets related to long-term trends such as satellites, robotics, quantum computing, and AI, retaining only those stocks that have seen significant price increases since the beginning of the year but have flat or lowered profit expectations. The average asset density ratio of this basket is about 1.4.

Valuation Signal: Heavy Asset Premium is at a Historically Above-Medium Level

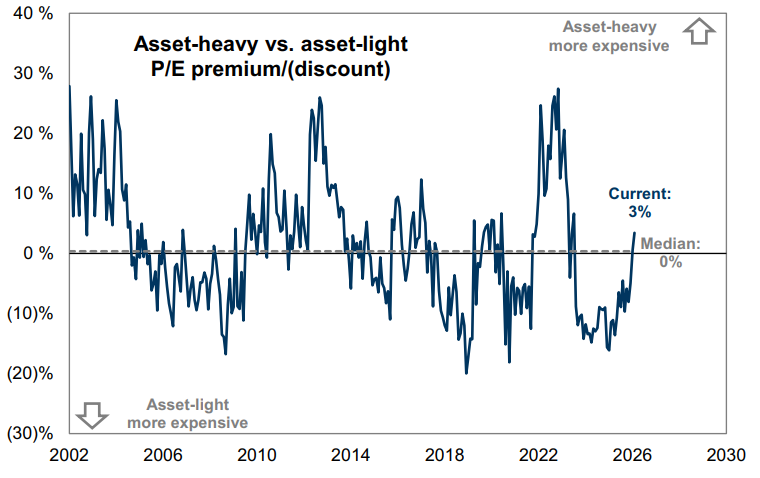

Goldman Sachs' research last month indicated that heavy asset stocks are currently trading at a valuation premium relative to light asset stocks. As of last month, the price-to-earnings ratio premium for heavy asset stocks was about 3%, placing it in the 62nd percentile of the past few decades, although still lower than the historical peaks of 2004, 2012, and 2022, it is no longer cheap.

Since November of last year, Goldman Sachs' industry-neutral heavy asset basket (GSTHHAIR) has cumulatively outperformed the light asset basket (GSTHLAIR) by about 20%. This round of strong performance in heavy assets, in Goldman Sachs' view, stems from investors' strong demand for "AI insulating" assets—looking for those physical asset stocks that are not easily disrupted by AI and have underperformed for many years.

Goldman Sachs suggests that the GSXUHALT short position could be paired with thematic long opportunities that the bank is optimistic about. The report pointed out that the recent market correction has created the largest "buy on dip" opportunity in the global stock market since "Liberation Day," allowing investors to short heavy asset stocks without fundamental support while establishing long exposure in directions supported by long-term trends.

Behind this strategic shift is Goldman Sachs' clear judgment on the internal differentiation of HALO trading: not all heavy asset stocks are worth holding; it is time to differentiate between those with real competitive barriers and profit momentum and those that are simply riding the coattails of the "heavy asset" label.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。