Author: Murphy

When investors buy a large number of Calls (call options), the counterparty is usually the market maker. After selling Calls, the Delta of their option portfolio turns negative. To maintain Delta neutrality, they typically need to buy spot or go long on futures for hedging.

However, in the actual market, what truly affects the price path is often not just Delta, but Gamma.

When market makers are in a Short Gamma state, the closer the price is to the key strike price, the faster the Delta changes, and the more the market makers need to continuously hedge in the direction of the price (buying on the way up and selling on the way down), which amplifies price volatility.

This is what we commonly refer to as the “Gamma Magnet effect.”

In the current cycle, the open interest in BTC options has long remained at the level of $40-$50 billion, which is close to or even exceeds the influence of some futures exchanges. A large amount of capital expresses direction through options, making the options structure an important driver of BTC's short-term price path, further affecting price volatility.

Structure expiring on March 20

From the Gamma Exposure (GEX) expiring on March 20, there is approximately $180 million of Gamma exposure around $74,000, and it is a Long Gamma structure.

(Figure 1 - BTC Option Gamma Risk Exposure_2026.3.20)

In this environment, the hedging actions of market makers often suppress volatility, making it easier for prices to oscillate around the strike price, thus objectively creating resistance around $74,000.

Structure expiring on March 27

However, after March 20, when approaching the next major strike date on March 27, there is a clear change in the options structure.

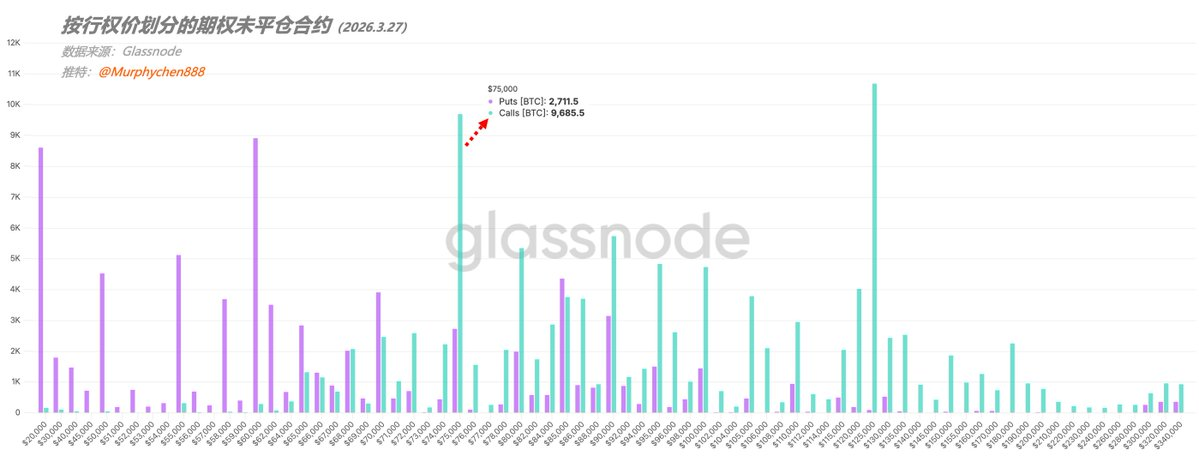

(Figure 2 - Options open contracts categorized by strike price_2026.3.27)

From the open interest (OI) structure, the strike price of $75,000 is likely to become the most concentrated area for Call options on that strike date: there are 9,685 BTC of Call OI (call options), while the Put (put options) have only 2,711 BTC.

The Call OI is significantly higher than the Put, indicating that a large amount of capital is betting that BTC will rise towards $75,000.

Who is leading: buyers or sellers?

Of course, merely from the OI structure, we cannot determine whether market makers are in a Short Gamma position, so we need to further observe the premium flow of the $75,000 Calls.

(Figure 3 - Cumulative change in the premium of $75,000 strike Call options)

According to data, in the two weeks from February 28 to March 14, concentrated buying activity of Calls occurred in the market, with the net premium of Calls rapidly rising from $5.8 million to $19.8 million, showing a clear accelerating trend (the blue curve in the figure), while BTC was fluctuating in the range of $66,000 to $68,000 at that time.

Based on this, we can conclude that the current rebound in BTC is driven not only by spot but also influenced by the options structure, indicating that there is demand for bullish options positioned in advance.

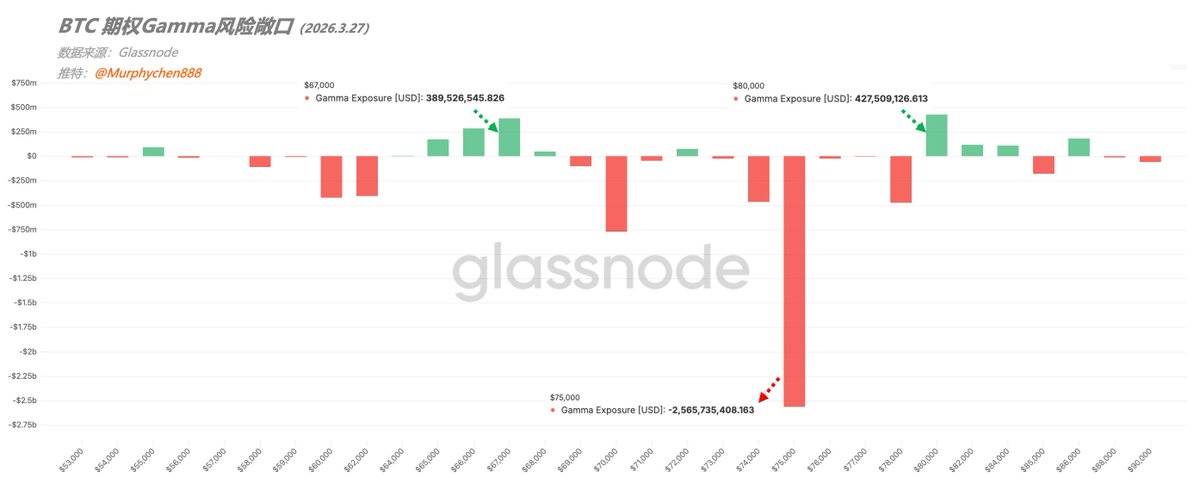

Change in Gamma structure

Combining the GEX expiring on March 27, we can see an approximate -$2.56 billion Gamma exposure around $75,000, indicating a significant Short Gamma structure; compared to March 20, there is an essential difference in both scale and nature.

(Figure 4 - BTC Option Gamma Risk Exposure_2026.3.27)

This means that if BTC continues to rise toward $75,000 after March 20, market makers in a Short Gamma environment will need to constantly hedge by buying spot or futures. This behavior may reinforce upward momentum and create a typical Gamma Magnet effect.

At the same time, the upper $80,000 and lower $67,000 correspond to Long Gamma exposures of $420 million and $390 million, respectively. When BTC prices approach $80,000, they may face stronger volatility suppression (resistance); when pulling back to the $65,000-$67,000 range, they will also gain some buffer.

However, as we can see from Figure 2, the OI around $67,000 is significantly weaker than that of $75,000 and $80,000, indicating that the hedging volume and marginal influence in that area are relatively limited. Therefore, compared to the significant Short Gamma core at $75,000, $67,000 resembles a lower buffer rather than strong support.

In simple terms, after the expiration date of March 20, the options structure of BTC will make $75,000 the new focal point, shifting from “suppressing volatility” to “amplifying volatility,” while generating resistance as it approaches $80,000 and support as it enters the $65,000-$67,000 range.

Especially as liquidity gradually diminishes, the driving logic of market prices also changes, which we should pay close attention to in the short term.

Delta refers to how much the price of the option will change when the BTC price moves. It determines how much BTC the market maker needs to buy or sell for hedging.

For example: a Call at $75,000, Delta = 0.4, means that if BTC rises by $1,000, the option price will approximately increase by $400.

Gamma refers to how quickly Delta changes when the BTC price continues to change; it determines the intensity of the market maker's hedging. That is, how quickly and how often the hedging needs to be adjusted.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。