Written by: Jordi Visser

Translated by: Luffy, Foresight News

The next big bull market for Bitcoin may begin from an area that is most unexpected: the private credit market.

This is not because a collapse in private credit would immediately benefit Bitcoin. In a true liquidity crisis, high liquidity assets like Bitcoin often get sold off first along with other assets. The first phase of the crisis is not redemption, but liquidation; the real core logic appears in the second phase.

In a system burdened with high debt, heavily financialized, and politically intolerant of long-term credit clearance, a liquidity "withdrawal" rarely lasts long. When the government injects liquidity again, Bitcoin tends to understand the significance of this move faster than almost any other asset.

Warren Buffett has already described this scenario in the most straightforward terms: "Only when the tide goes out do you discover who has been swimming naked." He also mocked private equity's "cherished fee structure and obsession with leverage," warning that in rare moments, "credit can vanish instantly, and debt will become a deadly financial trap."

What Buffett was discussing was not Bitcoin, but diagnosing a financial system built on leverage, opacity, and confidence. This diagnosis perfectly applies to today’s private credit market. When the tide goes out, hidden vulnerabilities are no longer theoretical risks but become the entire reality of the market.

This is why private credit is so important right now. According to Morgan Stanley's estimates, the market size will be around $3 trillion by early 2025 and is expected to approach $5 trillion by 2029, and warning signs have already appeared.

This week, Morgan Stanley implemented redemption restrictions on one of its private credit funds because the share of investor redemption applications approached 11% of the fund's total size; meanwhile, JPMorgan wrote down some loans directed at private credit funds, and market concerns about exposure in the software sector continued to heat up.

The focus is not that the entire market is in crisis, but that the pressure is no longer hypothetical; it is being reflected in redemption restrictions, asset write-downs, and changes in lender behavior.

AI is the Catalyst for the Crisis

The core risk is not just leverage itself, but that leverage is tied to an industry being repriced in real time by AI.

Morgan Stanley pointed out in March that about 25% of commercial development companies' investment portfolios are allocated to the software sector. Given the impact of AI on the business model of the software industry, this ratio is quite high.

For years, the financing logic of the software industry has been based on the assumption that recurring revenue equals stable cash flow, strong customer stickiness, high profit margins, and solid exit paths. However, AI is overturning all of this: pricing power is squeezed, products quickly become functional modules, competitive moats shrink, and computing power and product development investment become rigid expenses.

In other words, a large amount of private credit is based on potentially outdated software business models.

Bitcoin is Also in the Storm

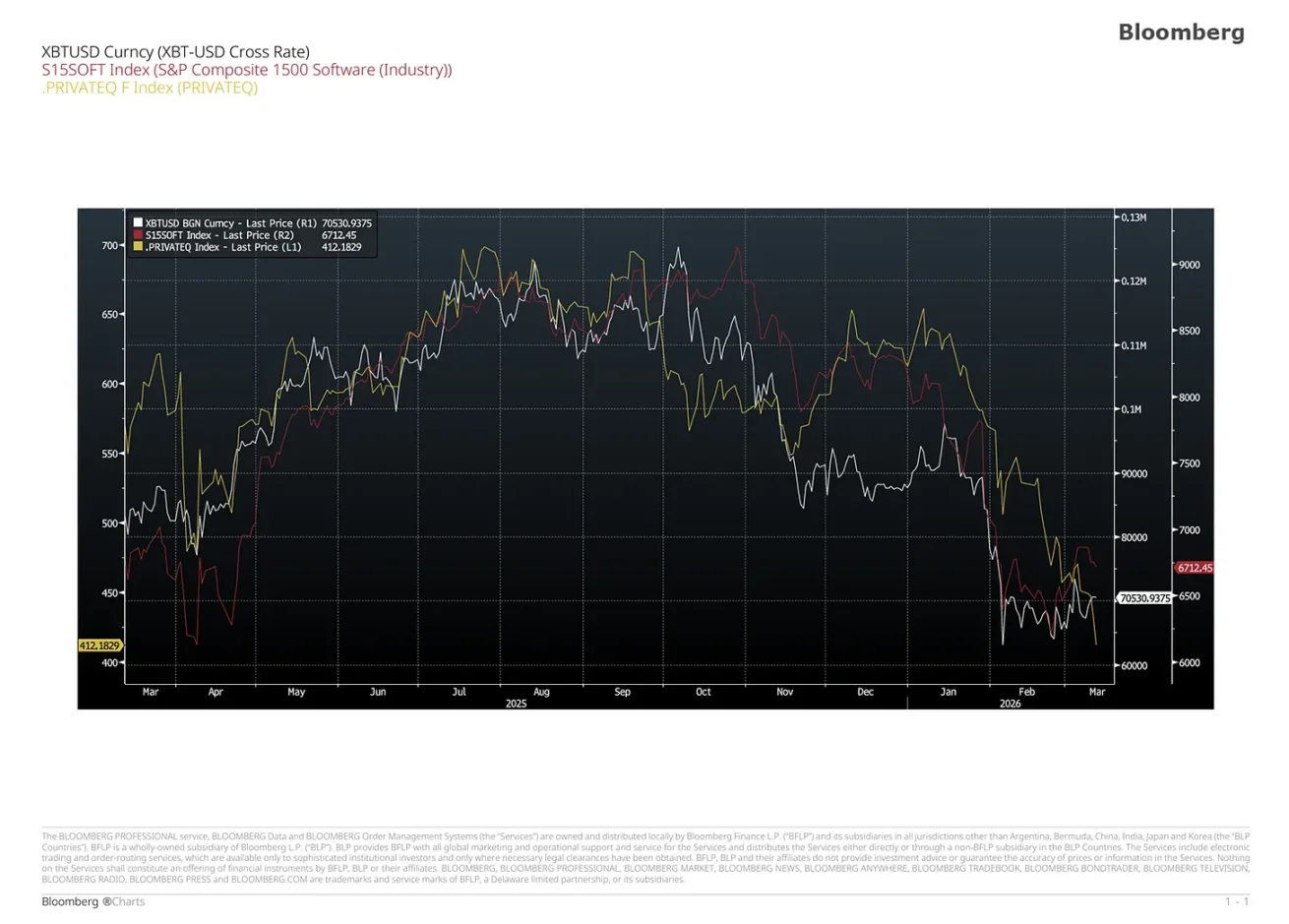

All discussions around software valuation and private credit ultimately point to Bitcoin. Comparing the movements of Bitcoin with software stocks and private equity stocks makes the connection clear:

Bitcoin's movement has characteristics of both software sector Beta and liquidity Beta, and currently, both forces are simultaneously pressuring it.

By 2025, I expected Bitcoin to experience a strong rise, driven by increased government support and the rise of AI entities, factors that should strengthen the crypto network effect, leading to a reevaluation alongside the software sector, becoming a high-growth asset class. Despite a rise in trading volume and market value of stablecoins, this optimistic expectation for Bitcoin ultimately did not materialize.

On the contrary, with the emergence of technologies like Opus 4.5 and OpenClaw, market focus shifted to AI's disruption of the software industry itself. Investors reassessed the sustainability of traditional software models, resulting in rapid reductions in valuation multiples, which also impacted the private credit that is an important source of capital for the software ecosystem.

AI forces disruptive repricing in the software industry, putting pressure on a major macro pricing logic for Bitcoin; meanwhile, the tightening global liquidity cycle further suppresses another core characteristic: its high sensitivity to global liquidity.

This is why a crack in private credit does not immediately benefit Bitcoin: in the short term, the effect is often the opposite. Bitcoin’s liquidity is good, its holdings are diversely distributed, and it is easily sellable; during the first phase of market pressure, liquidity priority far exceeds long-term value logic.

Bitcoin Falls First in Panic and Rises First in Rescue

History confirms this rhythm.

In March 2020 during the "cash is king" panic, Reuters reported that Bitcoin fell over 20% in a single day and accumulated a decline of over 30% in five days, as investors nearly sold off all assets. Subsequently, as policy liquidity was unleashed, by January 2021, Bitcoin had risen over 900% from its March low, as governments ramped up spending to counter the pandemic's impact, leading to inflation and currency devaluation concerns among investors, which Bitcoin reflected fully.

Bitcoin is not immune to panic; it simply reflects more quickly and sharply than other assets the rises brought about by subsequent rescue policies.

In the 2023 regional banking crisis in the U.S., the same script played out: Silicon Valley Bank faced $42 billion in withdrawals in a single day, with another $100 billion in withdrawal requests queued for the next day. Subsequently, authorities provided guarantees for all depositors, and the Federal Reserve launched a bank term financing program, providing loans at face value against eligible collateral. After that turmoil, Bitcoin’s price climbed to the highest point in nine months and more than doubled by the end of the year.

The core pattern remains consistent: Bitcoin often suffers during cash battles, only to pivot and realize the benefits of policy rescues.

Why Redemption is Inevitable

This mechanism is particularly crucial now, as the U.S. financial system cannot withstand a prolonged liquidity tightening.

The Congressional Budget Office stated in February 2026 that the federal deficit for fiscal year 2026 would reach $1.9 trillion, with publicly held debt accounting for 101% of GDP. Meanwhile, in early March, the Buffett Indicator (total U.S. stock market capitalization / GDP) was about 219%.

This is the reality of financialization: high sovereign debt and asset markets far exceeding the real economy. In this context, policymakers have no room to allow for a complete spontaneous liquidation. The association between the modern economy and asset prices is too high, and the connection between the state and economic growth and market operations is also too strong; therefore, a purely liquidative approach cannot be sustained.

The Federal Reserve has already shown this stress response, slowing down its balance sheet reduction in March 2025, deciding in October to halt security liquidation on December 1, and initiating reserve management purchases in December to maintain adequate reserves. Even without a full-blown crisis, the system is already retracing toward easing.

Once it’s understood that the financial system itself needs to restart liquidity, it is not difficult to judge: when the next private credit crisis erupts, policymakers are almost certain to step in.

The political aspect is even more so. In September 2025, the U.S. SEC Investor Advisory Committee pointed out that, despite expanding public participation channels through registered products, the transparency of private market assets is lower and the risks are higher. Morningstar indicated that the net asset size of semi-liquid funds reached $493 billion in the third quarter of 2025.

When retail funds and wealth channel funds are packaged into illiquid credit exposures, private credit is no longer just a niche institutional issue but a public issue. When opaque risks evolve into public problems, government intervention is inevitable.

Bitcoin Returns to Its Original Logic

The Bitcoin whitepaper proposed a peer-to-peer electronic cash system that allows direct transfers between transacting parties without going through financial institutions. The famous inscription on the genesis block — "The Chancellor is on the verge of the second bailout for banks" — reveals its political undertone.

The whitepaper provides the technical architecture, while the genesis block carries the political metaphor. Bitcoin was born out of a rebellion against a rescue culture, dependency on intermediaries, and arbitrary monetary policies.

Therefore, every time the government steps in to save a fragile system built on hidden leverage, Bitcoin's foundational logic becomes stronger.

Meanwhile, financial infrastructure is moving towards 24/7 operation. In October 2025, the Federal Reserve announced that Fedwire and the national settlement system planned to achieve Sunday and holiday operations in 2028 or 2029. This does not mean Bitcoin is being officially adopted, but it signifies that the system recognizes an important reality: the economy is increasingly digital and continuous, and compatibility with traditional banking hours is diminishing.

If AI entities become true economic participants, funds and collateral will need to circulate at software speed. This does not mean every transaction must be settled in Bitcoin, but it indicates that scarce, neutral, digital collateral will become more important.

The tide that Buffett spoke of is currently receding in the private credit market. AI is first to expose the most vulnerable credit assets, especially those that misjudge software income as permanent cash flow. Bitcoin suffers in the first wave of impact because it is simultaneously viewed as a dual Beta of software and liquidity.

But with American debt being too high, the economy financialized too deeply, and retail funds too tightly bound with private assets, policymakers cannot tolerate a prolonged, disordered liquidation. Liquidity will eventually return. And whenever liquidity restarts, Bitcoin is often one of the first assets to react.

This is why private credit is critically important in the current environment.

Ironically, Bitcoin was born for moments like this: a world filled with shadow banking, hidden leverage, high government debt, only able to respond to crises through monetary easing. Private credit is not just a risk sector in the market, but a concentrated collision point of rigid valuations, embedded leverage, AI disruption, retail fund intervention, and policy stress response.

Recent redemption restrictions and asset writedowns in private credit indicate that the adjustment process may have already begun. If private credit becomes the core area of the next liquidity withdrawal, the next big bull market for Bitcoin will not begin with halving narratives or a perfect macro environment, but will start with risk exposure and policy rescues, ultimately leading the market to realize: the financial system still cannot do without liquidity injection.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。