Author: Julien Bek

Translation: Shenchao TechFlow

Guide from Shenchao: Sequoia Capital partner Julien Bek wrote a well-structured article with the core argument: the next trillion-dollar company will not sell software tools but will sell outcomes directly. For every dollar spent on software, businesses spend six dollars on services. As AI brings the cost of “doing work” closer to zero, the real opportunity lies not in Copilot (assistive tools) but in Autopilot (automatically completing work).

He dissected automation opportunities in service industries such as insurance, accounting, healthcare, law, IT, procurement, recruitment, and consulting, attaching a matrix of opportunities drawn on the dimensions of "intelligence vs. judgment" and "outsourcing vs. in-house". This is valuable reference for AI entrepreneurs and investors.

The full text is as follows:

The next trillion-dollar company will be a software company disguised as a service company.

Every founder making AI tools is asking the same question: what if the next version of Claude turns my product into a feature? This concern is valid. If you are selling tools, you are racing against the models. But if you are selling the work itself, every time the model improves, your service becomes faster, cheaper, and harder to compete with. A company might spend $10,000 a year on QuickBooks and then another $120,000 hiring accountants for bookkeeping. The next legendary company will directly handle your accounting.

Intelligence vs. Judgment

Writing code is primarily “intelligence.” Knowing what to do next is “judgment.”

Translating a requirement document into code, testing, debugging: the rules are complex, but ultimately they are rules. Judgment is different. It requires experience and taste, the intuition accumulated from years of practice. Deciding what functionality should be next, whether to incur technical debt, when to release without being fully prepared.

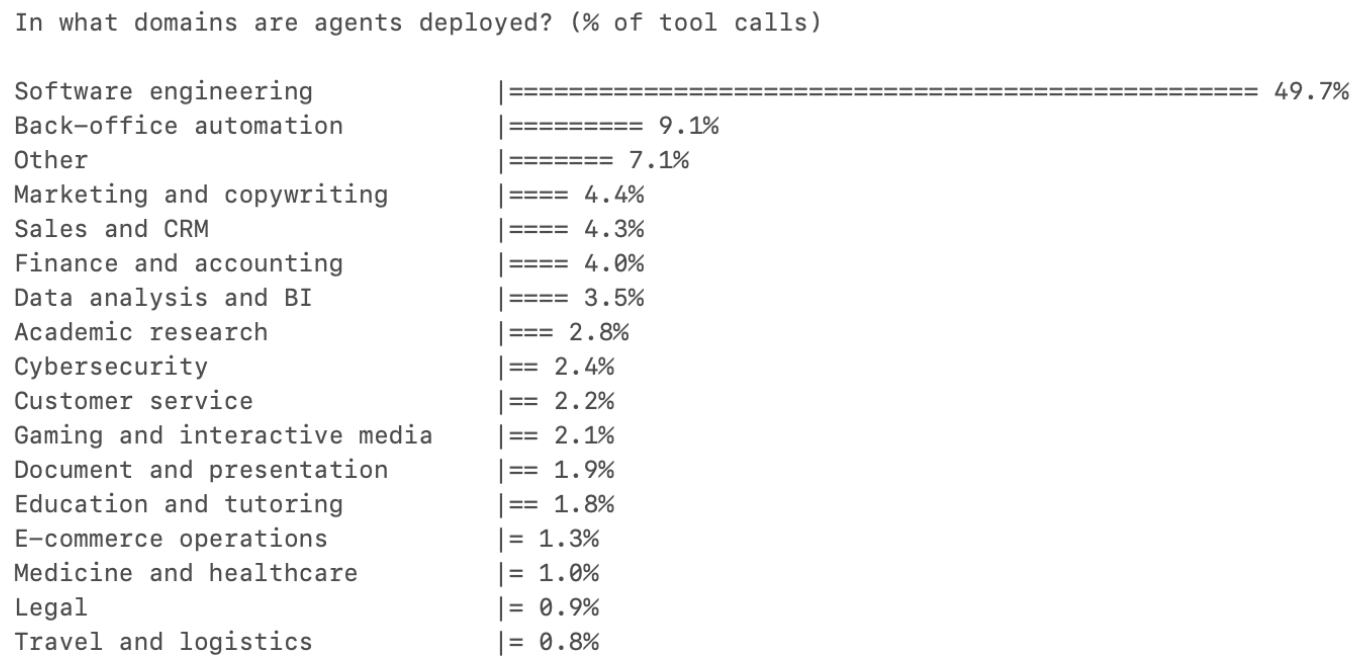

A year ago, most Cursor users treated AI as an autocomplete tool. Today, tasks initiated by Agents outnumber those initiated by humans. Software engineering accounts for more than half of all AI tool usage across professions, while other categories still linger in single digits. The reason is that software engineering is primarily intellectual work. AI has crossed that line — it can autonomously complete most intellectual tasks, leaving judgment to humans. Software engineering reached this point first, but it will spread to every profession.

Caption: AI tool usage percentages across professions, with software engineering far exceeding other categories

Copilot and Autopilot

Copilot sells tools. Autopilot sells work.

Until recently, AI models were still developing in terms of intelligence and judgment, so the correct path was to first create Copilot: putting AI in the hands of professionals, allowing them to decide how to use it. Harvey sells to law firms, Rogo sells to investment banks. Professionals are the customers, and tools make them more efficient; they are responsible for the output.

Today, models are smart enough that, in some categories, the best starting point is to go directly for Autopilot. Crosby sells to companies that need to draft NDAs, rather than selling to external legal consultants. WithCoverage sells to CFOs needing insurance rather than to insurance brokers. Customers purchase results directly. In any profession, the work budget far exceeds the tool budget, and Autopilot can capture the work budget from day one.

The higher the proportion of intelligence in a field, the faster Autopilot wins.

Integration

Today's judgment becomes tomorrow's intelligence. As AI systems accumulate proprietary data on what "good judgment looks like" in their fields, the frontier will shift. Copilot and Autopilot will converge. The transition from Copilot to Autopilot has already begun in several categories. But the starting position is crucial because it determines where Autopilot can currently win customers and start accumulating the data that ultimately enables it to handle judgment tasks as well.

Autopilot Strategy: Outsourcing as the Entry Point

For every dollar spent on software, six dollars are spent on services.

The TAM (Total Addressable Market) for Autopilot is all labor expenditures in a category, combining both internal and outsourced work. But the correct starting point is where outsourcing already exists.

If a task has already been outsourced, it tells you three things. First, the company has accepted that this work can be completed externally. Second, there’s a ready-made budget item that can be replaced cleanly. Third, the buyer is already purchasing results. Replacing an outsourcing contract with an AI-native service provider is a supplier switch. Replacing in-house staff is an organizational restructuring.

The strategy is: start with outsourced, intelligence-intensive tasks. Get distribution sorted. As AI accumulates data, then expand to internal, judgment-intensive work. Outsourced tasks are the wedge, internal work is the long-term TAM.

Crosby targets NDAs: a well-defined task, mostly intellectual work, that most companies already outsource to external lawyers. The budget is ready, the scope is clear, ROI is immediate, and replacement is frictionless.

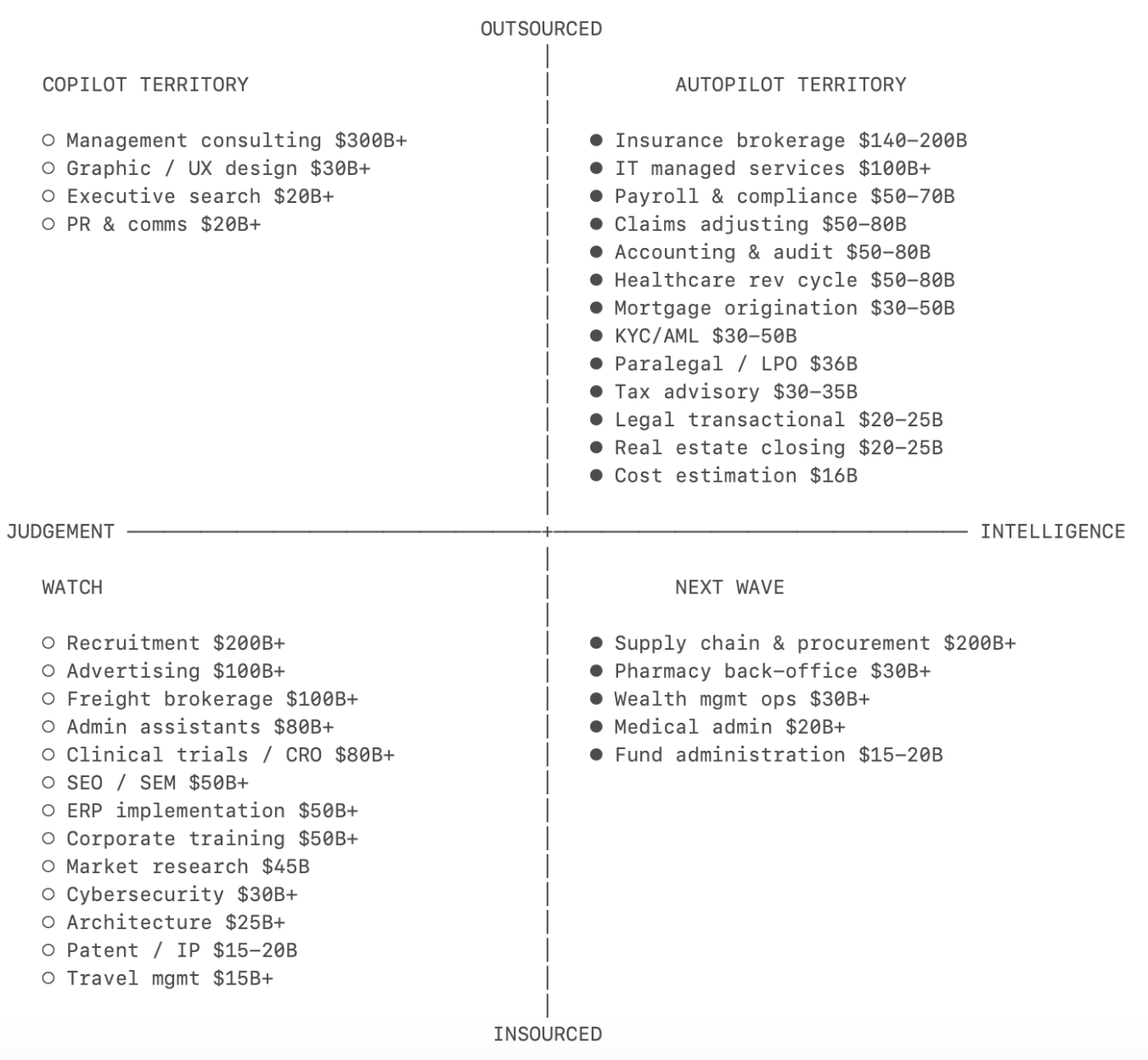

Opportunity Map

Plotting each service vertical on a spectrum of "intelligence to judgment" and "outsourcing to in-house" will yield a priority map, with labor TAM in parentheses. The following list is not exhaustive.

Caption: Autopilot opportunity matrix across service verticals (distributed by intelligence/judgment ratio and outsourcing/in-house ratio)

Insurance Brokerage ($140-200 billion).

The largest market on this list. Standard commercial insurance is highly standardized: the added value of a broker is essentially comparing prices and filling out forms between different underwriters, pure intellectual work. The distribution layer is extremely fragmented, with thousands of small brokers running the same processes without any single firm controlling the customer relationship. WithCoverage and Harper are interesting new entrants.

Accounting and Auditing (the outsourced portion alone is $50-80 billion in the U.S.).

The U.S. has lost about 340,000 accountants over the past five years, while demand has been increasing during the same period. 75% of CPAs are nearing retirement, the licensing path is lengthy, and starting salaries lag behind tech and finance. This structural shortage is driving accounting firms to adopt AI faster than almost any other profession. Rillet is building AI-native ERP to handle accounting directly. Basis started from the Copilot for accounting.

Healthcare Revenue Cycle Management (outsourced portion $50-80 billion in the U.S.).

When people hear "healthcare," they think of judgment-intensive work, but the billing layer is almost purely intellectual work. Medical coding is translating clinical notes into about 70,000 standardized ICD-10 codes. The rules are complex but ultimately are rules. Outsourcing is already mature and billed by results. Autopilot just needs to do the same for less cost. Anterior is leading the way.

Claims Adjustment (including TPA $50-80 billion).

On the other side of insurance policies, claims adjustment is another independent Autopilot scenario. Claims for standard policies are determined by cross-referencing damage lists with policy language, using actuarial tables to set reserves. The workforce of adjusters is aging, and no one is replacing them. The market heavily outsources to independent adjusters and TPAs like Crawford and Sedgwick. One industry, at least two different Autopilot opportunities. Pace is working on claims processing Autopilot, Strala is developing AI-native TPA.

Tax Consulting ($30-35 billion).

The CPA licensing system creates regulatory moats, but 80-90% of the underlying work is intellectual work. For every jurisdiction covered by tax Autopilot, the data moats grow deeper. The complexity of multi-jurisdictions is precisely why small and medium-sized businesses outsource, as no internal accountant can cover all bases. TaxGPT is an early entrant, with Skalar and Ravical in Europe.

Legal Transactional Work ($20-25 billion).

Contract drafting, NDAs, regulatory filings: high ratio of intelligence, routine outsourcing. The work output is standardized enough, and quality is verifiable, so buyers can trust AI outputs without needing deep legal expertise. Harvey is an emerging leader that is quickly pivoting to Autopilot; Crosby and Lawhive are new entrants that are Autopilot-native.

IT Managed Services (over $100 billion).

Every small to medium-sized enterprise outsources IT. Patches, monitoring, user configuration, alert triaging: intellectual work is run repeatedly in thousands of the same environments. Existing software layers (ConnectWise, Datto) sell tools to MSPs. No one has yet sold the result of "your IT is up and running" directly to companies. Edra is automating IT processes, Serval is automating IT support.

Supply Chain and Procurement (over $200 billion).

Most businesses only negotiate seriously with the top 20% of suppliers. The long-tail suppliers are completely unmonitored because it is not cost-effective to have someone do it. Contract leakage accounts for 2-5% of total procurement spending. The entry point is abandoned work: no budget item to justify, no incumbent to replace, just free money. Magentic is developing AI for direct procurement, AskLio is for indirect procurement. Tacto is building a record system and Copilot for the mid-market simultaneously.

Recruitment and Staffing (over $200 billion).

The largest service market on this list. The top of the recruitment funnel (screening, matching, outreach) is purely intellectual work, but closing deals and assessing cultural fit are judgments accumulated through years of pattern recognition. Autopilot's entry point is in high-volume, low-judgment roles, where matching is standardized. Juicebox, Mercor, Jack & Jill are emerging leaders building across the spectrum.

Management Consulting ($300-400 billion).

A huge market, but the work is primarily judgment. An interesting question is whether AI can deconstruct consulting into intelligence components (data collection, benchmarking analysis) and judgment components (strategic advice), where the intelligence level is automated, leaving the judgment layer to humans. The best candidate is to be determined.

The fastest-growing AI company in 2025 will be Copilot. In 2026, many will attempt to transition into Autopilot. They have product and customer recognition. But they also face the innovator's dilemma: selling work means kicking their own customers out of the work. This is the window of opportunity for pure Autopilot companies.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。