Written by: Eli5DeFi

Translated by: AididiaoJP, Foresight News

Looking at Bitcoin mining from the rearview mirror of 2024, it resembles a group of survivalists struggling to navigate the aftermath of the Bitcoin halving while enduring the lingering effects of the "crypto winter."

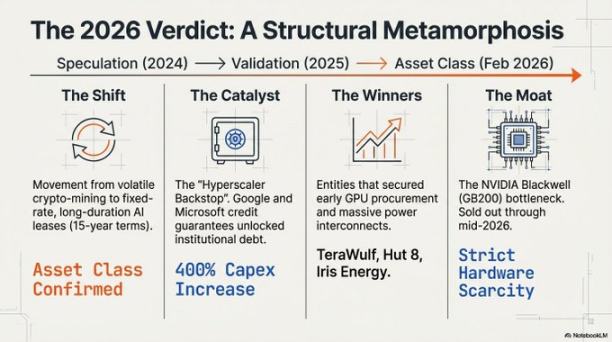

However, by early 2026, this impression has been completely overturned. The industry has undergone a fundamental transformation, evolving from a speculative mining outpost to the cornerstone of a new era—an "AI factory."

Driving this change is a brutal resource competition.

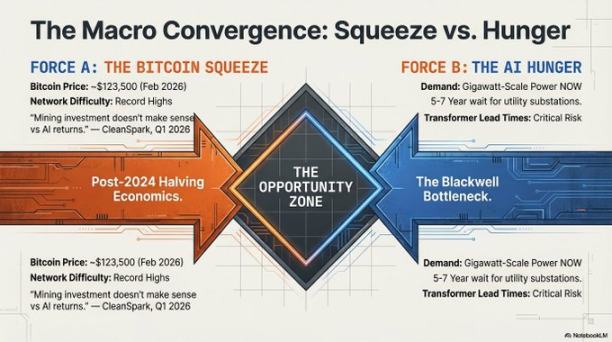

As global demand for AI computing power reaches a fever pitch, the bottleneck has shifted from "not enough chips" to "not enough electricity." High-performance computing requires something that cannot be downloaded or quickly manufactured: land that is already powered.

Those who were once mocked as volatile and unreliable Bitcoin miners have successfully transformed the power and land resources they secured around 2021 into a monopoly of infrastructure capital in 2026, becoming the indispensable "landlords" in the AI gold rush.

The Great Computing Flip

In the landscape of 2026, electricity has become the new scarce resource.

The primary "physical moat" protecting industry winners is the utility's power access points. Building a new substation now takes 5 to 7 years, and those existing sanctuaries—meaning the old mining sites already connected to the grid—have become the only places capable of meeting the immediate demands of cutting-edge AI model training.

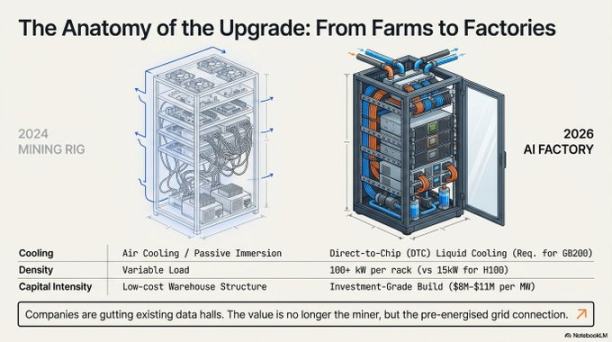

However, the entry threshold has shifted from merely "fencing the land" to a capital-intensive fortress. Due to the requirements of high-density liquid cooling and a global transformer shortage, the cost of constructing an AI-ready facility has surged to about $8 million to $11 million per megawatt. This exorbitant capital expenditure threshold has drawn a clear line of distinction between "execution leaders" and other players:

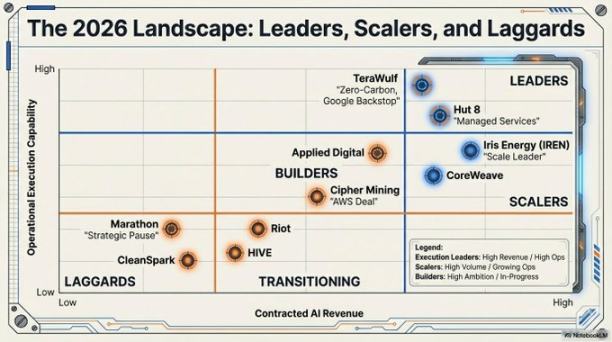

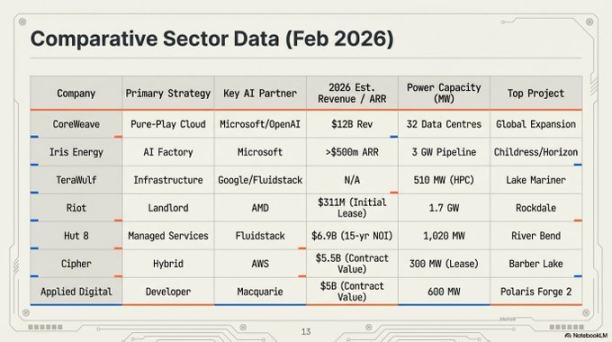

- Iris Energy (IREN): Industry scale leader, valued at $14 billion. It has a combination of 2910 megawatts of power and land to support its expanding "AI factory" footprint.

- Riot Platforms: Holds 1.7 gigawatts of approved power capacity. Riot has transformed its "Texas triangle" assets into strategic hosting centers and recently signed a landmark lease with AMD.

- TeraWulf and Hut 8: Recognized execution leaders. These two companies secured contracts worth $6.7 billion and $7 billion, respectively, successfully transforming their mining operations into high-value, investment-grade AI assets.

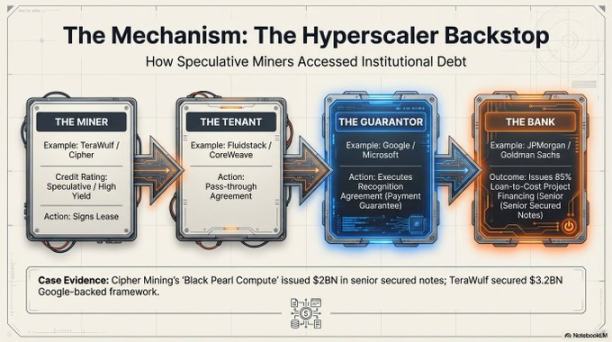

"Large Company Guarantees" - The End of Cryptocurrency Volatility?

Perhaps the most profound change is the structural reevaluation of business models, thanks to "credit enhancement."

In the past, due to the high volatility of Bitcoin prices, top financial institutions were unwilling to lend to miners. This scenario changed with the emergence of "large company guarantees."

Through "recognized agreements," industry giants like Google and Microsoft now provide financial guarantees for the rent paid to these former miners.

As a result, contracts that were once high-risk for miners have transformed into low-risk credit contracts for tech giants. The outcome is that the industry can enter the bond market at a preferential rate of about 7.125%. Companies like Cipher Mining and Hut 8 can secure project financing of up to 85% of project costs from JPMorgan and Goldman Sachs, which will not dilute equity. This "pay without dispute" landlord model has attracted substantial capital inflow from institutions like Vanguard, Oaktree, and Citadel.

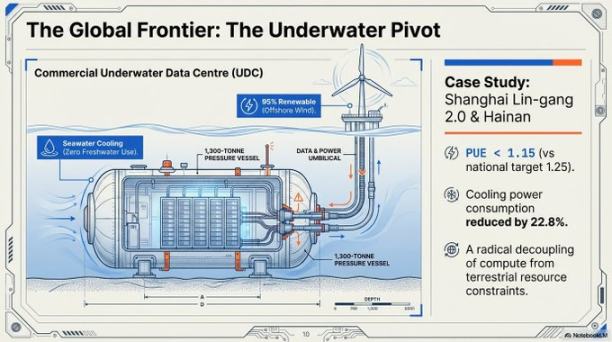

Blackwell Reality and Underwater Data Centers

The technological requirements of AI in 2026 make the past designs of air-cooled mining machines not only obsolete but also impractical for deploying high-density AI clusters.

The NVIDIA Blackwell GB200 NVL72 platform, with power consumption of up to 120 kilowatts per cabinet, forces the industry to move towards liquid cooling technology directly to the chips.

To address both cooling and land constraints, the industry has begun to look towards the "blue economy." Shanghai's Lingang 2.0 project serves as a model for commercial-scale underwater data centers.

- Technical indicators: The power usage efficiency of this facility reached 1.15, far exceeding the national target of 1.25. It uses seawater as the primary cooling source, reducing total power consumption by 40-60%.

- Precision deployment: Guided by GPS, the "Three Navigation Style" vessel can precisely submerge these 1300-ton underwater pods with zero margin of error, powered by offshore wind energy, completely removing the resource limitations on land.

"Blackwell Moat" and Hardware Holders

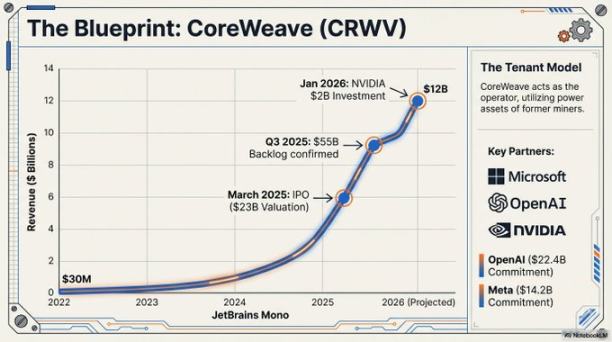

By 2026, a "supply chain wall" has solidified the hierarchy within the industry. Since NVIDIA's Blackwell architecture chips sold out before mid-2026, an order placed in 2024 has become a competitive barrier.

Without chips, electricity is useless; without electricity, chips are just bricks. The winners are those companies that have locked in both electricity and chips early on.

CoreWeave is preparing to go public with a valuation of $35 billion, backed by its massive hardware orders, including a $22.4 billion commitment from OpenAI. Those who failed to secure chips during the 2024 window have essentially been locked out of the core market for AI infrastructure.

"The Blackwell architecture has a backlog of 3.6 million units, effectively locking out latecomers from the primary market for AI infrastructure, a situation that is unlikely to change in the foreseeable future." - Jensen Huang, CEO of NVIDIA, 2026.

Beyond Mining Machines

The transition from "Bitcoin factory" to "AI digital infrastructure hub" marks a once-margin industry maturing into a significant component of global industrial policy.

The isolated, purely mining model is nearing its end. Instead, we have industrial-scale energy transition companies. They view computation—whether it be the SHA-256 algorithm for Bitcoin or training large language models—as an interchangeable output of their core electric assets, distributed according to demand.

As these gigawatt-scale "AI factories" become permanent components of the power grid, we must ask:

In a scenario where the income disparity per megawatt is so stark, can a purely mining model without AI business diversification continue to survive? More importantly, as these facilities transition from electricity-flexible "mining farms" to requiring stable supply AI "baseload", how will the global power grid adapt? At that point, data centers will no longer simply be electricity consumers but designers and architects of the power grid.

The mining machines have changed, but this high-risk energy arbitrage game has just begun.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。