Author: Jae, PANews

Conspiracy theories often spread more easily than the truth, and this is also true in the crypto world.

Especially during times when prices are stagnant and the market is anxious. When Bitcoin repeatedly struggles below $70,000, and when every trading day of the US stock market encounters strange selling pressure at 10 AM, investors can't help but wonder if a mysterious hand is manipulating the market.

As Jane Street becomes embroiled in legal disputes with Terraform Labs and harsh accusations in the crypto market, a miraculous phenomenon occurs: the clockwork-like "10 AM sell-off" scenario strangely disappears.

This New York-based quantitative trading giant, known for its low profile and high-frequency algorithms, happens to be an authorized participant (AP) for top Bitcoin spot ETFs like BlackRock and Fidelity.

On social media, Jane Street has been identified as the culprit hiding in the shadows of algorithms, pressing the "sell-off button" on time every day.

After systematic sorting, PANews found that Jane Street is not the real culprit behind Bitcoin's price drop, but it has indeed become the projection of market anxiety. A sufficiently powerful, sufficiently mysterious, and sufficiently suitable scapegoat to play the "villain" role.

Social Media Ignites, Jane Street Accused of Being the "10 AM Sell-Off" Behind-the-Scenes Manipulator

The story begins with a perfectly ordinary observation.

Since November 2025, keen traders have noticed that at a specific time shortly after the US stock market opens, around 10 AM Eastern Time, Bitcoin spot ETFs always encounter a wave of unusually large selling pressure. This has been nicknamed the "10 AM sell-off strategy" by the market.

However, this is not an ordinary pullback. Selling pressure typically concentrates half an hour after the market opens, quickly breaking through the prevailing liquidity depth, triggering a cascade of liquidations of leveraged long positions. Prices touch daily lows in panic, and then gradually stabilize.

This highly consistent "timestamp" has led market participants to sniff out the taste of algorithms.

Milk Road points out that the underlying logic of this operation is to exploit the weak liquidity early in the US stock market opening to create price crashes that lower the cost of subsequent accumulation. This behavior is known as "brushing down the trading price" in traditional financial markets, aimed at profiting from the market's structural vulnerabilities.

The fuel for conspiracy theories was further ignited in February 2026.

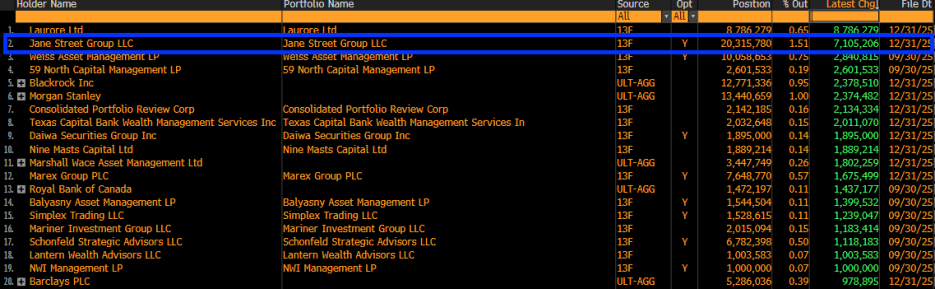

Jane Street's submitted 13F holdings report showed that it significantly increased its holdings of over 7.1 million shares of BlackRock's spot Bitcoin ETF (IBIT) in the fourth quarter of 2025, bringing its total holdings to 20.315 million shares, valued at approximately $790 million.

Once the data was released, social media exploded: since Jane Street is accumulating Bitcoin on such a large scale, isn't the 10 AM sell-off just to lower the cost of building a position?

A logical chain seems to emerge: motive (accumulation) + means (algorithm) = culprit (Jane Street).

However, Frontier Investments CEO Louis LaValle poured "cold water" on this: viewing the 13F disclosure as a simple "long accumulation" is a fundamental misunderstanding of the market-making business model.

As a principal market maker and AP for IBIT, Jane Street's ETF shares are more likely held to balance its options positions or execute hedging strategies, rather than making a one-sided bet.

The Disappearing Strategy Amid Legal Storms, Regulatory Overflows Deterring Sell-Off Algorithms

If the 13F data only triggered market misinterpretations, then the subsequent phenomenon added empirical color to this debate.

On February 24, Todd Snyder, the liquidator of Terraform Labs, filed a lawsuit accusing Jane Street of using a private communication channel established with Terraform insiders (former intern Bryce Pratt) to liquidate accurately just hours before the May 2022 Terra ecosystem collapse, suspected of insider trading and market manipulation.

Almost at the same time, Jane Street also faced accusations from the Securities and Exchange Board of India (SEBI) for manipulating the BANKNIFTY index, leading to a subsequent fine of $550 million.

The spotlight of the law suddenly illuminated.

Strangely, after the lawsuits related to Jane Street became public, the originally regular morning 10 AM selling pressure significantly eased or even disappeared.

This is difficult to explain by coincidence.

PANews believes that in the field of financial engineering, when a trading strategy is widely recognized or questioned by regulators, its profit margins (Alpha) will quickly diminish. The increase in regulatory risks will force algorithms to self-restrict, shifting from "aggressive profit-seeking" to "compliance hedging," which may directly lead to the collapse of specific sell-off patterns.

The disappearance of the "10 AM sell-off" phenomenon precisely indicates that it once existed and is highly related to regulatory pressure. But does this prove that it was Jane Street's "unique strategy"?

The answer remains ambiguous, but at least one thing is certain: when regulatory agencies scrutinize the internal operations of market makers, certain trading behaviors that skate the gray areas may be forced to cease due to compliance pressures.

10 AM Sell-Off Contradicts Market-Making Logic, Conspiracy Theories Hard to Establish

Although the community tends to blame price declines on the misdeeds of a single entity, the conspiracy theory accusing Jane Street of "deliberately suppressing Bitcoin prices" fundamentally does not hold up in the eyes of its opponents.

Keone Hon, co-founder of Monad and former employee of quantitative giant Jump Trading, along with Julio Moreno, head of research at CryptoQuant, provided strong technical counterarguments to this.

Keone Hon pointed out that shorting IBIT is difficult to unilaterally suppress Bitcoin prices.

Although the trading price of IBIT is anchored to Bitcoin, it is essentially a secondary market stock. If IBIT experiences a significant discount, APs and arbitrageurs will quickly intervene, buying the shares at low prices and redeeming Bitcoin in the primary market to close the spread. This arbitrage mechanism dictates that IBIT cannot independently decline outside of the spot price.

Julio Moreno argues that Jane Street's operations are no different from any "Delta neutral" fund.

"Real large market makers do not bet on direction," Xin Song, CEO of GSR Markets, a leading crypto market maker, stated in an interview with PANews.

Indeed, for market makers like Jane Street, bearing directional risk is extremely dangerous; they pursue a balance where "net risk exposure equals 0."

When Jane Street provides liquidity for IBIT as an AP, they face continuously changing inventory risks. If clients buy large amounts of IBIT, Jane Street, as the seller, needs to hold a short position. To hedge this position, they typically buy an equivalent amount of Bitcoin in the spot or futures market. This process is referred to as "dynamic hedging."

In this model, Jane Street's profits do not come from price increases or decreases, but from:

Bid-Ask Spread: earning returns by buying slightly lower prices and selling at slightly higher prices;

Funding Rate Arbitrage: locking in risk-free basis profits by buying ETF spot and simultaneously selling contracts in futures markets like CME (Basis Trade).

Although both strategies involve a large number of sell operations, they correspond to an equal amount of buying operations, theoretically leading to a neutral net price impact on the market.

Macroeconomic analyst Alex Krüger also released data to refute this: since January 1, the cumulative return rate of IBIT from 10 AM to 10:30 AM Eastern Time is 0.9%.

PANews believes that from a quantitative perspective, the "10 AM sell-off" is more likely due to the opening volatility of the US stock market triggering large-scale hedging demand. As the liquidity of IBIT is in a reconstruction phase at the early opening, this hedging operation gets amplified into what appears to be price manipulation.

In fact, giants like Jane Street hold substantial balance sheets, and if Bitcoin prices were to collapse due to their manipulation, the billions of dollars in related assets and derivative positions they hold would also face extreme liquidity risks and counterparty risks.

Structural Issues in Bitcoin Spot ETF Price Discovery Mechanism

Although conspiracy theories are denied by the technicians, ProCap CIO Jeff Park believes: the root of the problem lies within the current AP mechanism of Bitcoin spot ETFs.

The key to AP's significant impact on prices lies in its special legal status. As APs, organizations like Jane Street enjoy privileges under the SEC’s regulatory framework that ordinary traders cannot access:

Short Selling Rule Exemption: APs are often not bound by ordinary securities short selling restrictions during their market-making tasks. This means they do not need to borrow the spot to sell ETF shares and can hedge using Bitcoin futures instead of buying the spot;

Cash Model: Most current Bitcoin spot ETFs adopt a "cash creation/redemption" model, which is fundamentally different from the conventional "physical model" (like gold ETFs).

Jeff Park further points out that the AP mechanism may be undermining the price discovery function of the Bitcoin spot market.

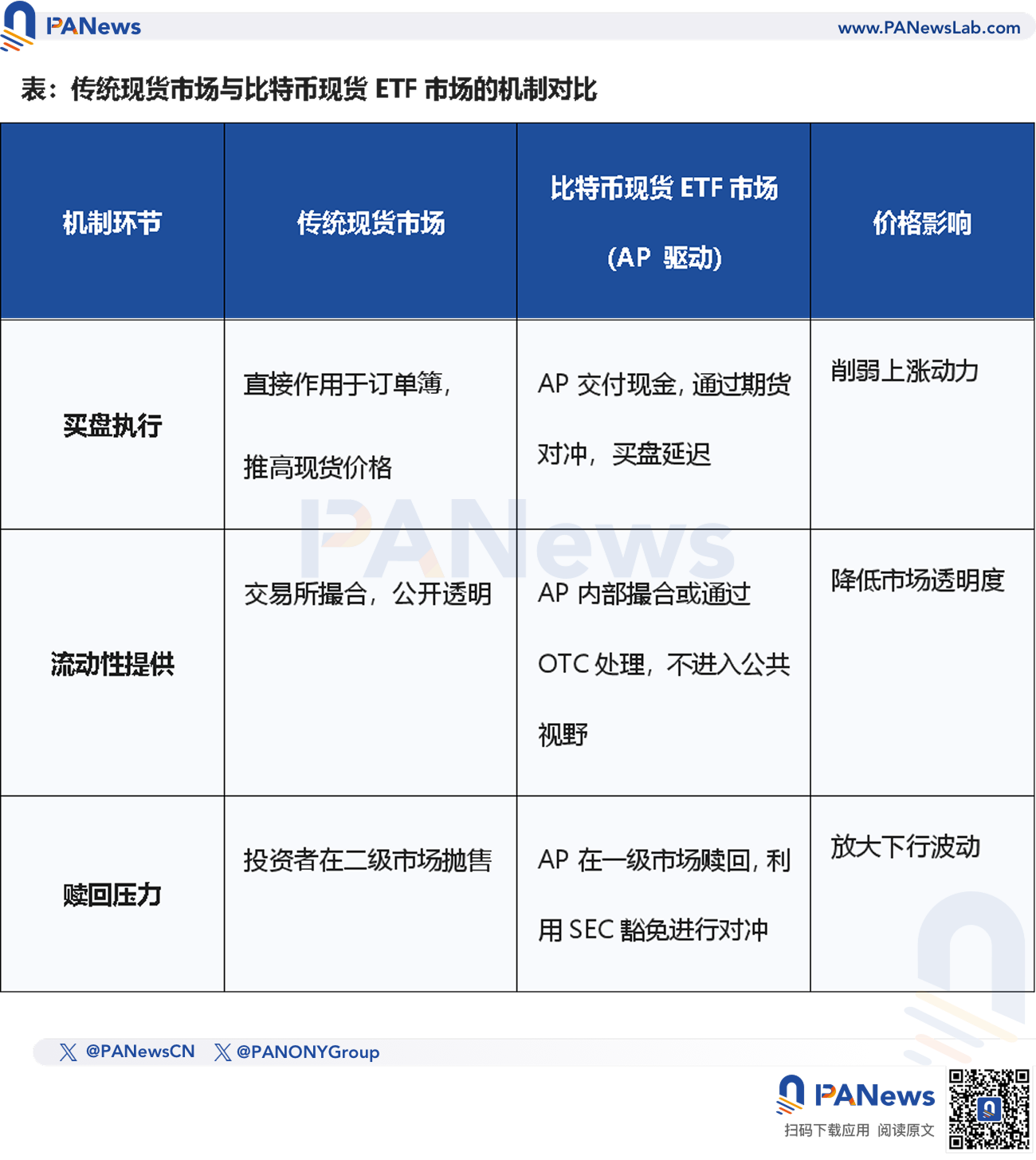

A deeper issue lies in the "cash" model itself. Bitcoin remains in the hands of APs for a very short period, spending most of its time "locked" in custodians' cold wallets. PANews believes that this "locked state," while reducing circulating supply, also cuts off the direct link between the ETF and the spot market.

Ideally, demand for ETFs should directly translate into the spot market. However, due to the presence of APs, this transmission process becomes mediated. APs often hedge risks through futures contracts rather than directly buying Bitcoin in the spot market.

The result of this behavior is that despite ETFs displaying net inflows of funds, the actual buying in the spot market does not reflect synchronously.

PANews believes that when Jane Street and other APs utilize short selling exemptions to hedge via futures, they are effectively only "synthesizing" demand for Bitcoin. This leads to ETF fund inflows potentially failing to equivalently translate into upward pressure on spot prices, thereby objectively forming a "soft suppression" of prices.

This structural mismatch results in a paradox: the larger the ETF, the more concentrated the Bitcoin price discovery rights are in a few APs. And Jane Street is one of the central nodes of this power structure.

Is the Quantitative Industry the Ceiling for Market Uptrends?

“As long as quantitative persists, declines will continue.”

The view that "the quantitative industry suppresses A-share upward movements" is widely circulated on social media, and even the parent company of DeepSeek, a private equity giant, is being accused of utilizing cutting-edge AI technology to excel in models while simultaneously being criticized for "harvesting liquidity" in the secondary market using "dimensionality reduction" algorithm tools, though this perspective is more of an emotional outburst.

A profound question is being posed: Is quantitative investment an "evolution of industrial civilization" in the market, or an "invisible suppressor" of healthy stock market growth?

Today, algorithmic trading (including high-frequency trading, algorithmic execution, and quantitative hedging) accounts for over 70% of the US stock market. In contrast, the quantitative penetration rate in the relatively nascent A-share market has seen a leap from 5% to around 25%-30% over the past ten years.

Even more surprising are the performance records of top hunters.

Contrary to popular belief, even with the increasing proportion of quantitative trading and the annual returns of top institutions, the S&P 500 index has cumulatively risen by as much as 260% over the past decade, while the CSI 300 index has only risen by about 60%.

This indicates that the growth of quantitative institutions does not necessarily have an adversarial relationship with the stable growth of the stock market.

Instead of saying that quantitative suppresses market uptrends, it is more accurate to say that it profoundly changes the speed of wealth distribution. In the US stock market, quantitative has completed industrial transformation; in the A-share market, it may still be in its growing pains; while in the crypto market, quantitative giants are reconstructing pricing power through structural tools (such as the ETF AP mechanism).

The so-called "sense of suppression" is essentially an impotence felt by traditional investment methods when faced with high-frequency algorithms and complex financial engineering. Quantitative will not disappear; it will only become a part of the market's breathing.

For crypto players, rather than searching for who the "villain" is, it is better to track the evolution of the ETF mechanism. Understanding the operational logic of this "Wall Street mint" is an essential lesson for every investor.

Conspiracy theories always spread more effectively than the truth because they are simple, direct, and align with emotions, but the real market is much more complex and also more boring than conspiracy theories.

The real enemy may never be a specific institution, but our neglect of complex mechanisms and our thirst for simple answers.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。