Author: CryptoSlate / Oluwapelumi Adejumo

Translated by: Deep Tide TechFlow

Deep Tide Guide: Bitcoin recently rebounded to $70,000, and a conspiracy theory linking Jane Street to "pressure selling at the US stock market open" went viral in the crypto community. This article dissects this claim from three dimensions: on-chain data, ETF structure, and options positions, concluding that the real problem is not Jane Street, but the price discovery black box of the ETF era—the opacity of institutional hedging is making it increasingly difficult for ordinary investors to understand the market.

The full text is as follows:

Bitcoin rebounded sharply to nearly $70,000 in the past 24 hours, reigniting a familiar debate in the crypto market: Do Wall Street institutions operating within the spot ETF ecosystem have too much influence over price discovery?

This time, the target is Jane Street—a quantitative trading firm that is an important intermediary for ETFs and is also a defendant in a new lawsuit related to the 2022 Terraform Labs collapse.

On social media, traders linked Bitcoin's recent rebound to a claim that a so-called "10 a.m. sell-off program" observed near the US stock market opening suddenly disappeared after the lawsuit became public.

This theory spread rapidly as it combined two already resonant sentiments: distrust of large trading institutions and anxiety about the increasing involvement of the Bitcoin market through traditional financial channels.

However, the evidence supporting the "collusion to suppress Bitcoin" narrative remains weak.

This incident more clearly reveals that the structure of the spot Bitcoin ETF has made it increasingly difficult for many investors to distinguish between genuine spot demand and market-making, hedging, and arbitrage activities.

In this sense, the Jane Street controversy transcends accusations against a single institution. Its core is how Bitcoin's new institutional infrastructure shapes price discovery, and whether the market is becoming more efficient or increasingly opaque.

The Origins of the Jane Street Bitcoin Rumor

The rumors took shape after Bitcoin's significant rebound over two consecutive trading days. Users on X began to assert that the so-called "10 a.m. sell-off program" had disappeared.

Notably, the X account Negentropic, operated by Glassnode co-founders Jan Happel and Yann Allemann, played a crucial role in spreading this theory. They claimed, "The Jane Street lawsuit was made public, and Bitcoin's 10 a.m. crash miraculously vanished."

This claim quickly gained attention because Jane Street is not a nobody. It is one of the largest trading firms in the world and a well-known participant in the Bitcoin ETF market, serving as an authorized participant for IBIT (BlackRock's spot Bitcoin ETF).

In practice, this closely integrates it into the core mechanism that maintains the alignment between ETF share prices and the value of underlying holdings.

Meanwhile, legal disputes against the company further fueled the controversy.

The liquidators of Terraform Labs filed a lawsuit in Manhattan, accusing institutions like Jane Street of profiting from material non-public information related to Terraform's liquidity operations during the collapse of TerraUSD in May 2022.

The complaint alleges that Terraform withdrew $150 million of TerraUSD liquidity from Curve's 3pool, while wallets associated with Jane Street withdrew about $85 million within minutes of the announcement of this information.

Jane Street denies any wrongdoing and claims the case is a desperate attempt to shift responsibility for the losses caused by Terraform's own actions onto others.

This lawsuit does not prove anything about current Bitcoin trading.

But it explains why traders would quickly link Jane Street to an observable market pattern. In the crypto world, trust is often fragile, and institutions accused in one market event often become suspects in the next.

Industry Insiders Refute the Rumor

Against this backdrop, some Bitcoin traders believe that the top cryptocurrency has been subjected to mechanical sell-offs near the US stock market openings for months, liquidating long positions and creating a liquidity vacuum in a thin order book.

If such sell-offs disappeared after Jane Street faced new legal pressures, perhaps the company was always pressuring the market.

Moreover, its early association with FTX founder Sam Bankman-Fried also cast a shadow over its reputation. Bankman-Fried worked at this trading firm before founding FTX.

This narrative is emotionally compelling, but asserting it is much easier than proving it.

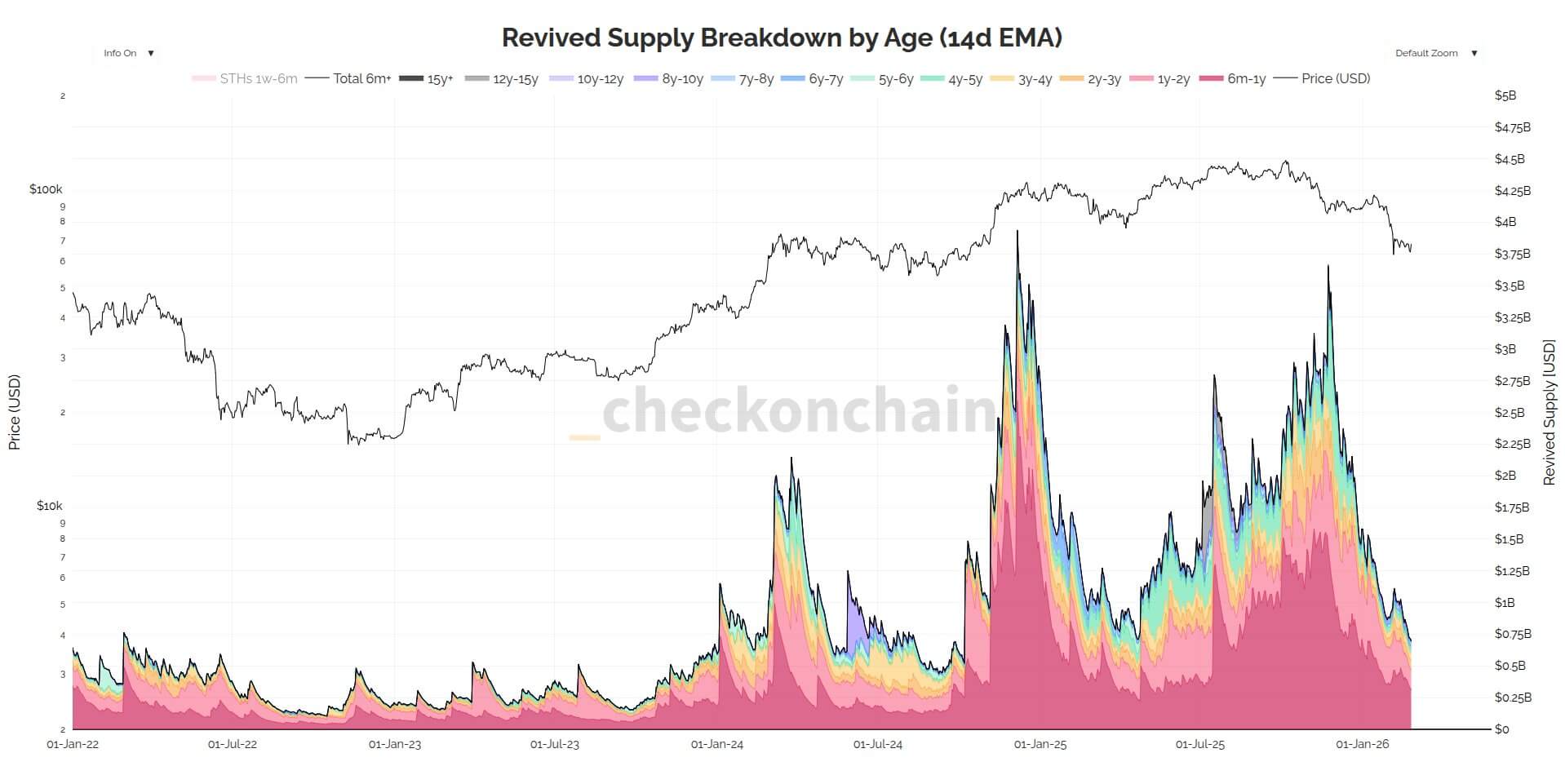

On-chain analyst James Check from Checkonchain directly refuted this argument, stating that Jane Street did not suppress Bitcoin; instead, long-term holders selling into the market better explains the price movements.

CryptoQuant's research director Julio Moreno shares a similar view, arguing that this theory overlooks a more obvious driving factor: a sharp decline in spot Bitcoin demand since early October 2025.

He adds that the operating mechanism attributed to Jane Street resembles the delta-neutral position management methods commonly used by many trading firms.

The value of these rebuttals lies in their direct confrontation with the core weakness of the rumor: Bitcoin, before entering 2026, was already under pressure from broader macro repricing forces.

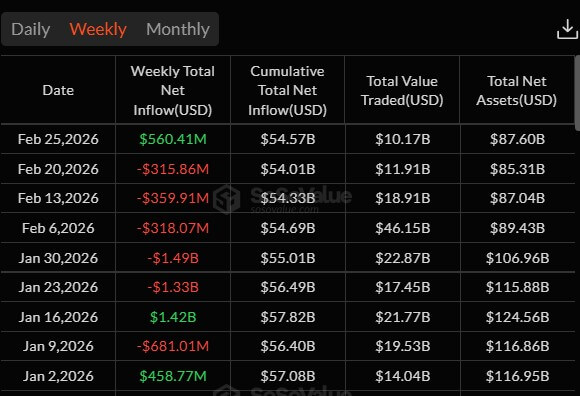

SoSo Value data shows that institutional investors have continuously reduced exposure to Bitcoin ETFs for five weeks, with total outflows from spot Bitcoin ETFs reaching about $4.5 billion.

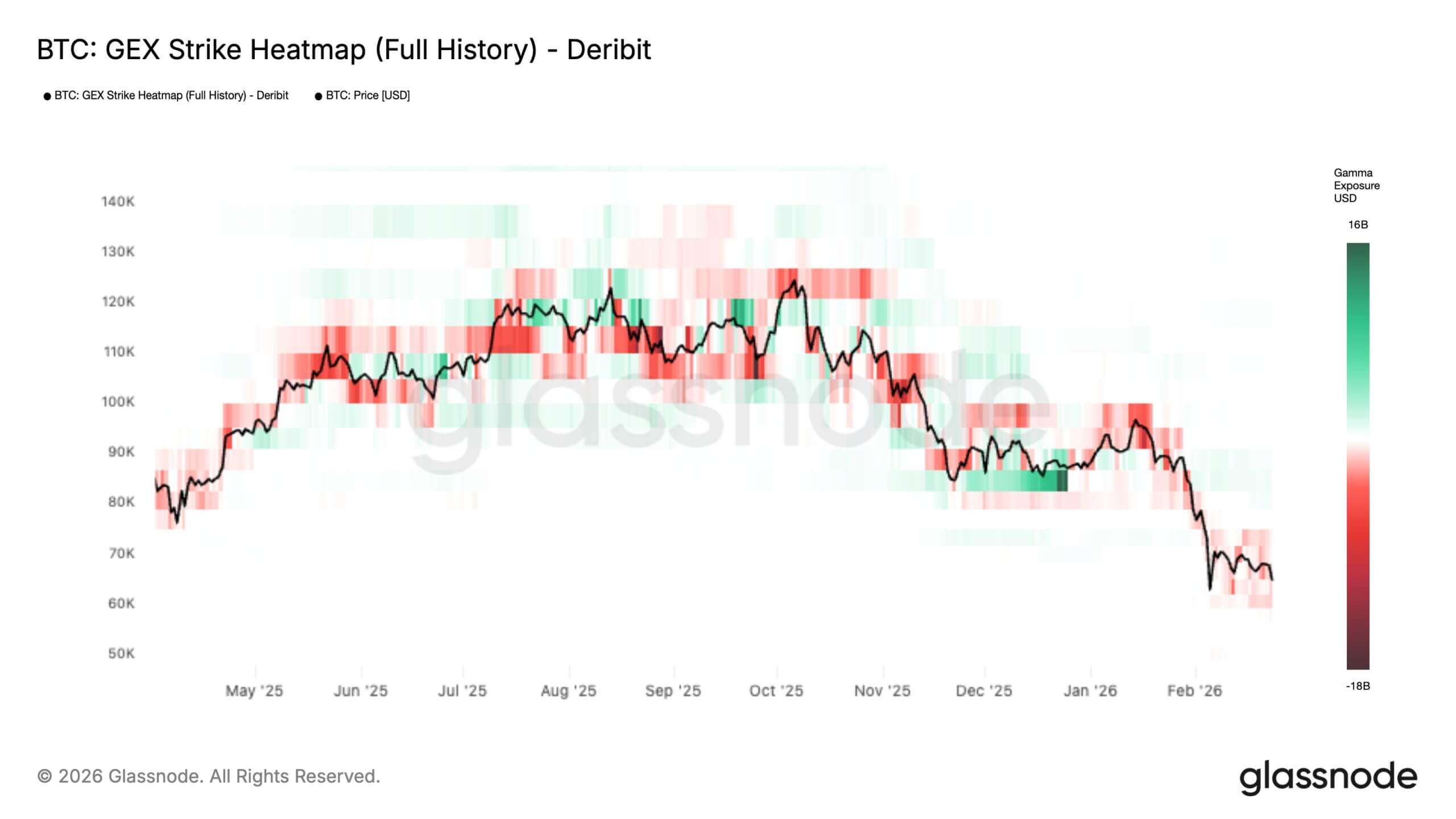

Meanwhile, Glassnode data shows that the recurring market pressures early this month have triggered structural changes in the Bitcoin options market, moving towards a more unstable pattern.

The agency notes that the historical gamma exposure (GEX) heat map shows that negative gamma in the current price and lower regions is expanding, while the "resistance wall" of positive gamma above the spot price is diminishing.

In plain language: those options positions that typically serve as shock absorbers are fading, leaving the market increasingly in a range where hedging flows no longer buffer declines; instead, they amplify downward movements.

This dynamic is important: when prices are in a short-gamma range, market makers' delta hedging tends to follow the market trend rather than sell when prices drop and buy when they rise.

The result is that the market can move faster and farther on relatively small catalysts—leading to greater intraday volatility and an increased risk of cascading price movements through key levels—until Bitcoin reaches the next thick "gamma wall" when hedging switches back to a buffering mode.

In other words, traders are already in an environment where it's easy to see "intent" anywhere. When liquidity is thin and leverage is high, almost any sharp movement can appear to be organized behavior.

The ETF Pipeline is Harder to Read than It Appears

The deeper issue raised by the Jane Street controversy is structural, not targeted at any single institution.

As ProCap Financial's Chief Investment Officer Jeff Park argues, the real issue is not whether a single company is "exclusively suppressing" Bitcoin, but whether the ETF market structure gives authorized participants a level of discretion that the public cannot see through.

This point is crucial, as investors are often accustomed to interpreting ETF disclosure data as clean directional signals—but that is not the case. While 13F filings can show a large long position in an ETF, SEC guidelines clearly state that short positions are not included, and short options will not offset long positions net.

In practice, the market may see the inventory but not the futures, options, or other hedging tools that wrap around it.

This opacity is further exacerbated by the way trust is built. BlackRock's disclosure for IBIT shows that the trust can deal with share creation and redemption through authorized participants and can also trade with specified Bitcoin counterparties.

As of this filing, these counterparties include JSCT, LLC, the affiliate of Jane Street Capital, and affiliates of Virtu Americas, Virtu Financial Singapore.

The document also shows that the list of authorized participants has expanded to include institutions like JPMorgan, Castle Securities, Citigroup, Goldman Sachs, UBS, Macquarie, and more, with increasingly more companies gaining access to the ETF creation and redemption mechanism.

Park's viewpoint is that this structure distorts outsiders' interpretation of ETF cash flows.

Under the old cash model, creation of ETF shares required funds to buy spot Bitcoin. But after the SEC approved physical creation and redemption of crypto ETPs in July 2025, authorized participants gained greater flexibility in obtaining and delivering the underlying assets.

The SEC indicated that this change would reduce product costs and improve efficiency. But it also means that an authorized participant's exposure can be managed through a broader range of tools and counterparties, making it harder to determine when ETF activity reflects genuine spot demand versus inventory management, basis trading, or hedging builds.

These are not evidence of abuse, and Park's argument does not depend on proving that Jane Street or any other company has engaged in misconduct. His sharper point is that in the era of Bitcoin ETFs, a black box has been inserted between public holdings data and the underlying price discovery process.

The starting point of trading looks like ordinary market-making behavior, and the endpoint does too. What is hard to observe is the intermediate links: whether hedging is done through spot, futures, swaps, or some combination of the three, and whether natural arbitrage mechanisms are genuinely transmitting real spot demand onto Bitcoin.

This is precisely why the Jane Street rumors resonate. It is less an accusation against a particular participant and more a signal—revealing how limited the market's understanding is of its own operational pipeline.

Why the US Stock Market Open Feels Like a Selling Pressure Zone

The "10 a.m. theory" sounds plausible because even without intentional manipulation, the US stock market open is inherently a real volatility window.

This time period is filled with cross-asset rebalancing, stock-related risk adjustments, and derivative hedging operations.

In a market where ETF intermediaries can hedge inventory with futures or other tools, futures may pull spot prices, not just follow them.

When the order book is thin, these actions may appear larger and more conspiratorial than they actually are. Bloomberg reported earlier this month that Bitcoin market depth is still over 35% lower than in October, highlighting how fragile liquidity has become.

Meanwhile, macro analyst Alex Kruger stated that existing data does not support the claim of a "systematic sell-off at 10 a.m. every day."

He wrote that since January 1, IBIT's cumulative return in the eastern time window from 10:00 to 10:30 has been positive at 0.9%, while the window from 10:00 to 10:15 decreased by 1%.

In his view, this is noise, not evidence of a repeatable suppression program.

More importantly, he says, the performance patterns of these two windows closely align with Nasdaq, indicating a general repricing of risk assets rather than a Bitcoin-exclusive operation.

This interpretation aligns better with the broader market context than the viral narrative.

If Bitcoin is increasingly packaged through ETFs as a macro risk asset, then the pressure at the US stock market open—especially in a thinly-traded market—repeatedly creating weakness in Bitcoin during the same intraday window should not be surprising.

On-chain Scarcity is Clear, Price Discovery is Not

The supply of Bitcoin is fixed by protocol. Any changes in the ETF market structure cannot alter this. What is changing is the increasing proportion of demand—and skepticism—now flowing through the channel.

The Jane Street controversy reveals the rift between these two realities. On-chain scarcity is transparent, while the institutional systems layered on top are not.

Investors can see the circulating shares of the ETF and some disclosed holdings but cannot see every hedge behind the market makers’ books, every internal net exposure, or every cross-market position.

This gap creates space for misunderstanding and distrust.

Jane Street has also faced scrutiny in other markets, which does not help the situation. In July 2025, India's securities regulator issued a temporary order regarding an index manipulation case involving a Jane Street entity, and Reuters later reported that SEBI banned the company from entering the Indian securities market during the case review. Jane Street denied any wrongdoing there as well.

The Indian case is unrelated to Bitcoin, but it explains why when Jane Street's name reappears in the headlines, crypto traders are ready to imagine the worst.

However, the existing facts do not prove that Jane Street has engaged in deliberate Bitcoin suppression schemes.

What they prove is something else: The post-ETF era Bitcoin market has become easier to enter, more deeply integrated with institutions, and harder for ordinary investors to interpret.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。