Written by: David, Deep Tide TechFlow

The cryptocurrency market is entering winter, BTC has halved from its peak.

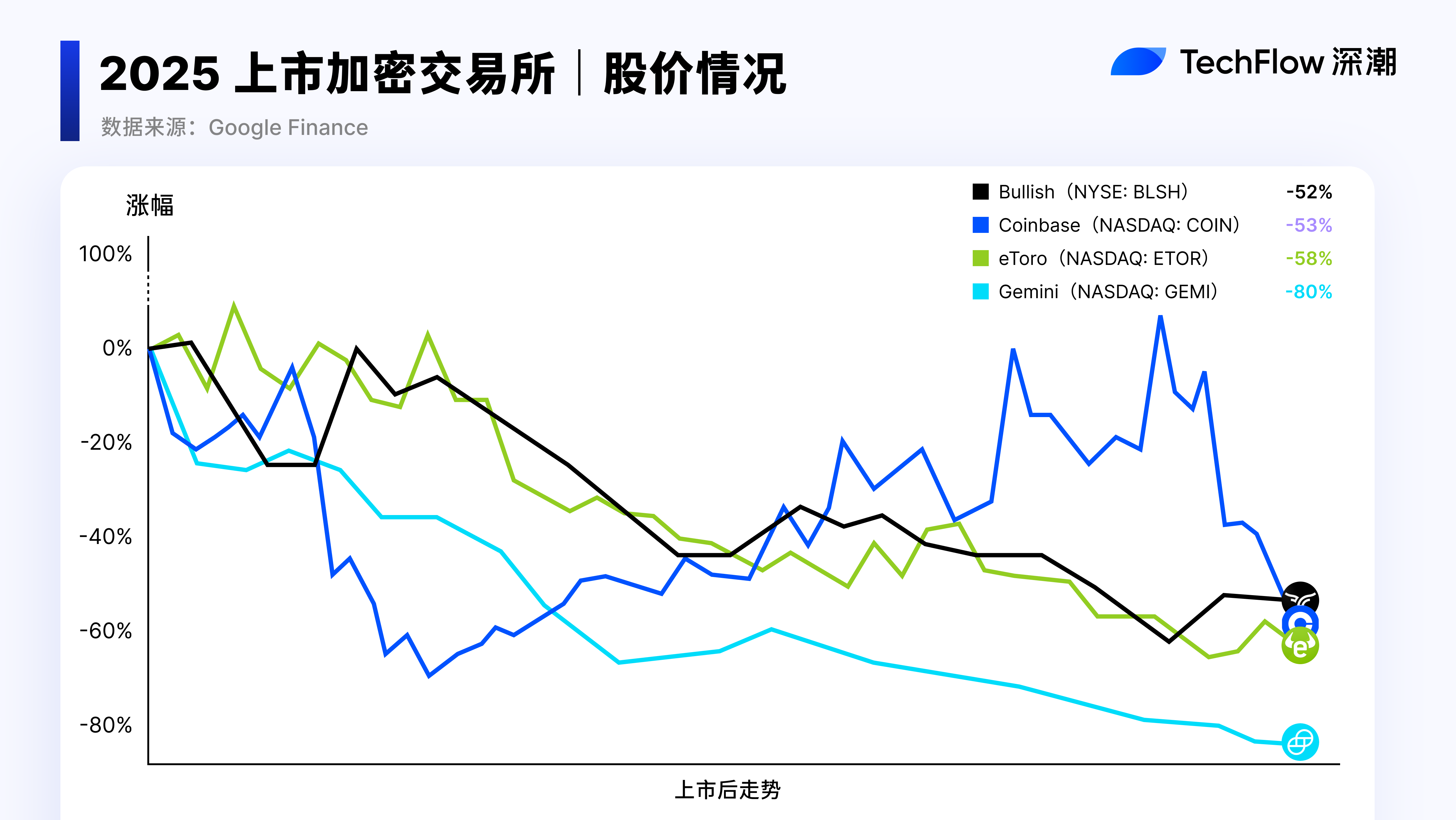

Beyond the price of coins, another set of data is not good either: nearly all the cryptocurrency companies that planned to go public in 2025 have also faced disaster.

Gemini has dropped nearly 80% from its offering price, Bullish is down over 52%, eToro has fallen 58%, and Circle is down 11%. Kraken's application has been submitted, with a valuation of $15 billion to $20 billion, waiting in line to go public.

These cryptocurrency exchanges have chosen the traditional path: grow revenue, then IPO, letting the public market price them, but the answers given by the public market are very harsh.

At the same time, another path is not much better.

BNB and Binance have no legal equity relationship, FTT has gone to zero, Coinbase does not issue tokens, but there is no bridge between equity and cryptocurrency users.

To date, there has not been a satisfactory value anchoring solution for the category of exchange tokens.

Last week, Backpack Exchange offered a new answer: tokens staked for a year can be exchanged for 20% of the company's equity at a fixed ratio. This is the first of its kind in the cryptocurrency industry.

What exactly are the exchange tokens you hold anchored to? Is it a coupon that shrinks with trading volume or is it part of the company's value?

After the collective crash of cryptocurrency company IPOs in 2025, this question has become more urgent than ever.

When Tokens Lead to Equity

The token empowerment plan announced by Backpack Exchange on February 23 can be summed up in one sentence:

Users who stake tokens for a year can exchange them for company equity at a fixed ratio, with the reserved equity pool currently accounting for 20% of the company.

Its CEO, Armani Ferrante, explained the reasoning behind this on X:

“The utility of most tokens is a promise; unless a protocol is decentralized enough that the team can run off to the Bahamas to drink coconut juice and it can still operate, the so-called value of tokens is empty talk.”

This statement is harsh but not exaggerated.

The value of most exchange tokens depends on the continuous operation of the team, but holders receive no ownership. Backpack’s choice is to break through this layer of window dressing and provide direct equity.

This plan relies on the upcoming platform token from Backpack.

However, this token has not even been given an official name yet, and the TGE timing is also unconfirmed; Ferrante hinted that it may happen as early as the end of March. But the framework for the token economy has already been laid out.

There will be a total of 1 billion tokens. 25% will be unlocked on the first day, about 250 million tokens, all distributed to users with loyalty points and Mad Lads NFT holders.

This proportion is higher than the common 7% to 15% seen in the industry; Backpack's claim is to allow early users to choose to sell freely instead of being locked up.

The remaining 75% will be split into two halves. 37.5% will go to users, gradually released based on milestones such as product launches and regulatory approvals. The other 37.5% will go into the company treasury, locked until one year after the completion of the U.S. IPO.

The team does not have a direct token allocation; they hold company equity, which can only be realized after the IPO.

This design carries additional significance in a bear market.

Utility tokens rise with trading volume in a bull market but also shrink in a bear market. The buyback strength of BNB depends on Binance's profits, which in turn depend on trading volume, which depends on market conditions.

The chain is long, and every link will be discounted in a bear market.

The equity binding attempts to cut this chain.

If the token can be exchanged for company equity, then its value anchoring will not just be platform trading volume but also the valuation of the company itself.

According to Axios, Backpack is currently negotiating a new round of financing at a pre-money valuation of $1 billion. The theoretical value corresponding to the 20% equity pool is $200 million.

Of course, this $200 million is a paper figure. The exchange ratio has not been disclosed, and legal documents have not been published; there is no timeline for the IPO. But at least in terms of design intent, Backpack has found a value anchor for the token that does not fluctuate entirely with the token price.

This also explains why this plan was announced in a bear market.

In a bull market, the token can sustain its price through trading volume and sentiment; no one cares what it is anchored to. In a bear market, it becomes necessary to answer the question, "With the token price falling, what is this thing I hold still worth?"

What It Means for Holders

What exactly will exchanging tokens for equity yield? As of this writing, Backpack has announced the direction but not the details.

Will it be direct shareholding, options, or some kind of rights certificate? Do holders have voting rights, dividend rights, or the right to information disclosure? Backpack says that the details will be gradually announced in the coming weeks, but the only thing you can be certain of right now is this.

That is, tokens must be staked for a year.

The cryptocurrency industry has seen too many designs of "get on the bus first and pay later," and the final ticket often looks quite different from the promises made when boarding. Before the details are released, the 20% equity pool is an intention, not a contract.

Assuming the details turn out to be reasonable, the next question for the staker is liquidity.

You are locking up a token that can be sold at any time on the exchange for a year, exchanging it for equity in an unlisted company. This is converting a high-liquidity asset into a low-liquidity asset.

Private equity is not like tokens; there is no 24-hour trading market. To realize the equity, you have only two options: wait for the IPO or find an over-the-counter buyer.

And the IPO is the core premise of the entire design.

The earlier mentioned performance of cryptocurrency companies after the IPOs in 2025 has already indicated that an IPO does not equal realizing valuation. There can be a huge difference between the $1 billion valuation offered in the primary market and the final pricing in the public market; the value of the equity held by the staker depends on the latter, not the former.

What if the IPO is delayed or does not happen at all?

The team’s tokens may still be locked, but your equity will also have no exit channel. Ferrante himself has admitted that the IPO could happen soon or far away, or it might not happen at all.

So for holders, the real choice for them is like this:

Do not stake, hold the tokens, endure the price fluctuations but retain liquidity. In a bear market, liquidity itself is already the most scarce resource.

Stake for a year, give up liquidity, betting on: reasonable exchange terms, company successfully going public, and post-IPO valuation holding up. If one of these three conditions is lacking, the expected return on this transaction will shrink significantly.

If Backpack really succeeds in the IPO and maintains its valuation, early stakers might receive the first batch of real company equity acquired through tokens in the industry.

Valuation Reset in a Bear Market

Every bear market in the cryptocurrency market forces out some real issues.

The bear market in 2018 punctured the ICO bubble, with most utility tokens going to zero, leading the industry to reflect on “whether tokens are necessary at all.” After the collapse of FTX in 2022, the focus of reflection shifted to transparency and proof of reserves.

The current set of problems is more direct:

When the token price has halved from its peak, trading volume has shrunk, where is the value anchor for exchange tokens?

No one cared about this question during the bull market. In a bear market, as trading volume shrinks, the value of the token is entirely tied to the platform's short-term operational status, with a weak ability to transcend cycles.

Backpack’s equity binding model, regardless of whether it can ultimately be implemented, at least attempts to address this issue, seeking to give tokens a value support that does not fluctuate solely with trading volume.

But this response is also nested within another layer of dilemma: the valuation of exchanges is undergoing a collective reset.

Before 2025, the valuation logic of cryptocurrency exchanges essentially relied on trading volume multiplied by a multiple. In a bull market, as trading volume expands, valuations inflate accordingly. However, the public market is increasingly unwilling to buy into this.

The share prices of several listed exchange companies plummeted collectively, essentially saying that the public market does not believe your income is sustainable and is unwilling to price at peak levels.

This means that whether it is tokens or equity, anchoring on the valuation of exchanges itself carries cyclical risks.

Backpack links tokens to equity, addressing the identity issue of “what tokens represent,” but not solving the pricing issue of “how much the exchange is worth.”

The latter depends on whether Backpack can differentiate its revenue structure, rather than simply relying on trading fees.

From a broader perspective, most cryptocurrency projects are experiencing a generational turnover in token economic design. At least in a bear market, the industry is being forced to reflect on a question that should have been considered long ago: where should the value of tokens really come from?

Exchanging Future Equity for Today's Lifeline

In the past few years, the business model of exchanges has perhaps been a bit arrogant:

Build a venue, issue a platform token, earn fees from liquidity spilling over in a bull market, and then symbolically use a small portion of profits for buybacks and burns. Users holding the tokens are essentially paying for the prosperity of the platform.

But the crypto winter has thoroughly shattered this logic.

When retail investors exit, trading volume shrinks, and the "ultimate exit path" of IPO is also ruthlessly rejected by the public market, exchanges find themselves facing a brutal struggle for self-rescue.

In this stage of stock game, those who can lock in the last remaining funds of users will be able to survive until the next cycle.

When the illusory "token empowerment (such as transaction fee discounts, new token lottery tickets)" completely fails, to maintain user funds willingly on the platform during the prolonged decline, exchanges must present truly significant stakes, which are the company's most core assets:

Equity.

This is a defensive battle to exchange bottom-line cards for survival time.

This year, as long as users' tokens remain locked in Backpack's pool, the platform's TVL has a guaranteed bottom, and business data will not look too bad, allowing that $1 billion valuation story to continue to be told.

You cannot say this is generous; it is more like an extremely pragmatic self-rescue strategy: using equity options of an unlisted company to acquire the most precious asset needed to survive the crypto winter, a stable and non-dispersive financial base.

Backpack's token exchange for equity hopes to become a turning point in the design of exchange tokens, rather than another narrative that failed to materialize in a bear market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。