I. Outlook

1. Macroeconomic Summary and Future Predictions

Last week, the macroeconomic environment in the U.S. was in a quiet transitional period between the end of the year and the beginning of the new year, with almost no new significant economic data released. The market mainly digested previous information and adjusted positions and risk management. The overall tone continued the previous assessment: inflation has clearly retreated but still shows stickiness on the service side, the job market continues to cool, and demand momentum is weak. The Federal Reserve confirmed the end of the rate hike cycle in the December meeting and entered a policy observation period. Holiday factors led to low market liquidity, with U.S. Treasury yields and the dollar maintaining low volatility. U.S. stocks operated at high levels but with converging fluctuations, reflecting a consensus among funds on a "soft landing" while remaining cautious.

Looking ahead, as the holiday season ends and January's economic data returns in abundance (employment, inflation, consumption), the market will reassess the speed and depth of the U.S. economic downturn. For the market, the beginning of the year will shift from "expectation-driven" to "data-driven," with volatility expected to rise, and the directional movement of asset prices will rely more on whether the data supports a moderate slowdown rather than a recession.

2. Market Movements and Warnings in the Cryptocurrency Industry

Last week, the cryptocurrency market experienced a significant rebound against the backdrop of low liquidity at the year's end and beginning. Bitcoin quickly rebounded from around $90,000, driving the overall recovery of mainstream assets. Notably, the MEME sector performed exceptionally well in this round of rebound, with several leading and emerging MEME tokens recording gains far exceeding the market average, with trading volume and on-chain activity amplifying simultaneously, becoming the core direction for capital speculation and emotional release. Funds clearly migrated from defensive assets to high-elasticity varieties, with risk appetite rapidly increasing in a short time.

In terms of warnings, the strength of MEME reflects more of an emotion and liquidity-driven phenomenon rather than fundamental improvement, with volatility and drawdown risks also significantly amplified. Additionally, as January's macro data returns, the market's repricing of interest rates and liquidity may test this round of MEME-led rebound. Overall, the current market still leans towards a phase of repair, and caution is needed regarding the sharp volatility risk following emotional peaks.

3. Industry and Sector Hotspots

Mu Digital, a core platform that raised $2.1 million with investment from Cointelegraph, serves as a unified entry point to top investment opportunities in Asia; with total funding of $10.4 million, RateX, backed by well-known institutions such as Solana, Animoca, and GSR, is a trading protocol for leveraged and spot returns operating across multiple chains, providing yield tokenization and the splitting and trading of returns and principal.

II. Market Hotspot Sectors and Potential Projects of the Week

1. Overview of Potential Projects

1.1. Brief Analysis of Mu Digital, a Core Platform that Raised $2.1 Million with Investment from Cointelegraph—Making Digital Assets Simpler, Safer, and More Valuable

Introduction

Mu Digital is a unified entry point to top investment opportunities in Asia. Whether the market is in a bull or bear phase, you can earn up to 15% returns on stablecoins. Mu Digital unlocks the highest quality yield investment opportunities in Asia—previously available only to high-net-worth clients and large financial institutions.

Now, any user with a crypto wallet can directly access the largest and most reputable government and corporate lenders in Asia.

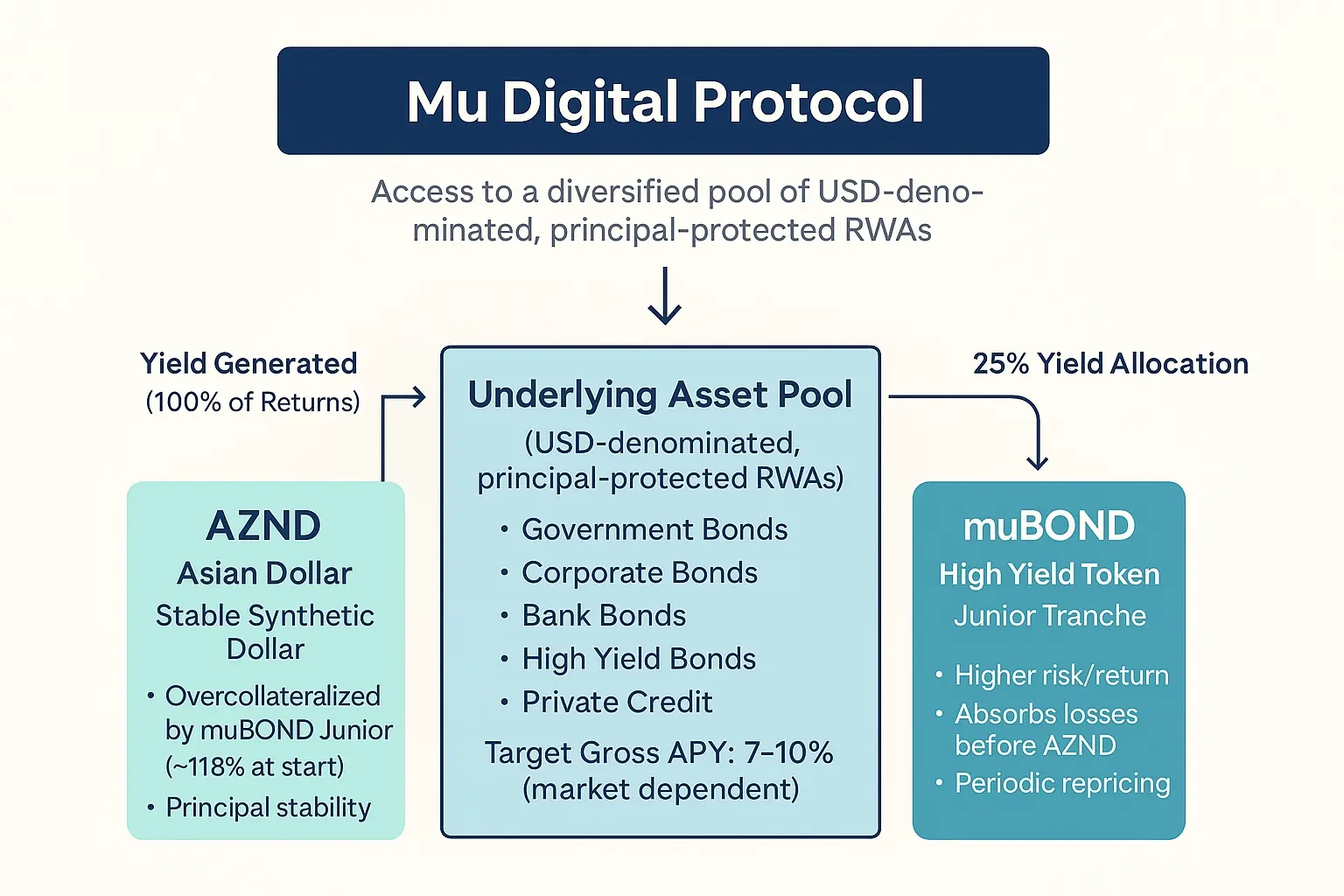

Overview of Mu Digital Protocol Architecture

The Mu Digital protocol provides DeFi users access to a dollar-denominated, decentralized, and principal-protected RWA investment pool through a dual-token structure.

Dual-Token Structure

- AZND: Asian Dollar

A synthetic dollar that pursues capital stability

Typically over-collateralized by the junior position of muBOND (approximately 118% at launch)

75% of the income generated by the asset pool is allocated to the AZND locking contract (see Locking)

- muBOND: High-Yield Token

Junior position, high risk, high potential return

In the event of losses, muBOND absorbs losses first (AZND receives priority protection)

Regularly repriced to reflect the performance of the underlying asset portfolio

25% of the asset pool's income is allocated to muBOND holders

Underlying Asset Pool

The asset pool consists of high-quality fixed-income assets and is held by trusted traditional financial custodians.

All assets are dollar-denominated (no exchange rate risk) and provide principal protection at maturity.

Asset types include but are not limited to:

Government bonds

Corporate bonds

Bank bonds

High-yield bonds

Private credit

Mu Digital aims for the asset pool to achieve a gross annualized yield (APY) of 7–10%, but actual performance may vary due to market conditions and the performance of the underlying asset portfolio.

Yield Generation Mechanism

Mu Digital provides users with sustainable and predictable returns by investing in a diversified, dollar-denominated, and principal-protected fixed-income asset portfolio in the Asia-Pacific region.

The underlying assets are managed by the traditional financial institution Golden Hill Asset Management (GHAM), whose team has professional experience managing billions of dollars in assets, ensuring the best balance between returns and risks.

The asset pool mainly includes:

Government bonds (credit rating BBB or above)

Corporate bonds (investment-grade bonds of large Asian companies, BBB- or above)

Bank bonds (including globally systemically important banks, rated BBB or above)

High-yield bonds (large industrial companies in the Asia-Pacific region, minimum BB)

Private credit (targeted lending projects in cooperation with large financial institutions)

At the same time, Mu Digital and GHAM have jointly established a comprehensive institutional-level risk management framework to ensure that user funds are strictly protected while pursuing stable returns.

Risk Control Mechanism

Mu Digital systematically manages liquidity risk, credit risk, and price risk to achieve stable and controllable returns.

- Liquidity Risk

At least 80% allocated to highly liquid, freely tradable bonds

Private credit (lower liquidity) strictly limited to within 20% of the asset pool

A high proportion of investment-grade bonds to reduce volatility

Maintain credit lines with prime brokers to ensure quick liquidity when selling bonds

- Credit Risk

Aim to maintain an average portfolio rating of BBB or above

Continuously monitor credit events for all positions and regularly assess changes in portfolio ratings

Private credit must co-invest with reputable large financial institutions to reduce counterparty risk

- Price Risk

Control the portfolio's duration to no more than 5 years to reduce the market value impact of interest rate fluctuations

Use a maturity ladder to ensure stable cash flow replenishment and avoid forced selling

Actively take profits when the portfolio performs well (Active Management)

Transparency and Reporting Disclosure

Mu Digital prioritizes transparency as a core principle, providing continuous, verifiable updates to keep users informed about the asset pool's status and the protocol's health.

- Weekly NAV Report

The fund manager will publish the net asset value (NAV) of the asset pool weekly

Disclose market value changes and actual returns of RWA assets

Future updates may be enhanced to higher frequency

- Monthly Fund Performance Report

GHAM publishes monthly performance reports (qualitative + quantitative analysis)

Provides portfolio structure by asset type, duration, and credit rating

Allows users to understand how the portfolio adheres to the risk framework

- On-chain Treasury Wallet

Establish an on-chain treasury to support rapid minting and redemption for authorized users

Wallet address and balance are publicly available in real-time for on-chain self-verification

These funds are completely isolated from company operating funds

Price Stability Mechanism

Mu Digital ensures the price stability of AZND through a layered risk structure, with muBOND serving as the junior buffer layer to absorb priority losses, supplemented by a protocol insurance fund for additional protection.

1. muBOND Absorbs Losses (Core Stability Mechanism)

muBOND accounts for about 15% of the protocol's TVL, serving as the system's "first loss capital."

If the underlying asset pool experiences a short-term market value decline due to market fluctuations (interest rate increases, credit spread widening, etc.), the losses will directly reflect on the muBOND NAV without affecting AZND.

Only when the portfolio losses exceed the entire buffer layer of muBOND may AZND be impacted.

Example: If the portfolio declines by 5%, all losses are absorbed by muBOND, and AZND maintains its value of $1.

2. Insurance Fund

Serves as an additional capital buffer to cover potential losses exceeding muBOND.

Established through the long-term accumulation of protocol fees.

Uses include:

Covering redemption gaps

Providing liquidity during market stress

Stabilizing AZND NAV during extreme volatility

Tron Comments

Mu Digital's advantage lies in its introduction of high-quality dollar-denominated fixed-income assets (RWA) from the Asia-Pacific region into DeFi, providing principal protection and sustainable returns through a dual-token layered structure (AZND + muBOND), allowing ordinary crypto users to access stable, high-credit investment channels that were previously only available to institutions. A professional TradFi team manages the asset pool, complemented by a strict framework for liquidity, credit, and interest rate risks, and achieves high transparency through a public on-chain treasury and regular NAV reports, making it closer to institutional-grade yield products. However, its disadvantages include: the mechanism's reliance on TradFi custody and active management, which presents a certain degree of centralized credit risk; the performance of returns is highly correlated with the market interest rate environment of the asset pool; at the same time, the stability of AZND depends on the scale and sustainability of the muBOND buffer layer and insurance fund, which may face capacity limitations in the early stages.

Overall, Mu Digital has clear advantages in "stability, real returns + risk-layered protection + strong transparency," but it still needs to gradually strengthen its scale, risk resistance, and degree of decentralization.

1.2. Interpretation of RateX, which raised a total of $10.4 million with investments from well-known institutions such as Solana, Animoca, and GSR—making on-chain yields more transparent, efficient, and accessible

Introduction

RateX is a trading protocol for leveraged yields and spot yields operating across multiple chains, providing yield tokenization and the splitting and trading of returns and principal.

On RateX, users can engage in leveraged trading of yield tokens (YT) for various yield-bearing assets (YBA) to capture yield opportunities arising from yield fluctuations with higher capital efficiency.

In addition to leveraged yield trading, RateX also offers two integrated features: Earn Fixed Yield and Yield Liquidity Farming, to meet different users' yield and risk preference needs.

RateX Protocol Framework Analysis

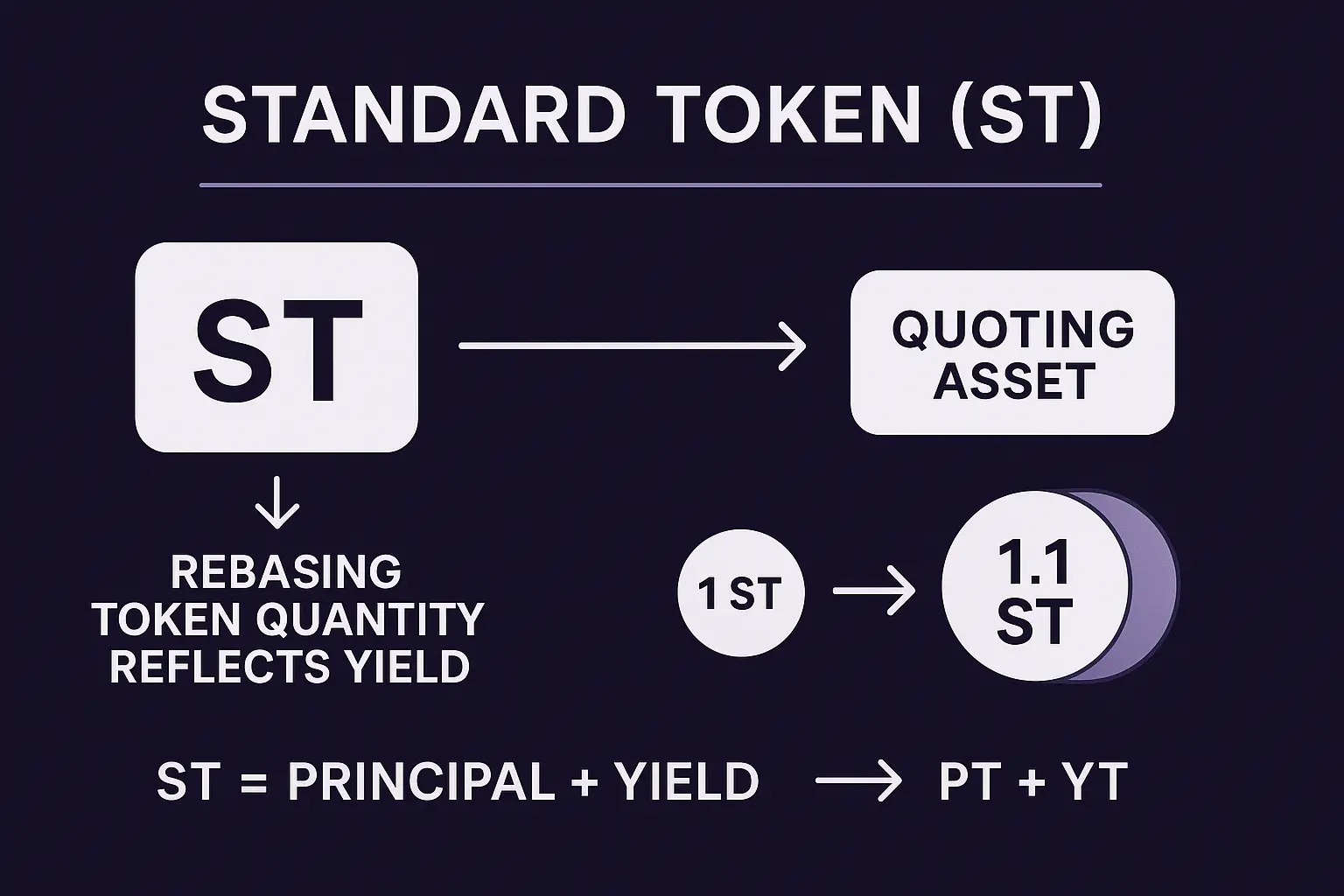

1. Standard Token (ST)

ST is the standardized yield token designed by RateX to uniformly represent the yield performance of various yield-bearing assets.

Its core mechanism:

Constant price, yield reflected in quantity (Rebase)

The price of each unit of ST is fixed equal to the priced asset (e.g., always equal to 1 SOL).

Yield does not cause the "token price to rise," but automatically increases the number of ST in the account to reflect equivalent value of yield.

Example:

1 JitoSOL → After one year, due to 10% APR, it becomes 1.1 SOL

But 1 ST-JitoSOL → The price remains 1 SOL, and the quantity becomes 1.1

→ Yield is entirely reflected through quantity.

Value composition of ST (decomposability)

The value of ST at any moment = Principal (PT) + Yield (YT)

At maturity:

ST_maturity = Principal + Yield

At the current moment:

STpresent = PTpresent + YT_present

→ This allows RateX to cleanly achieve the splitting and trading of principal/yield.

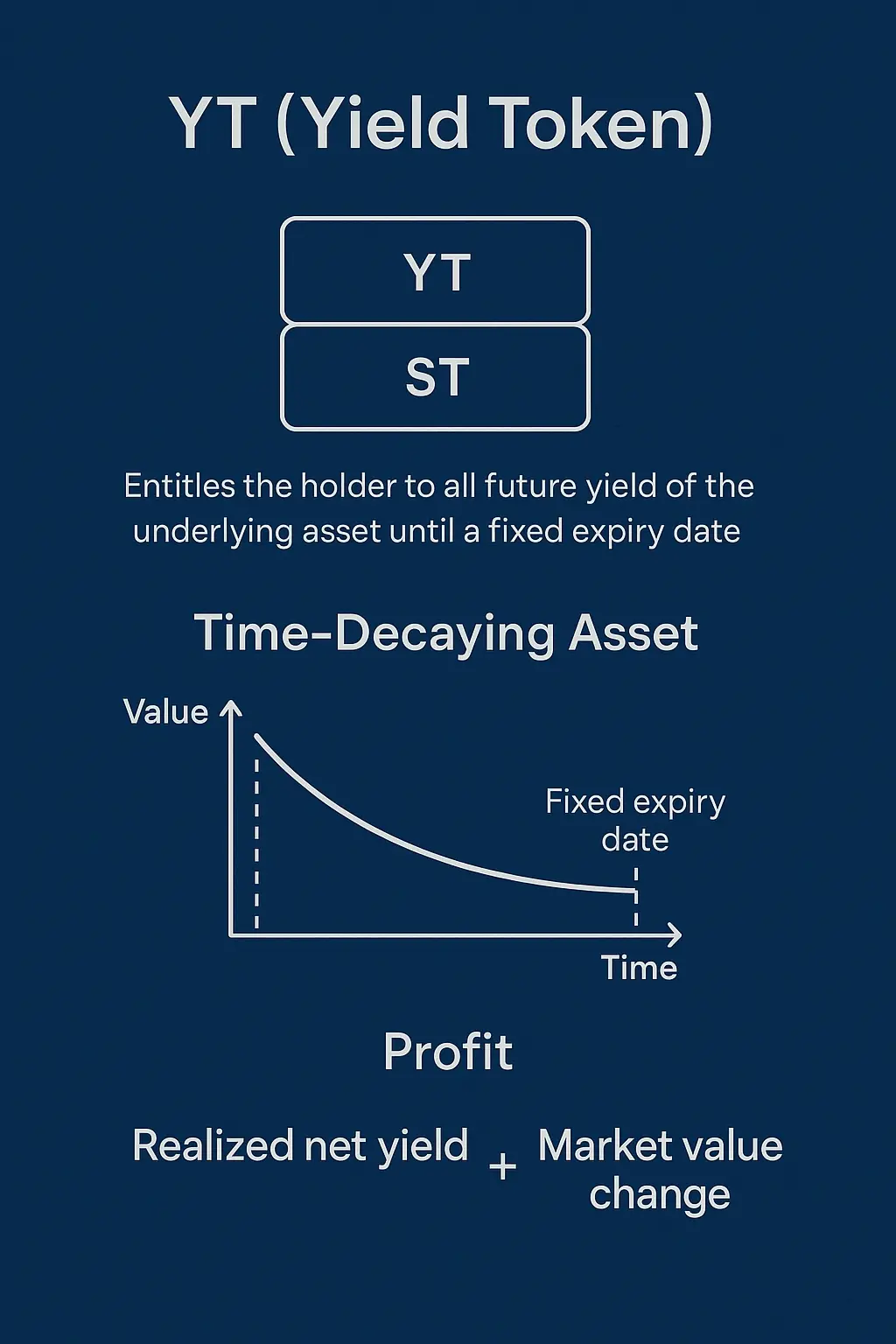

2. Yield Token (YT)

YT (Yield Token) represents the entire future yield rights generated by a yield-bearing asset (YBA) from now until a fixed maturity date.

For example: YT-mSOL-2412 = owning all mSOL staking yields from now until 2024/12/28.

Key Characteristics of YT: Time Decay

YT is an asset with diminishing value over time:

The closer it gets to maturity, the less future yield remains to be claimed

→ Therefore, the price of YT gradually approaches 0Continuous receipt of yield during the holding period → simultaneously reduces remaining future yield

Sources of Profit for YT (Two Parts)

The yield from holding YT comes from:

Realized Net Yield

Actual yield received − Value of YT diminished over time (time amortization)Market Value Change

Current YT price − Remaining unamortized value at purchase

Pricing of YT: Determined by "Implied Yield"

The price of YT is entirely determined by the implied yield because:

ST = PT + YT

Selling YT = Selling future yield of ST, leaving only PT

Holding PT to maturity ultimately allows receipt of ST

→ Therefore, the price of YT = market expectation of future yield (Implied Yield)

The price ratio of YT/ST is a single-variable function of the implied yield—implied yield is the sole determinant of YT.

3. Principal Token (PT)

PT represents the principal portion of a yield-bearing asset (YBA). Holding PT = receiving the principal value of the corresponding ST at maturity (i.e., an equivalent amount of ST).

Formation of PT

Users can:

Buy a yield-bearing asset (e.g., stETH)

Sell its future yield portion (YT)

→ What remains is PT (only retaining principal exposure)

The essence of PT valuation: Present value of ST principal discounted

PT's value = Principal of ST, discounted by the implied yield.

In other words:

The higher the implied yield → The lower the discounted price of PT (cheaper)

The longer the duration → The greater the discount → The cheaper PT

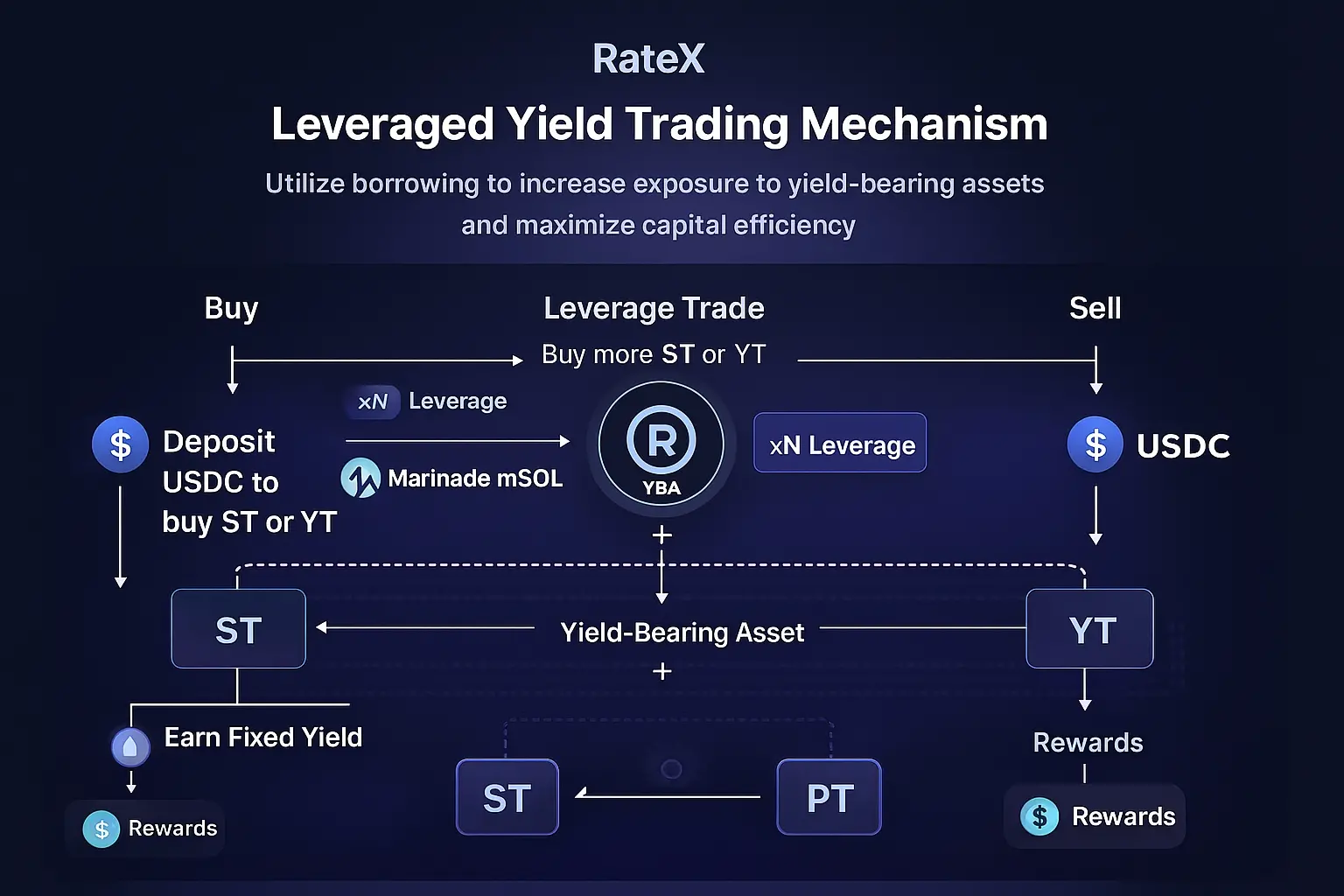

RateX Leveraged Yield Trading Mechanism Analysis

RateX allows users to engage in leveraged trading of yield tokens (YT or ST) for various yield-bearing assets (YBA)—that is, using borrowing or margin to amplify yield exposure.

Users can obtain the yield rights/principal split of the underlying asset by purchasing ST/YT, or they can borrow/lend these tokens to amplify yield or hedge yield fluctuations.

It includes two features: Earn Fixed Yield and Yield Liquidity Farming, catering to different risk preferences and yield strategies:

Fixed yield is suitable for conservative users;

Liquidity mining is suitable for active users seeking high alpha.

Why this mechanism is attractive

High capital efficiency: By leveraging and splitting tokens, a small amount of capital can amplify yield exposure.

Strong flexibility: Users can freely choose fixed yield, liquidity mining, or leveraged yield trading, adapting to different risk preferences and market cycles.

Liquidity and tradability: Yield Token / Standard Token / Principal Token are all tradable assets, and users do not need to lock up or hold long-term.

Yield and risk configurability: Through token splitting and leverage multiples, users can configure their yield/risk combinations independently.

Tron Comments

RateX's advantage lies in its ability to freely combine yield rights and principal of yield-bearing assets through the ST/PT/YT splitting model + leverage mechanism, forming a highly flexible and capital-efficient leveraged yield trading market. Users can amplify yields, lock in fixed returns, or participate in yield liquidity mining in a multi-chain environment with lower costs and higher flexibility, while also obtaining a more transparent and combinable yield structure design.

However, its disadvantages include: the complexity of yield splitting and leverage structure, which presents a higher understanding threshold for ordinary users; at the same time, leverage amplifies both yield and risk; YT's time decay and changes in implied yield require active management, or it may lead to losses; finally, the system relies on the stability of the yield-bearing assets themselves and on-chain liquidity, which may experience increased volatility or liquidity pressure in extreme market conditions.

2. Detailed Explanation of Key Projects of the Week

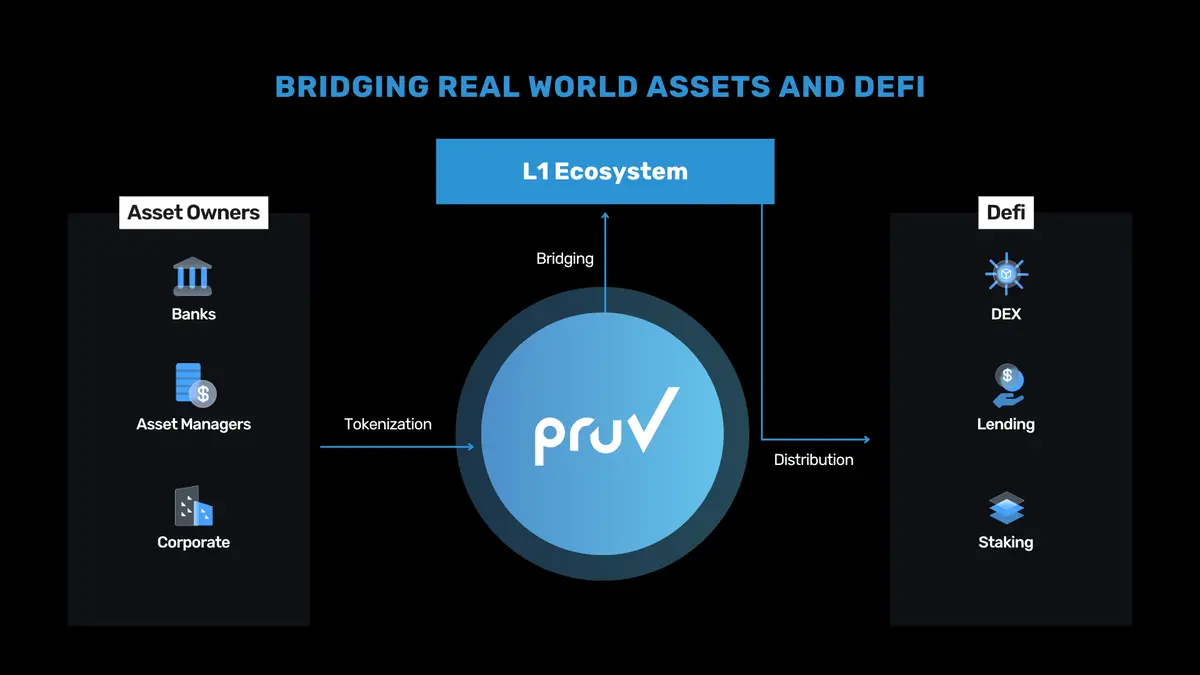

2.1. Detailed Explanation of Pruv Finance, which raised a total of $3 million, led by UOB—A Trustworthy On-Chain Standardized Entry for RWA

Introduction

Pruv Finance is an RWA infrastructure that brings real-world assets into the DeFi ecosystem. It enables users to access trustworthy, tokenizable real assets that can be freely traded and fully integrated and interoperable with DeFi protocols across multiple chains.

Architecture Overview

Pruv connects a diverse network of participants and streamlines and standardizes the complete lifecycle of real-world assets—from asset acquisition, tokenization, distribution to DeFi integration.

Pruv selects high-quality assets from trustworthy partners in the global market, ensuring that all assets meet strict compliance and due diligence standards. Only verified assets that are regulatory-ready will enter the ecosystem.

After passing the audit, assets will be tokenized on-chain, with smart contracts managing ownership, yield distribution, and regulatory rules, thus providing security and trustworthiness. The tokenized assets will first be distributed to qualified partners, including multiple L1/L2 foundations (such as Avalanche, Polygon, Stellar). Subsequently, these RWAs can be bridged across networks such as Polygon, Avalanche, Sei, Manta, and Stellar, allowing users to access and use them in any ecosystem.

All DeFi users can trade, integrate, and earn yields from these assets on-chain, unlocking real returns and combinable financial opportunities throughout the ecosystem. Meanwhile, Pruv continuously monitors asset performance, compliance, and security, enabling users to participate in investments within a stable and trustworthy environment.

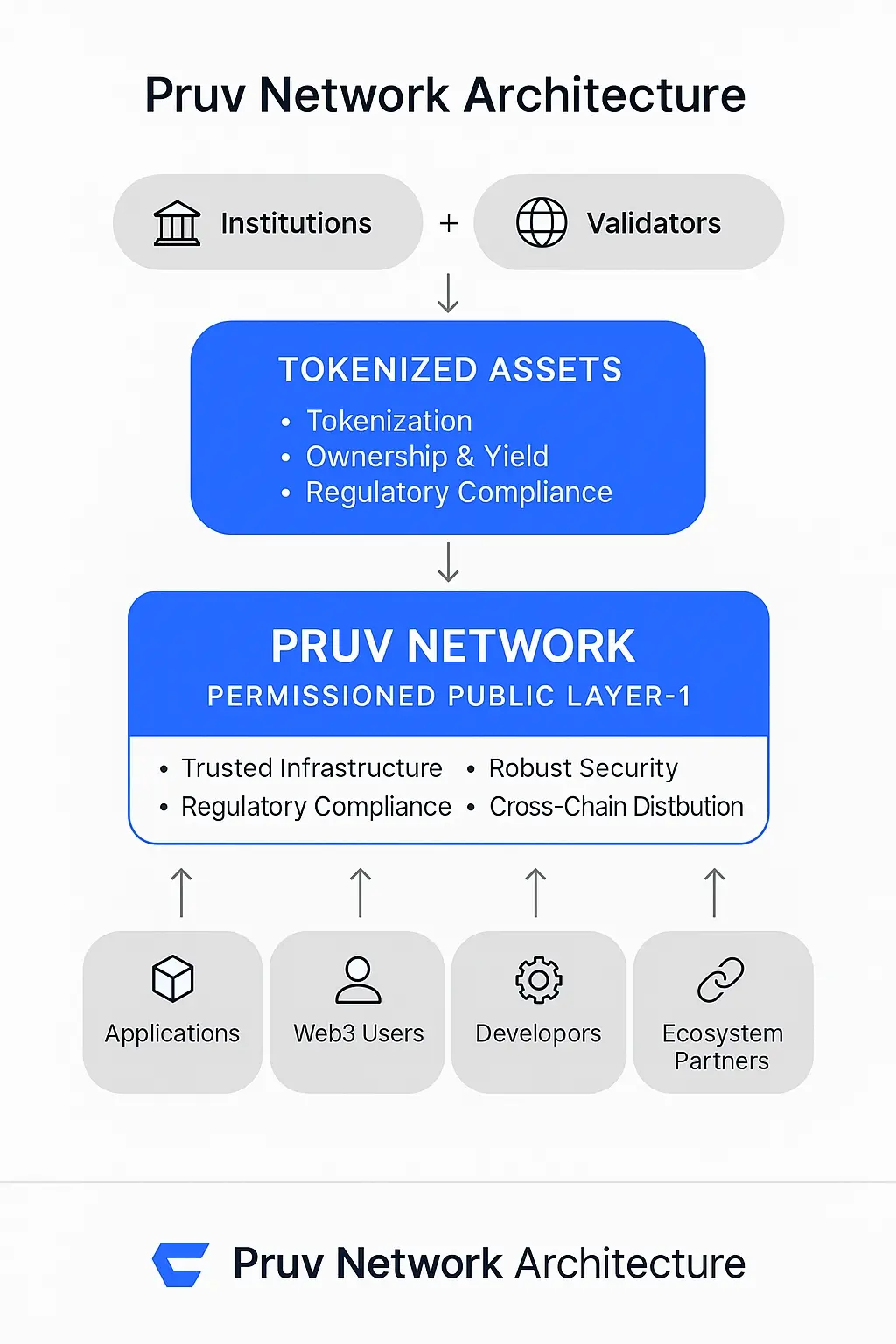

Pruv Network Analysis

Pruv Network is a financial-grade Layer-1 blockchain specifically designed for the tokenization of real-world assets, aiming to securely and compliantly bring traditional financial assets into Web3. The network only allows globally licensed financial institutions to serve as validation nodes, ensuring the security and credibility of asset issuance, management, and settlement.

Bilateral Infrastructure for TradFi and DeFi

Current public chains lack regulatory capabilities and are unsuitable for high-value financial assets; private chains, while secure, lack interoperability and liquidity.

Pruv Network, as a permissioned public blockchain, possesses transparency, regulatory compliance, and cross-chain liquidity, perfectly fitting the needs of financial institutions.

It provides a reliable RWA issuance and integration platform for:

Traditional financial participants (banks, asset management, bond-issuing institutions)

Web3 communities (DAOs, L1/L2 foundations, DeFi protocols)

Core Advantages

1. Trusted Infrastructure

Validation nodes consist of licensed financial institutions (such as licensed banks and investment firms in Asia), ensuring bank-level governance and security.

2. Strong Compliance

Built-in KYC/AML, audit trails, privacy protection, and compliance modules meet global regulatory requirements.

3. High Performance and Composability

Offers low-cost, high-throughput, cross-chain interoperability, supporting real-time settlement and asset cross-chain flow for financial-grade applications.

4. Financial Institution Friendly

Addresses the regulatory risks of public chains and the liquidity dilemmas of private chains, becoming an ideal foundational layer for banks and institutions to enter the blockchain space.

Multi-Layer Security Architecture

Pruv Network employs a bank-grade multi-layer security system, including:

Secure PoS consensus

End-to-end encryption

Multi-signature wallets

Real-time threat monitoring

Fully audited smart contracts

Regular penetration testing—ensuring the security of asset tokenization and large-scale financial applications.

Comprehensive Regulatory Compliance Modules

The network includes:

KYC/AML identity management

CTF prevention mechanisms

Smart compliance modules (automatically executing compliance rules)

Traceable audit logs

Compliance with GDPR and other privacy protection requirements

Enabling it to meet the demands of global financial regulatory systems.

Tron Comments

Pruv's advantage lies in its role as a permissioned public blockchain specifically designed for real-world assets (RWA), with globally licensed financial institutions serving as validation nodes, achieving bank-level security, strong regulatory compliance, trustworthy asset issuance, and cross-chain distribution, providing high-quality, reliable asset infrastructure for institutions and Web3 users. At the same time, it addresses the lack of regulatory capability in traditional public chains and the lack of interoperability in private chains, allowing traditional finance and DeFi to truly integrate and unleash the scaling growth potential of institutional-grade RWA.

Its disadvantages include: a highly dependent operational model on institutional nodes and regulatory frameworks, resulting in a relatively limited degree of decentralization; the asset introduction and ecosystem building require a longer institutional collaboration cycle; early liquidity and developer ecosystems may need more time to cultivate.

### Industry Data Analysis

1. Overall Market Performance

1.1. Spot BTC vs ETH Price Trends

BTC

ETH

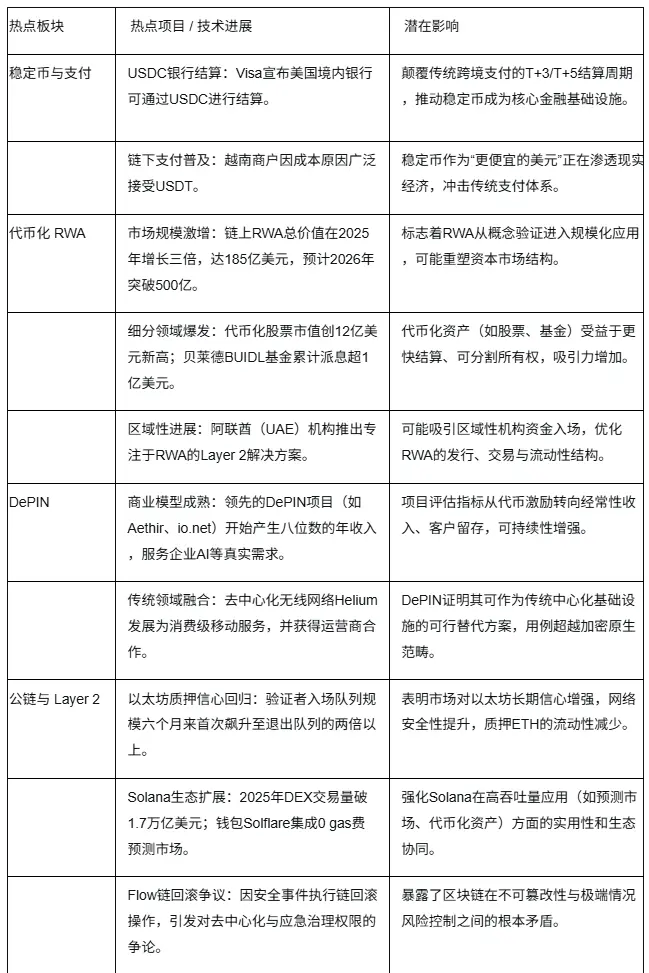

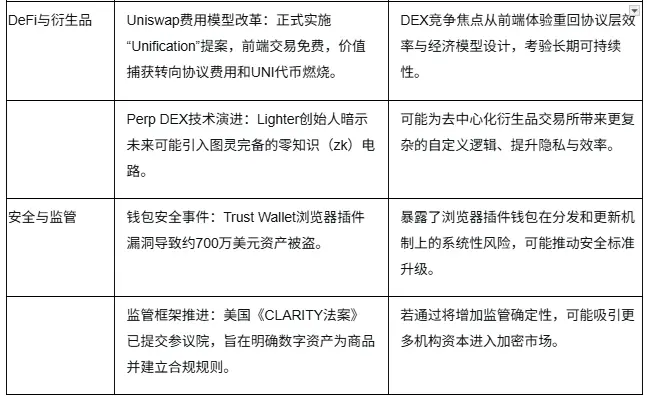

2. Hot Sector Summary

### 3. Macroeconomic Data Review and Key Data Release Points for Next Week

Important data released this week:

January 9: U.S. unemployment rate for December; U.S. seasonally adjusted non-farm payrolls for December.

### 4. Regulatory Policies

United States

Regulatory Framework Shift: The Chair of the U.S. Securities and Exchange Commission (SEC) announced plans to unveil a "regulatory sandbox" framework for digital asset companies in January 2026. This framework aims to provide regulatory flexibility for crypto projects, allowing them to test new products under supervision without immediately meeting full securities registration requirements.

Legislative Process Pending: The "Digital Asset Market Clarity Act" (CLARITY Act), which aims to clarify the commodity status of digital assets and delineate the regulatory responsibilities of the SEC and the Commodity Futures Trading Commission (CFTC), is still awaiting Senate review, and its passage in January 2026 remains uncertain.

European Union

New Tax Transparency Regulations Effective: Starting January 1, 2026, the OECD-led "Crypto-Asset Reporting Framework" (CARF) will take effect in 48 jurisdictions, including EU member states. This framework requires crypto service platforms to collect and report users' tax residency, transaction information, and other data to facilitate automatic cross-border tax information exchange.

Comprehensive Regulation Implementation Underway: The EU's "Markets in Crypto-Assets Regulation" (MiCA) is in the process of full implementation. For example, Spain has required all crypto service providers to obtain MiCA licenses by July 1, 2026.

United Kingdom

Simultaneous Implementation of New Tax Regulations: Similar to the U.S. and EU, the UK will also implement the OECD's "Crypto-Asset Reporting Framework" (CARF) starting January 1, 2026, enhancing the collection and cross-border exchange of tax information related to crypto asset transactions.

Building an Independent Regulatory Framework: Following Brexit, the UK is working to establish an independent crypto regulatory framework. The Financial Conduct Authority (FCA) plans to complete relevant regulations by the end of 2026, with the core goal of protecting consumers and maintaining market integrity.

Other Regions

- Uzbekistan: Reports indicate that the country plans to promote stablecoins as an official payment method within a new regulatory sandbox starting January 1, 2026, which will also support the trading of tokenized securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。