In the context of relatively loose expectations in both China and the United States, suppressing the downward volatility of assets, and amidst extreme panic where funds and sentiment have not fully recovered, ETH still finds itself in a favorable "strike zone" for buying.

Author: Trend Research

Since the market crash on October 11, the entire cryptocurrency market has been lackluster, with market makers and investors suffering heavy losses, and the recovery of funds and sentiment will take time.

However, the cryptocurrency market is not short of new volatility and opportunities, and we remain optimistic about the future market.

This is because the trend of mainstream cryptocurrency assets integrating with traditional finance into a new business model has not changed; rather, it has rapidly accumulated a moat during the market downturn.

1. Strengthening Wall Street Consensus

On December 3, U.S. SEC Chairman Paul Atkins stated in an exclusive interview with FOX at the New York Stock Exchange: "In the coming years, the entire U.S. financial market may migrate on-chain."

Atkins stated:

(1) The core advantage of tokenization is that if assets exist on the blockchain, the ownership structure and asset attributes will be highly transparent. Currently, listed companies often do not know who their shareholders are, where they are located, or where their shares are.

(2) Tokenization is also expected to achieve "T+0" settlement, replacing the current "T+1" trading settlement cycle. In principle, the on-chain delivery versus payment (DVP) / receipt versus payment (RVP) mechanism can reduce market risk and enhance transparency, while the time lag between clearing, settlement, and fund delivery is one of the sources of systemic risk.

(3) He believes that tokenization is an inevitable trend in financial services, and mainstream banks and brokerages are already moving towards tokenization. The world may not even need 10 years… perhaps it will become a reality in just a few years. We are actively embracing new technologies to ensure that the U.S. maintains a leading position in areas such as cryptocurrency.

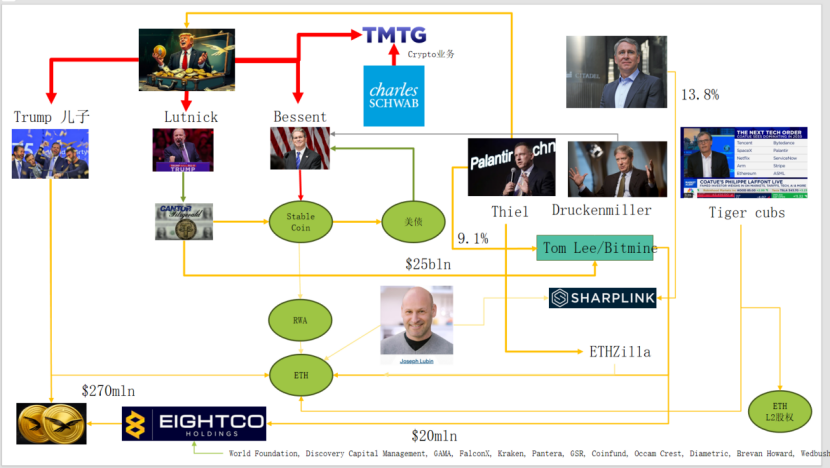

In fact, Wall Street and Washington have already built a deep capital network into cryptocurrency, forming a new narrative chain: U.S. political and economic elites → U.S. Treasuries → Stablecoins / Crypto Treasury Companies → Ethereum + RWA + L2

From this diagram, we can see the complex connections between the Trump family, traditional bond market makers, the Treasury, technology companies, and crypto companies, with the green oval connections forming the main framework:

(1) Stable Coin (USDT, USDC, WLD-backed dollar assets, etc.)

The main reserve assets are short-term U.S. Treasuries + bank deposits, held through brokers like Cantor.

(2) U.S. Treasuries

Managed and issued by Treasury / Bessent

Used by Palantir, Druckenmiller, Tiger Cubs, etc., as low-risk interest rate bases

These are also the yield assets pursued by stablecoins / treasury companies.

(3) RWA

From U.S. Treasuries, mortgages, accounts receivable to housing finance

Tokenization is completed through Ethereum L1 / L2 protocols.

(4) ETH & ETH L2 Equity

Ethereum is the main chain that supports RWA, stablecoins, DeFi, and AI-DeFi

L2 equity / tokens represent claims on future transaction volumes and fee cash flows.

This chain expresses:

Dollar credit → U.S. Treasuries → Stablecoin reserves → Various crypto treasuries / RWA protocols → Ultimately settled in ETH / L2.

From the TVL of RWA, compared to other public chains during the October 11 decline, ETH is the only public chain that quickly repaired its decline and rose, currently with a TVL of 12.4 billion, accounting for 64.5% of the total cryptocurrency market.

2. Ethereum's Exploration of Value Capture

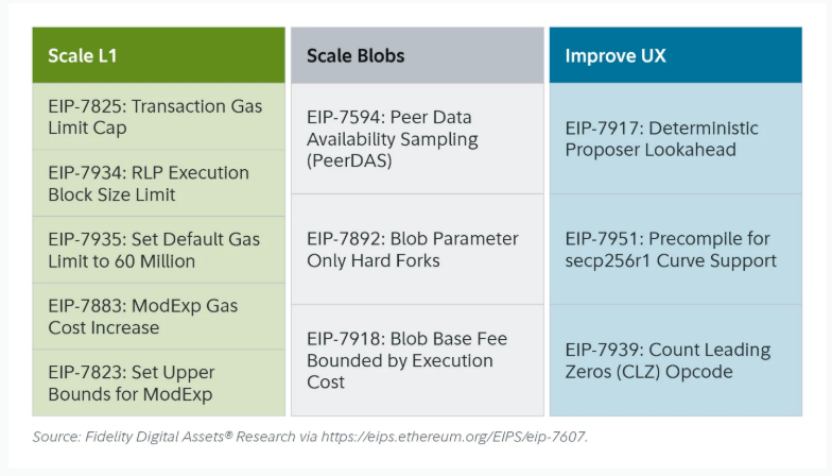

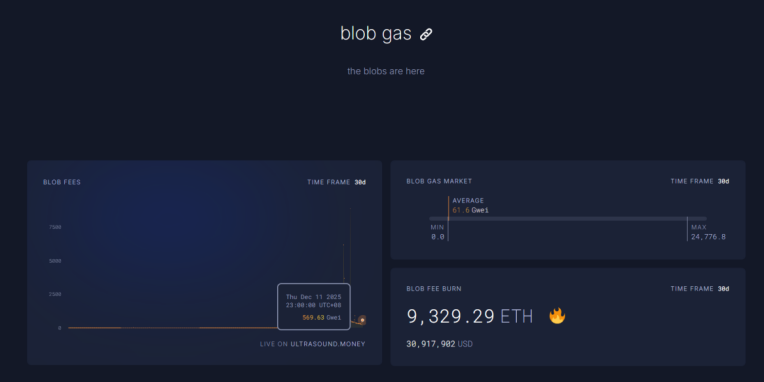

Recently, the Ethereum Fusaka upgrade did not create much of a stir in the market, but from the perspective of network structure and economic model evolution, it is a "milestone event." Fusaka is not just about scaling through EIPs like PeerDAS, but it attempts to address the insufficient value capture of the L1 mainnet caused by the development of L2.

Through EIP-7918, ETH introduces a "dynamic floor price" for blob base fees, binding its lower limit to the L1 execution layer base fee, requiring blobs to pay DA fees at a unit price of at least approximately 1/16 of the L1 base fee; this means Rollups can no longer occupy blob bandwidth at nearly zero cost for an extended period, and the corresponding fees will flow back to ETH holders in the form of burns.

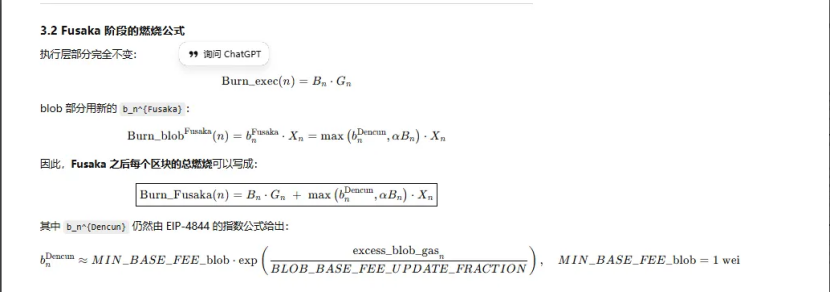

There have been three upgrades related to "burning" in Ethereum:

(1) London (one-dimensional): only burns the execution layer, ETH begins to generate structural burns due to L1 usage.

(2) Dencun (two-dimensional + independent blob market): burns execution layer + blob, L2 data written to blobs will also burn ETH, but during low demand, the blob portion is nearly zero.

(3) Fusaka (two-dimensional + blob bound to L1): to use L2 (blob), one must pay at least a fixed proportion of the L1 base fee, which will be burned, making L2 activities more stably mapped to ETH burns.

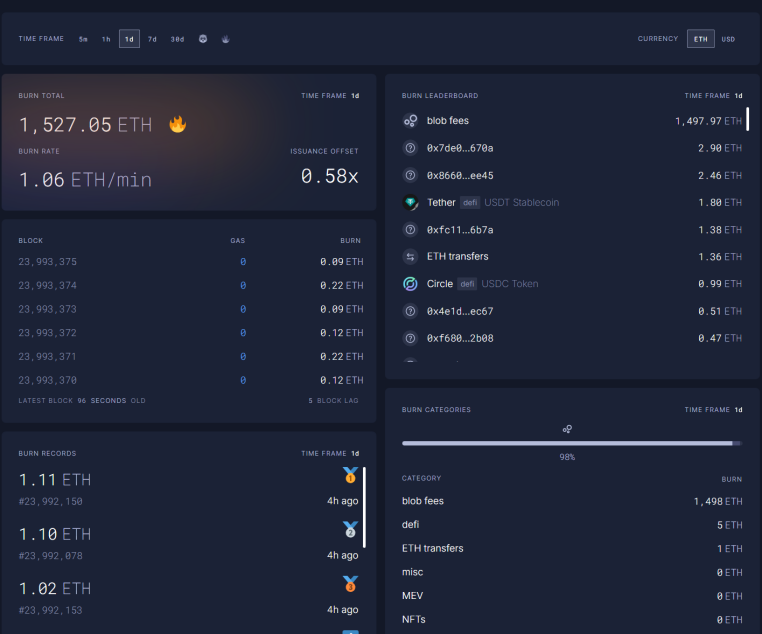

Currently, blob fees reached 569.63 billion times the fees before the Fusaka upgrade at 23:00 on December 11, burning 1,527 ETH in one day. Blob fees have become the highest contributing portion to burns, reaching as high as 98%. As ETH L2 becomes more active, this upgrade is expected to bring ETH back to deflation.

3. Strengthening Ethereum's Technical Position

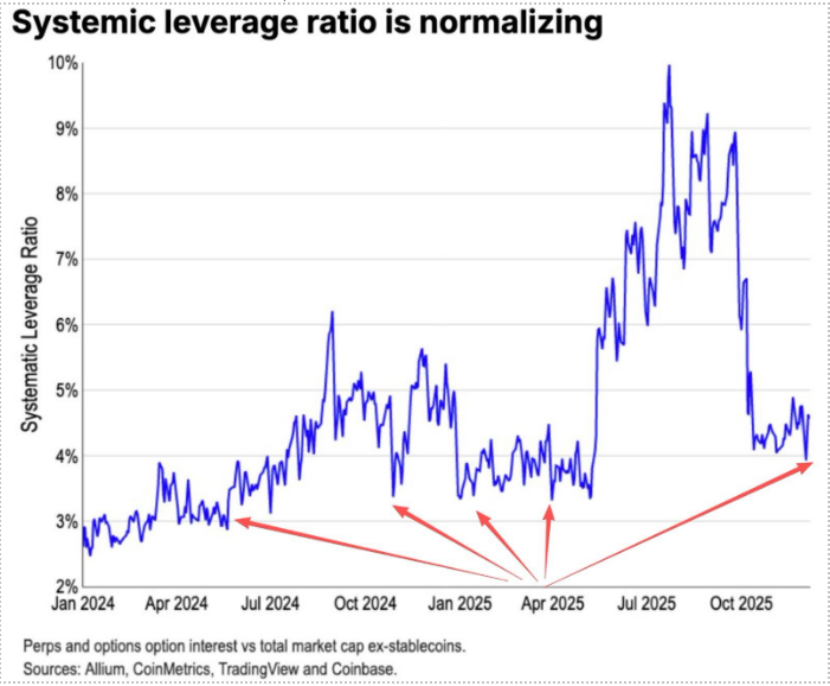

During the October 11 decline, ETH's futures leverage was fully cleared, ultimately leading to a liquidation of leveraged positions in the spot market, while many who lacked faith in ETH caused many ancient OGs to reduce their positions and flee. According to Coinbase data, speculative leverage in the crypto space has dropped to historically low levels of 4%.

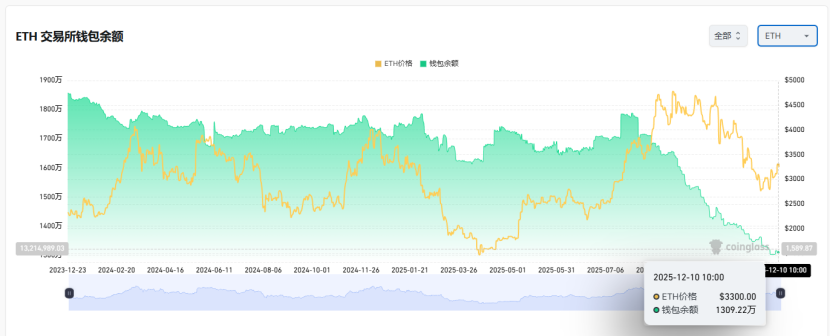

In the past, a significant portion of ETH's shorts came from traditional Long BTC/Short ETH pair trading, especially as this pair generally performed very well in previous bear markets, but this time an unexpected situation occurred. The ETH/BTC ratio has maintained a sideways resistance since November.

ETH now has an exchange inventory of 13 million coins, about 10% of the total supply, at a historical low. As the Long BTC / Short ETH pair has become ineffective since November, there may gradually be a "short squeeze" opportunity in the market during this extreme panic.

As we approach 2025-2026, both China and the U.S. have released friendly signals regarding future monetary and fiscal policies:

The U.S. will actively pursue tax cuts, interest rate reductions, and relaxed crypto regulations, while China will implement moderate easing and financial stability measures (suppressing volatility).

In the context of relatively loose expectations in both China and the United States, suppressing the downward volatility of assets, and amidst extreme panic where funds and sentiment have not fully recovered, ETH still finds itself in a favorable "strike zone" for buying.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。