Author: Frank, PANews

On December 1, U.S. time, the Federal Reserve officially announced the end of its quantitative tightening (QT) policy. On the same day, the cryptocurrency market experienced a collective rebound, with BTC rising about 8%, returning to above $93,000, while ETH surged nearly 10%, reclaiming the $3,000 mark. Other altcoins also saw a wave of exuberant increases, with SUI up 20% and SOL up 13%.

In an instant, the market shifted from silence to celebration, and with the end of QT, the market is anticipating a new wave of liquidity.

However, there are differing opinions; some believe that this sudden surge is merely a flash in the pan during a bear market, rather than the beginning of a new trend. So, historically, does the end of QT really bring new momentum to the market? PANews attempts to review the historical changes in the cryptocurrency market following the end of QT in a methodical manner.

From the End of QT in 2019 to the Darkest Moment

The last end of QT occurred on August 1, 2019, over six years ago. Let’s turn back the clock to that time.

In the summer of 2019, the cryptocurrency market had just concluded a small bull market peak. After experiencing a dramatic drop at the end of 2018, BTC rose significantly, peaking at $13,970. Although still distant from the previous high of $19,000, the market believed the entire cryptocurrency industry was heading towards a new bull market and would break new highs.

On July 31, the Federal Reserve announced during the Federal Open Market Committee (FOMC) meeting that it would officially end the QT plan on August 1, 2019. At that time, Bitcoin had just undergone a significant correction of nearly 30%, falling to around $9,400. After the Fed announced the end of QT, it surged by 6% on July 31 and returned to the $12,000 mark in the following days.

However, this upward trend did not last long. On September 26, the cryptocurrency market faced another crash, with prices dropping to a low of $7,800. Although there was a brief rise in October due to favorable blockchain policies in China, the market soon fell back into a bear market of volatility and panic. It wasn't until the outbreak of the pandemic in 2020, on the eve of the Fed's quantitative easing (QE), that an unprecedented crash occurred on March 12.

During the same period, the Nasdaq index in the U.S. stock market soared from August 2019 to February 2020, continuously creating new highs, reaching a historical peak of 9,838 points in February 2020. Both the cryptocurrency market and the stock market entered a state of collapse from February to March 2020.

Thus, this is the old script of the cryptocurrency market from the end of the last QT to the beginning of the Fed's QE. In this historical cycle, Bitcoin and the cryptocurrency market seemed to have briefly benefited from the end of QT, but before QE began, they quickly returned to a downward trajectory.

Of course, every moment in history is unique.

That summer, Facebook announced the Libra project, and Bakkt launched physically delivered Bitcoin futures, which greatly invigorated the market. Meanwhile, the PlusToken Ponzi scheme collapsed in June 2019, leading to significant sell-offs that pressured the entire cryptocurrency market.

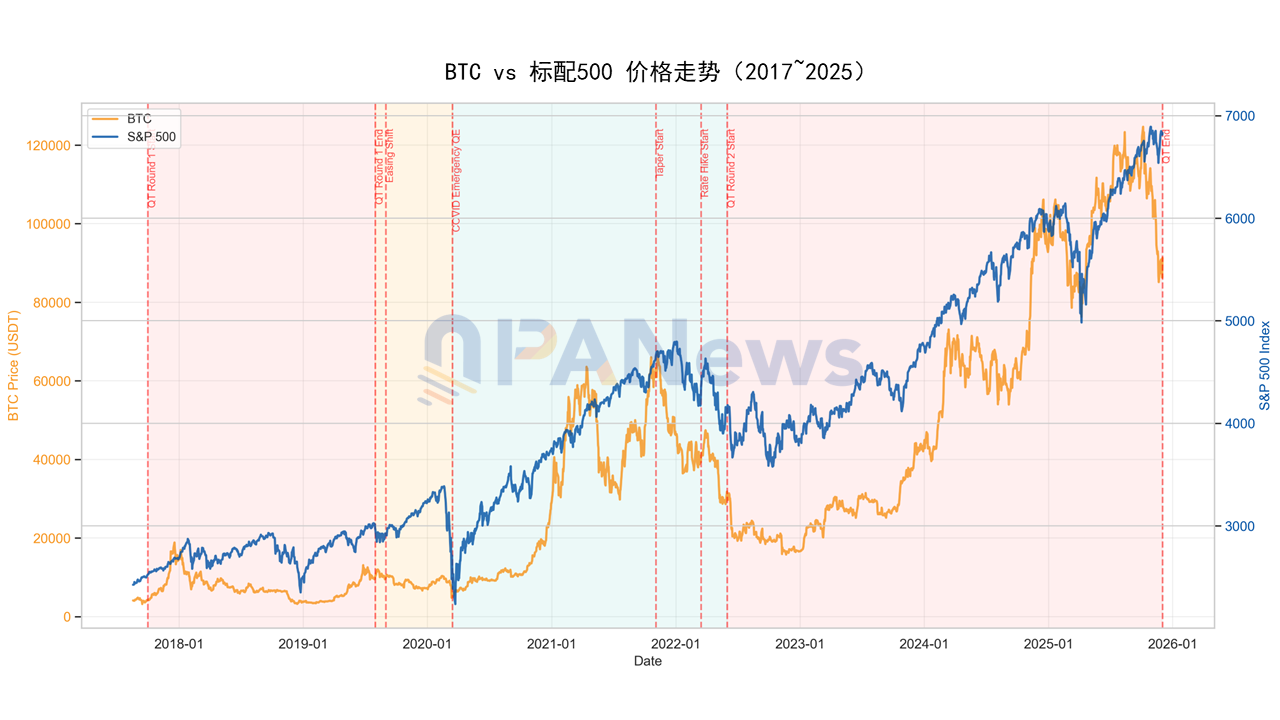

Comparison of Bitcoin's correlation with the S&P 500 from 2017 to present

Current Situation: Tenfold Growth, More Stable Trends

So how different is today from the past?

By December 2025, Bitcoin had just experienced a significant correction of over 36% from the historical high of $126,199 created in October. Although the details of the K-line and prices are vastly different from the past, the current phase seems to mirror that of 2019, both undergoing a major fluctuation after a bull market. This phase can be seen as the beginning of a bear market from one perspective, while from another, it can be viewed as a halftime break in a bull market.

From a fundamental perspective, today’s cryptocurrency market is recognized by traditional financial markets. People are no longer excited by the entry or layout of a major company; it has become commonplace for publicly listed companies to adopt cryptocurrency treasury strategies and cryptocurrency ETFs. The overall market size of cryptocurrencies has increased by about tenfold compared to 2019. The market's main players have completely shifted from retail investors to institutional investors.

Comparison of Bitcoin's trends from 2017-2019 and 2023-2025

In terms of market trends, there is a significant difference in the process, even though the results are similar. To clearly see the historical trends at the end of QT in these two instances, PANews compared the market trends from the two years before the end of QT in 2019 with those from the two years before the end of QT in 2025. When normalizing the price starting points to 100, we can observe an interesting phenomenon: the percentage increase before the end of QT in both cycles is quite close, with 142% in 2019 and 131% now, indicating that both cycles increased by about 2.4 times.

However, the process of this trend shows a huge difference, as it is evident that in the past two years, Bitcoin's trend has become more stable, no longer experiencing the extreme volatility of the previous cycle.

Another key factor is that the current cryptocurrency market has become more strongly correlated with the U.S. stock market, with the correlation currently maintaining between 0.4 and 0.6, indicating a strong correlation. In contrast, the correlation between BTC and the S&P 500 index in 2019 ranged from -0.4 to 0.2 (indicating little to no correlation, or even negative correlation).

While the overall direction is to rise and fall together, in the context of existing capital, funds have prioritized more certain U.S. tech stocks over cryptocurrencies. For example, on December 2, when the Fed announced the end of QT, the Nasdaq had already begun a recovery trend despite having experienced a correction. It had returned to levels close to the previous high of 24,019 points. In contrast, Bitcoin's trend was much weaker, not only experiencing a larger drop during the correction but also showing a weaker rebound before the announcement. Of course, this is partly due to the high volatility of cryptocurrencies as risk assets, but overall, the cryptocurrency market seems more like a tech stock in the U.S. stock market.

QT is Not the Starting Gun, QE is the True Redemption

Bitcoin follows the U.S. stock market, while other altcoins follow Bitcoin. This makes the future trends of the cryptocurrency market increasingly dependent on macro market changes. Since it is a "follower," merely relying on the end of QT as a "stop-loss" policy may not be sufficient to support an independent market. What the market truly craves is real "blood transfusion"—quantitative easing (QE).

From the results of the market trends after the last QT, although the cryptocurrency market briefly rebounded due to QT expectations, it generally experienced a process of fluctuating decline until after March 15, 2020, when the Fed announced "unlimited QE," leading to a rise alongside the U.S. stock market.

At the current time point, although QT has ended, the Fed has not yet officially entered the quantitative easing phase. However, mainstream financial institutions generally expect a moderate easing of U.S. economic and Fed policies, believing that the Fed will continue to cut interest rates and may even restart quantitative easing.

Several institutions, including Goldman Sachs and Bank of America, expect the Fed to continue cutting rates in 2026, with some predicting two rate cuts in that year. Deutsche Bank and others predict that the Fed may restart QE as early as the first quarter of 2026. However, there is also a risk that these expectations have been priced in early; Goldman Sachs noted in its November 2026 global market outlook that "the baseline outlook for the global market in 2026 is moderate, with Fed easing, improved fiscal policy, and reduced tariff shocks supporting growth, but the market has already priced in these expectations, and caution is needed regarding risks that may fall short of expectations."

Additionally, while there are expectations for quantitative easing, cryptocurrencies are no longer the hottest topic in the market; the rise of the AI market is squeezing the attention and expectations for the cryptocurrency market. Many Bitcoin mining companies have gradually shifted towards AI computing networks in this context. In November, among the top ten cryptocurrency mining companies ranked by computing power, seven reported that their AI or high-performance computing projects had generated revenue, while the remaining three planned to follow suit.

In summary, whether from historical experience or current realities, the end of QT does not seem to signal the start of a new bull market. The true "blood transfusion" appears to be more crucially linked to the beginning of quantitative easing.

Moreover, even if quantitative easing begins, the size of the cryptocurrency market is already ten times larger than in 2019, and its trends are stabilizing. Whether it can still initiate past growth rates of tenfold remains a question mark. We must also acknowledge that blockchain or cryptocurrencies are no longer the most dazzling protagonists on the market stage; AI is currently the star.

All these changes cast a heavy fog over the future of the cryptocurrency market. Excessive optimism and pessimism are both untimely.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。