Author: Jiawei, IOSG

In the late 1990s, investment in the internet focused heavily on infrastructure. At that time, the capital market almost entirely bet on fiber optic networks, ISP providers, CDNs, and manufacturers of servers and routers. Cisco's stock price soared, and by 2000, its market value exceeded $500 billion, making it one of the most valuable companies in the world; fiber optic equipment manufacturers like Nortel and Lucent also became hot commodities, attracting hundreds of billions in financing.

During this boom, the United States added millions of kilometers of fiber optic cables between 1996 and 2001, building capacity far beyond the actual demand at the time. The result was a severe oversupply around the year 2000—cross-country bandwidth prices dropped by more than 90% in just a few years, and the marginal cost of connecting to the internet approached zero.

Although this wave of infrastructure allowed later companies like Google and Facebook to thrive on cheap, ubiquitous networks, it also brought growing pains for the frenzied investors of the time: the valuation bubble in infrastructure quickly burst, and the market value of star companies like Cisco shrank by more than 70% in just a few years.

Doesn't this sound similar to the Crypto scene over the past two years?

1. The Era of Infrastructure May Be Coming to an End?

Block Space Transitioning from Scarcity to Abundance

The expansion of block space and the exploration of the blockchain's "impossible triangle" largely dominated the early development of the crypto industry for several years, making it a suitable topic to discuss as a hallmark element.

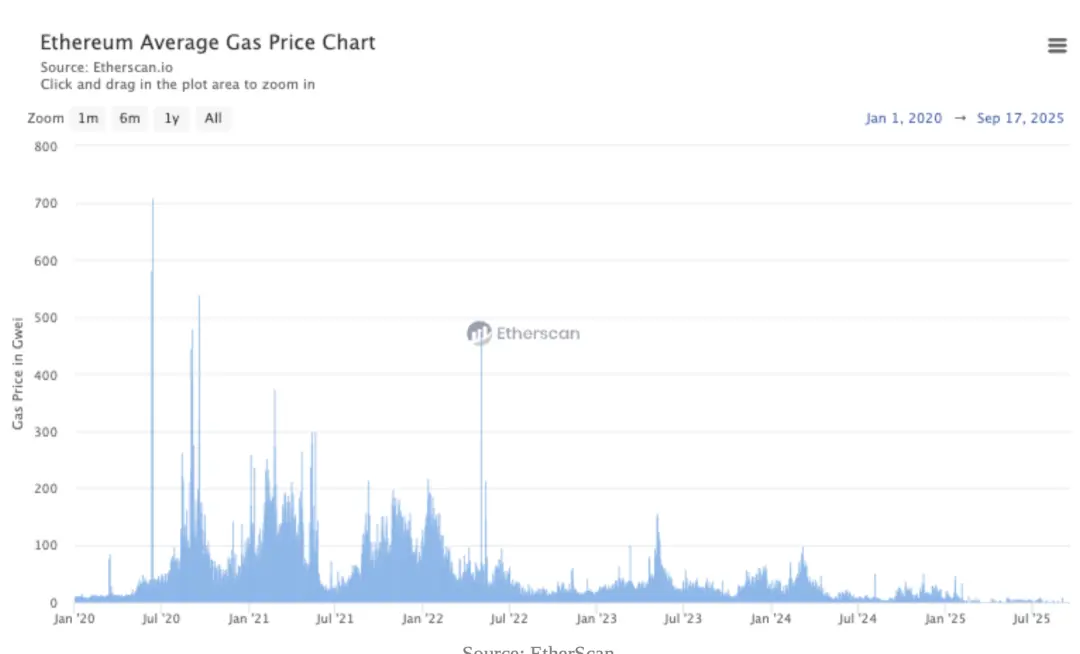

▲Source: EtherScan

In the early stages, public chains had extremely limited throughput, and block space was a scarce resource. For example, during DeFi Summer, with various on-chain activities overlapping, the cost of a single DEX interaction often ranged from $20 to $50, and during extreme congestion, transaction costs could reach hundreds of dollars. By the time of the NFT boom, the demand and calls for expansion peaked.

Ethereum's composability is a significant advantage, but it also increased the complexity and gas consumption of individual calls, with limited block capacity being prioritized by high-value transactions. As investors, we often discuss L1's transaction fees and burning mechanisms, using these as anchors for L1 valuation. During this period, the market assigned high pricing to infrastructure, and the so-called "fat protocols thin applications" narrative gained acceptance, leading to a wave of construction of expansion solutions, even to the point of bubble.

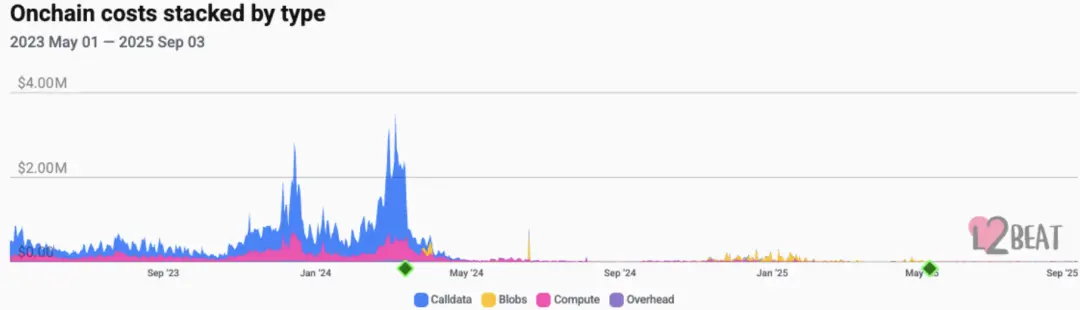

▲Source: L2Beats

In terms of results, Ethereum's key upgrades (such as EIP-4844) migrated L2's data availability from expensive calldata to lower-cost blobs, significantly reducing the unit cost of L2. The transaction fees for mainstream L2s generally dropped to the level of a few cents. The introduction of modular and Rollup-as-a-Service solutions also significantly lowered the marginal cost of block space. Various Alt-L1s supporting different virtual machines also emerged. The result is that block space transitioned from a single scarce asset to a highly interchangeable commodity.

The above chart shows the changes in on-chain costs for various L2s over the past few years. It can be seen that from 2023 to early 2024, calldata accounted for the main cost, with daily costs approaching $4 million. Subsequently, in mid-2024, the introduction of EIP-4844 led to blobs gradually replacing calldata as the dominant cost, resulting in a significant decrease in overall on-chain costs. Entering 2025, total expenses tended to a lower level.

As a result, more and more applications can place their core logic directly on-chain, rather than adopting the complex architecture of off-chain processing followed by on-chain submission.

From this point on, we see value capture beginning to shift from underlying infrastructure to applications and distribution layers that can directly handle traffic, enhance conversion, and form cash flow loops.

Evolution of Revenue Streams

Building on the last paragraph of the previous section, we can intuitively verify this viewpoint in terms of revenue. During the infrastructure narrative-dominated cycle, the market's valuation of L1/L2 protocols was primarily based on their technical strength, ecosystem potential, and expected network effects, known as "protocol premium." The token value capture model was often indirect (e.g., through network staking, governance rights, and vague expectations of transaction fees).

The value capture of applications is more direct: generating verifiable on-chain revenue through transaction fees, subscription fees, service fees, etc. This revenue can be directly used for token buybacks and burns, dividends, or reinvestment for growth, forming a tight feedback loop. The revenue sources for applications have become solid—more from actual service fee income rather than token incentives or market narratives.

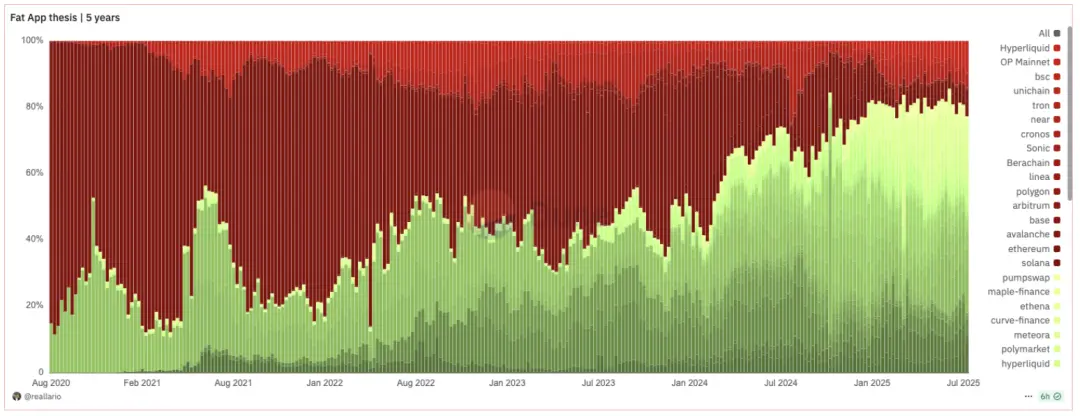

▲Source: Dune@reallario

The above chart roughly compares the revenue of protocols (in red) and applications (in green) from 2020 to the present. We can see that the value captured by applications is gradually increasing, reaching about 80% this year. The table below lists the 30-day revenue rankings of protocols as compiled by TokenTerminal, where L1/L2 only accounts for 20% among 20 projects. Notably, applications such as stablecoins, DeFi, wallets, and trading tools stand out.

▲Source: ASXN

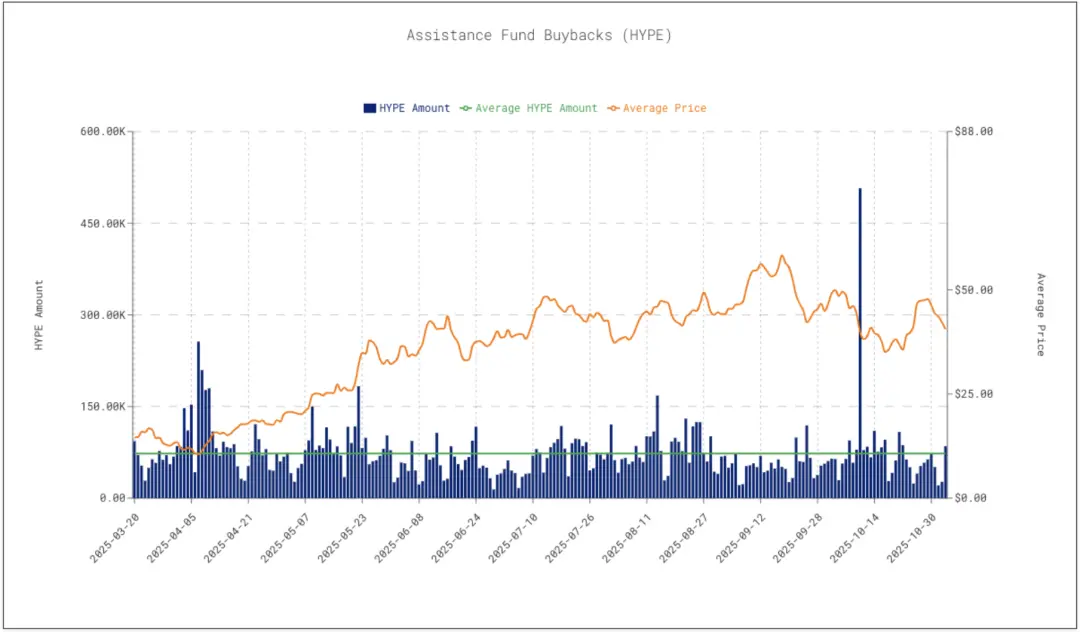

Moreover, due to the market response from buybacks, the price performance of application tokens is increasingly correlated with their revenue data.

Hyperliquid's daily buyback scale is about $4 million, providing significant support for token prices. Buybacks are considered one of the important factors driving price rebounds. This indicates that the market is beginning to directly associate protocol revenue with buyback behavior in determining token value, rather than relying solely on sentiment or narratives. I expect this trend to continue to strengthen.

2. Embracing Applications as the Mainstream of a New Cycle

The Golden Age of Asian Developers

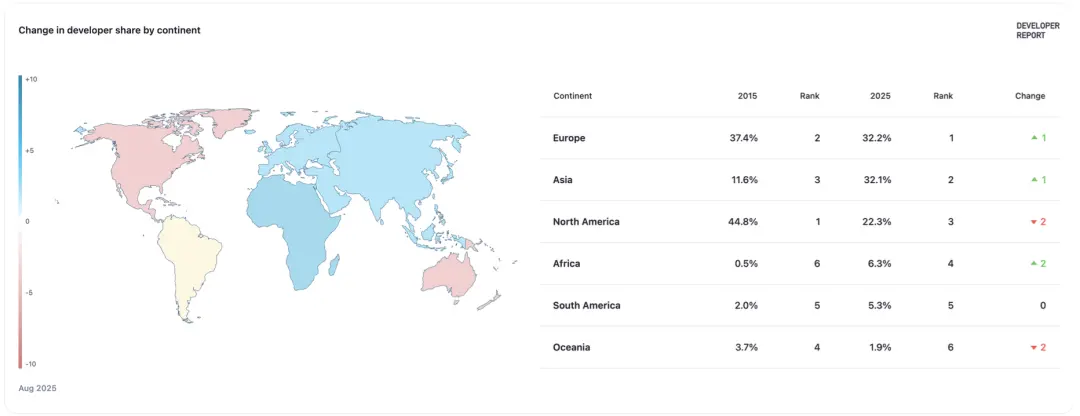

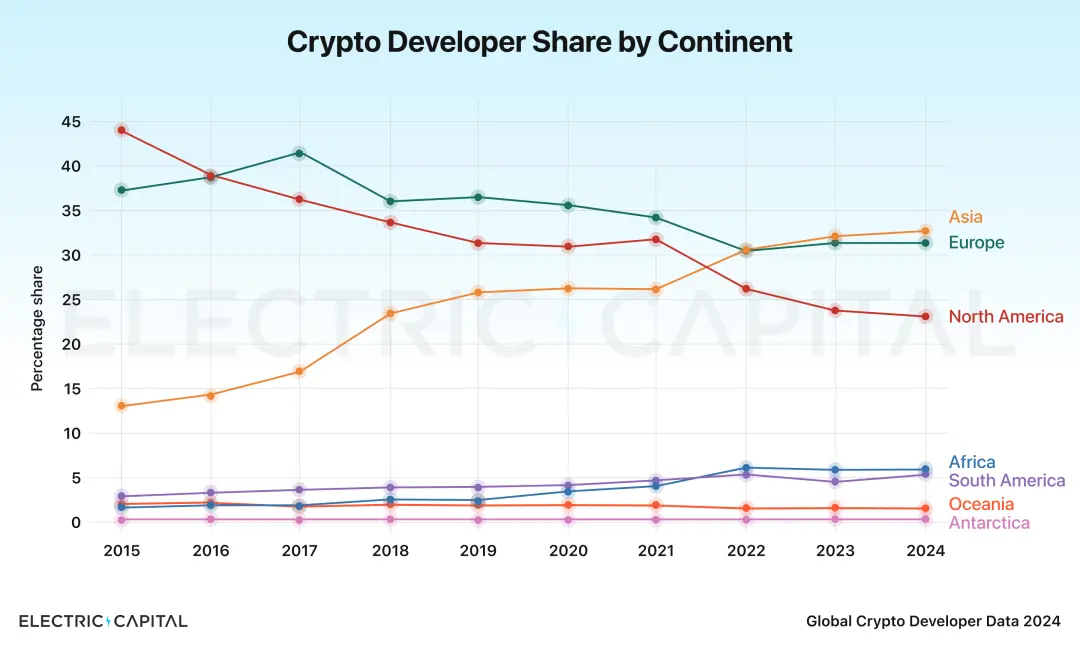

▲Source: Electric Capital

▲Source: Electric Capital

Electric Capital's 2024 Developer Report shows that the proportion of blockchain developers in Asia has reached 32% for the first time, surpassing North America to become the largest developer hub in the world.

Over the past decade, global products like TikTok, Temu, and DeepSeek have proven the outstanding capabilities of Chinese teams in engineering, product development, growth, and operations. Asian teams, especially Chinese teams, have a strong iterative rhythm, can quickly validate needs, and achieve overseas expansion through localization and growth strategies. Crypto aligns perfectly with these characteristics: it requires rapid iteration and adjustment to adapt to market trends; it must serve global users, cross-lingual communities, and multiple market regulations simultaneously.

Therefore, Asian developers, particularly Chinese teams, have a structural advantage in the crypto application cycle: they possess strong engineering capabilities and are sensitive to market speculation cycles with strong execution power.

In this context, Asian developers have a natural advantage, enabling them to deliver globally competitive crypto applications more quickly. The applications we see in this cycle, such as Rabby Wallet, gmgn.ai, and Pendle, are representative of Asian teams on the global stage.

We expect to see this shift happen quickly: the market trend will transition from being dominated by American narratives to Asian products leading the way, followed by expansion into the European and American markets. Asian teams and markets will gain more influence in the application cycle.

Primary Market Investment in the Application Cycle

Here are some insights on primary market investments:

Trading, asset issuance, and financial applications still have the best PMF and are almost the only products that can survive a bear market. Corresponding examples include perpetuals like Hyperliquid, launchpads like Pump.fun, and products like Ethena, which package capital rate arbitrage into products that can be understood and used by a broader user base.

For investments in niche tracks with significant uncertainty, consider investing in the beta of the track, thinking about which projects will benefit from the development of that track. A typical example is prediction markets—there are approximately 97 publicly available prediction market projects, with Polymarket and Kalshi being the more obvious winners, making it unlikely for long-tail projects to overtake them. Investing in tools for prediction markets, such as aggregators and chip analysis tools, is more certain and can capture the benefits of track development, turning a difficult multiple-choice question into a single-choice question.

Once products are available, the next core step is how to bring these applications to the masses. In addition to common entry points like Social Login provided by Privy, I believe that aggregated trading frontends and mobile platforms are also quite important. In the application cycle, whether it's perpetuals or prediction markets, mobile platforms will be the most natural touchpoint for users, whether for their first deposits or daily high-frequency operations, as the experience will be smoother on mobile.

The value of an aggregated frontend lies in the distribution of traffic. Distribution channels directly determine user conversion efficiency and project cash flow.

Wallets are also an important part of this logic.

I believe that wallets are no longer just simple asset management tools; they are positioned similarly to Web2 browsers. Wallets directly capture order flow, distributing it to block builders and seekers, thus monetizing traffic; at the same time, wallets serve as distribution channels, becoming direct entry points for users to access other applications through built-in cross-chain bridges, integrated DEXs, and third-party services like staking. In this sense, wallets control order flow and traffic distribution rights, serving as the primary entry point for user relationships.

For the infrastructure throughout the cycle, I believe that some public chains created out of thin air have lost their meaning of existence; however, infrastructure that provides foundational services around applications can still capture value. Here are a few specific points:

- Infrastructure that provides customized multi-chain deployment and application chain building for applications, such as VOID;

- Companies providing user onboarding services (covering login, wallets, deposits and withdrawals, etc.), such as Privy and Fun.xyz; this can also include wallets and payment layers (fiat on/off ramps, SDKs, MPC custody, etc.);

- Cross-chain bridges: As the multi-chain world becomes a reality, the influx of application traffic will urgently require secure and compliant cross-chain bridges.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。