The operating company behind the Kadena blockchain, Kadena Organization, announced its shutdown on October 21. The wording of its announcement was formal, calm, yet heartbreakingly concise.

The company expressed gratitude to the community, mentioning that the "market environment" was the reason for the shutdown, and confirmed that all business activities and blockchain maintenance would cease immediately.

In the last notification on the X platform (formerly Twitter), the team reminded users that the network's security would still be maintained by miners, and the code would remain open source, meaning that the blockchain technology layer would continue to exist.

However, beneath this technical "continuation" lies a harsher reality: Kadena's economic vitality and community foundation have vanished.

Kadena's shutdown is not an isolated failure but part of a deeper structural adjustment within the cryptocurrency industry.

In this process, those that have consistently failed to achieve "product-market fit" (PMF), have never formed a specialized positioning, and have not developed attractive supporting applications at the infrastructure level will gradually exit the market.

The Road to Despair

Kadena's starting point combined "industry background" with "grand vision."

Founded by former JPMorgan engineers Stuart Popejoy and William Martino, the project promised in 2018 to provide functionalities that Ethereum could not achieve at the time, such as high-throughput proof-of-work (PoW) smart contracts through a system called "Braided Chains."

Its proprietary programming language, Pact, emphasized "human-readable code" and "formal verification," aiming to position Kadena as a blockchain network that is "both secure and scalable."

But "innovation without user adoption is ultimately just an unfinished story."

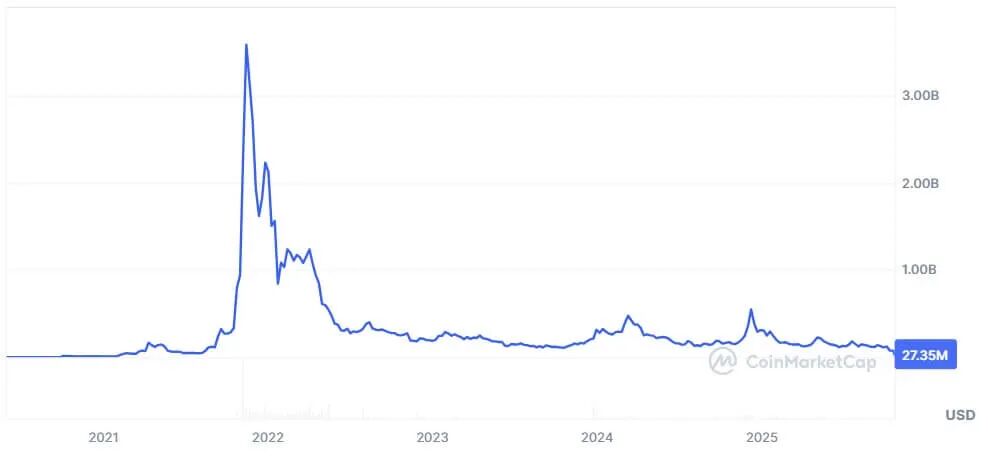

Kadena launched its mainnet in 2019, building a limited developer ecosystem. According to CoinMarketCap data, its valuation once approached $4 billion in 2021, but subsequently plummeted over 99% from that peak.

During this period, only a few mainstream decentralized applications emerged in the Kadena ecosystem, such as Babena, which peaked at a total value locked (TVL) of only $8 million.

Meanwhile, liquidity continued to flow towards ecosystems with stronger user appeal, first to Ethereum, then to Solana, and later to layer two networks like Base built directly on Ethereum.

Cryptocurrency researcher Noveleader pointed out that Kadena has failed to shake Ethereum's dominance over the virtual machine for years, and the price trend of its token KDA and the development of projects within its ecosystem have also struggled.

This phenomenon reveals the core contradiction behind Kadena's shutdown: a severe mismatch between supply and demand in the current cryptocurrency economy.

Since 2021, venture capital has poured billions into "modular first-layer networks," "second-layer networks," and "Rollups," all promising to solve issues of "scalability," "decentralization," or "transaction costs."

However, the actual user market size has seen almost no growth.

According to data from L2Beat and DeFiLlama, there are currently over 100 rolling upgrade projects and more than 200 independent chains across various ecosystems (from Ethereum forks to Cosmos-based application chains).

Yet the vast majority of them have fewer than 2,000 daily active users (DAU).

The reason is simple: they are all competing for the same group of participants, including traders, yield farmers, and liquidity providers, without offering any new value.

Startup developer Greg Tomaselli accurately summarized this situation: "A blockchain network without a clear value proposition and widespread application scenarios is ultimately doomed to fail."

The Illusion of Differentiation

Kadena's collapse exposes a truth the industry is reluctant to face: technological novelty does not equate to "product-market fit."

Almost every new blockchain claims to solve issues of "scalability," "latency," or "Gas fee efficiency."

But very few projects can articulate: when most users are deeply integrated into the Ethereum, Solana, or Binance ecosystems, who still needs a new chain?

Like many "ambitious first-layer networks," Kadena attempted to achieve differentiation through "performance metrics," providing high throughput while maintaining the security of proof-of-work.

But in the cryptocurrency industry, "performance" has long been a "homogeneous commodity."

Once a network can handle thousands of transactions per second, the core of "differentiation" shifts from "speed of operation" to "purpose of operation."

Ethereum's success did not stem from being "the fastest," but because it became the "default ecosystem" for tokens, decentralized autonomous organizations (DAOs), and decentralized finance (DeFi) protocols; Solana's rise benefited from nurturing high-frequency trading and social application scenarios.

Kadena, like projects such as EOS, has never clearly defined its core positioning beyond "better than existing chains."

This "build the chain first, then wait for the market" logic is at the heart of the infrastructure bubble, with each new chain chasing "imagined demand," while users continue to concentrate in ecosystems that offer "liquidity and community culture."

The end result is that hundreds of "technically feasible but economically irrelevant" networks maintain operations through inertia, gradually heading towards extinction.

The Era of Specialization

Moreover, the rise of second-layer networks within the Ethereum ecosystem and the consolidation of their dominant position have completely rewritten the "rules of the game" for infrastructure design.

Core participants in the Ethereum ecosystem, AminCad, pointed out that almost all "mainstream alternative first-layer networks with considerable market value" were launched before Ethereum's "Dencun Upgrade."

This upgrade significantly enhanced Ethereum's scalability and reduced transaction costs for second-layer solutions.

He believes this upgrade rendered the "so-called first-layer premium" of these alternative chains completely ineffective, "essentially relegating them to relics of the 'pre-Ethereum second-layer scalability era.'"

AminCad stated: "Now, from a 'scalability' perspective, there is no reason to choose 'launching as an alternative first-layer network' over 'a second-layer network with Ethereum as the settlement layer.' Therefore, there is no evidence that newly launched chains can gain any premium through a 'single-layer architecture.'"

He also mentioned that second-layer blockchains using Ethereum as a long-term settlement layer have operational costs about 99% lower than "independent alternative first-layer networks."

Meanwhile, the market is "rewarding specialization rather than generalization."

Successful blockchains no longer position themselves as "universal platforms," but as "digital economies focused on specific verticals."

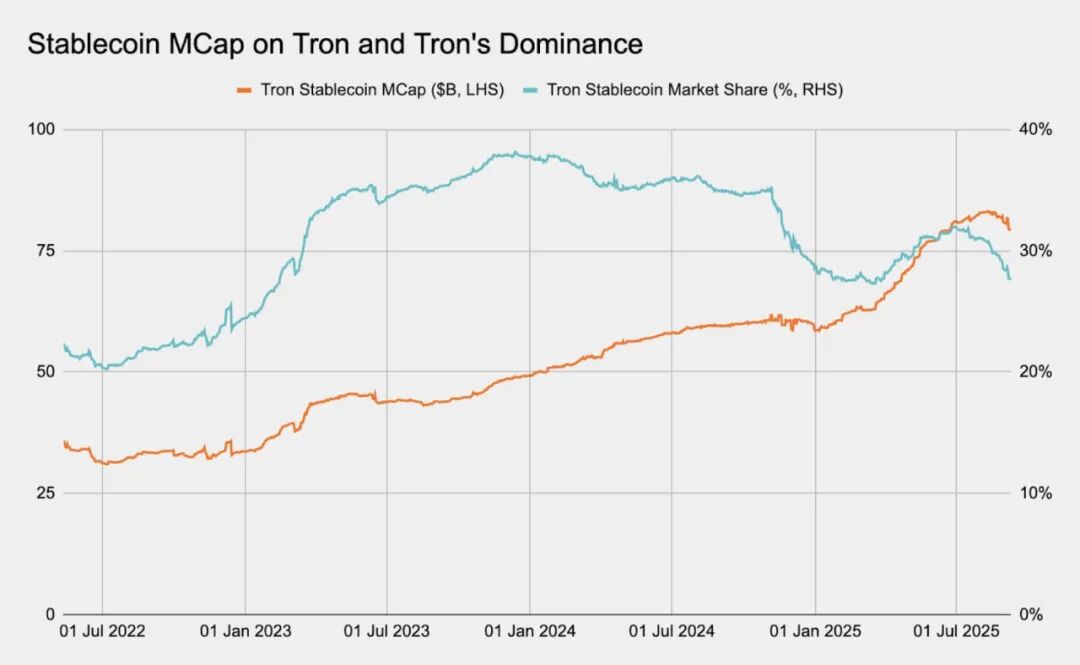

For example, first-layer networks like Plasma and TRON focus on "global stablecoin payments," providing instant transfers, extremely low fees, and complete EVM compatibility.

The competitive advantage of these chains lies not in "general throughput," but in "occupying niche markets."

Their core differentiation lies in "practicality and narrative," rather than mere "architecture," while Kadena lacks both.

This shift marks the industry entering a "more mature phase": from "technological vanity" to "economic gravity."

Thus, chains that can survive the "upcoming wave of consolidation" must possess the following traits: "sustained demand" that attracts real users, stable transaction volumes, and a value cycle that "demonstrates the value of their own block space."

The Coming Consolidation

Kadena's failure foreshadows the future direction of the "overbuilt infrastructure layer" in cryptocurrency. The market cannot support the situation where "hundreds of chains compete for the same liquidity and developer resources."

In previous cycles, "frenzied capital" masked inefficiencies in the industry, with venture funds incubating dozens of first-layer network projects, assuming each project could find a niche market.

But "liquidity is not infinite," and users always prefer "more convenient" options.

In the coming years, "consolidation" will replace "expansion": some networks will merge or interoperate through "shared sequencers" or "modular frameworks"; others will quietly fade away, leaving only traces in GitHub archives.

Only those networks with a "clear vertical positioning" (such as gaming, social, real-world assets (RWA), or institutional finance) will survive as "independent ecosystems."

This logic is similar to the early internet: there were once dozens of protocols competing for dominance, but ultimately only a few, like HTTP and DNS, became "universal standards," while the rest were quietly eliminated.

Today, the cryptocurrency industry is entering its own "elimination phase."

For developers, this means that "vanity chains" will decrease, and more "composable infrastructure" will be built on "validated ecosystems."

For investors, this serves as a reminder: "investing in first-layer networks" is no longer a "broad bet on innovation," but a "selective bet on 'network gravity,'" with the core focus on the ability to "attract and retain capital," rather than merely "computational power."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。