Through the jungle, we see order and longevity.

Written by: Daii

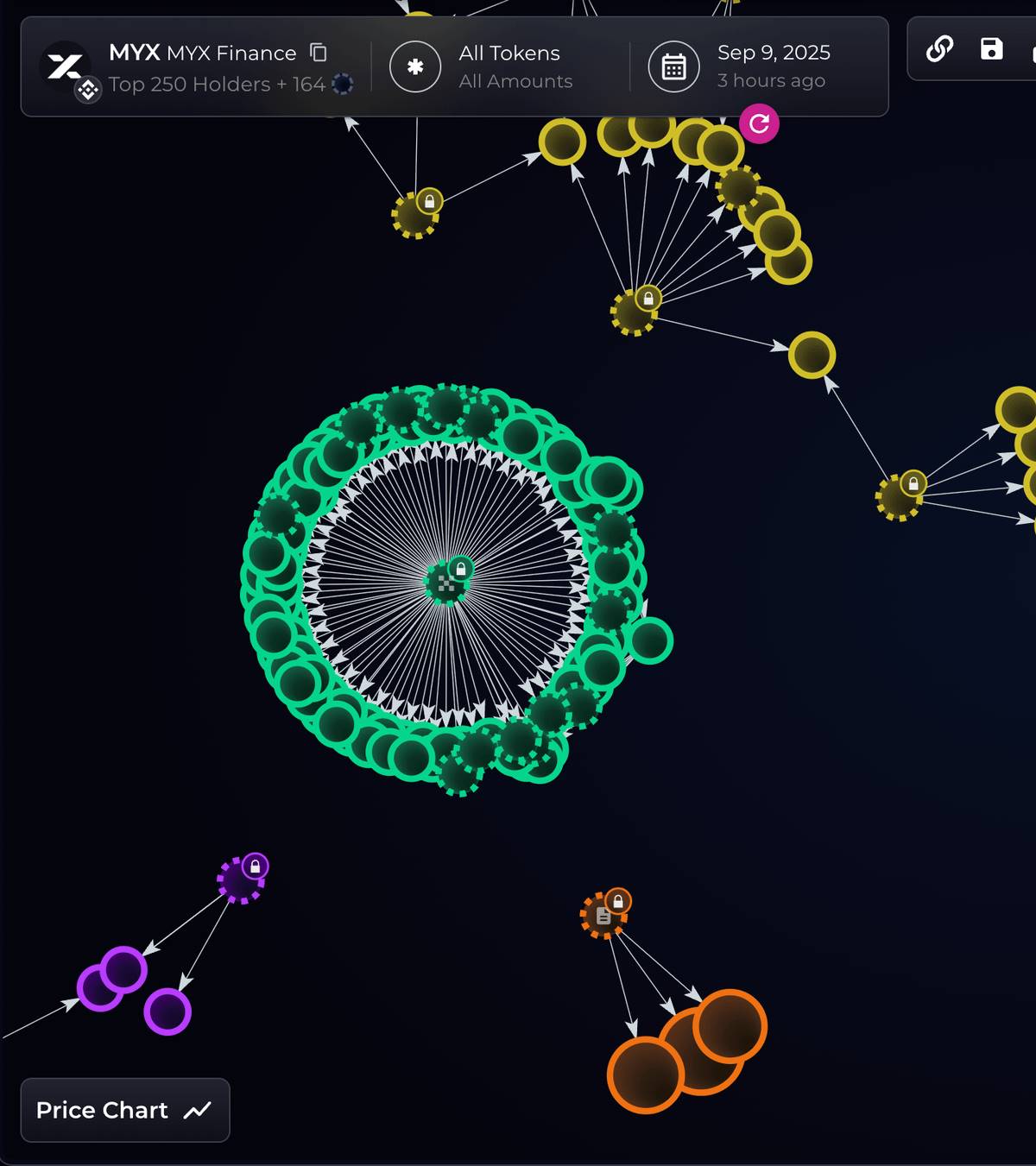

First, let's look at a recent MYX show.

In early September 2025, its price on multiple exchanges skyrocketed like a rocket. Within a week, it peaked at over ten dollars, and the media amplified the hype.

Immediately after, the on-chain data team Bubblemaps posted a series of long threads on X (formerly Twitter): "The same entity used 100 newly funded wallets to withdraw about $170 million from the MYX airdrop," providing on-chain tracking details (posted continuously since September 9).

Subsequently, industry media and news platforms followed up and reprinted the information, and the situation quickly escalated. Ordinary users also expressed their direct feelings on different platforms:

A user on Binance Square, "Arfath 29," posted a reminder: "The top 5 addresses hold 72.63% of the total supply; once they dump, retail investors will be left holding the bag." (Mid-September, posted on Binance Square). This is not professional jargon, just plain language: a few large holders call the shots.

Another user on Binance Square, "Lenora Opatz yMnL," was even more straightforward: "Many people shorted this broken coin and lost all their previous gains, like having liquidity pulled out every hour; they can't escape." (Mid-September, posted on Binance Square). This reflects the "dilemma" retail investors feel in real volatility.

The next day to the third day, the media began to systematically sort out the entire situation: some articles referred to this wave of market activity as a combination of "spot lifting—squeezing out contract shorts—selling while hot"; they even compared the timing of unlocking 39 million tokens with the price peak, reminding that this was the "best liquidity and easiest distribution" window. Dates, amplitudes, and liquidation amounts were all quantified.

The price increase and selling were clear to everyone. In fact, the "gears" of this round of short squeezing were quite obvious:

Low circulation + Spot price increase → Index rise → Contract liquidation → Passive buying pushes higher.

The core principle is: small amounts of spot money leverage large amounts of contracts.

As long as the price is pushed past a few key levels, the liquidation engine will continue to buy for the bulls, forming a feedback loop of "price increase—liquidation—further price increase," leading to a mass exit of shorts. This was the direct background for the "over $40 million in liquidations" on September 8-9.

However, MYX officially responded on September 10, denying fraud and manipulation, stating that the airdrop rewards were "based on real trading and LP contributions," and indicated that they would pay more attention to preventing witch attacks (implying that these airdrop tokens were claimed by witches). On the same day, several English media outlets recorded this response and cited the long thread from Bubblemaps on September 9. In other words, accusations and defenses were laid out simultaneously, with each side holding firm to their claims. (Coinspeaker)

The most critical support for MYX's denial of manipulation is that MYX is currently around $15.

However, if you think that MYX did not push for higher selling based on this, you are gravely mistaken. The reason is simple:

"Standing firm at a high position" does not equal "reasonable valuation"; it is more about the synergy of structure and rhythm.

MYX currently has a circulation of about 197 million, accounting for about 20% of the total supply; under the "low circulation / high FDV" framework, the "elasticity" of the unit price is significant. As long as the new selling pressure is not intense (MYX airdrops are unlocked monthly) and the market makers are willing to absorb, the price can stay high for a long time.

In short, the script of this MYX show is not new:

Low circulation supports the price, derivative leverage amplifies volatility, and liquidations turn shorts into buying pressure;

The reason the price remains high is mostly due to structural supply tightness, increased entry points, and the combined effect of upgraded narratives.

Regardless of which side you stand on, at least clarify two things:

Whoever controls the order and flow can better dictate the rhythm;

High-level consolidation does not mean the risk has disappeared.

Therefore, if you participated in MYX trading and lost a lot of money, it is not surprising. Because this game inherently favors those who control the narrative and the chips. For MYX, it’s best not to touch it. If you, like me, have an airdrop, just sell it when the time is right.

If we abstract this type of repeatedly played story into a framework, its name would be:

Predatory Market Structure

It is not a single-point scam but a whole set of intentionally assembled "institutional arrangements + trading mechanisms + incentive designs," allowing the side with more information and concentrated power to stably and repeatedly extract value from weaker participants.

In simple terms, the predatory market structure is a jungle society, where the only rule is—survival of the fittest.

In traditional finance, this structure hides in order flow rebates and dark pool internalization, in market-making hype and deceptive orders;

In the crypto world, it transforms, using "high FDV, low circulation" issuance methods, creative distribution and order flow (MEV), KOL amplification chains, and liquidation mechanisms to perform old tricks faster and more violently.

In other words, it is not a "bug" in the system but a "feature" written into the products and institutions. Understanding this, the question is no longer "who ripped off whom," but why this structure can operate long-term, what maintains its moat, and what we can do.

Next, we will break it down one by one.

1. Why "predation" in the crypto circle is "persistent"

Just like the MYX example above, on the surface, it appears to be a specific project, a piece of news, or a market crash, but behind it, several long-term unchanging foundations are at work—who has more agile information, who has the ability to turn information into profit, and where the gaps in the system are.

Understanding these three foundations is key to grasping why the same set of tricks can be repeatedly performed and knowing where to start to protect oneself.

1.1 The Three Pillars of Predation

If you only focus on one or two instances of volatility, it is easy to blame everything on "human greed." But zooming out, you will see a more stable "topography":

The first pillar is information asymmetry.

This is not a new term—economist Akerlof explained it with the "lemons market" back in 1970: when buyers find it hard to distinguish good from bad, bad products will drive good ones out of the market.

"Lemon" is not a literary metaphor but a colloquial term in American slang for problematic cars or substandard products (the U.S. even has a specific "Lemon Law" to protect buyers). In the early 20th century, media used "lemon" to refer to "purchased inferior goods," later specifically indicating problematic used cars.

Akerlof used the used car market as a metaphor: sellers know the true condition of the car, while buyers find it hard to discern and can only bid based on "average quality," resulting in quality car owners being unwilling to sell, and lemons driving good cars out of the market, leading to a decline in overall quality.

In crypto, project teams understand token distribution, unlocking rhythms, and market-making arrangements better than ordinary people, resulting in "quality scarcity and poor quality rampant."

This theory is not just theoretical; it has been validated by generations of data.

The second pillar is that there is always a party with the ability and motivation to exploit the asymmetry.

In traditional securities markets, whoever controls how your orders are routed and in what order they are executed can more easily "eat a little spread" in places you can't see. Therefore, U.S. regulators require brokers to disclose order routing and fulfill "best execution," even facing heavy penalties for failing to meet obligations—such as Robinhood in 2020, which was fined $65 million by the SEC for failing to adequately disclose rebates and not providing customers with the best prices.

This shows that control over routing and order can turn into "invisible costs" that retail investors find hard to detect. (sec.gov)

Applying the same logic on-chain is more straightforward: whoever can alter the order of entry may profit by sandwiching your trades, which is what is often referred to in research as "order flow." Multiple papers have systematically documented these "sandwiching" practices since 2019, pointing out that they harm the transaction quality for ordinary users and can even affect consensus stability in severe cases.

The value of order flow lies in its ability to convert "temporal precedence" into "certain benefits."

This is what you often hear about MEV attacks. "A Comprehensive Analysis of MEV Sandwich Attacks: From Ordering to Flash Swaps" is my detailed breakdown of one MEV attack that caused a trader to lose $215,000 in one go.

The third pillar is a loose or lagging external environment.

When an activity does the same thing as traditional finance but operates outside of regulation, it effectively gives predators a "low-risk, high-reward" haven.

The International Organization of Securities Commissions (IOSCO) released two sets of final recommendations in 2023-2024, one for crypto and digital asset service providers (18 items) and one for DeFi (9 items). The core message is to clearly delineate the red line of "same activities, same risks, same regulatory outcomes": if you are engaging in activities that involve risks needing management in the securities market, you should face similar conflict isolation, information disclosure, and market manipulation constraints.

In other words, while the institutional fences are being repaired, gaps do exist, and predators are best at thriving in these gaps. (iosco.org)

1.2 Weaponizing "Complexity"

Information asymmetry is not always "natural"; often, it is deliberately amplified.

The 2008 financial crisis serves as a ready-made "complexity" textbook: slicing high-risk loans into layered securities, paired with overly optimistic ratings, makes it hard to understand how many hidden risks are truly involved; the Financial Crisis Inquiry Commission (FCIC) report extensively reviewed this chain, concluding plainly—complex structures obscure real risks. (fcic-static.law.stanford.edu)

The "complexity" of the crypto world has changed its shell: token economics can be written in any way you don't understand—permissions, minting, blacklists, taxes, unlocking— as long as there are enough variables, it is almost destined that "ordinary people won't understand." Complexity here is given a "mission": I don't need every investor to understand; as long as the majority don't, the chips can be transferred under seemingly fair but actually highly asymmetric conditions. (Kaiko Research)

"Complexity" has another layer of utility: it obscures responsibility.

When the process is long enough, and the roles are numerous, each link can say, "I am just following the procedure." This is precisely the lesson from the old script of "from lending to distribution" in 2008: risks were fragmented, responsibilities were further divided, and when something went wrong, it became difficult to trace a clear line of accountability.

Crypto has often replicated this "chain-like" division of labor—issuing, market making, listing, custody, marketing—interconnected yet pointing to different legal entities. This is also why the International Organization of Securities Commissions (IOSCO) repeatedly points out the serious conflicts of interest in vertical integration; only by dismantling this layer of "complexity" can we potentially prevent the repeated occurrence of predation, which we will discuss in detail later. (iosco.org)

1.3 "Emotions" are "mass-produced"

If "complexity" makes it hard to see clearly, then "mass production of emotions" makes it hard to stop.

Social platforms have changed the speed and radius of narrative dissemination; "emotions" can be manufactured in bulk like products. Chainalysis's annual report in 2024 noted that among the ERC-20 tokens newly listed on DEX in 2023, 54% exhibited characteristics of "suspected price manipulation"—this does not mean they all involved scams, but it indicates that the model of "scripted hype" is extremely common; at the same time, these tokens collectively accounted for only 1.3% of total DEX trading volume, meaning they are small but dense and easily manipulated. This aligns perfectly with the business logic of "using small money to leverage large volume, using large volume to attract real liquidity." (Chainalysis)

Even more frightening is that the "megaphone" is continuously evolving, even becoming automated.

Research in 2023 revealed a crypto "bot army" operating on the X platform, using generative AI to automatically write copy, auto-reply, and drive traffic to suspicious sites in bulk; the technology is not sophisticated, but the idea is clear: turning "hype" from a manual workshop into an assembly line.

By 2024 and 2025, media and on-chain evidence-gathering institutions further observed that scams and "pig-butchering" schemes leveraging AI were not decreasing but rather increasing in scale, even moving towards "template outsourcing."

When the costs of "scripts" and "emotions" are driven down to extremely low levels, the information waterfall will continuously push people toward that familiar place—rushing in at the busiest times, getting stuck at the most crowded exits. (WIRED)

1.4 Summary

Putting these three major points together makes it clear: many times, it's not that you have bad luck, but that "more powerful people" have turned information asymmetry into a business, weaponized complexity, and mass-produced emotions. As long as "control" and "profit distribution" are not aligned, this game will continue to replay—whether it's Wall Street's CDOs or on-chain memes.

You might ask: everything has a beginning and an end; when will the "predation" in the crypto circle come to an end?

2. Is there an end to "predation" in the crypto circle?

Yes, but "predation" never disappears on its own. The order of capital markets is almost always formed as scars when wounds are stitched up. The current predation in the crypto circle is merely a replica of the stock market. Knowing how predation in the stock market comes to an end makes it easy to guess the timeline for the crypto circle.

2.1 The End of "Predation" in the Stock Market

The stock market of the last century was like this: the "Black Thursday" of 1929 pulled Wall Street down from its pedestal, and the Dow Jones index subsequently fell to nearly 90% by 1932, leading to bank failures and a collapse of confidence, which ultimately prompted the creation of the Securities Act (1933) and the Securities Exchange Act (1934), along with the now-familiar SEC (U.S. Securities and Exchange Commission).

The mission of this agency is quite simple: to protect investors, maintain a fair and orderly market, and promote capital formation—its emergence marked a turning point: capital markets were transitioning from a "wild growth" jungle to a "regulated playing field."

Crisis—legislation—evolution is a recurring rhythm in the century-long history of the stock market.

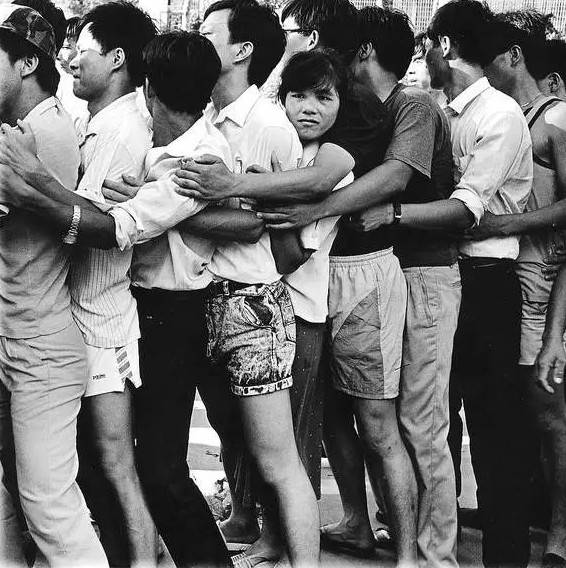

Looking back at China, it is the same. The "Shenzhen 8.10" incident in 1992 nearly halved the newly established stock market in just a few days, directly leading to the establishment of the China Securities Regulatory Commission (CSRC) in October of the same year, transitioning from a "free-for-all" experimental field to a market with "regulatory thresholds." The image below shows people queuing to purchase new stock subscription lottery tickets during the incident.

So, when we ask, "Is there an end to predation in the crypto circle?" a more accurate statement would be:

Yes, but it will not come voluntarily.

From the footprints of the stock market, the end usually appears after significant chaos, marked by the integration of systematic rules, disclosures, and "brakes."

2.2 Where is the Way Out for the Crypto Circle?

The solutions are actually already available; the key lies in implementation.

As early as November 2023, the International Organization of Securities Commissions (IOSCO) released 18 final recommendations for the crypto and digital asset market (CDA), translating the "well-established practices" of traditional securities markets into the crypto context:

The same activities, the same risks, should have the same regulatory outcomes.

These recommendations directly address most of the "old problems" in the crypto circle: conflicts of interest in centralized service providers (CASPs), market manipulation and insider trading, custody and client asset segregation, technological and operational risks, as well as the appropriateness and marketing boundaries for retail users. IOSCO's press release prominently stated the principle of "same activities, same risks, same regulatory outcomes," along with a complete report. (iosco.org)

In December of the same year, IOSCO presented 9 final recommendations for the DeFi direction, breaking down the seemingly ownerless area of "decentralization" into accountable "Responsible Persons":

Whoever designs the product, operates the front end, or collects fees should bear corresponding obligations for information disclosure, risk management, and cross-border cooperation.

The accompanying Umbrella Note explains how the CDA and DeFi recommendations interconnect—regardless of whether you are a centralized platform or the organizer, distributor, or front-end operator of a smart contract, as long as you are engaged in similar securities market activities, you should fall under the same results-oriented regulatory framework.

This is not a "one-size-fits-all" approach but rather a transfer of "expected outcomes": what you do should align with the results. All original texts can be downloaded and verified on the IOSCO website. (iosco.org)

If you imagine the "post-implementation crypto circle," the scene won't be unfamiliar:

Trading orders should have clear boundaries, like the traditional market's "prohibition of inferior price transactions," striving to avoid sandwiching ordinary people in between;

Information disclosure should shift from "beautiful white papers" to "auditable fact lists," laying out token distribution, unlocking schedules, contract permissions, and related party interests;

Conflicts of interest should either be isolated or let prices compete—whoever controls the order flow/traffic rights should make this part of the profit transparent and competitive, returning fees to users rather than letting them disappear into a black box.

The familiar "brakes," "prohibition of inferior price transactions," and "broker-dealer segregation" in the stock market all have transferable shadows in the crypto world. The reason IOSCO's two sets of recommendations are called "results-oriented" is that they do not insist on whether you are using a chain or a database; they only ask what financial functions you have achieved, aligning you with the same order and responsibility. (sec.gov)

2.3 Summary

Of course, the end of "predation" will not come on its own. The order of the stock market grew out of major declines, scandals, and costs; the crypto circle will not skip the "growing pains."

But the good news is: this time it is not starting from scratch; a ready toolbox is already laid out on the table—reports, terms, processes, disclosure templates, and even bridges on "how to connect centralization and decentralization" have been written.

What remains is how the industry and regulators can integrate them into reality: handing over the speed of narrative to technology and the bottom line of order to rules. Once these nails are firmly driven in, although "predation" will not completely disappear, it will become increasingly expensive, difficult, and less worthwhile.

However, you must remember that before "predation" disappears, it is also the most dangerous moment.

3. In the present, you need a resilient investment philosophy

Resilience is not about whether you can "predict tops and bottoms," but whether you have a sense of order that does not self-destruct in any market condition.

It consists of three principles:

Only invest in assets you are willing to hold for ten years; reverse the information asymmetry into a process of due diligence; and remove leverage from your vocabulary.

3.1 Only invest in coins you are willing to hold for ten years

"Willing to hold for 10 years" is the gate; behind the gate is the definition.

Benjamin Graham defined investing as "the operation of committing capital with the expectation of safety and adequate return based on thorough analysis; anything else is speculation." This is not just a platitude but shifts the question from "how much can I earn" back to "what am I actually buying." (Novel Investor)

What you are willing to hold for ten years is usually an asset with clear utility, sustainable cash flow, or network effects; those that cannot pass this test are mostly just the next wave of "excitement." The value of this boundary lies in forcing you to first answer "what am I buying," rather than "how much can I earn."

Data also reminds us not to overestimate our "speed of decision-making." Classic large-sample studies tracked 66,465 household accounts: the more frequently you trade, the worse your returns; the most "diligent" group had an annualized return of only 11.4%, while the market benchmark was 17.9%. The same applies at the institutional level: the S&P's SPIVA scorecard shows that in 2024, 65% of actively managed funds in the U.S. underperformed the S&P 500; extending the time frame, the proportion of underperformance is even higher.

In plain language: make fewer decisions, but make the right ones. (faculty.haas.berkeley.edu)

3.2 Reverse "information asymmetry" into "I understand it before I invest"

In crypto, "complexity" is often used as armor: permissions, taxes, blacklists, inflation, unlocking schedules… the more variables there are, the easier it is to keep ordinary people out. Instead of passively taking hits, it's better to systematize the due diligence process and regain control over your win rate.

The first step is to look at the supply structure: place the fully diluted valuation (FDV)—circulation ratio—unlocking rhythm on the same sheet of paper. Multiple verifiable studies have long recorded a common phenomenon: before and after large unlocks, increased volatility and weakening prices are more common, and the larger the unlock, the more obvious the pressure. You can cross-check Kaiko's quarterly/annual research with TokenUnlocks' timeline to first determine "who will provide selling pressure in the coming months." (Kaiko Research; TokenUnlocks)

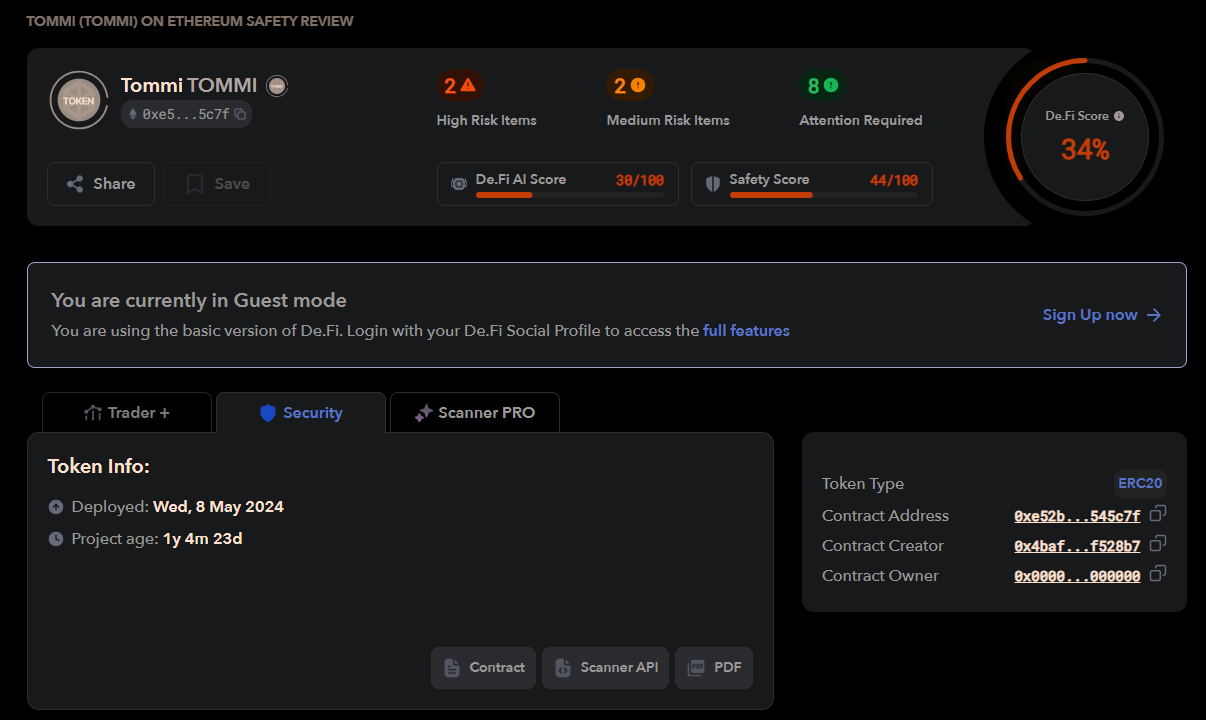

The second step is to conduct a contract health check: you can use tools like De.Fi Scanner for a quick screening to identify potential pitfalls—these are not audits, but they are sufficient to raise red flags for obvious issues in advance (as shown below).

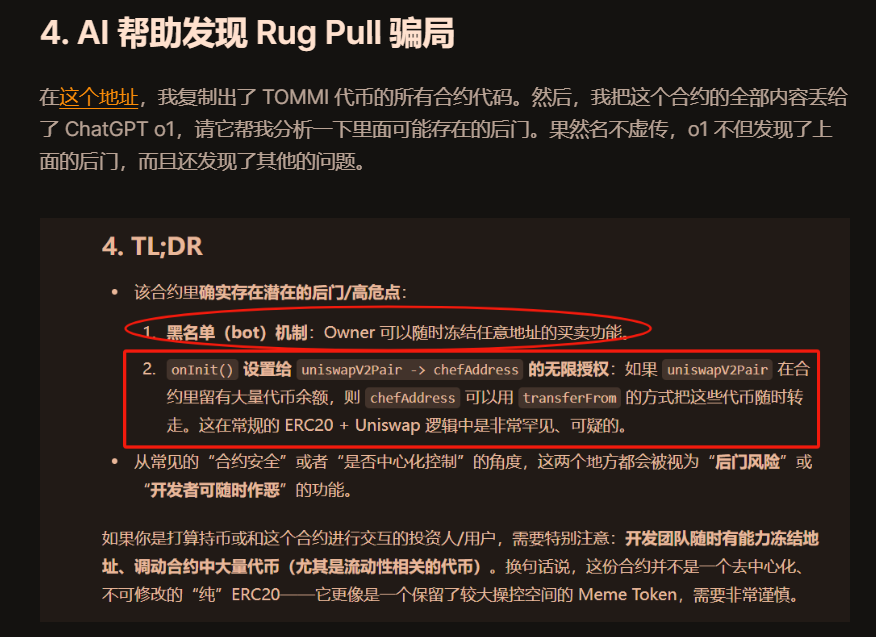

If you want to further understand contract issues, you can use AI for deeper analysis. In the "Beginner's Guide: How to Avoid the '100x Coin' Trap," I detailed how to use ChatGPT to discover that the TOMMI project not only has backdoors but also poses risks of blacklisting.

The third step is to manage trade execution and remove yourself from the "sandwiched" queue. First, use aggregators to compare prices; go with whoever can provide a better actual executable price.

On EVM chains: I often use 1inch (including Fusion/RFQ) and Odos (Protected Swaps); the former can utilize market maker quotes, while the latter provides MEV protection routing (as shown below), significantly reducing slippage and "sandwiching."

On Solana, Jupiter and Titan's routing capabilities and private channels can also lower the probability of being hunted. Regardless of the chain, tightening slippage, breaking large amounts into smaller ones, and prioritizing channels with MEV protection/private memory pools are all forms of "physical isolation" you can implement right now.

In simple terms, first understand the three things: "supply—permissions—execution," and then decide whether to take action. By doing this, you have already transformed a large part of the information asymmetry into your own certainty.

3.3 Remove "leverage" from your vocabulary

Leverage is the trigger that magnifies normal fluctuations into "liquidations."

The Financial Stability Board's assessment bluntly states: the automatic liquidation mechanisms, collateral chains, and pseudo-anonymous leverage of crypto CEX and DeFi make forced deleveraging during downturns more contagious and self-amplifying; once prices touch the liquidation threshold, machines will make decisions before humans, thus exacerbating the decline.

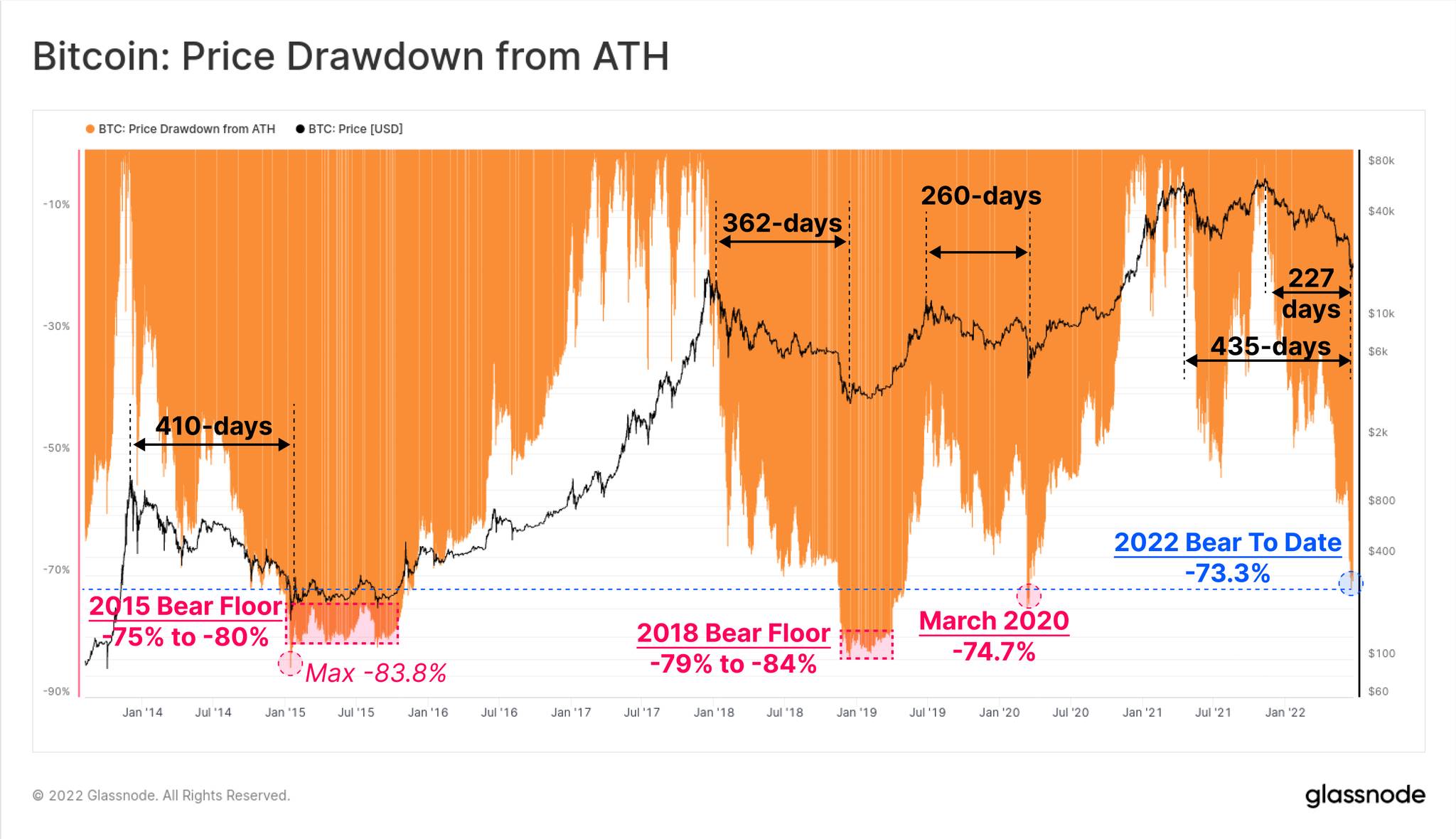

History is also very straightforward: it is not uncommon for Bitcoin to experience 30%-50% pullbacks during bull markets, and complete cycles have seen declines of 80% from peak to bear bottom multiple times, as shown below.

So first set a life-and-death line for yourself: do not use leverage, especially do not hand over your survival to liquidation engines; then reduce your positions and frequency to a level where you can "sleep well."

3.4 Summary

On-chain data has long reminded us: the noise often exceeds the volume, and the exits are often very narrow; while order and compounding require slowness and patience.

Resilience is not about turning yourself into a sharp blade, but about putting on "armor."

Do not gamble against the structural advantages of "predators."

Conclusion: Through the jungle, see order and the long term

Zooming out, you will see two forces advancing simultaneously:

On one side, gold mining and predation are taking turns, while on the other, order is slowly but steadily growing.

The crypto world's "transition from disorder to order" has entered the construction phase—IOSCO's results-oriented framework is being implemented, European compliance rules are accelerating in formation, and compliant capital and on-chain infrastructure are beginning to move toward each other.

Stablecoins have turned cross-border clearing and settlement into "real-time, programmable" public utilities, while ETFs and tokenized assets are bringing trust and auditing back on-site.

All these changes convey the same signal:

Predation is not the endgame; order is approaching; bubbles are not everything; value is solidifying.

However, before the rules are fully laid out, you still need to wear your armor and not gamble against structural advantages.

Remember: Give speed to others, keep survival for yourself; cycles are indifferent, compounding has patience.

When order is restored, advantages will shift from "quick hands" to "patience and discipline," and you will be glad you stood on the side of long slopes and thick snow.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。