Author: @BlazingKevin_, the Researcher at Movemaker

The Real Adoption and Expansion of Dollar Stablecoins

In our previous analysis, we argued that the birth of Plasma was a key strategic move by Tether to fundamentally transform its business model from a passive "stablecoin issuer" to an active "global payment infrastructure operator," aiming to recapture the immense value seized by third-party public chains. The urgency and importance of this strategic layout are continuously amplified by an irreversible macro trend: the adoption of dollar stablecoins in the real world is undergoing a significant paradigm shift and entering an accelerated expansion phase.

1. Quantitative Expansion of Market Size

First, from a macro data perspective, the overall scale of the stablecoin market is experiencing a new round of structural growth. Compared to the market cycle two years ago, the total market capitalization of global stablecoins has risen from about $120 billion to $290 billion, achieving a 140% increase. This data indicates that the demand for stablecoins has surpassed the speculative and trading realms of the crypto-native field, beginning to gain recognition as an independent asset class and financial tool in a broader market.

2. Explosive Core Application Scenario: Cross-Border Payments

The strongest manifestation of this growth is in the vertical field of cross-border payments. Two years ago, the actual use cases of stablecoins for cross-border settlements were still in their infancy and almost negligible. According to the latest data, the current monthly settlement volume in this field has surpassed $60 billion. More notably, the growth rate is impressive—monthly growth of 20% to 30% clearly demonstrates a steep adoption curve.

Despite the rapid growth, its market penetration remains in the very early stages. Relative to the current global traditional cross-border payment market, which amounts to as much as $200 trillion annually, the share of stablecoins remains insignificant, indicating that there is still enormous growth potential in the future, potentially tens or even hundreds of times.

3. Core Driving Force: "Currency Substitution" Demand in High-Inflation Economies

The accelerated adoption of stablecoins is driven by strong economic forces in the real world, particularly evident in emerging markets and high-inflation countries.

An in-depth analysis report from Cointelegraph in August pointed out that in countries like Venezuela, the sovereign currency (the Bolívar) has essentially lost its core function as a medium of daily commercial transactions due to hyperinflation. Strict capital controls, a dysfunctional local banking system, and chaotic official exchange rates have created a "scorched earth" financial environment. In this context, citizens and businesses actively seek currency substitutes, and dollar stablecoins, which offer ample liquidity and value stability, have proven to be far more reliable than cash or local bank transfers, becoming the market's spontaneous choice of "hard currency."

This phenomenon is not unique to Venezuela. Since the global inflation wave in 2022, several major economies, including Argentina, Nigeria, Turkey, and Brazil, have faced severe depreciation pressures on their national currencies, leading to a massive demand for value storage and payment hedging.

Venezuela ranks 18th globally in cryptocurrency adoption. Source: Chainalysis

According to Chainalysis data, Venezuela's cryptocurrency adoption rate ranks 18th in the world. More compelling data shows that in 2024, 47% of small transactions under $10,000 in the country will be completed using stablecoins, making it the ninth largest country in the world by per capita cryptocurrency adoption. This is no longer a niche behavior; it is strong evidence that stablecoins have deeply embedded themselves in the socio-economic fabric.

More importantly, this adoption is gradually moving from the spontaneously "gray" area to the officially recognized "sunshine" area. In Brazil, stablecoins have been integrated into the national instant payment system PIX; in Argentina, using stablecoins to pay for large contract amounts like rent has also gained legal recognition. These cases mark the evolution of stablecoin adoption from "bottom-up spontaneity" to "top-down confirmation."

Dollar Stablecoins: Three Strategic Pillars of U.S. National Interest

Since the regulatory framework represented by the "Genius Act" has clarified, the growth trajectory of dollar stablecoins has shown an exponential acceleration, and its long-term potential has yet to hit a ceiling. This explosive growth is not just a market behavior but is deeply tied to U.S. national strategic interests. From a macro perspective, the global expansion of dollar stablecoins can bring at least three strategic benefits to the U.S.:

1. Maintaining Dollar Hegemony: An Asymmetric Extension of Monetary Influence

Over the past decade, the global process of "de-dollarization" has been slow but steadily advancing, posing a long-term erosion of the dollar's status as an international reserve and settlement currency. The rise of dollar stablecoins provides a new, asymmetric solution to reverse this trend.

Especially in the high-inflation countries mentioned earlier, the proliferation of dollar stablecoins essentially constructs a parallel "digital dollarization" economy outside the financial systems of sovereign nations. It effectively bypasses these countries' capital controls and fragile fiat currency systems, allowing the value proposition of the dollar to reach end users directly. This approach does not employ any traditional geopolitical or military means but achieves deep monetary penetration into these economies, significantly expanding the actual coverage of the "dollar ecosystem" (traditional dollars + digital dollars), thereby consolidating the dollar's international status in a new dimension.

2. Alleviating Fiscal Pressure: Creating Structural Demand for U.S. Treasury Bonds

The second strategic pillar is to support the increasingly heavy fiscal burden of the U.S. government, which is crucial. The stability of the U.S. Treasury bond market, particularly its yield levels, is a core concern of U.S. economic policy. The extreme sensitivity of the Trump administration to fluctuations in the 10-year Treasury yield during tariff disputes illustrates that the Treasury bond market is the cornerstone of the U.S. macroeconomy.

The issuance mechanism of dollar stablecoins naturally creates a large and continuously growing source of demand for U.S. Treasury bonds. Although the reserve assets of current stablecoin issuers are already heavily allocated to U.S. Treasury bonds, as their total market capitalization further expands, their role as a "major buyer of U.S. bonds" will become increasingly significant. Citibank's analysis model predicts that by 2030, the potential long-term scale of the stablecoin market could reach $1.6 trillion. The model further indicates that there will be hundreds of billions of incremental demand for U.S. bonds, primarily from three sources: 1) the reallocation of globally circulating dollar cash to digital forms (about $240 billion); 2) partial reallocation of global central bank base money (M0) (about $109 billion); and 3) the reallocation of foreign-held dollar deposits to stablecoins (about $273 billion). This new purchasing power will play a significant positive role in stabilizing U.S. Treasury yields and reducing government financing costs.

3. Consolidating First-Mover Advantage: Leading Rule-Making in the Digital Asset Era

Finally, the U.S. is fully committed to ensuring its dominant position in the global crypto market, and dollar stablecoins are the core tool to achieve this goal. The regulatory shift from past suppression to current embrace, this 180-degree turn, clearly exposes the evolution of its strategic intentions. When decision-makers realized they could not completely stifle crypto technology, they quickly shifted to a strategy of "incorporation" and "utilization," aiming to bring this emerging field into their regulatory and economic framework through the establishment of a comprehensive legal framework.

This strategy is not unique to the U.S. but is a competition among major global economies. All countries and regions actively legislating for stablecoins ultimately aim to secure advantageous positions in this new fintech race and share in future dividends. By supporting dollar stablecoins, the U.S. aims to ensure that the underlying settlement standards of the future global digital economy remain firmly in its hands.

The Status of Non-Dollar Stablecoins: Structural Dilemmas and Strategic Necessity

1. Extreme Centralization of Market Structure

Despite the strong expansion momentum of dollar stablecoins, a healthy global digital asset ecosystem should ideally present a landscape of multiple fiat currencies coexisting. However, real data reveals an extremely imbalanced picture: the market space for non-dollar stablecoins is being severely squeezed.

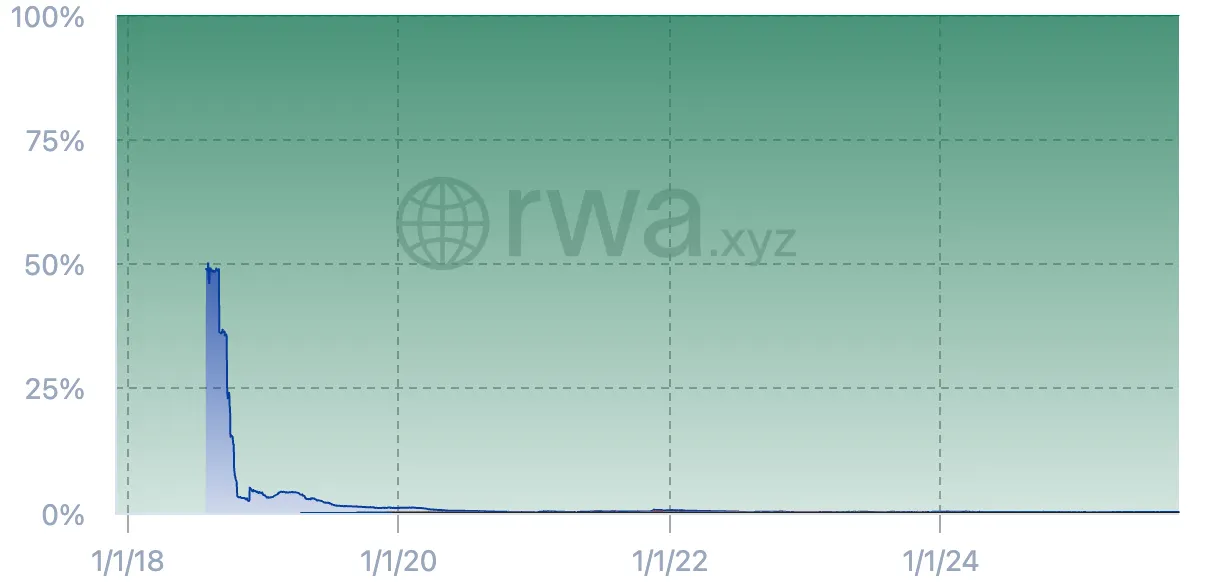

Market share of stablecoins supported by different fiat currencies. Source: rwa.xyz

Data shows that this segment has experienced dramatic shrinkage. In the early stages of market development in 2018, non-dollar stablecoins held a market share of 48.98%, almost on par with dollar stablecoins (51.02%). However, today, their total market share has collapsed to just 0.18%. In absolute terms, the total market capitalization of non-dollar stablecoins is only $526 million, with euro stablecoins (at $456 million) dominating nearly 88.7% of the absolute market. This indicates that, outside of the dollar, no other fiat currency has been able to form effective market competitiveness in the stablecoin arena.

2. Structural Risks: "Exchange Rate Tax" for Non-Dollar Zone Users

As the stablecoin market becomes increasingly intertwined with real-world economic activities, this "unipolar system" composed of dollar stablecoins poses potential structural risks for users in non-dollar zones (especially in developed economies that are also in low-inflation environments). The core issue is that they are forced to bear unnecessary foreign exchange volatility risks while participating in the global crypto economy.

We can illustrate this issue through a typical user path:

Suppose a user in Tokyo uses Japanese yen (JPY) to purchase Ethereum (ETH) on the local compliant exchange bitFlyer. When she wishes to invest these assets into a global DeFi protocol (such as lending on Aave or providing liquidity on Uniswap), she finds that the core liquidity pools of these mainstream protocols are almost entirely denominated in dollar stablecoins (USDC, USDT, etc.).

The concept of "yen balance" in her bitFlyer account cannot be directly transferred to the on-chain world. To participate in DeFi, she must hold a stable asset that is tokenized on-chain. In the absence of a sufficiently liquid and composable yen stablecoin, her only option is to exchange ETH for a dollar stablecoin. This operation adds an unnecessary layer of JPY/USD exchange rate exposure to her investment portfolio. Regardless of whether she profits or incurs losses in the future, when she eventually converts back to yen, she will have to bear the exchange rate fluctuations during that period, effectively being taxed with an invisible "exchange rate tax."

3. Systemic Risks and the Strategic Necessity for Diversification

From a more macro perspective, the current liquidity lifeline of the entire crypto economy is almost entirely dependent on dollar stablecoins, which constitutes a potential and highly concentrated systemic risk point. Any extreme regulation, technical failure, or monetary policy shock originating from the U.S. could have catastrophic effects on the global market.

Therefore, promoting the development of high-quality stablecoins such as the euro, pound, and yen is far more significant than mere market competition. It is akin to building a "risk isolation wall" and a "systemic backup plan" for the global crypto economy. A diversified multi-fiat stablecoin ecosystem can effectively hedge against the risks brought by excessive reliance on a single national currency and regulatory system, enhancing the overall system's anti-fragility.

For major economies like the EU and Japan, promoting stablecoins regulated by their own financial systems and pegged to their own currencies is no longer a purely commercial act but an extension of maintaining their "monetary sovereignty in the digital age," a national strategic task. Although non-dollar stablecoins currently lag far behind dollar stablecoins in scale and liquidity, their logical foundation is solid, and their development is an inevitable historical trend. Next, we will provide a detailed introduction to the development of major non-dollar stablecoins.

Euro Stablecoin

Against the backdrop of the dollar's absolute dominance in the global stablecoin market, the evolution path of the euro stablecoin provides us with an excellent sample to observe how non-dollar currencies attempt to break through under regulatory drives.

1. Two Stages of Market Evolution: From Early Exploration to Regulation-Driven Acceleration

The development history of the euro stablecoin can be clearly divided into two stages, with the EU's Markets in Crypto-Assets Regulation (MiCA) serving as a watershed:

- Early Exploration Stage (Pre-MiCA): The hallmark project of this stage is the STASIS Euro (EURS), launched in 2018. As a market pioneer, EURS faced a long period of slow growth, with its market capitalization hovering between tens of millions to one hundred million euros. This reflects that, in the absence of a clear regulatory framework and institutional demand, the market was limited to a few local crypto enthusiasts in Europe, failing to achieve economies of scale.

- Accelerated Development Stage (Driven by MiCA): The proposal and gradual implementation of the MiCA regulation have been fundamental catalysts for changing the game. It provides market participants with unprecedented legal certainty, attracting formal entry from industry giants. Stablecoin issuers Circle (issuer of USDC) and Tether (issuer of USDT) respectively launched Euro Coin (EURC) and Euro Tether (EURT). Notably, Circle, with the approach of MiCA, began actively promoting its multi-chain deployment strategy during 2023-2024, expanding EURC to multiple mainstream public chains such as Ethereum, Solana, and Avalanche.

The results of this strategic transformation are evidenced by data: from 2023 to October 2025, the total market capitalization of euro stablecoins experienced rapid growth, currently reaching $456 million. Among them, Circle's EURC contributed the vast majority of the increment, with its market capitalization achieving a 155% increase in 2025, growing from $117 million at the beginning of the year to $298 million. Although the absolute value still has a huge gap compared to dollar stablecoins, its growth rate shows a strong momentum of catching up.

2. Market Acceptance Assessment: Infrastructure Ready, Network Effects Insufficient

- Integration with Exchanges and DeFi: The euro stablecoin has completed the basic infrastructure setup. All major exchanges, including Coinbase, Kraken, and Binance, have listed EURC or EURT and provided trading pairs with mainstream crypto assets. At the same time, leading DeFi protocols such as Aave, Uniswap, and Curve have also completed integration. Particularly in protocols like Curve, which optimize stablecoin exchanges, the liquidity scale of euro stablecoin pools is steadily increasing.

- Potential Application Scenarios: In the payment and remittance sectors, some Web3 payment applications and fintech companies have begun small-scale pilots, utilizing euro stablecoins for instant settlements and cross-border payments within the eurozone.

- Core Barrier—Cognitive Gap: Despite the initial completeness of the infrastructure, the euro stablecoin faces a significant "cognitive gap" and "network effect deficit." In the mental models of the vast majority of global crypto users, the concept of "stablecoin" is almost synonymous with "dollar stablecoin," making it extremely challenging for euro stablecoins to acquire new users and liquidity.

3. Dual Dilemmas for Future Development

- Potential Competition from Official Digital Euro (CBDC): The European Central Bank (ECB) is actively advancing the research and development of a digital euro. Once a central bank-issued digital euro, which carries no credit risk, is launched, it will pose direct and asymmetric competition to privately issued euro stablecoins. At that time, the digital euro is likely to gain overwhelming advantages in regulatory status and application scenarios, thereby squeezing the survival space of private stablecoins.

- Business Model Challenges from Interest Rate Differences: This is a more fundamental economic constraint. The core profit of stablecoin issuers comes from the interest income of their reserve assets (mainly short-term government bonds). Historically, interest rates in the eurozone have been lower than those in the U.S. This means that, at the same scale, the profitability of issuing euro stablecoins is inherently weaker than that of issuing dollar stablecoins. This difference in profitability directly limits the issuers' ability to promote DeFi protocol integration and user adoption through revenue sharing and liquidity incentives, creating a negative cycle that hinders their cold start and scale expansion.

Australian Dollar Stablecoin

The Australian dollar stablecoin market presents a development paradigm that is entirely different from that of the eurozone. Although its total public market capitalization is about $20 million, ranking second among global non-dollar stablecoins, its most notable feature is the top-down exploration led by traditional banking institutions rather than crypto-native companies.

1. Market Dominant Force: Entry of Traditional Banks

The most notable stablecoin projects in Australia originate from two giants among the "Big Four" banks—Australia and New Zealand Banking Group (ANZ) and National Australia Bank (NAB), which have launched A$DC and AUDN, respectively. This phenomenon is extremely rare on a global scale, marking a direct recognition of the potential value of stablecoin technology by the mainstream financial system. However, it is worth noting that these two bank-issued stablecoins are still primarily in the stage of interbank settlements and internal pilots, and have not yet been widely opened to the public.

The supply of Australian dollar stablecoins aimed at the retail and crypto trading market is mainly filled by third-party payment companies, with AUDD being a representative.

AUDD (by Novatti)

- Issuer Background: Novatti is a licensed payment service provider listed on the Australian Securities Exchange (ASX), with a dual background in compliance and fintech.

- Target Audience: Its positioning is clear, primarily serving three types of users: cryptocurrency traders, individuals or businesses with Australian dollar cross-border remittance needs, and Web3 application developers.

- Technical Path: AUDD has chosen to issue on public chains known for payment efficiency, such as Stellar, Ripple, and Algorand, rather than Ethereum, reflecting its strategic focus on payments and settlements.

- Market Position: Currently, AUDD is the most accessible and usable Australian dollar stablecoin for retail users.

2. Core Development Dilemma: Dual Uncertainty from Regulation and Official CBDC

- Lack of Regulatory Framework: Unlike the EU, which has fully implemented the MiCA regulation, Australia has yet to establish a comprehensive and clear legal framework for stablecoins by October 2025. This regulatory lag constitutes the biggest bottleneck for market development. Even strong banks like ANZ and NAB can only explore on a small scale, unable to promote products to the public on a large scale in the absence of clear regulatory definitions. This greatly limits the development speed and scale of the entire Australian dollar stablecoin ecosystem.

- Potential Competition from Official Digital Australian Dollar (CBDC): The Reserve Bank of Australia (RBA) has maintained a positive attitude toward issuing an official CBDC and has recently successfully completed related pilot projects. This progress brings a second layer of uncertainty to the market. If the RBA decides to officially issue a digital Australian dollar in the future, as a "ultimate risk-free asset" directly backed by the central bank with no credit risk, it will form a direct competitive relationship with stablecoins issued by commercial banks or private institutions. At that time, it remains unclear whether the two will coexist complementarily or compete as substitutes.

Korean Won Stablecoin

The South Korean market presents us with a unique paradox: as a country with a high acceptance of crypto assets, it lacks the "soil" for the growth of stablecoins. This is in stark contrast to the bottom-up adoption driven by the public in high-inflation countries, fundamentally due to the fact that South Korea's highly developed fintech and instant payment systems have already met the daily needs of the vast majority of users, thereby weakening the "intrinsic motivation" of stablecoins as a payment alternative.

Therefore, for the Korean won stablecoin to gain market adoption, the only viable path is a "top-down" strategic push led by large institutions. This may include the following scenarios:

- Led by the government or tech giants like Naver and Kakao, seamlessly integrating it into existing payment or remittance backends.

- Promoted by mainstream exchanges, replacing physical Korean won as the core trading medium with the Korean won stablecoin.

- Introduced by platform providers offering innovative incentives or micro-payment features based on stablecoins.

However, before these scenarios can be realized, the market faces a series of deep-seated structural barriers.

1. Core Development Dilemma: Legislative Vacuum and Corporate Caution

The most significant bottleneck currently is the serious lag in legislation. Although the South Korean National Assembly has five related bills pending, the legislative process is extremely slow. According to the current (October 2025) progress forecast, even if the Financial Services Commission (FSC) can submit a government proposal on time, the relevant laws will not officially take effect until early 2027 at the earliest. Before that, no company can legally and on a large scale conduct stablecoin business within a legal framework.

This regulatory uncertainty directly leads to a division and general caution among South Korean enterprises:

- Small Enterprises: Show a positive willingness to participate, but their activities are more for public relations effects and market voice, generally lacking the capital, compliance, and technical capabilities required for large-scale stablecoin operations.

- Large Enterprises (Chaebols): Generally adopt an extremely cautious "hold and wait" strategy. Their core considerations are twofold: first, the legal risks are too high; second, they assess that the actual commercial returns from shifting to blockchain technology in a highly competitive domestic market are insufficient to attract their investment of substantial resources.

Currently, all activities surrounding the Korean won stablecoin are basically limited to theoretical discussions and trademark applications.

2. Four Structural Barriers

In summary, the challenges faced by the Korean won stablecoin can be attributed to four interrelated structural barriers:

- Technical Route Dispute: Private Chain vs. Public Chain The Bank of Korea and regulatory bodies like the FSC strongly prefer to issue stablecoins on a "Korean-style customized private chain" due to primary considerations of risk controllability. However, this idea is widely regarded in the industry as "disappointing." It not only contradicts the core values of blockchain, which are openness, permissionless access, and interoperability, but it is also likely to further fragment the Korean financial system into multiple disconnected private networks, creating inefficient "walled gardens."

- Dual Constraints of Reserve Asset Market: Scarcity and Low Yield The business model of stablecoins is rooted in reserve assets. Korea faces a dual dilemma: first, its domestic financial market lacks short-term government bonds with maturities of less than one year, which means the most ideal and safest category of reserve assets is missing. Second, even alternative assets like currency-stable bonds lack the market scale and liquidity to support large-scale stablecoin issuance. More critically, the yield of about 2% in the Korean bond market is far below the approximately 4% level in the U.S., which greatly weakens the profitability motivation for issuers to operate stablecoin businesses, making it commercially unattractive.

- Technical Misunderstanding of Public Chain Regulation The prevailing view among the Korean government that "public chain risks are too high and difficult to regulate" is, to some extent, a misunderstanding of existing technology. In fact, through well-designed smart contracts, effective user identity verification (KYC) and compliance control over fund flows can be achieved on an open public chain.

- Collective Lack of Vision and Urgency The fundamental issue is that from the government, financial institutions to large enterprises, no key participant has proposed a clear goal or a specific plan for the future of the Korean won stablecoin. The entire market is caught in a state of "collective waiting," leading to a strategic stagnation. However, the evolution of global blockchain finance will not wait for any latecomers. If Korea waits until 2027 to launch its stablecoin on a closed private chain, it will find itself far behind the world.

Hong Kong Dollar Stablecoin

The development path of stablecoins in Hong Kong presents a complex picture formed by clear local regulations, active market participation, and cautious regulatory forces from the mainland. Currently, Hong Kong is at a critical turning point, transitioning from an initial overheating phase to a new stage of "localized cooling" and structural differentiation.

Despite market fluctuations, Hong Kong's official stance remains firm. The Secretary for Financial Services and the Treasury, Christopher Hui, has publicly stated that the licensing application for compliant stablecoins is progressing according to the established framework, with the first batch of licenses expected to be issued as scheduled in early 2026.

1. Hong Kong's Active Layout and Initial Market Overheating

Hong Kong's strategic goal of becoming a global leading virtual asset center is very clear. To this end, the Hong Kong government has taken a series of proactive and clearly paced measures:

- March 2024: Launched a "sandbox" for stablecoin issuers, providing a regulated testing environment for the market.

- August 1, 2025: Officially implemented the "Stablecoin Ordinance," establishing the world's first comprehensive and clear regulatory legal framework for stablecoins.

This leading regulatory certainty has greatly stimulated market enthusiasm, attracting over 77 companies to express their intention to apply, leading to a temporarily "overheated" situation in this sector. However, the rush of many financial institutions with Chinese backgrounds has raised cautious attention from mainland regulatory bodies.

2. Cautious Intervention by Mainland Regulators

Recent "window guidance" from mainland regulatory bodies to relevant Chinese institutions is not aimed at stifling innovation but is based on the following considerations:

- Risk Isolation: Ensuring that potential risks from Hong Kong's virtual asset business do not transmit back to the mainland's large and strictly regulated parent financial system through equity relationships.

- Capital Control: Preventing mainland funds from entering Hong Kong's virtual asset market through non-compliant channels.

- Market Order: Requiring Chinese institutions to maintain a low profile, avoiding excessive publicity or creating media hotspots to prevent irrational overheating in the market.

The tension between "Hong Kong's global ambition" and "mainland financial prudence" is the core background for understanding the current dynamics of the Hong Kong dollar stablecoin market.

3. Market Status: Localized Cooling, Slowed Expectations, Structural Differentiation

The intervention of mainland regulators has had an immediate impact on the market, which can be summarized as follows:

- First Batch of Exits: Before the official application deadline on September 30, at least four financial institutions with Chinese backgrounds, including Guotai Junan International, have publicly announced their withdrawal from the stablecoin license application or have postponed RWA-related business. Market expectations suggest that some originally proactive Chinese banks (such as Bank of China Hong Kong) may also delay their application processes.

- Strategy Shift to "What Can Be Done but Not Said": The guidance from mainland regulators is not a complete ban but requires "keeping a low profile." This forces Chinese institutions to shift their strategy from an initial high-profile entry to more cautious internal research and quiet layout.

- Market Structural Differentiation: This round of "cooling" is localized and asymmetric. The affected entities are highly concentrated among institutions with Chinese backgrounds. Meanwhile, local Hong Kong and other international financial institutions continue to advance their virtual asset businesses in an orderly manner within the existing legal framework.

- License Issuance Rhythm Expectations: The market generally expects that the first batch of licenses will follow a cautious rhythm similar to that of VASP exchange licenses, with only a very limited number (possibly just one or two) of licenses issued by the end of 2025 or early 2026, with subsequent gradual releases based on market development.

4. Strategic Dilemmas Facing the Hong Kong Dollar Stablecoin

- Uncertainty Under Mainland Regulatory Influence: This is the most core dilemma currently. Chinese institutions are an indispensable part of the Hong Kong financial market, and their collective "pause" or "low profile" will undoubtedly affect the market scale, liquidity depth, and application breadth of the Hong Kong dollar stablecoin in its early issuance phase. Hong Kong authorities need to seek a delicate dynamic balance between promoting market openness and responding to mainland regulatory concerns.

- Contradiction Between Development Pace and Global Competition: Compared to the "full warming" of the U.S. market, Hong Kong has adopted a more "restrained and prudent" development pace under mainland influence. While this cautious rhythm helps in risk control, it also exposes Hong Kong to the risk of missing the time window and falling behind competitors in the global financial innovation race.

- Balancing Risks and Dividends: The intervention of mainland regulators effectively forces Chinese institutions to reassess the risk-reward ratio of being "first movers." While early entrants can enjoy the greatest policy dividends and first-mover advantages, they must also bear the highest costs of market and compliance trial and error.

Japanese Yen Stablecoin

The development path of stablecoins in Japan is a carefully designed financial infrastructure innovation driven from the top down by the government, set against its unique macroeconomic background. The core driving force does not come from speculative demand from the public but from the urgent need to address the structural economic dilemmas of "low interest rates, low growth, and deflationary pressures" that the country has long faced. Stablecoins are seen as a policy tool that can enhance financial efficiency, invigorate capital flows, and inject new momentum into the weak domestic payment system and illiquid government bond market.

To this end, the Japanese government has established one of the world's most rigorous regulatory frameworks for stablecoins through a series of legislations, including the "Amendment to the Fund Settlement Act." Its strategic intent is extremely clear: to transform stablecoins from purely "crypto assets" into "financial infrastructure" that serves national strategy.

1. From Theory to Practice: The Launch of the First Compliant Product

Currently, the Japanese stablecoin market has officially transitioned from the "theoretical preparation period" to the "commercial practice period."

- Significant Event: The fintech startup JPYC Inc. has received regulatory approval to issue the first fully compliant yen stablecoin, "JPYC," in the fall of 2025.

- Key Cooperation Model: This issuance reveals the market access model in Japan—"technological innovation by startups (JPYC Inc.) + compliance infrastructure from major platforms (Mitsubishi UFJ Trust Bank's Progmat Coin)." This indicates that regulators are open to innovation, provided that it is anchored within the strong compliance framework of licensed financial institutions.

- Technical Path and Business Ambition: "JPYC" plans to issue on multiple mainstream public chains such as Ethereum and Avalanche, reflecting its pursuit of openness and composability under compliance. Its goal of issuing 1 trillion yen within three years, along with attracting A-round investments from international giants like Circle, demonstrates its strong determination to capture the market.

The positioning of JPYC is not to replace fiat currency but to serve as "on-chain yen," becoming a bridge that seamlessly extends the functions and value of yen into the global digital economy.

2. Core Application Scenarios

- International Remittances and Corporate Settlements: Providing near real-time, low-cost payment solutions for students studying abroad, cross-border e-commerce, and simplifying B2B payment processes and cross-border fund management using smart contracts.

- Building a Local Web3 Ecosystem: As an on-chain "native liquidity carrier" denominated in yen, it provides a stable value medium for Japan's large gaming, NFT, and other Web3 applications, constructing its underlying financial infrastructure.

3. Multi-Layered National Strategic Intent

The launch of the yen stablecoin carries Japan's multi-layered strategic considerations:

- Defensive Strategy: Competing for Digital Currency Sovereignty This is the most core initiative. By launching a compliant yen stablecoin, Japan aims to break the monopoly of dollar stablecoins in the digital world, providing a non-dollar option for Japan's cross-border trade and international settlements, thereby reducing dependence on traditional systems like SWIFT.

- Economic Strategy: Activating the Government Bond Market and Innovating Monetary Policy Tools This is a clever design that achieves "two birds with one stone." By mandating a significant allocation of reserve assets to Japanese government bonds (JGBs), it not only creates a new structural buyer for the long-term demand-deficient bond market, helping to lower the government's financing costs; in the longer term, the central bank may even use adjustments to stablecoin reserve requirements as a new monetary policy tool to regulate market liquidity.

- Development Strategy: Promoting Financial Infrastructure Upgrades The approval of JPYC will act as a "catfish effect" within Japan's conservative financial system, invigorating the innovative vitality of local giants like Sony and Mizuho, modernizing the domestic payment system, and safely connecting Japan's financial system to the global Web3 ecosystem in a highly compliant manner, avoiding falling behind in the next wave of digital finance.

4. Challenges and the Demonstrative Effect of the "Japanese Model"

- Business Model Challenges: In a zero-interest-rate environment, the traditional profit model relying on interest from reserve assets has completely failed. This requires issuers to quickly achieve a massive issuance scale to maintain operations through "thin profit margins and high sales" economies of scale.

- Extreme Risk Control Framework:

- Legal Definition: Strictly defining stablecoins as "electronic payment tools," fundamentally stripping them of their speculative attributes.

- Subject Limitation: Issuers are limited to licensed financial institutions such as banks and trust companies.

- Unique "Asset Sufficiency Clause": Requiring issuers to cover any shortfall with their own capital when reserve assets depreciate. This is a strong constraint not seen in European and American regulations, greatly ensuring the safety of user assets.

- Mandatory Anti-Money Laundering/KYC Reviews.

In summary, the "trust-based," "strongly regulated," and "semi-decentralized" stablecoin model pioneered by Japan achieves extreme safety and compliance. It provides a highly valuable reference for other Asian economies, such as Hong Kong and South Korea, which also prioritize financial stability, and may lead the entire East Asian region to form a new regulatory consensus on "compliant stablecoins."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。