A new generation faces its own business battles, and the next to take the stage is the USDH war.

Author: Tristero Research

Translation: Deep Tide TechFlow

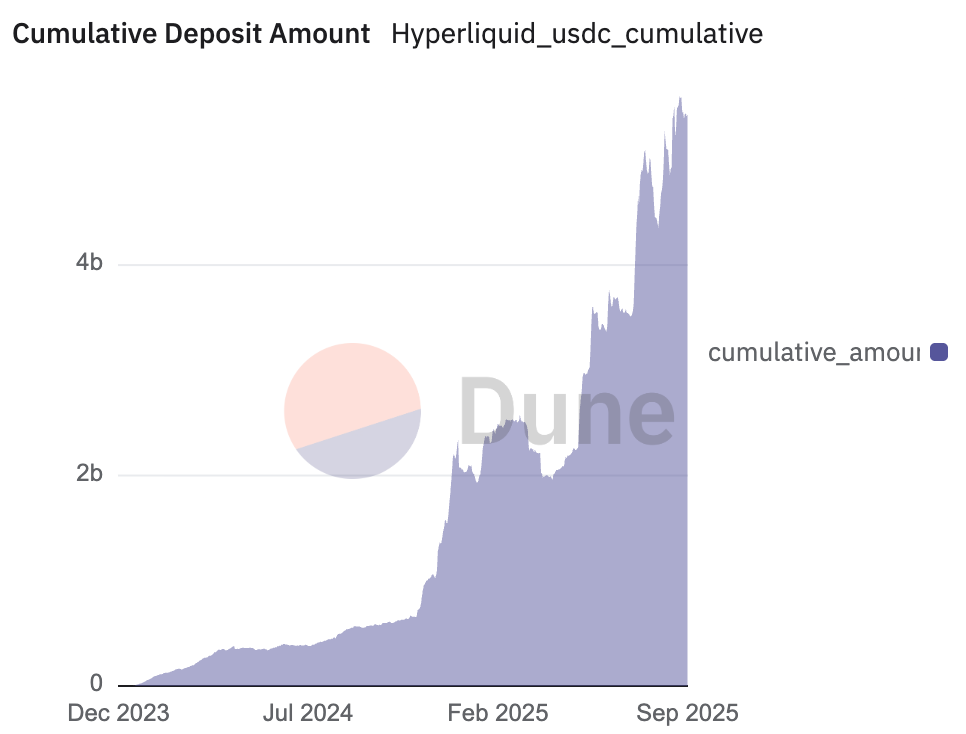

Hyperliquid is one of the fastest-growing perpetual contract exchanges in the DeFi space, with billions of dollars locked in value. With an extremely smooth user experience and a rapidly expanding user base, the exchange has become the dominant platform for on-chain derivatives trading. Currently, its trading engine is powered by over $5.6 billion in stablecoins, the vast majority of which are Circle's USDC.

This capital generates a massive revenue stream through underlying reserves, but currently, these earnings flow to external institutions. Now, the Hyperliquid community is working to reclaim it.

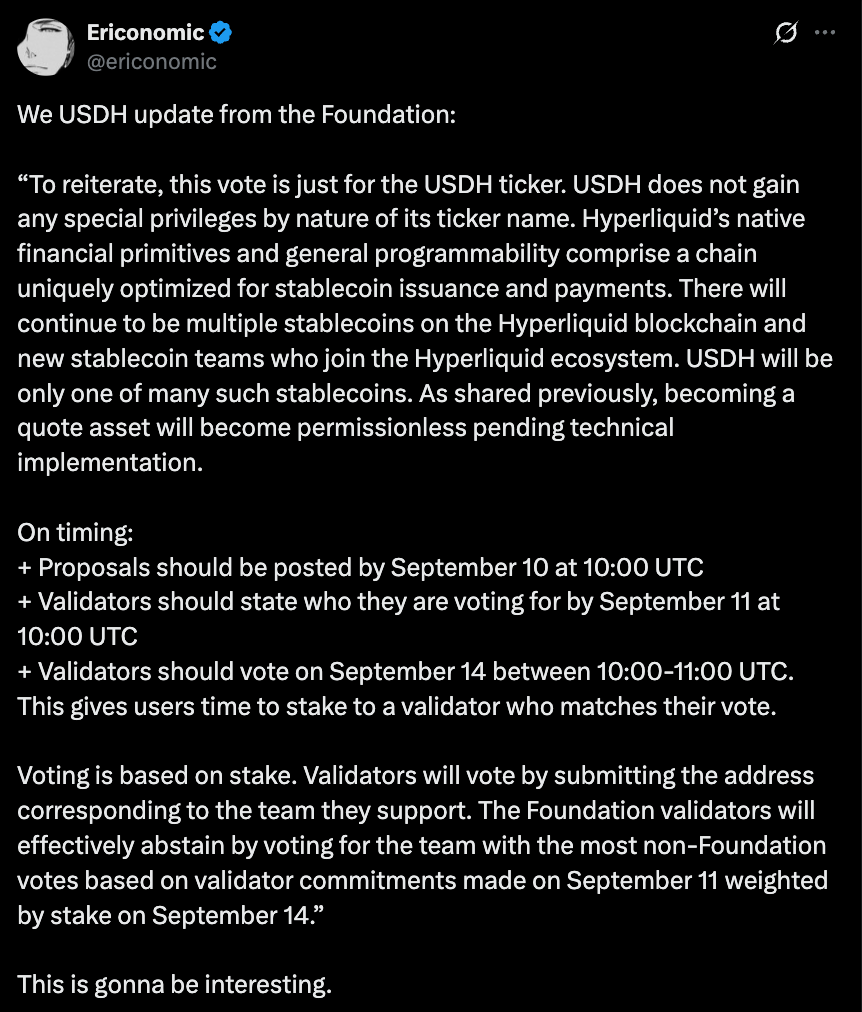

On September 14, Hyperliquid will face a decisive showdown. Its validators will conduct a critical vote to determine who will hold the keys to USDH—this is the platform's first native stablecoin. The significance of this vote goes beyond the ownership of a token; it concerns control over a financial engine that can reintegrate hundreds of millions of dollars in revenue back into the ecosystem. This process is akin to a multi-billion dollar request for quotes (RFQ) or government bond auction, but it will be conducted transparently on-chain. Validators secure the network by staking HYPE and also act as a "recruitment committee," deciding who will mint USDH and how the billions in revenue will be redistributed.

The differences between the candidates are evident—one side is a team of crypto-native developers committed to full alignment, while the other is an institutional financial giant with deep pockets and a mature operational mechanism.

Mature Model: A Potential Opportunity of $220 Million Annually

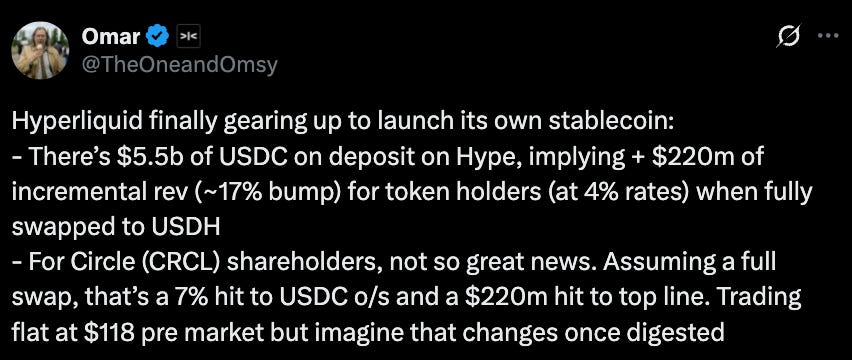

To understand the significance of this competition, one must first look at the flow of funds. Currently, USDC occupies the throne of stablecoins. Its issuer, Circle, quietly accumulates wealth by investing reserve funds in U.S. Treasury bonds and earning returns, having gained $658 million in just one quarter. This is the business model that Hyperliquid plans to emulate.

By replacing third-party stablecoins with the native stablecoin USDH, the platform can avoid value outflow and redirect funds back to itself. Based on existing balances, the reserves of USDH alone could generate $220 million in revenue annually. This marks Hyperliquid's transition from "tenant" to "landlord"—no longer a customer of external stablecoins but possessing its own financial foundation. For Circle, this competition is crucial: losing Hyperliquid's capital reserves could instantly reduce its revenue by up to 10%, exposing its heavy reliance on interest income.

The only question facing the community is not whether to pursue this prize, but whom to trust to achieve it.

However, Circle does not intend to give up its position easily. Before the USDH plan surfaced, Circle had already taken action to solidify its standing in Hyperliquid, announcing the launch of native USDC and CCTP V2 at the end of July. This upgrade promises seamless USDC transfers across supported blockchains, enhancing capital efficiency—without wrapped tokens or traditional cross-chain methods. Circle also introduced its institutional-grade fiat on/off ramp through Circle Mint. The message is clear: as the issuer of USDC, Circle will not easily relinquish Hyperliquid's liquidity to competitors.

Candidates: A Clash of Ideas

Multiple different visions surrounding USDH have emerged, each representing a different strategic path for Hyperliquid.

Hyperliquid Native Team Native Markets quickly joined the race after the USDH announcement, proposing a stablecoin compliant with the GENIUS Act, specifically designed for the platform. Their plan includes integrating fiat gateways to simplify the flow of funds and sharing revenue with the Hyperliquid Assistance Fund. Team members include seasoned professionals like former Uniswap Labs president MC Lader, but some community members have questioned the timing and funding sources of their proposal. The team positions itself as the most localized option—combining compliance, on-chain expertise, and a commitment to returning value to the ecosystem. The advantages are clear: a trustworthy local project promising regulatory compliance and close alignment with $HYPE. The downside is that some community members question whether the timing is right and whether the team has the resources to achieve scalable delivery.

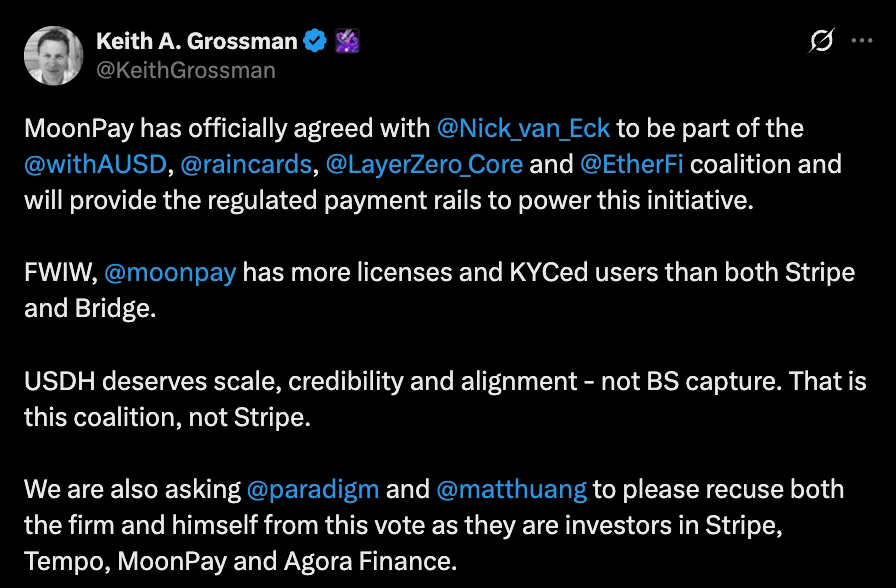

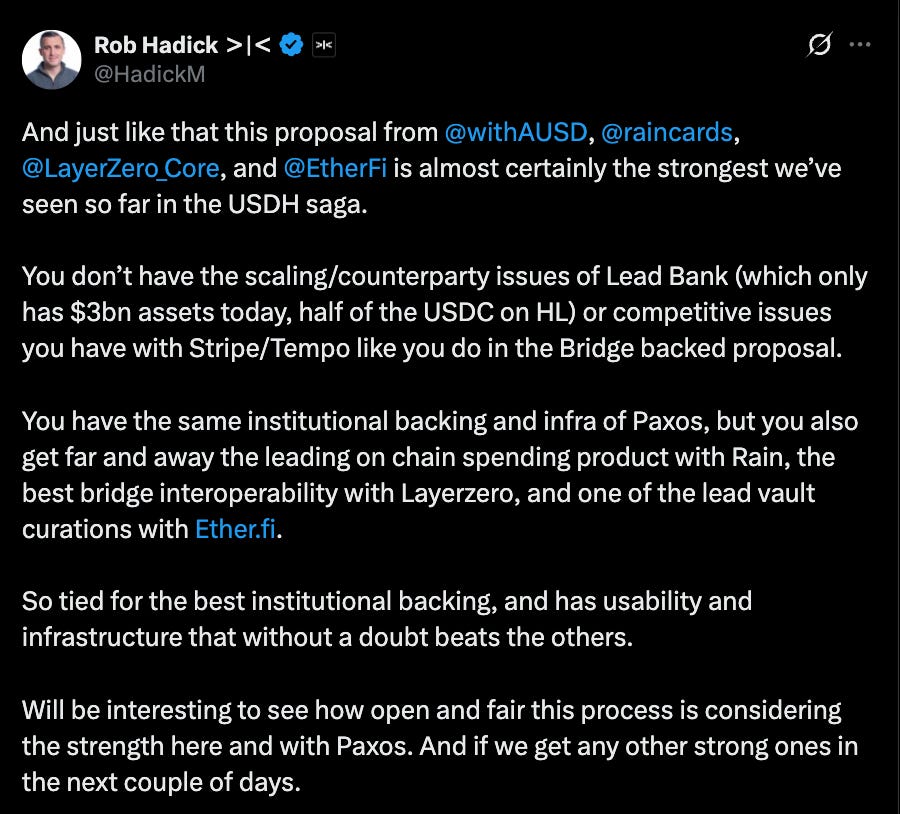

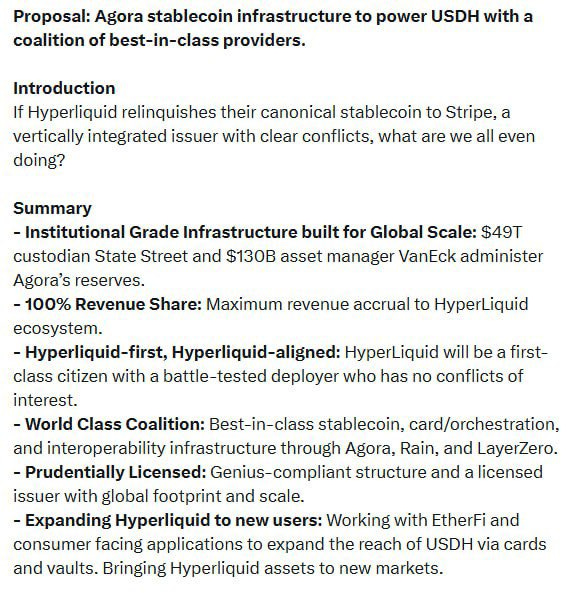

A proposal gaining significant momentum comes from Agora, a stablecoin infrastructure provider, which has formed an alliance with established partners. Agora is supported by MoonPay, a cryptocurrency deposit service provider with a larger number of licensed jurisdictions and KYC users than Stripe;

Rain, which offers seamless on-chain consumption and card services; and LayerZero, which provides optimal cross-chain interoperability.

With recent funding of $50 million led by Paradigm, Agora emphasizes compliance through proof of reserves and positions itself as fully aligned with Hyperliquid's interests. Its reserves will be custodied by State Street, managed by VanEck, and proof of reserves will be provided by Chaos Labs. The team also commits to providing at least $10 million in initial liquidity through partners like Cross River and Customers Bank. Their proposal offers a mature model supported by institutions and makes a core commitment: every dollar of net income from USDH reserves will flow back into the Hyperliquid ecosystem. In practice, this means that the growth of the stablecoin will directly translate into benefits for HYPE holders. Its advantages lie in institutional credibility, capital support, and distribution capabilities. However, reliance on banks and custodians may reintroduce the off-chain bottlenecks that USDH originally sought to avoid.

Stripe has proposed a plan to make USDH a pillar of a global stablecoin payment network by acquiring Bridge for $1.1 billion. Bridge's infrastructure has already enabled businesses to accept and settle stablecoin payments (like USDC) in over 100 countries at low fees and near-instantly, while integration with Stripe brings regulatory credibility, a developer-friendly API stack, and seamless card/payment connections. The company also plans to launch its own fiat-backed stablecoin USDB within the Bridge ecosystem, aiming to avoid external blockchain costs and create a defensive moat. The advantages are clear: Stripe's scale, brand, and distribution capabilities can push USDH into mainstream commercial sectors. However, the risk lies in strategic control: a vertically integrated fintech company with its own public chain (Tempo) and wallet (Privy) may ultimately control the core monetary layer of Hyperliquid.

Other candidates have chosen different paths. Paxos, a regulated trust company based in New York, offers the most conservative option: compliance above all. Paxos commits to using 95% of the interest from USDH reserves directly for HYPE buybacks. Paxos also promises to list HYPE on its supported networks (including PayPal, Venmo, and MercadoLibre)—an institutional distribution channel unmatched by other candidates. Although the regulatory environment in the U.S. has become more favorable under the Trump administration, Paxos remains the preferred choice for those who view durability and regulatory approval as the cornerstones of USDH's long-term legitimacy. Its weakness lies in its complete reliance on fiat custody, facing risks from U.S. banks and regulators—vulnerabilities that previously led to the failure of BUSD.

In contrast, Frax Finance offers a DeFi-native solution. Born from the crypto ecosystem, Frax's proposal prioritizes on-chain mechanisms, deep community governance, and a revenue-sharing strategy that appeals to crypto purists. Their campaign is a bet on a more decentralized, community-centered vision for USDH's future. Its design supports USDH at a 1:1 ratio backed by frxUSD and U.S. Treasury bonds managed by asset giants like BlackRock, allowing seamless conversion to USDC, USDT, frxUSD, and fiat. Frax also commits to distributing 100% of the revenue directly to Hyperliquid users, with governance fully controlled by validators. Its advantages lie in a tested high-yield, community-driven model that aligns closely with crypto ideals; its weaknesses include reliance on frxUSD and off-chain Treasury bonds, which may introduce external risks and limit adoption compared to traditional fiat institutions.

Konelia is a smaller and lesser-known participant in the USDH race, submitting bids through the same on-chain auction process as larger competitors. Its plan emphasizes compliant issuance, reserve management, and ecosystem alignment tailored for Hyperliquid's high-performance Layer 1. Unlike top competitors, this proposal lacks public details and has attracted limited community attention. Although officially recognized as a valid bidder, Konelia is viewed more as a peripheral participant in the race rather than a frontrunner. Its advantages lie in formal qualifications and an L1-customized proposal, but the lack of details, brand recognition, and community support puts it at a disadvantage compared to capital-rich competitors.

Finally, the xDFi team, composed of DeFi veterans from SushiSwap and LayerZero, proposed a fully crypto-collateralized cross-chain stablecoin USDH, covering 23 EVM chains from day one. Backed by assets such as ETH, BTC, USDC, and AVAX, balances will achieve native synchronization across chains through xD infrastructure, avoiding cross-chain and fragmentation issues. The design allocates 69% of the revenue to $HYPE governance, 30% to validators, and 1% for protocol maintenance, making USDH community-owned and free from banks or custodians. Its appeal lies in its censorship-resistant, crypto-pure design, deepening Hyperliquid's role as a liquidity hub; its risk, however, is that stability relies on volatile crypto collateral and lacks regulatory support for mainstream adoption.

Curve takes a different approach, positioning itself as a partner rather than a competitor. Based on its crvUSD LLAMMA mechanism, Curve proposes a dual stablecoin system: a regulated USDH supported by Paxos or Agora, and a decentralized dUSDH supported by HYPE and HLP but operating on Curve's CDP infrastructure, governed by Hyperliquid. This setup can unlock looping, leverage, and yield strategies while creating a powerful flywheel for HYPE and HLP value. Curve points out the resilience and stable peg of crvUSD in volatile markets and offers flexible licensing terms, emphasizing that its CDP model has generated annual revenues of $2.5 million to $10 million at a scale of $100 million. Its advantage lies in a balanced "best of both worlds"—regulatory coverage combined with decentralized options; its disadvantage is that liquidity and brand may suffer from the split between the two tokens, as well as the reflexive risk of using Hyperliquid's own assets as collateral.

Decentralized Authorization

The final decision will be made by Hyperliquid's validators through on-chain voting. To ensure a fair and community-driven outcome, the Hyperliquid Foundation announced it will abstain from voting, a significant move.

By committing to support the majority opinion, the foundation chooses to step back—eliminating concerns about centralization and clearly stating that decision-making is entirely in the hands of stakeholders.

September 14 will not just be a vote—it will be a test of the maturity of DeFi governance, shifting from symbolic fee-switching debates to the awarding of contracts worth billions of dollars determined by community votes.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。