The stock market no longer waits for the bell to ring, and investment no longer requires broker permission.

Written by: 1912212.eth, Foresight News

Investing in U.S. stocks is essentially betting on the fate of the United States. If you had invested $10,000 in the S&P 500 index in 2002, it would have grown to $85,900 now. If that $10,000 had been invested in the Nasdaq index, you might have received a return of $114,900.

As the largest securities market in the world, U.S. stocks rarely disappoint investors. However, there are still too many countries and regions where investors cannot access such assets, missing out on wealth opportunities.

What would happen if purchasing such assets no longer required an account, was not limited by region or trading hours? With just a smartphone and a balance in a crypto wallet, one could buy shares of U.S. giants anytime and anywhere. This is no longer a fictional scenario; it is the reality brought about by the "tokenization of U.S. stocks."

In the next era, the stock market will no longer wait for the bell to ring, and investment will no longer require brokers to place orders.

Tokenization is simply the process of converting real-world assets into programmable, tradable digital tokens. These tokens are based on blockchain technology and typically comply with ERC-20 or similar standards, ensuring transparency and security. Tokenized U.S. Stocks refer to mapping or anchoring the stocks of U.S. listed companies (such as Apple, Tesla, etc.) onto the blockchain in the form of tokens, allowing them to be traded, transferred, and held on-chain like cryptocurrencies.

In short, in the blockchain world, "replicating" a traditional stock turns it into "on-chain assets." For example, a stock worth tens of thousands of dollars can be fragmented into thousands of smaller units, allowing ordinary investors to participate with a low threshold. The advantages of tokenization include 24/7 trading, reduced intermediary costs, and enhanced liquidity, but it also faces regulatory uncertainties and technical risks.

For investors, the threshold for investing in U.S. stocks is lowered after tokenization. For companies, the motivation to explore tokenization stems from multiple factors. The liquidity bottleneck in traditional financial markets is becoming increasingly prominent, especially during non-trading hours. Additionally, institutional investors like BlackRock and JPMorgan are viewing tokenization as a tool to reduce financing costs. The improvement of the regulatory environment provides policy support for this wave.

So why is the wave of tokenization flooding into U.S. stocks?

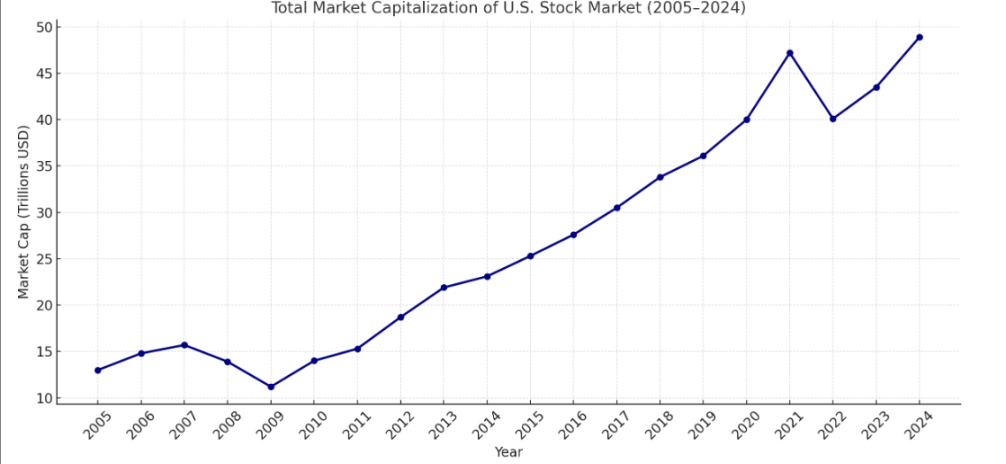

U.S. stocks have unique advantages that other assets do not possess. First, as the largest stock market in the world, the total market capitalization of U.S. stocks is expected to reach between $52 trillion and $59 trillion by 2025, a scale far exceeding that of other countries or regions. The total market capitalization of global stock markets is around $124 trillion, with U.S. stocks accounting for over 40%.

High returns are another key factor; the S&P index recently reached a historic high of $6,336. The average annual return of the S&P 500 index since 1957 is about 10.4% (approximately 6.5% after adjusting for inflation), while the average annual return over the past 20 years has been 10.364%, and over the past 30 years, it has been 9%. The threshold for trading U.S. stocks outside the U.S. is relatively high; traditional investments require opening a brokerage account, meeting minimum investment amounts, adhering to trading hours (only weekdays from 9:30 AM to 4:00 PM Eastern Time), and dealing with cross-border regulatory and tax complexities. This is especially cumbersome and costly for overseas investors.

The Wave of Tokenization

Retail investors are flocking to tokenized U.S. stocks to bypass barriers and wealth effects. But what about institutional actions? Crypto exchanges, on-chain protocols, and internet brokerages are gearing up.

On May 22, cryptocurrency exchange Kraken partnered with Backed Finance to launch a tokenized stock and ETF trading service called "xStocks," covering over 50 U.S. listed stocks and ETFs, including Apple, Tesla, and Nvidia.

Another cryptocurrency exchange, Bybit, has chosen to enter the U.S. stock market in collaboration with Swarm. Notably, Kraken and Bybit do not issue stock tokens themselves but opt to collaborate with other third parties. Those truly issuing stock tokens include Backed Finance and Securitize. The former collaborates with protocols like Uniswap and complies with MiFiD and Swiss DLT regulations to offer freely transferable tokenized stocks that support on-chain trading. Securitize partners with well-known institutions like BlackRock and VanEck to provide end-to-end tokenization services.

However, the most talked-about and high-profile tokenization in the crypto space comes from the blockchain institutional platform Ondo Finance and the well-known U.S. brokerage Robinhood.

Ondo Finance is an institutional-level platform focused on tokenizing traditional financial assets and bringing them onto the blockchain. It is currently the most recognized project among RWA (Real World Asset) projects that have issued tokens, with the most comprehensive product line. Ondo's flagship product, USDY, is a tokenized U.S. Treasury bond, with a total TVL reaching $1.39 billion. However, the market seems to be lukewarm, with its token price declining from $2 to around $0.70, oscillating for a long time.

With the wave of tokenization of U.S. stocks rising, Ondo has become more aggressive. Since early July, it first partnered with Pantera Capital to plan a $250 million investment to promote RWA tokenization, and then on July 4, it acquired the U.S. Securities and Exchange Commission-regulated broker Oasis Pro to obtain a series of licenses for U.S. securities. Ondo also plans to launch tokenized stock trading in the coming months.

In just one month, Ondo has become particularly aggressive on the path of tokenizing U.S. stocks.

On July 10, Ondo acquired Strangelove to accelerate the development of a full-stack RWA platform and recently initiated a global market alliance, collaborating with public chains, DEXs, wallets, data service providers, cross-chain protocols, DeFi, and other products to unify industry standards.

It is foreseeable that after launching tokenized U.S. stocks, Ondo will leverage its strong resource integration capabilities to push its offerings to every corner of the crypto market, making it easy for crypto players to purchase tokenized U.S. stocks.

Robinhood is also personally entering the tokenization of U.S. stocks, becoming the first publicly listed brokerage to take the plunge.

This player, which has disrupted the traditional brokerage industry with a zero-commission trading model, has attracted a large number of young investors, especially millennials, with its low threshold and user-friendly interface, with an average user age of 35. It has 25.8 million funded accounts, holding $221 billion in assets.

In June of this year, Robinhood launched over 200 on-chain stock tokens, even introducing tokenized equity for OpenAI and SpaceX, giving each qualified user €5 in OpenAI tokens.

Robinhood founder Tenev candidly stated the fundamental issue in the private equity market: the best companies have too many options and do not actively consider retail investors, leading to a "reverse selection problem." The key innovation of tokenization is that it "can function without being chosen to join by the tokenized company," which is precisely the breakthrough that Robinhood can promote.

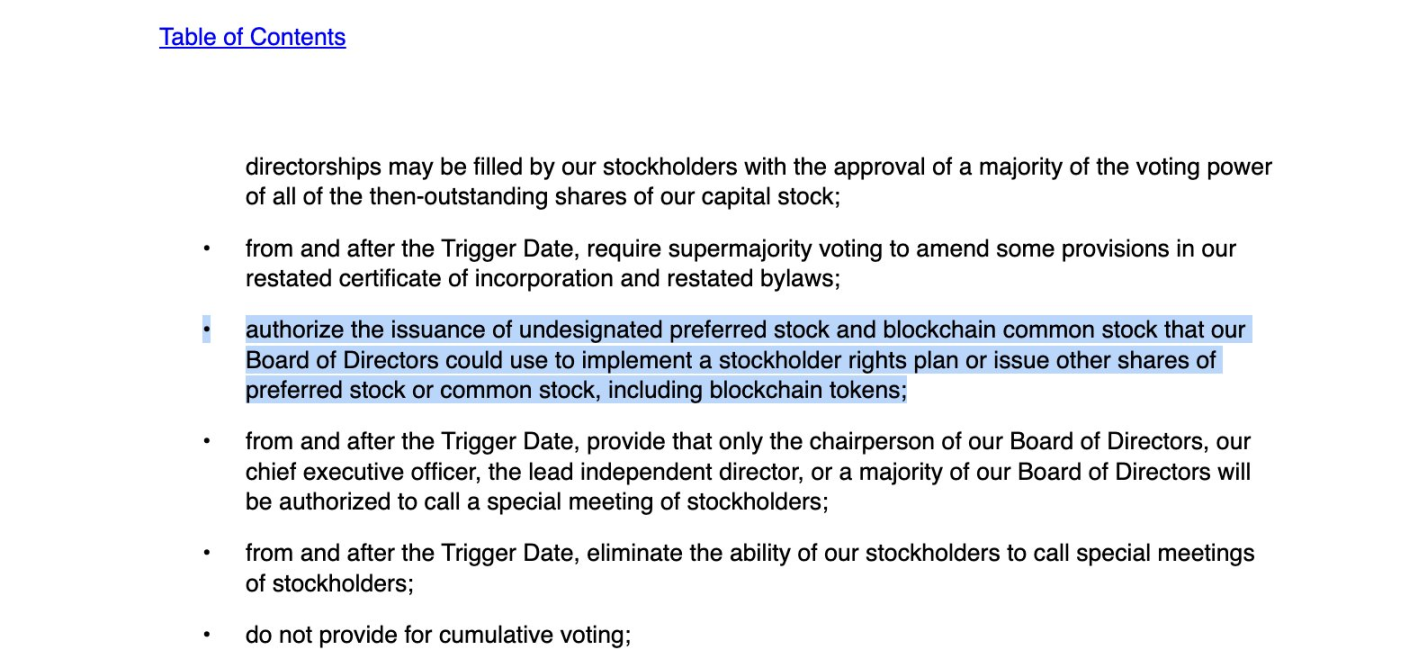

On July 21, the design software giant Figma revised its IPO S-1 filing. In the new document, in addition to confirming the IPO price range, a significant difference from the S-1 submitted earlier in the month is the explicit statement that the company has officially authorized the establishment of a new class of "blockchain common stock." This grants the company's board the power to issue stocks in the form of blockchain tokens in the future. In a sense, institutions can reach potential investors from around the world through a borderless blockchain platform, gaining more potential buyers.

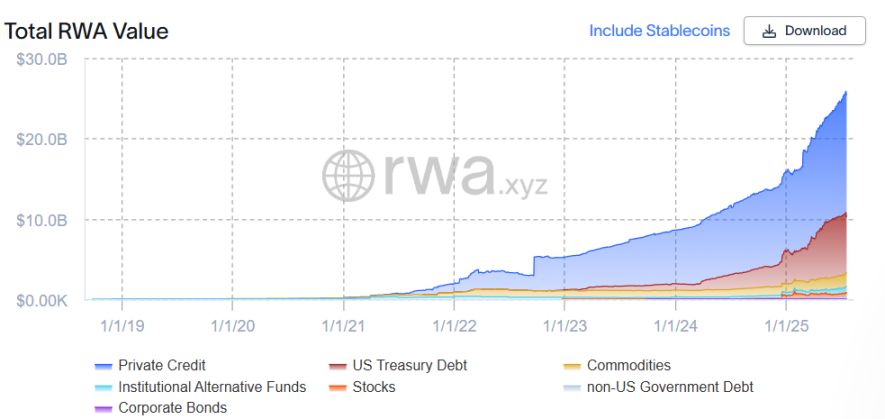

In the first half of 2025, on-chain tokenization of U.S. stocks has shifted from concept to reality. According to data from rwa.xyz, its total TVL has risen to $530 million, with the number of monthly active addresses surging to 70,000.

Tokenization is penetrating from pure crypto into traditional finance: no longer a speculative tool, but a bridge to enhance efficiency.

The Wild Past

The current booming wave of tokenization of U.S. stocks is not a new phenomenon; its past is the price paid for innovation.

The early attempts at tokenizing U.S. stocks can be traced back to the experimental explorations of decentralized protocols in the last cycle. Synthetix was one of the earliest platforms to support synthetic asset trading of U.S. stocks, allowing users to hold tokens like sTSLA and sAAPL on-chain to simulate the price performance of U.S. stocks. However, these assets lacked real stock backing, relying solely on collateral mechanisms and oracle price feeds, leading to weak liquidity and the risk of decoupling. Statistics show that the cumulative trading volume of sTSLA on the Synthetix platform was less than 800 times, and most projects eventually transformed due to regulatory pressure and unsustainable business models.

Although there were no shareholder rights, it opened the door for mapping crypto assets to real assets. This model provided prices through oracles, bypassing traditional custody mechanisms and offering a reference paradigm for subsequent players.

At the same time, centralized exchanges became the main drivers of early tokenization of U.S. stocks. In 2020, FTX partnered with the German licensed broker CM-Equity to launch tokenized stocks for Tesla, Apple, and others, allowing non-U.S. users to trade 24/7, with the tokens backed by real stocks. In 2021, Binance followed suit by launching "stock tokens," allowing users to trade Tesla and other assets with zero commission using USDT.

However, this model is essentially a derivative within CEX, lacking on-chain transparency and compliance backing, which quickly led to warnings from regulatory agencies in multiple countries. FTX's tokenized stock trading volume reached $94 million in the fourth quarter of 2021, but with the platform's bankruptcy in 2022, related services abruptly ceased; Binance also delisted its products after just three months due to regulatory pressure.

The ideal is beautiful, but the reality is harsh. The FTX collapse in 2022 became a watershed moment for the tokenization of U.S. stocks, shifting the market from "wild growth" to "compliance reconstruction."

These cases expose the core contradictions of early tokenization of U.S. stocks: the imbalance among technological feasibility, compliance costs, and market demand. However, these practices laid the groundwork for today's more compliant and structured tokenization attempts, pushing the market to recognize the potential of asset tokenization.

The true on-chain U.S. stock assets were brought back to the agenda after 2022, with the rising popularity of the RWA (Real World Asset) concept. Representative projects like Backed Finance generally adopt relatively friendly jurisdictions such as Switzerland and Liechtenstein, using a "1:1 custody + verifiable reserves + on-chain issuance" approach to map real U.S. stock securities into tokens compliant with standards like ERC-20, which possess stronger compliance and traceability.

In 2024, Exodus Movement became the first publicly listed company in the U.S. to tokenize common stock, issuing the EXOD token through the Algorand blockchain, allowing users to convert on-chain tokens to NYSE shares on a 1:1 basis. This marks a shift in the SEC's attitude towards on-chain stocks, but the tokens only support price tracking and do not include shareholder rights such as voting.

Challenges and Risks

In a field full of opportunities, risks always accompany. The liquidity of on-chain U.S. stocks is a significant challenge.

On July 3, the token tracking Apple, AAPLX, saw its price surge to $236.72, a 12% premium over the stock's trading price at that time. A similar token tracking Amazon soared to $891.58 on July 5, four times the previous day's closing price. An extreme case occurred on the peer-to-peer cryptocurrency trading platform Jupiter. Blockchain data showed that earlier on July 3, an unidentified user attempted to purchase about $500 worth of Amazon token AMZNX, briefly pushing its price up to $23,781.22, over 100 times the previous day's closing price for Amazon.

The "xStocks" issued in collaboration with Backed Finance and Kraken primarily map various stock tracking tokens. However, due to low trading volumes on multiple cryptocurrency exchanges, these tokens can experience severe price fluctuations when users buy or sell beyond the market's capacity. Such volatility may intensify during nighttime and weekends when the stock market is closed.

The liquidity of the market itself, oracle issues, and potential manipulation concerns deter many players from engaging with on-chain U.S. stocks.

Additionally, user rights protection has raised market concerns. After Robinhood announced the launch of OpenAI equity tokens, OpenAI quickly responded on X: "These 'OpenAI tokens' are not OpenAI equity. We have not partnered with Robinhood, nor do we participate or endorse this. Any transfer of equity requires our approval — we have not approved it. Please be cautious."

Elon Musk also mocked: "Your 'equity' is fake." EU regulators, such as the Bank of Lithuania, intervened to investigate, and the SEC warned of potential violations, causing Robinhood's stock price to reverse and decline. Bernstein analysts pointed out that the company is betting on SEC policy support and the passage of the CLARITY Act to open the tokenized asset market.

Amidst the significant controversy, Robinhood founder and CEO Vlad Tenev recently expressed on a program that the reactions from OpenAI and SpaceX are understandable but unfair. He used a vivid analogy: it is like "digital NIMBYism" — in principle, everyone supports tokenization, but when it actually happens to them, the appeal is not as strong. What people really want is not complex financial instruments, but "capital as a service" — press a button, and funds can enter your account, he stated.

Whether potential market demand can support a large-scale on-chain stock market is worth questioning. A seasoned player told Foresight News, "Doing U.S. stocks on-chain is essentially finding U.S. stock investors among crypto players, who are used to 24/7 global trading and the significant volatility of the crypto world. It is worth questioning how many players in this space are actually interested in U.S. stocks."

Moreover, he added, "For non-crypto players, learning to use on-chain wallets to trade U.S. stocks is also a barrier."

Another challenge comes from regulation, as finance is typically a heavily regulated field.

Recently, SEC Chairman Paul Atkins stated that he is considering introducing a cryptocurrency "innovation exemption" policy to encourage the market to advance the tokenization process.

However, this is not a blanket solution.

When Apple stock is "copied" onto the blockchain, who ensures it truly represents shareholder rights? Who is responsible for information disclosure, compliant trading, and anti-money laundering? Under U.S. securities law, any issuance and transfer of securities must be registered or exempted, while the decentralized nature of on-chain assets is fundamentally at odds with traditional compliance logic.

In a recent statement on securities tokenization, the SEC indicated, "Tokenization has the potential to facilitate capital formation and enhance investors' ability to use their assets as collateral. However, despite the significant potential of blockchain technology, it does not possess 'magic' to change the nature of the underlying assets. Tokenized securities remain securities. Therefore, market participants must carefully consider and comply with relevant federal securities laws when trading such instruments."

Once cross-border custody, KYC deficiencies, or liquidity directed towards non-registered platforms are involved, tokenized U.S. stocks are likely to be viewed by the SEC as illegal securities issuance. This is a test for innovators and a blind spot for regulators — they cannot ignore it, yet it is difficult to govern new paradigms with old rules.

Thus, how subsequent tokenization companies and protocols navigate the gray regulatory area while "dancing with shackles" becomes an important issue that must be faced.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。