Author: Cynic, CGV Research

Under the strategic shift of the Trump administration fully embracing crypto assets, the scale of crypto reserves held by publicly listed companies is about to surpass the $100 billion mark. This article systematically outlines the global landscape of corporate crypto reserves, deeply analyzes the capital operation model centered around MicroStrategy, and explores the differentiated paths and potential risks of altcoin reserve companies—this "digital assetization" experiment led by traditional enterprises is reshaping the future paradigm of corporate financial management.

Global Crypto Reserve Enterprises Overview

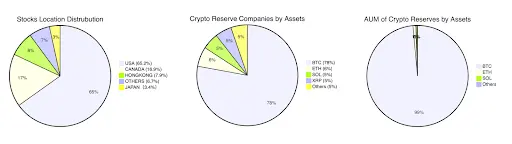

From the distribution of listed companies, U.S. companies account for 65.2%, Canada 16.9%, Hong Kong 7.9%, and Japan has a small number of companies holding reserves (3.4%), while other countries account for 6.7%.

In terms of the types of crypto assets held by listed companies, BTC accounts for 78%, with ETH, SOL, XRP, and others close in proportion, all at around 5%-6%, while companies holding other crypto assets account for the remaining 5%.

In terms of the value of crypto assets held by listed companies, BTC is in an absolute leading position, accounting for 99% of the value, with the remaining assets making up the other 1%.

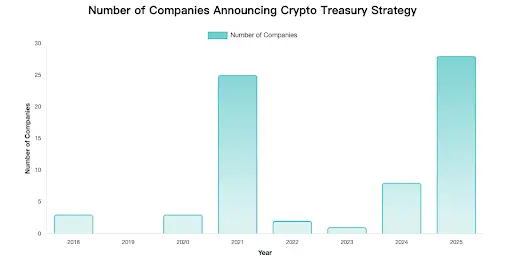

According to the statistical analysis of the time when companies first announced their crypto strategic reserves, the results are shown in the following chart.

Note: Only accurately disclosed partial data is included.

From the chart, we can observe distinct peaks and troughs, which correspond with the bull and bear cycles of the cryptocurrency market itself.

Two Significant Peak Periods:

- 2021: 25 companies announced strategic reserves, mainly driven by the rise in Bitcoin prices and the demonstration effect of MicroStrategy.

- 2025: 28 companies, reaching a historical peak, indicating an increased acceptance of cryptocurrency as a corporate reserve asset.

Characteristics of the Trough Period:

- 2022-2023: Only 3 companies entered the market, reflecting the impact of the bear market in crypto and regulatory uncertainties.

Recently, more companies have been announcing their crypto reserves, and it is expected that the number of publicly listed companies with crypto reserves will exceed 200 this year, with the adoption of cryptocurrencies in traditional industries continuing to rise.

Strategic Reserves, Capital Operations, and Stock Price Performance

From the current capital operation models of various digital asset reserve companies, they can be summarized into the following categories:

- Leverage Hoarding Model: Companies with weaker main businesses raise funds through debt and financing to purchase crypto assets, aiming to increase net assets as crypto assets appreciate, which in turn boosts stock prices and allows for further financing, creating a positive feedback loop. Essentially, this model turns the company's stock into a leveraged spot asset for crypto. If operated properly, it can leverage small costs to synchronize the rise of stock prices and net assets. Typical cases: MicroStrategy ($MSTR BTC reserves), SharpLink Gaming ($SBET ETH reserves), DeFi Development Corp ($DFDV SOL reserves), Nano Labs ($NA BNB reserves), Eyenovia ($EYEN HYPE reserves).

- Cash Management Model: Companies with strong main businesses (unrelated to crypto) use excess cash flow to purchase quality crypto assets for investment returns. This usually does not have a significant impact on stock prices and may even lead to declines due to investor concerns about neglecting the main business. Typical cases: Tesla ($TSLA BTC reserves), Boyaa Interactive (HK0403 BTC reserves), Meitu (HK1357 BTC + ETH reserves).

- Business Reserve Model: Companies whose main business is related to crypto engage in direct or indirect reserve activities. For example, exchange businesses require reserves, and mining companies retain mined Bitcoin as reserves to mitigate potential business risks. Typical cases: Coinbase ($COIN various crypto asset reserves), Marathon Digital ($MARA BTC reserves).

| Company (Market) | Reserve Currency | Holding Size | Stock Price Impact | Capital Operation Model |

|------------------|------------------|--------------|--------------------|-------------------------|

| MicroStrategy (US) | BTC | 592,345 BTC (approx. $63.4 billion) | Stock price rose over 3000% after announcement, latest purchase caused stock price to fluctuate 2-3% | Leverage Hoarding |

| Marathon Digital (US) | BTC | 49,179 BTC (approx. $5.3 billion) | Stock price fluctuated significantly after announcement | Business Operation |

| Metaplanet (JP) | BTC | 12,345 BTC (approx. $1.3 billion) | Stock price fell 0.94% after latest purchase, overall strategy received positive feedback | Leverage Hoarding |

| Tesla (US) | BTC | 11,509 BTC (approx. $1.2 billion) | Stock price surged after purchase in 2021, holding steady with relatively stable stock price | Cash Management |

| Coinbase Global (US) | BTC, ETH, etc. | 9,267 BTC (approx. $99 million)

115,700 ETH (approx. $28 million) | As an exchange, stock price impact is relatively small | Business Operation |

| SharpLink Gaming (US) | ETH | 188,478 ETH (approx. $47 million) | After rising more than tenfold, single-day drop of 70% | Leverage Hoarding |

| DeFi Development Corp (US) | SOL | 609,190 SOL (approx. $10.7 million) | Since announcement, stock price rose as much as 6000%, with a 70% pullback from the peak | Leverage Hoarding |

| Trident Digital (SG) | XRP | Announced plan to raise $500 million to purchase XRP on June 12, 2025 | Significant fluctuations on the day, ultimately closed down 3% | Leverage Hoarding |

| Nano Labs (US) | BNB | Target reserve of $1 billion in BNB | Stock price doubled after announcement, reaching a two-year high | Leverage Hoarding |

| Eyenovia→Hyperion DeFi (US) | HYPE | Target of 1 million HYPE (approx. $5 million) | Stock price rose 134% on the day, continuing to hit new highs, with an increase of over 380% since the announcement | Leverage Hoarding |

| Meitu (HK) | Bitcoin + Ethereum | Fully liquidated (originally held 940 BTC + 31,000 ETH) | Stock price surged 4% after selling all crypto assets for a profit of $80 million at the end of 2024 | Cash Management |

Among many enterprises, MicroStrategy has flexibly utilized leverage, transforming from a software service provider with years of losses into a Bitcoin whale with a market value of hundreds of billions, making its operation model worthy of in-depth study.

MicroStrategy: A Textbook on Crypto Reserve Leverage Operations

Five Years of Thirtyfold Increase: Bitcoin Leverage Proxy

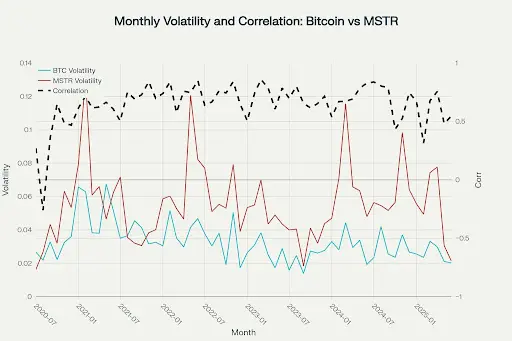

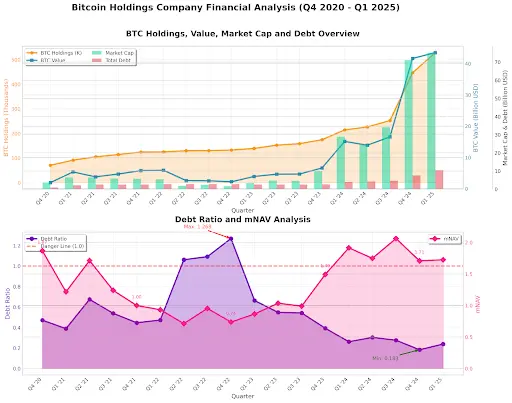

Since MicroStrategy announced its Bitcoin strategic reserve in 2020, its stock price has shown a high correlation with Bitcoin prices, and its volatility is much higher than that of Bitcoin itself, as can be intuitively seen from the chart below. From August 2020 to now, MSTR has increased nearly 30 times, while Bitcoin's price has only increased tenfold during the same period.

By comparing the volatility and correlation of Bitcoin and MSTR on a monthly basis, it can be seen that most of the time, MSTR's price correlation with Bitcoin is in the range of 0.6-0.8, showing a strong correlation; at the same time, MSTR's volatility is several times higher than that of Bitcoin. As a result, MSTR can be considered a leveraged security for Bitcoin. On the other hand, MSTR's Bitcoin leverage attribute can also be verified: In June 2025, MSTR's one-month call option implied volatility was 110%, 40 percentage points higher than Bitcoin's spot, indicating that the market assigns it a leverage premium.

A Precision Capital Operation Machine

The core of the MicroStrategy model is to obtain funds for purchasing Bitcoin at a lower financing cost. As long as the expected return on Bitcoin is higher than the actual financing cost, the model can continue to exist.

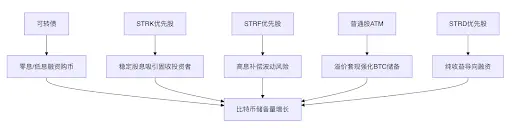

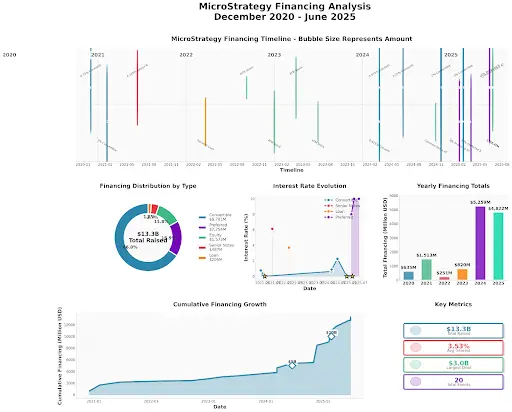

MicroStrategy has created a matrix of capital tools that transforms Bitcoin's volatility into structured financing advantages, employing various financing strategies to form a self-reinforcing capital cycle. VanEck analysts have described it as a "pioneering experiment combining digital currency economics with traditional corporate finance."

The core objectives of MicroStrategy's capital operations are twofold: controlling the debt ratio and increasing the number of BTC per share. Assuming BTC rises in the long term, achieving these two core objectives will also increase the value of MicroStrategy's stock.

For MicroStrategy, collateralized lending has hidden costs and limitations, such as insufficient capital efficiency (requiring a 150% over-collateralization rate), uncontrollable liquidation risks, and limitations on the scale of financing.

Compared to collateralized lending, financing methods such as convertible bonds and preferred stocks with implicit options can further reduce costs and have a smaller impact on the asset-liability structure. Selling ATM common stock can also quickly and flexibly raise cash. Preferred stocks, in terms of accounting treatment, are recorded as equity rather than debt, which can further reduce the debt ratio compared to convertible bonds.

| Tool Type | Mechanism | Investor | Company | Risk Characteristics | |-----------|-----------|----------|---------|----------------------| | Convertible Bonds | Under specific conditions, bonds can be converted into common stock at a predetermined conversion ratio, allowing participation in equity appreciation; if conversion conditions are not met, holders can receive interest and principal repayment according to bond terms | Low-risk Bitcoin call options | Low-cost financing, optimizing capital structure after conversion | High-priority repayment + conversion gains | | ATM Common Stock | A mechanism for gradually publicly selling common stock at market prices through registered securities dealer agreements; there is no minimum fundraising requirement, and the company can decide the timing, scale, and price of issuance based on funding needs and market conditions; funds from stock sales are directly included in the company's books without the need for a custody or trust account | Maximum Bitcoin exposure | Highly flexible financing channel | Full exposure to BTC volatility | | STRK | Annual interest of 8.00%, cumulative, with a liquidation priority of $100 per share, can be converted into common stock at an initial conversion rate of 0.10 times on any trading day | Stable dividends + call options + hedging tools | | |

Flexible dividend payments, supporting cash common stock mixed payments, tax-deductible

Dividends + conversion rights protection

STRF

Annual interest of 10.00%, similar to cumulative preferred stock, unpaid dividends will compound; in case of significant changes (such as mergers, sales), the company can be requested to repurchase shares at face value; no conversion rights

Fixed income + hedging

Flexible dividend payments, tax-deductible

High-interest compensation for volatility risk

STRK

Annual interest of 10.00%, but non-cumulative, paid in cash; in case of significant changes, the company can be requested to repurchase shares at the original selling price ($100); no conversion rights

Fixed income + hedging tools

Flexible dividend payments, tax-deductible

Pure dividend cash flow

This complex matrix of capital tools is favored by professional investors, allowing them to arbitrage differences in actual volatility, implied volatility, and other components of option pricing models, which also establishes a loyal buying base for MicroStrategy's financing tools.

By combining quarterly Bitcoin holdings with liabilities and significant capital operation events, we can observe:

Through the combination of various financing tools, MicroStrategy issues convertible bonds and preferred stocks in a bull market with high Bitcoin volatility and positive stock premiums to expand Bitcoin holdings, while in a bear market with low Bitcoin volatility and negative stock premiums, it sells common stock via ATM to prevent excessive debt ratios from triggering a chain liquidation risk.

During high premium periods, convertible bonds and preferred stocks are prioritized for the following reasons:

- Dilution Delay Effect: Directly issuing common stock (ATM) will immediately dilute existing shareholders' equity. In contrast, convertible bonds and preferred stocks embed conversion options, delaying equity dilution to the future.

- Tax Efficiency Structure: Preferred stock dividends can deduct 30% of taxable income, reducing the effective cost of the 8% dividend rate STRK to 5.6%, lower than the 7.2% interest rate of comparable corporate bonds. Common stock financing does not generate tax deduction benefits.

- Avoiding Reflexivity Risk: Large-scale ATM is seen as a signal that management believes the stock price is overvalued, which may trigger programmatic sell-offs.

- Debt Ratio* = Total Liabilities ÷ Total BTC Value Held

- mNAV = Market Capitalization ÷ Total BTC Value Held

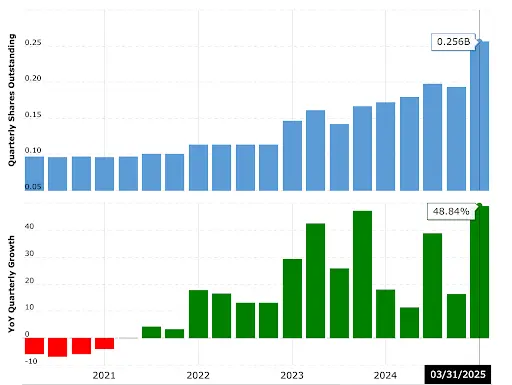

Due to its unique financing structure, when Bitcoin rises, MSTR increases at a higher rate, and a large amount of debt will be converted into equity. In fact, since MicroStrategy announced its Bitcoin purchases, its total equity has risen from 100M to 256M, an increase of 156%.

Will a large amount of equity issuance dilute shareholders' rights? From the data, since Q4 2020, MicroStrategy's equity has increased by 156%, yet the stock price has increased by only 30 times, indicating that shareholder equity has not been diluted but significantly enhanced. To better represent shareholder equity, MicroStrategy proposed the metric of BTC per Share, with the goal of continuously increasing BTC per Share through capital operations. From the chart, it can be seen that in the long term, BTC per Share has consistently been on an upward trend, rising tenfold from the initial 0.0002 BTC per Share.

Mathematically, when MSTR's stock price has a high positive premium over Bitcoin (mNAV>1), potential equity dilution financing to purchase Bitcoin can continuously push up BTC per Share. mNAV > 1 means that the funds raised per share can purchase more BTC than the current BTC per Share, and although the original shares are diluted, the BTC value contained in each share is still increasing.

Future Projections for MicroStrategy

I believe the key factors for the success of the MicroStrategy model are threefold: regulatory arbitrage, correct bets on Bitcoin appreciation, and excellent capital operation capabilities. At the same time, risks are also hidden within.

Legal and Regulatory Changes

- The Richness of Bitcoin Investment Tools Squeezes MicroStrategy's Buying Power: When MicroStrategy first announced its Bitcoin strategic reserve, Bitcoin spot ETFs had not yet been approved, and many investment institutions could not directly obtain Bitcoin risk exposure within a compliant framework, so they purchased through MicroStrategy as a proxy asset. However, after Trump took office, the government strongly promoted cryptocurrencies, and a large number of compliant crypto-related investment tools have emerged, gradually narrowing the space for regulatory arbitrage.

- SEC Restrictions on Excessive Debt for "Non-Productive Assets": Although MicroStrategy has maintained a controllable debt ratio through precise debt management, its current debt rate is significantly lower than that of many publicly listed companies of similar market value. However, the debt of publicly listed companies is usually used for business expansion, while MicroStrategy's debt is entirely for investment, which may lead the SEC to reclassify it as an investment company, raising its capital adequacy requirements by over 30%, thus compressing leverage space.

- Capital Gains Tax: If unrealized capital gains on company-held assets are taxed, MicroStrategy will face significant cash tax pressures. (The current OBBB bill stipulates that taxes are only levied upon sale.)

Bitcoin Market Dependency Risks

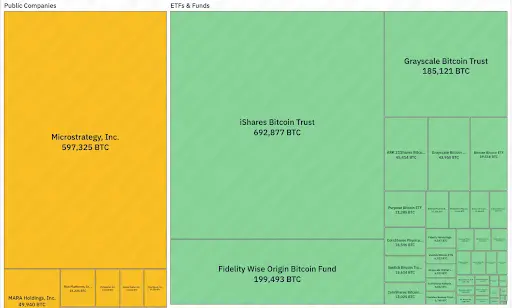

- Volatility Amplifier: MicroStrategy currently holds 2.84% of the total Bitcoin supply, and when Bitcoin volatility rises, the volatility of MicroStrategy's stock price will also increase several times compared to Bitcoin volatility, putting significant pressure on stock prices during downturns.

- Irrational Premium: MicroStrategy's market value has long been at a premium of over 70% to the net value of its Bitcoin holdings, with most of this premium stemming from the market's irrational expectations of Bitcoin appreciation.

Debt Leverage's Ponzi-like Structural Risks

- Reliance on Convertible Bond Circular Financing: The cycle of "borrowing new debt → purchasing BTC → pushing up stock price → issuing more debt" exhibits dual Ponzi characteristics. When large bonds mature, if Bitcoin prices do not continue to rise to support stock prices, the issuance of new debt will be hindered, triggering a liquidity crisis (debt rollover risk); if BTC prices fall, causing stock prices to drop below the convertible bond conversion threshold, the company will be forced to repay in cash (conversion price inversion).

- Lack of Stable Cash Flow: Since the company does not have a stable cash flow source and cannot sell Bitcoin, MicroStrategy's debt repayment methods are primarily through equity issuance (debt-to-equity swaps, ATM). When stock prices or Bitcoin prices fall, financing costs significantly increase, which may lead to the risk of financing channels closing or substantial dilution, making it difficult to continue increasing holdings or maintain operational cash flow.

In the long run, when entering a downturn cycle for risk assets, multiple overlapping risks may trigger a chain reaction, forming a technical risk transmission mechanism that leads to a death spiral:

Another possibility is proactive regulatory intervention, converting MicroStrategy into a Bitcoin ETF or similar financial product. If MicroStrategy's current holding of 2.88% of the total Bitcoin supply were to face a sell-off liquidation wave, it could directly lead to a collapse of the crypto market; converting to an ETF or similar type would be much safer. Although MicroStrategy holds a large amount of Bitcoin, it is not particularly outstanding when compared to ETFs. Additionally, on July 2, 2025, the SEC approved the conversion of the Grayscale Digital Large Cap Fund into an ETF holding a combination of assets such as BTC, ETH, XRP, SOL, and ADA, indicating the possibility.

Altcoin Reserve Experiment: Taking $SBET and $DFDV as Examples

Valuation Regression Analysis: From Sentiment-Driven to Fundamental Pricing

The Volatility Path and Stabilization Signals of $SBET

Causes of Wild Fluctuations: In May 2025, $SBET announced a PIPE financing of $425 million to acquire 176,271 ETH (valued at $463 million at the time), becoming the largest publicly listed holder of ETH globally, with the stock price soaring 400% in a single day. Subsequently, SEC filings revealed that PIPE investors could resell their shares, triggering panic selling in the market over dilution, causing the stock price to plummet 70%. Ethereum co-founder Joseph Lubin (Chairman of the $SBET Board) clarified that there was "no shareholder selling," but market sentiment had already been damaged.

Signs of Valuation Recovery:

As of July 2025, the $SBET stock price stabilized around $10, with an mNAV of approximately 1.2 (about 2.67 after accounting for PIPE issuance).

The stabilization momentum comes from:

- Appreciation of ETH Holdings: An additional purchase of $30.6 million for 12,207 ETH, bringing total holdings to 188,478 ETH (approximately $47 million), accounting for 80% of market capitalization.

- Realization of Staking Rewards: Earned 120 ETH through liquid staking derivatives (LSD);

- Improved Liquidity: Average daily trading volume of 12.6 million shares, with short interest dropping to 8.53%.

The Ecological Integration Premium of $DFDV

Compared to $SBET, although $DFDV's volatility is also very high, its stock price has stronger support against declines. Despite experiencing a single-day drop of 36%, $DFDV still has a 30-fold stock price gain since its transformation. This is partly due to the company's low market value before the transformation and partly because of its business diversity, especially its investments in infrastructure, which provide more valuation support.

Valuation Support from SOL Reserves:

$DFDV holds 621,313 SOL (approximately $10.7 million), with three sources of income:

- SOL Price Appreciation (accounting for 90% of holding value);

- Staking Rewards (annualized 5%-7%);

- Validator Commissions (charged to ecological projects like $BONK).

PoW vs. PoS: The Impact of Staking Returns

The annualized returns from native staking of PoS cryptocurrencies like ETH and SOL may not directly affect valuation models, but liquid staking is expected to enhance the flexibility of capital operations.

- Bitcoin, as a PoW token, does not have an interest mechanism, but its total supply is fixed, and the inflation rate continues to decline (currently at 1.8%), giving the asset scarcity. PoS tokens can earn returns through staking, and when the staking return rate exceeds the token's inflation rate, the staked assets gain nominal appreciation. Currently, SOL staking annualized returns are 7%-13%, with an inflation rate of 5%; ETH staking annualized returns are 3%-5%, with an inflation rate of less than 1%. The current ETH/SOL staking can generate additional returns, but attention should be paid to the changes in inflation rates and staking returns.

- The returns generated from staking are coin-based and cannot be converted into purchasing power in the secondary market to drive further price increases.

- Liquid staking allows for earning staking returns while also utilizing liquid assets for DeFi activities, such as collateralized lending, enhancing the flexibility of capital operations. (For example, $DFDV has issued its own liquid asset DFDVSOL)

The Success Factors of $MSTR in the Applicability Verification of Altcoin Reserve Companies

Regulatory Arbitrage: Shrinking Space

Recently, the approval speed for ETF applications has noticeably accelerated, with multiple institutions applying for ETFs related to different cryptocurrencies, making approval just a matter of time. Before more complex financial instruments targeting specific cryptocurrencies emerge, the stocks and bond tools of altcoin reserve companies can still meet some investors' needs, but the space for regulatory arbitrage is gradually narrowing.

Tokens

30-Day Volatility

Institutional Holding Ratio

ETF Catalysis Progress

BTC

45%

63%

Approved spot ETF

ETH

68%

28%

Approved

SOL

82%

12%

Multiple applications pending approval

Betting on Token Price Increases: Doubts About Altcoin Future Performance

Bitcoin, as "digital gold," possesses global liquidity consensus, while ETH/SOL lacks equivalent status. BTC has reserve asset properties, but ETH/SOL are mostly viewed as utility assets.

During the period of 2024-2025, altcoins are expected to perform poorly relative to Bitcoin:

- Bitcoin's dominance is expected to continue rising in 2024, reaching around 65%.

- Historically, altcoin seasons usually begin after Bitcoin peaks, but in this cycle, altcoins have lagged behind.

When Bitcoin reached new highs in this cycle, ETH and SOL were still below 50% of their historical highs.

Capital Operation Capability: Upgraded Flexibility

Compared to Bitcoin's strategic reserves, altcoin strategic reserve companies can participate more deeply in public chain ecosystem businesses to generate cash income while leveraging DeFi to improve capital utilization.

For example:

- $SBET is chaired by the founder of Consensys, with future prospects for expanding cash flow businesses such as wallets, public chains, and staking services.

- $DFDV, in collaboration with Solana's largest meme coin $BONK, acquired a validator network, with commission income accounting for 34% of Q2 revenue.

- $DFDV packages staking returns into DeFi tradable assets through dfdvSOL, attracting on-chain capital.

- $HYPD (formerly Eyenovia $EYEN) uses its reserve $HYPE for staking and lending, while expanding node operations and referral commission businesses.

- $BTCS (Ethereum node and staking service provider) uses $ETH for staking and obtains low-cost funding through AAVE by using LST and BTC as collateral.

In summary, the shrinking space for regulatory arbitrage and the uncertainty of token price increases will force altcoin reserve companies to innovate their operational models, deeply engage in on-chain ecosystems, and build cash flow through ecosystem businesses to enhance risk resistance.

As MicroStrategy uses sophisticated capital tools to convert Bitcoin into "volatility leverage," altcoin reserve companies are attempting to solve valuation dilemmas through DeFi operations. However, the contraction of the regulatory arbitrage window, differences in token consensus strength, and inflation concerns of the PoS mechanism make this experiment still full of variables. It is foreseeable that as more traditional enterprises enter the market, the strategic reserve of crypto assets will shift from aggressive betting to rational allocation—its ultimate significance may not lie in short-term arbitrage but in promoting the entry of corporate balance sheets into the programmable era.

As Michael Saylor said, "We are not buying Bitcoin; we are building a financial system for the digital age." The ultimate test of this experiment will be whether the balance sheet can withstand dual pressures when Bitcoin enters a bear market—this is also a question that traditional enterprises must answer before entering the market.

Disclaimer: This article is a CGV research report and does not constitute any investment advice, for reference only.

CGV (Cryptogram Venture) is a crypto investment institution headquartered in Tokyo, Japan. Since 2017, its funds and predecessor funds have cumulatively participated in investments in over 200 projects. Since 2022, CGV has invested in and incubated the licensed yen stablecoin JPYW, positioning itself early in the crypto stablecoin field. Starting in 2024, CGV is entering the coin-stock and RWA markets, participating in projects like Nabito (NA) and Victory Securities (8540.HK) for private placements. Currently, CGV also has branches in Hong Kong, Silicon Valley, and other locations.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。