Despite the large market space for tokenized US stocks, there are currently not many investment options available for investors.

Written by: Lawrence Lee, Mint Ventures

Recently, there have been many developments in the field of tokenized US stocks:

Centralized exchange Kraken announced the launch of its tokenized stock trading platform xStocks.

Centralized exchange Coinbase announced it is seeking regulatory approval for its tokenized stock trading.

Public blockchain Solana submitted a framework for blockchain-based tokenized US stock products.

US-based public blockchains and exchanges are accelerating the process of tokenizing US stocks. Coupled with the recent excitement following Circle's listing, one cannot help but feel optimistic about the prospects of tokenized US stocks.

In fact, the value proposition of tokenized US stocks is very clear:

Expands the trading market size: Provides a 24/7, borderless, permissionless trading venue for US stock trading, which is currently not possible with Nasdaq or the New York Stock Exchange (although Nasdaq is applying for 24-hour trading, it is expected to be realized by the second half of 2026).

Superior composability: By integrating with existing DeFi infrastructure, US stock assets can be used as collateral, margin, and to build indices and fund products, leading to many currently unimaginable use cases.

The demands from both supply and demand sides are also clear:

Supply side (US-listed companies): Reach potential investors from around the world through a borderless blockchain platform, gaining more potential buyers.

Demand side (investors): Many investors who previously could not trade US stocks directly for various reasons can now allocate and speculate on US stock assets directly through blockchain.

Quoted from “US Stocks on the Chain and STO: An Unseen Narrative”

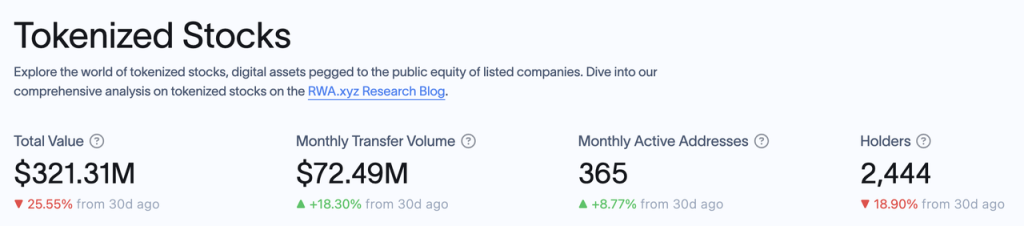

In this round of lenient crypto regulatory cycles, progress is highly likely. According to data from RWA.xyz, the current market capitalization of tokenized stocks is only $321 million, with 2,444 addresses holding tokenized stocks.

The huge market space and the currently limited asset scale form a stark contrast.

In this article, we will introduce and analyze the current players in the tokenized US stock market and the product solutions of other players promoting tokenized US stocks, as well as list potential investment targets under this concept.

This article reflects the author's thoughts as of the time of publication, which may change in the future. The views expressed are highly subjective and may contain errors in facts, data, or reasoning. All opinions in this article are not investment advice, and criticism and further discussion from peers and readers are welcome.

According to data from RWA.xyz, the current tokenized stock market has the following projects based on issuance scale:

We will introduce the business models of Exodus, Backed Finance, and Dinari one by one (Montis Group focuses on European stocks, and SwarmX's business is similar to Backed Finance but on a smaller scale), as well as the progress of several other important players currently promoting tokenized US stock business.

Exodus

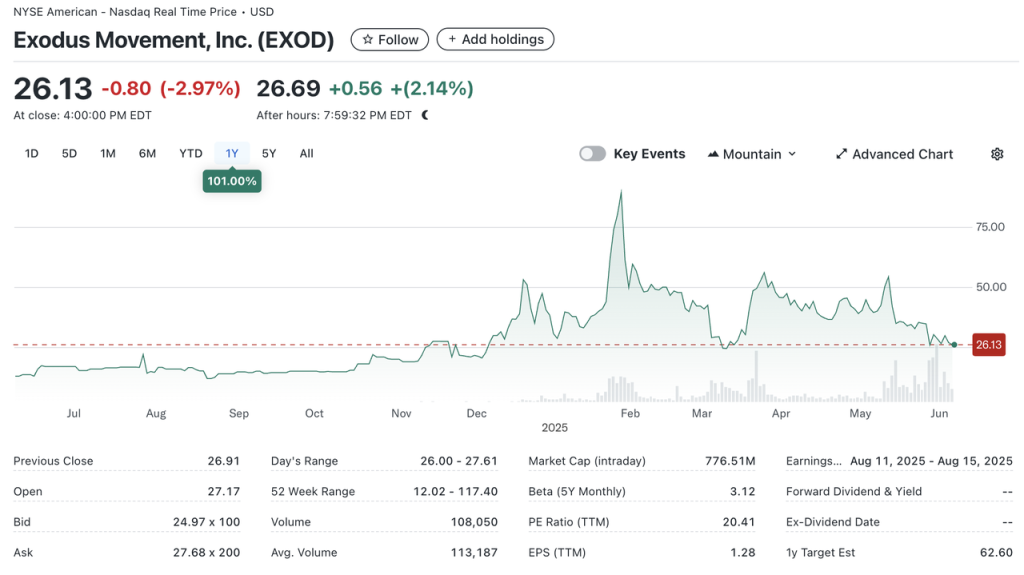

Exodus (NYSE.EXOD) is a US company primarily focused on developing non-custodial crypto wallets, with its stock listed on the New York Stock Exchange (NYSE.EXOD). In addition to its own branded wallet, Exodus has previously collaborated with the NFT market MagicEden to launch a wallet.

As early as 2021, Exodus allowed users to migrate their common stock to the Algorand chain through Securitize, but the tokens migrated to the chain could not be traded or transferred on-chain and did not include governance rights or other economic rights (such as dividends). The Exodus token is more like a "digital twin" of real shares, with its symbolic significance on-chain being greater than its actual significance.

Currently, EXOD has a market capitalization of $770 million, with approximately $240 million on-chain.

Exodus is the first stock approved by the SEC to tokenize its common stock (or more accurately, Exodus is the first stock approved by the SEC to be listed on NYSE as a tokenizable stock). However, this process was not smooth; the listing of Exodus stock was delayed from May 2024 until it officially went live on NYSE in December.

However, the tokenization of Exodus's stock is only for its own stock, and the tokenized stock cannot be traded, which is of little significance to us web3 investors.

Dinari

Dinari is a US-registered company founded in 2021, focusing on stock tokenization within the US compliance framework. In 2023, it completed a $10 million seed round of financing and a $12.7 million Series A round in 2024, with investors including Hack VC, Blockchange Ventures, Coinbase CTO Balaji Srinivasan, F Prime Capital, VanEck Ventures, and Blizzard (Avalanche Fund). Among them, F Prime is a fund under asset management giant Fidelity, and the investments from Fidelity and VanEck also demonstrate traditional asset management institutions' recognition of the tokenized US stock market.

Dinari only supports non-US users, and the process for trading US stocks is as follows:

User completes KYC.

User selects the US stocks they wish to purchase and pays with USD+ issued by Dinari (a stablecoin backed by short-term government bonds issued by Dinari, which can be exchanged for USDC).

Dinari submits the order to a partnered brokerage (Alpaca Securities or Interactive Brokers), and after the brokerage completes the order, the shares are held in a custodian bank, and Dinari mints corresponding dShares for the user.

Currently, Dinari operates on Arbitrum, Base, and the Ethereum mainnet, with all dShares corresponding 1:1 to real-world equity. Users can view their dShares corresponding to equity on Dinari's official website, and Dinari can also distribute dividends or conduct stock splits for users holding its dShares.

However, dShares cannot be traded on-chain; to sell dShares, users can only trade through Dinari's official website, with the actual trading process being the reverse of the purchase process. dShares trading must also adhere to US trading hours, and trading cannot occur outside of these hours. In terms of product form, in addition to direct stock trading, they also provide stock trading APIs that can collaborate with other trading frontends.

In fact, Dinari's business process, i.e., "KYC -> payment exchange -> compliant brokerage clearing and settlement," is consistent with the mainstream way for non-US users to participate in US stock trading. The main difference is that the asset categories users pay with are Hong Kong dollars, euros, etc., while Dinari accepts crypto assets, with the rest executed entirely under the SEC's regulatory framework.

As a company primarily focused on tokenizing US stocks, Dinari's decision to register in the US (most other projects are registered in Europe) shows its confidence in its compliance capabilities. Their tokenized US stock product officially launched in 2023, and at that time, even the former SEC chairman Gary Gensler, known for his strict stance on crypto regulation, could not find fault with their business model. After the new SEC chairman Paul Atkins took office, the SEC specifically met with Dinari, requesting Dinari to demonstrate its system and answer related questions, indicating that their product is impeccable in terms of compliance and that the team has strong resources in compliance.

However, since Dinari's tokenized US stocks do not support on-chain trading, cryptocurrencies for Dinari are merely an entry and payment method. Functionally, Dinari's products are not much different from those of Futu, Robinhood, and others. For their target users, the product experience of Dinari does not have an advantage over competitors. For a user in Hong Kong, the experience of trading US stocks on Dinari is no better than trading US stocks on Futu, and they cannot use margin trading or other trading functions, and may even have to pay higher fees.

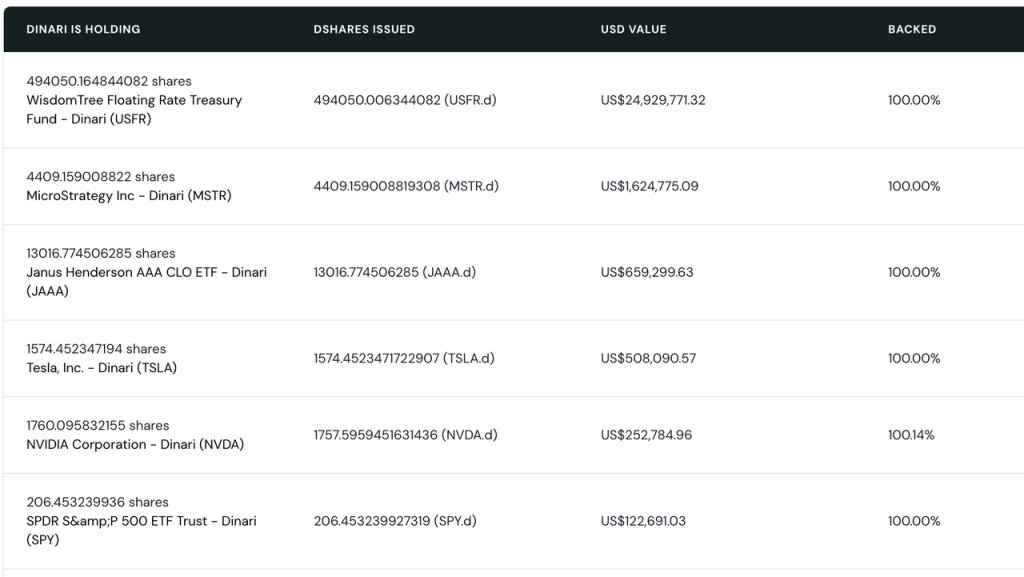

Perhaps due to this, Dinari's tokenized stock market size has remained small, with only MSTR having a market capitalization exceeding $1 million among tokenized stocks, and only five tokenized stocks exceeding $100,000. Currently, most of its total value locked (TVL) comes from its floating-rate government bond products.

Current market capitalization of Dinari's tokenized stocks.

Overall, Dinari's tokenized stock business model has received regulatory certification, but strict compliance has also led to its tokenized stocks being unable to trade or stake on-chain, losing composability, making the experience of holding its dShares less appealing than traditional brokerages, and the product is not very attractive to mainstream web3 users.

Among the current market players, a similar project to Dinari is the community project of the meme coin Stonks, mystonks.org. According to the reserve report disclosed by the project team, their US stock account currently has a market value exceeding $50 million, and user trading is more active than Dinari.

However, mystonks.org's compliance structure has flaws, such as the qualifications of its securities custody account not being clearly stated, and users being unable to verify the reserve report, etc.

Backed Finance

Backed Finance is a Swiss company, also established in 2021, with its products launched in early 2023. In 2024, it completed a $9.5 million financing round led by Gnosis, with participation from Cyber Fund, Blockchain Founders Fund, Blue Bay Capital, and others.

Like Dinari, Backed does not provide services for US users. Its business process is as follows:

The issuer (professional investors) completes KYC certification and review on Backed Finance.

The issuer selects the US stocks they wish to purchase and pays with stablecoins.

Backed Finance submits the order to a partnered brokerage to complete the stock purchase, then Backed Finance mints the corresponding bSTOCK token for the issuer.

Both bSTOCK and its wrapped version wbSTOCK can be freely traded on-chain (the wrapping is mainly for handling stock dividends, etc.), and retail investors can directly purchase bSTOCK or wbSTOCK on-chain.

It can be seen that, unlike Dinari where retail users directly purchase US stocks, Backed Finance currently has professional investors buy US stocks and then transfer them to retail users. This significantly improves overall operational efficiency and allows for 24/7 trading. Another important difference is that the bSTOCK token issued by Backed is an unrestricted ERC-20 token, allowing users to create liquidity pools (LP) for other users to purchase.

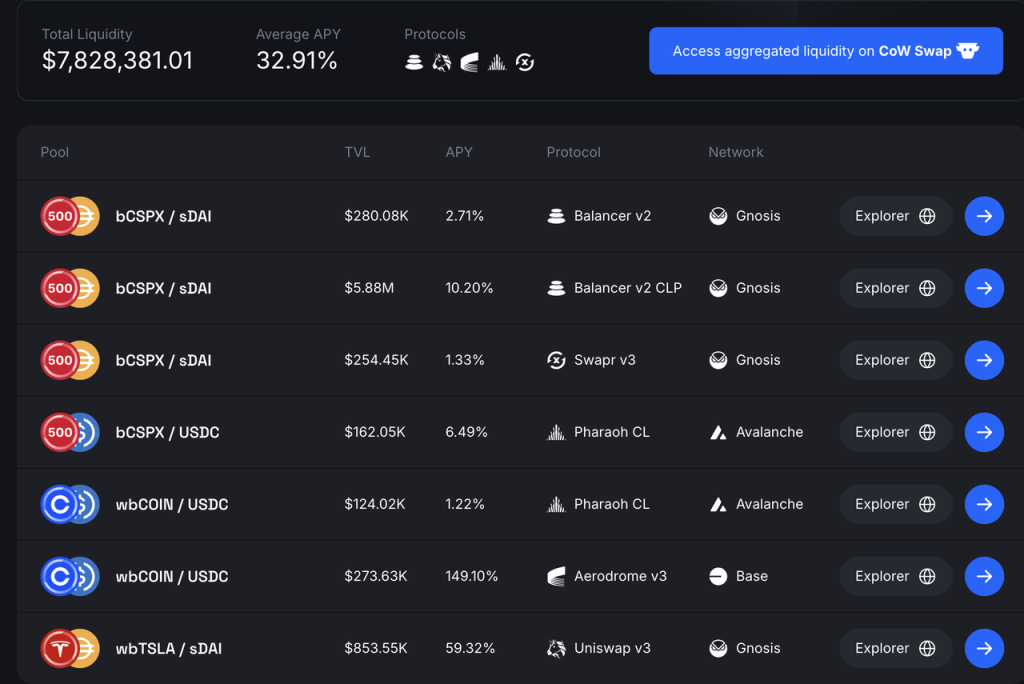

Liquidity of Backed tokenized stocks.

The on-chain liquidity of Backed Finance mainly comes from the SPX index, Coinbase, and Tesla, with users pairing bSTOCK tokens with stablecoins to enter AMM pools. Currently, the total TVL of the liquidity pool is close to $8 million, with an average APY of 32.91%. Liquidity is distributed across Gnosis's Balancer and Swapr, Base's Aerodrome, and Avalanche's Pharaoh, with the bCOIN-USDC pool achieving an APY of 149%.

It is worth noting that Backed Finance imposes no restrictions on the on-chain trading functionality of its bSTOCK tokens, providing users with a second path to hold their bSTOCK, namely:

On-chain users (no KYC required) can directly purchase bSTOCK using stablecoins like USDC or sDAI.

This effectively breaks through the KYC limitations, and the trading experience is no different from trading ordinary on-chain tokens, making it easier to promote among web3 users. An unrestricted ERC-20 token also opens the door to composability for tokenized stockholders, such as pairing with stablecoins to achieve an average APY of 33%. This may also be the reason why Backed Finance's TVL is nearly ten times that of Dinari.

In terms of compliance, the entity behind Backed Finance is registered in Switzerland, and the aforementioned business model of "tokenized stocks corresponding to ERC-20 tokens can be freely transferred" has been recognized by European regulatory authorities (source). Backed Finance has also published reserve proof audited by The Network Firm.

However, the SEC in the US has not yet commented on Backed Finance's business. While it is good that the securities traded by Backed are US stocks and have received permission from Switzerland, it is more important how US regulatory authorities evaluate this business model.

Among other projects, SwarmX has a business model similar to Backed Finance, but it has significant gaps in business scale and compliance details compared to Backed Finance.

Although the market capitalization of Backed Finance's tokenized stocks is ten times that of Dinari, the asset scale of over $20 million and $8 million in TVL is still not high, and on-chain trading is not very active. The reasons are:

There are not enough use cases for tokenized stocks on-chain; currently, they can only serve as LPs, and the advantages of composability have not been fully realized. This may be related to concerns about the legality of such models in associated lending, stablecoin, and other protocols.

More importantly, there is insufficient liquidity. Backed itself is not an exchange and does not have "natural" liquidity to support its tokenized stock trading. Under the current model, the liquidity of its tokenized stocks relies on the issuers, including how many tokenized stocks the issuers are willing to hold and how much liquidity they are willing to add to the LP. Currently, Backed's issuers do not seem willing to increase their investment in this area.

If the SEC can further clarify the regulatory framework and determine the feasibility of the Backed model, the above two points may improve.

xStocks

In May of this year, US exchange Kraken announced a collaboration with Backed Finance and Solana to launch xStocks.

On June 30, the xStocks product was officially launched. Its partners include not only Backed, Kraken, and Solana, but also centralized exchanges Kraken and Bybit, decentralized exchanges on Solana such as Raydium and Jupiter, lending protocol Kamino, Bybit's incubated Dex Byreal, oracle Chainlink, payment protocol Alchemy Pay, and brokerage Alpaca.

Source: xStocks official website.

The legal structure of the xStocks product is completely consistent with Backed Finance, and it currently supports over 200 stock products, with Kraken's trading hours being 5*24. From the perspective of partnerships, Kraken, Bybit, Jupiter, Raydium, and Byreal are all exchanges supporting xStocks; Kamino can use xStocks as collateral, and Kamino Swap can also facilitate xStocks trading; Solana is the public blockchain on which xStocks operates; Chainlink is responsible for reserve reporting; and Alpaca is the partnered brokerage.

Currently, since the product has just launched, various data statistics are not yet complete, and trading volume is also low. However, compared to Backed Finance's own products, xStocks has more key partners:

In the centralized exchange space, there are Kraken and Bybit, which are more likely to leverage existing market makers and users to provide better liquidity for xStocks.

On-chain, there are various DEXs and Kamino, which for the first time provide use cases for tokenized US stocks beyond just being LPs. Other protocols may also support xStocks in the future, further expanding its composability.

From this perspective, although xStocks has just launched, I believe it will quickly surpass existing players and become the largest issuer of tokenized US stocks.

Robinhood

Robinhood, which has been actively expanding into crypto business, also submitted a report to the SEC in April 2025, hoping the SEC would establish a regulatory framework for RWA that includes tokenized stocks. In May, Bloomberg reported that Robinhood would create a blockchain platform to allow European investors to invest in US stocks, with Arbitrum or Solana as alternative public blockchains.

On June 30, Robinhood officially announced the launch of a tokenized US stock trading product for European investors, which supports dividend distribution and has 5*24 access time.

Robinhood's tokenized stock product was initially issued on Arbitrum. In the future, its tokenized stock infrastructure will operate on Robinhood's own L2, which is also based on Arbitrum.

However, according to Robinhood's official documentation, its current tokenized stock product is not a true tokenized stock but rather a contract that tracks the corresponding US stock price, with the related assets securely held by a US-licensed institution in a Robinhood Europe account. Robinhood Europe issues the contracts and records them on the blockchain. Its tokenized stocks can currently only be traded on Robinhood and cannot be transferred.

Other Players in the Space

In addition to the products mentioned above that have specific business operations launched, there are many other players actively working on tokenized US stock business, including:

Solana

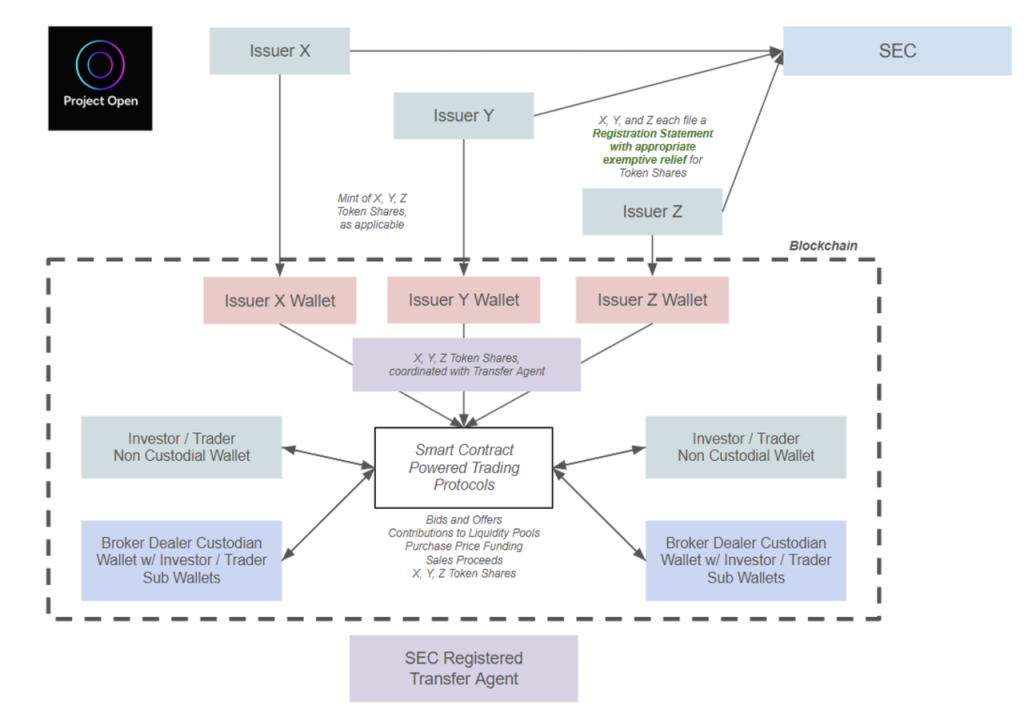

Solana places great importance on tokenized stocks. In addition to the aforementioned xStocks, Solana has also established the Solana Policy Institute (SPI), "aimed at educating policymakers on why decentralized networks like Solana are the future infrastructure of the digital economy." Currently, two projects are being promoted: one is the establishment of a project called Project Open, "aimed at achieving compliant blockchain-based securities issuance and trading, utilizing blockchain technology to create more efficient, transparent, and accessible capital markets while maintaining strong investor protections." Members of Project Open include SPI, DEX Orca on the Solana chain, RWA service provider Superstate, and law firm Lowenstein Sandler LLP.

Project Open began submitting public written opinions to the SEC's crypto working group multiple times in April of this year, and the SEC's crypto working group met with them on June 12 to discuss. After the meeting, Project Open members submitted further explanations of their business.

The tokenized US stock issuance and trading process advocated by Project Open is as follows:

The process is summarized as follows:

Issuers need to apply for SEC approval in advance; once approved, they can issue tokenized US stocks.

Users wishing to purchase tokenized US stocks must complete KYC in advance; after completion, they can use cryptocurrency to buy the tokenized US stocks issued by the issuer.

A transfer agent registered with the SEC records the flow of shares on-chain.

Project Open also specifically proposes that the SEC allow peer-to-peer trading of tokenized US stocks through smart contract protocols, meaning that holders of tokenized US stocks can trade within AMMs, thus opening the door to on-chain composability. However, according to the framework proposed in the document, all users holding tokenized US stock shares must complete KYC. To implement the above process, Project Open is seeking an 18-month exemption relief or confirmatory guidance for various operations (for details, see the reference materials).

Overall, Project Open's proposal supplements the existing Backed Finance scheme with KYC requirements. From my perspective, this proposal is almost certain to pass under the current SEC, which is relatively tolerant of DeFi; the only question is the timing of its approval.

Coinbase

As early as 2020, when Coinbase applied for a listing on Nasdaq, its application documents included the idea of issuing tokenized COIN on-chain, but it was abandoned due to not meeting the SEC's requirements at the time. Recently, Coinbase is seeking a no-action letter or exemptive relief from the SEC to launch its tokenized stock business. However, there are currently no detailed documents available, and we can only confirm from press releases that:

Coinbase's tokenized stock trading plan is open to US users.

This is a major distinction from other current players in the tokenized stock market, allowing Coinbase to compete directly with internet brokerages like Robinhood and traditional brokerages like Charles Schwab. Of course, this has far less impact on web3 investors than on Nasdaq:COIN.

Ondo

Ondo, which has already achieved results in the treasury-type RWA market (see Mint Ventures' previous article about Ondo), has also long planned to engage in tokenized US stock business. According to their documentation, their tokenized US stock product has the following characteristics:

Open to non-US users.

Trading hours are 24/7.

Tokens are minted and burned in real-time.

Allows the use of tokenized US stock assets as collateral.

From the above characteristics, Ondo's product is quite similar to the new framework proposed by Solana. Ondo also announced at Solana's Accelerate conference that it plans to launch a tokenized US stock product on the Solana network.

Ondo's tokenized US stock product, Ondo Global Markets, is scheduled to launch later this year.

This summarizes the current state of the tokenized US stock market and the situation of several other players that are actively working in this space.

From the fundamental motivation of demand, the main purpose for users to purchase tokenized stocks is to profit from stock price fluctuations, focusing on the liquidity of trading venues, redemption capabilities, and whether transactions can be conducted without KYC. Whether a compliant institution is necessary for tokenization is not a concern for users, which is why there has always been a way to provide US stock trading products through derivatives in the web3 market.

Providing US Stock Trading through Derivatives

Currently, the main providers of US stock derivatives services are Gains Network (on Arbitrum and Polygon) and Helix (on Injective). Their users do not actually trade US stocks, so there is no need to tokenize US stocks.

The core product logic is essentially applying perpetual contract logic to US stocks, typically as follows:

Trading users do not need KYC, using stablecoins as collateral, allowing for leveraged trading.

Trading hours are the same as US stock trading hours.

The underlying price is directly sourced from trusted data sources, such as Chainlink.

Funding rates are used to balance the price difference between on-exchange prices and fair prices.

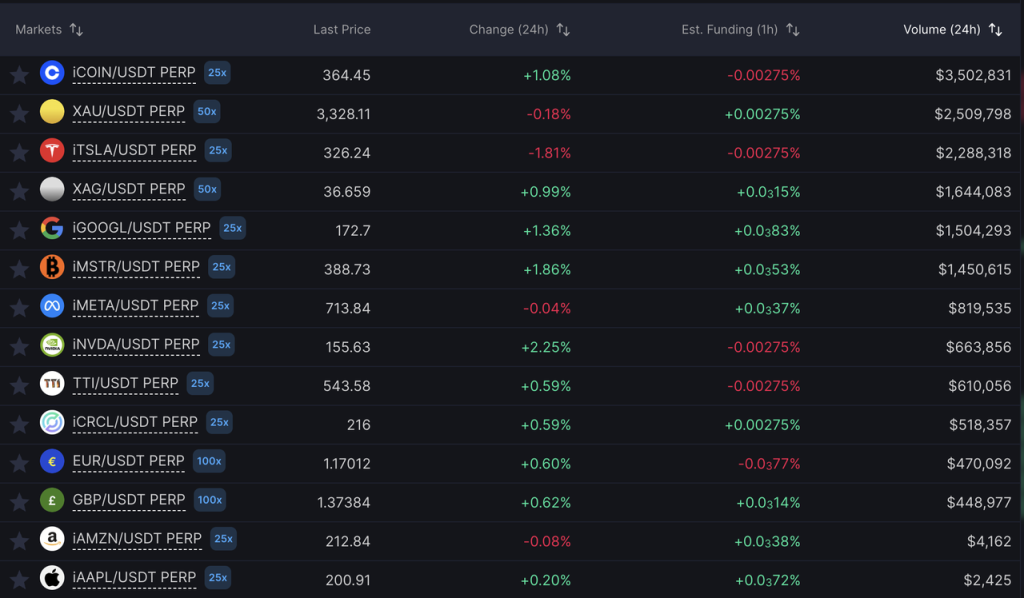

However, whether it is the current Gains and Helix or the previous Synthetix and Mirror, platforms that trade US stocks in the form of synthetic assets have not generated significant trading volume. Currently, Helix's US stock product has an average daily trading volume of no more than $10 million, while Gains' daily trading volume is less than $2 million. The reasons may include:

This form presents obvious regulatory risks because, although they do not actually provide trading of US stocks, they effectively become the exchange for users to trade US stocks. Regulatory authorities have clear requirements for any exchange, and KYC is the most fundamental part of regulation. Such platforms may escape regulatory scrutiny when their volume is low, but if their volume increases, they can easily attract regulatory attention.

The aforementioned products do not have sufficient liquidity to support users' actual trading needs. The liquidity of these products relies on their own on-exchange solutions and cannot depend on any third party, and these products cannot provide users with truly usable trading depth.

Trading volume of Helix's US stock & forex products and the order book of COIN, which has the highest trading volume.

On the centralized exchange side, Bybit recently launched a US stock trading platform based on MT5, which also uses a similar perpetual contract product logic, not conducting actual trading of US stocks but trading indices with stablecoins as collateral.

In addition, the yet-to-launch Shift project has introduced the concept of Asset-Referenced Tokens (ART), which reportedly can enable US stock trading without KYC. The product process is as follows:

Shift purchases US stocks and collateralizes them with compliant brokerages like Interactive Brokers, using Chainlink for reserve proof.

Shift issues reference asset tokens ART based on the reserved US stocks, with each ART backed by corresponding US stock assets, but ART is not a tokenized US stock.

End users do not need KYC to purchase ART tokens.

Shift's plan maintains a 100% correspondence between ART and the underlying US stocks, but ART is not a tokenized US stock and does not confer ownership, dividend rights, or voting rights, thus making it exempt from various regulatory rules regarding securities, allowing for the KYC-free feature (source).

Of course, from a regulatory perspective, ART cannot be pegged to securities-type assets. It is currently unclear how the Shift team plans to specifically implement "pegging ART to US stocks," and it is uncertain whether the specific product plan will truly follow the above process. However, this plan achieves KYC-free US stock trading through certain loopholes in regulatory provisions and is worth ongoing attention.

What Kind of Tokenized US Stock Products Does the Market Need?

Regardless of the method of tokenizing US stocks, the core processes are as follows:

Tokenization: This process is usually handled by compliant institutions, which regularly provide reserve proof, essentially allowing KYC-compliant users to purchase US stocks before they are put on-chain. This step does not differ much among various schemes.

Trading: End users trade the tokenized stocks. The differences among various schemes mainly lie here: some do not allow trading (Exodus), some only allow trading through traditional brokerage channels (Dinari and mystonks.org), while others support on-chain trading (Backed Finance, Solana, Ondo, Kraken). Notably, Backed Finance currently supports KYC-free users to directly purchase its tokenized US stock products through AMMs under the Swiss compliance framework.

For end users, the main concerns in the tokenization process are compliance and asset security. Currently, most market players can ensure these two points well. The main focus is on the trading process. For example, if Dinari can only trade through traditional brokerage channels and does not provide liquidity mining, lending, or other services for tokenized stocks, then the significance of tokenization is largely diminished. Even if compliance is perfect and the process is well-established, it is difficult to attract users.

In contrast, the schemes of xStocks, Backed Finance, and Solana represent more meaningful long-term tokenized US stock solutions. After tokenization, US stocks are traded not through traditional brokerage channels but on-chain, which can more effectively leverage the 24/7 availability and composability advantages brought by DeFi.

However, in the short term, on-chain liquidity will be difficult to match the liquidity of traditional channels. Low liquidity exchanges are essentially unusable; if the venues providing tokenized US stocks cannot attract more liquidity, the influence of tokenized US stocks will also be hard to expand. This is why I believe xStocks can quickly become a leader in tokenized US stocks.

From this perspective, if the regulatory framework gradually clarifies and tokenized US stock products truly gain popularity in web3, the exchanges that ultimately capture more market share may still be those with better liquidity and more trader users.

In fact, from the few examples in the last cycle, we can see that Synthetix, Mirror, and Gains all launched products including US stock trading in 2020, but the most influential US stock trading product was FTX. FTX's scheme is actually quite similar to the current Backed Finance scheme, but FTX's stock trading volume and AUM far exceed those of the later entrant, Backed Finance.

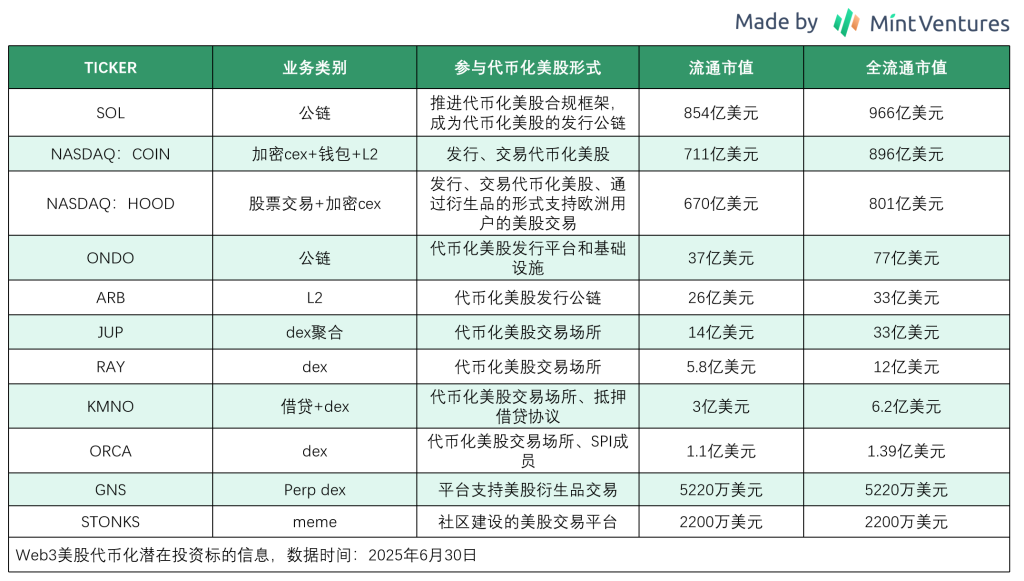

Potential Investment Targets

Despite the large market space for tokenized US stocks, there are currently not many investment targets available for investors to choose from.

Among the existing players, neither Dinari nor Backed Finance has issued tokens, and Dinari has explicitly stated that it will not issue tokens. The only potential investment target could be the Meme token stonks corresponding to mystonks.org.

Among the actively engaged players, the market capitalization of tokens from Coinbase, Solana, and Ondo is already relatively high, and their main business is not tokenized US stocks. The advancement of tokenized US stocks has some impact on their tokens, but the extent of this impact is difficult to predict.

xStocks' partners include leading Dex Raydium and Jupiter from Solana, as well as the lending protocol Kamino, but this collaboration is unlikely to significantly enhance the aforementioned protocols.

In the SPI's Project Open team, Phantom and Superstate have not yet issued tokens, while only Orca has issued a token.

In the derivatives projects, Helix has not issued a token, and only GNS is an optional target.

Due to the different business categories of the above projects, the forms of participation in tokenized US stocks also vary, making it impossible to conduct a valuation comparison. Below is a list of the basic information of the relevant tokens:

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。