In-depth exploration of the reasons behind the rise of PayFi, an overview of the current state of its industry, and key case studies, as well as the potential application scenarios.

Written by: Kedar@Foresight Ventures, Alice@Foresight Ventures

Contributor: Max Hamilton @Foresight Ventures

PayFi: The Transformative Force in Financial Transactions

In today's world, cross-border payments often take days, and businesses face transaction fees that can reach billions of dollars. PayFi has emerged as an innovative solution that combines the advantages of decentralized finance (DeFi) with the immediacy of modern payment systems, promising to reshape the future landscape of transactions.

As the global financial landscape continues to evolve, PayFi is emerging at the intersection of blockchain technology and payment systems, aiming to combine the efficiency of DeFi with the immediacy and convenience of modern payment solutions to transform the way transactions are conducted. This article will delve into the reasons behind the rise of PayFi, provide an overview of its industry, list key case studies, and explore its potential application scenarios.

I. The Birth Background and Advantages of PayFi

(1) Bridging the Gap Between DeFi and Payments

The traditional financial system has long suffered from inefficiencies in settlement, such as lengthy settlement times, high transaction costs, and limited accessibility, which were starkly revealed during the 2008 financial crisis. Although DeFi has introduced innovative financial services through decentralized platforms, it lacks the real-time processing capabilities needed for everyday transactions.

PayFi leverages blockchain technology to achieve real-time settlement of transactions. Based on the theory of the time value of money (TVM), which states that disposable currency today is more valuable than an equivalent amount of currency in the future due to its potential earning capacity, PayFi maximizes financial efficiency through instant, secure, and low-cost transactions.

(2) Unique Advantages of PayFi

Real-time settlement: Transactions are completed instantly, eliminating delays associated with traditional banking systems.

Security and reliability: The immutable ledger feature of blockchain ensures transaction security and transparency, providing assurance to users.

Cost reduction: By removing intermediaries, transaction fees are significantly reduced, saving users money.

Global reach: Its decentralized platform reaches markets that traditional financial services have not adequately covered, including unbanked populations, achieving financial inclusivity.

Innovative products: It gives rise to novel financial service models such as "buy now, pay never," and provides creators with advanced monetization pathways and other innovative applications.

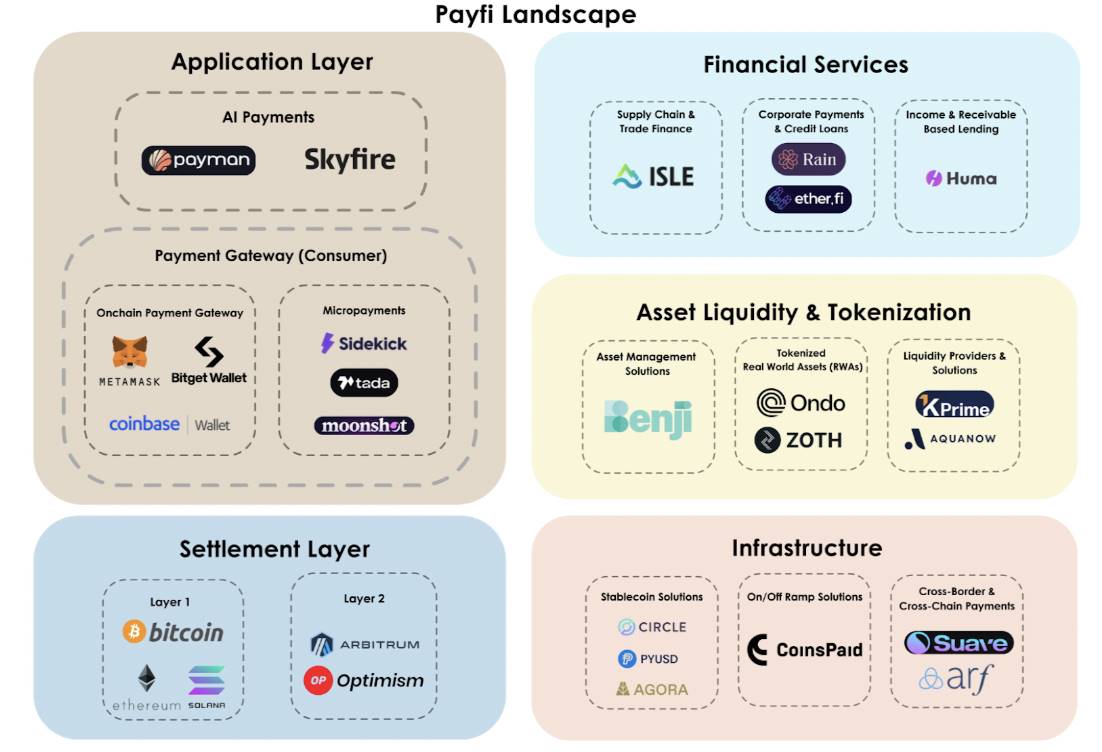

II. Overview of the PayFi Industry and Insights into Sub-sectors

The PayFi ecosystem is thriving, with various industries actively innovating to address financial challenges. Below is an analysis of its key sub-sectors and examples of innovative companies within each field.

(1) Cross-chain and Cross-border Payments

Persistent Issues in Traditional Cross-border Payments

Slow speed and high latency: Traditional payment channels are inefficient, with settlements often taking days. The complexity of settlement processes across time zones and banking hours exacerbates payment delays.

Inefficient use of funds and pre-funding constraints: Pre-funding requirements force financial institutions to maintain foreign currency funds in their accounts, resulting in a global liquidity gap of $4 trillion. Idle funds cannot generate returns, becoming a hidden cost for financial institutions that is passed on to end users, leading to higher fees for users.

High transaction costs: Multiple intermediaries impose layers of fees, including pre-funding costs and currency exchange fees, with the average global cost of cross-border remittances reaching 6.35% (World Bank statistics).

Industry Innovation Cases

Arf: Builds a regulated global settlement banking platform that provides on-chain liquidity solutions for financial institutions. By utilizing stablecoins like USDC, it achieves the immediacy and low-cost advantages of cross-border settlements, providing real-time liquidity for cross-border transactions on demand, eliminating the reliance on large cash reserves in pre-funding accounts; it offers USDC-based instant credit lines, allowing financial institutions to temporarily borrow funds during transactions and repay after settlement. Arf discards the pre-funding account model, effectively reducing funding requirements and settlement times with its USDC-based short-term liquidity solutions, significantly cutting operational costs for financial institutions engaged in global transactions. Emphasizing transparency, it creates comprehensive traceable lending records, easily tracking all loan, repayment, and receivable information via blockchain. Upholding strict compliance principles, as a member of the VQF Financial Services Standards Association, it adheres to international standards for anti-money laundering and financial regulation, setting an example for the industry. To date, it has successfully processed over $1.6 billion in on-chain transactions, maintaining a zero-default record.

suave.money: Develops a cross-chain payment solution that enables businesses to receive cryptocurrency payments from any blockchain network. Businesses can seamlessly integrate various token payments and flexibly choose the tokens they wish to receive based on their needs, enhancing payment flexibility within the blockchain ecosystem. The suave.money platform simplifies cross-chain transactions, allowing businesses to attract user groups from different blockchain ecosystems without managing multiple wallets or rewriting decentralized applications (DApps), thereby broadening their customer base. By facilitating payment convenience from over ten blockchain networks, it enhances liquidity acquisition capabilities, providing strong support for the expansion of DeFi and Web3 projects and increasing market coverage. It simplifies cross-chain transaction processes, reducing operational complexity for businesses, allowing them to attract customers more broadly within the blockchain ecosystem without relying on specialized infrastructure, creating more opportunities for business development. With its innovative capabilities, it helps businesses tap into the trillion-dollar potential of cross-chain capital, occupying a significant position in the rapidly evolving DeFi and crypto payment sectors, offering users unparalleled flexibility and convenience.

(2) Income and Receivables-based Lending

Challenges of Traditional Lending Models: Traditional lending relies on collateral, excluding potential borrowers who lack substantial assets or credit histories, limiting the inclusivity and fairness of financial services.

Emergence of Innovative Solutions: Platforms like Huma Finance allow users to use future income or receivables as collateral for loans, utilizing blockchain technology to achieve transparency and efficiency in the lending process.

Positive Effects: This innovative model significantly enhances financial inclusivity, providing new avenues for funding in underserved markets overlooked by traditional financial institutions, promoting balanced economic development and social equity.

Huma Finance's Practical Case: Constructs a decentralized lending protocol that offers income and receivables-based lending services for businesses and individuals. By connecting borrowers with global investors through an on-chain platform, it pioneers an income-supported lending model distinct from traditional DeFi over-collateralization models. Collaborating with platforms like Circle, Request Network, and Superfluid, it launched the world's first on-chain factoring market on Ethereum and Polygon, allowing users to use tokenized invoices or payment streams as collateral, broadening the range and forms of collateral. Leveraging blockchain efficiency, the factoring process is completed on-chain in under a minute, providing a convenient experience for users. Huma Finance's technical architecture includes several key components. The decentralized income portfolio layer converts invoices, paychecks, staking rewards, and other income sources into tokenizable assets, providing a rich asset base for lending operations. The assessment agent framework accurately evaluates various lending needs, ensuring reliable and stable on-chain credit quality. The smart contract suite enables diverse lending use cases, from invoice factoring to general credit lines, through configurable smart contracts, catering to the personalized needs of different users. Huma Finance focuses on providing much-needed liquidity support for small and medium-sized enterprises and unbanked populations, helping these groups break through traditional financial constraints to access previously unattainable funding resources, promoting their economic development and social integration, and making a positive contribution to building a more equitable and inclusive financial ecosystem.

(3) Tokenization of Real-World Assets

Challenges in Traditional Asset Trading: The trading process for real-world assets such as real estate is cumbersome, with high intermediary costs and slow transaction speeds, causing inconvenience and economic burdens for both buyers and sellers.

Innovative Breakthroughs in Tokenization: Tokenizing real estate and other real-world assets through smart contract technology allows asset ownership to be divided into multiple parts, enabling fractional ownership trading while significantly speeding up transaction processes and injecting new vitality into the asset trading market.

Significant Advantages: This tokenization model notably lowers the barriers to market entry for investors, allowing more participants to engage in real-world asset investments while greatly enhancing asset liquidity, accelerating the buying and selling process, and enabling more efficient allocation and circulation of market resources.

Successful Practice of Ondo Finance: Ondo Finance has launched tokenized U.S. Treasury bonds and other yield-generating products on a blockchain platform, opening up new investment channels for investors to conveniently access short-term U.S. Treasury bonds and other fixed-income assets through decentralized finance (DeFi), achieving an organic integration of traditional financial markets and DeFi. Ondo Finance's innovative products provide investors with stable, attractive returns while ensuring liquidity and security, breaking down barriers between traditional financial markets and DeFi, allowing more investors to share in the previously relatively closed capital market dividends, enriching their asset allocation portfolios, and enhancing the overall efficiency and vitality of the financial market. As of September 2024, Ondo Finance has achieved remarkable results in the tokenized U.S. Treasury bond product sector, with a total locked value (TVL) exceeding $600 million. Among these, the USDY (yield-bearing stablecoin) has a locked amount of $384 million, and the OUSG (tokenized U.S. Treasury bonds) has a locked amount of $221 million, fully demonstrating the market's high recognition and wide acceptance of its innovative products, highlighting its leading position and strong influence in the field of real-world asset tokenization.

Zoth's Innovative Contribution: Zoth has built a market platform specifically for tokenizing trade finance assets, providing investors with a convenient way to access fixed-income products denominated in U.S. dollars. By tokenizing traditional financial assets such as trade receivables and corporate bonds, Zoth bridges the gap between traditional finance and decentralized finance (DeFi), creating high-yield, low-risk investment opportunities for investors while providing businesses with new financing channels and capital management methods. Zoth's platform plays a significant role in the market, not only offering quality investment options to investors, helping them achieve asset appreciation and preservation, but also providing strong support for business development. By tokenizing trade finance assets, companies can unlock working capital more efficiently, optimize their capital structure, and enhance their competitiveness and risk resilience. Additionally, this helps promote the optimal allocation of capital in global markets, directing financial resources more reasonably to businesses and projects in need, further improving the on-chain trade finance ecosystem and making a positive contribution to the stability and development of the entire financial market.

(4) Corporate Payment and Credit Solutions

New Consumer Demands and Limitations of Traditional Credit: In today's consumer market, there is a higher demand for flexibility in payment methods, with consumers expecting a more convenient and diverse payment experience without bearing heavy debt burdens. However, traditional credit models often fail to meet this demand, causing inconvenience and financial pressure for consumers.

PayFi's Innovative Model: To address this market demand, PayFi innovatively introduces unique payment models such as "buy now, pay never," cleverly utilizing interest income obtained from DeFi lending platforms to offset purchase costs, providing consumers with a new, more flexible, and debt-free payment solution that greatly enhances purchasing power and shopping experience.

Industry Innovation Cases

Rain: Launched a corporate card supported by USDC, designed for the daily business payment needs of Web3 teams (such as decentralized autonomous organizations (DAOs) and various protocol projects). With this corporate card, Web3 teams can conveniently use their on-chain assets (such as USDC) to pay for travel expenses, office supplies, and other daily business costs without the cumbersome conversion between cryptocurrencies and fiat currencies, greatly simplifying corporate payment processes and improving financial management efficiency. Rain's corporate card is an important component of its expense management platform, fully leveraging the advantages of blockchain technology to achieve seamless integration of digital assets with traditional payment systems. Through this innovative payment method, companies can manage their finances more efficiently, reducing intermediary costs and time consumption while providing more convenient and secure payment solutions for businesses in the blockchain and crypto sectors, effectively promoting the development and application of the Web3 industry.

Ether.fi: The "Ether.fi Cash" product launched by Ether.fi has garnered widespread attention in the market. This is a credit card in collaboration with Visa, featuring unique innovative functions. Users holding this card can easily obtain borrowing limits using their crypto assets (including various Ethereum-based assets) as collateral, allowing them to spend fiat currency without selling their crypto assets, providing users with a more flexible way to manage funds and a better consumption experience. Additionally, the "Ether.fi Cash" credit card is deeply integrated with Ethereum's Layer 2 network, Scroll, which significantly reduces transaction costs and further enhances user value for money. Moreover, the card supports peer-to-peer USDC transfer functions, allowing users to transfer and manage funds more conveniently, meeting payment needs in different scenarios while bypassing traditional banking intermediaries to save users additional costs. Furthermore, to enhance user engagement and satisfaction, the "Ether.fi Cash" credit card offers attractive cashback rewards, bringing tangible economic benefits to users during their consumption process, further enhancing the product's market competitiveness and user loyalty.

Bitget Card: The Visa card launched by Bitget serves as an important bridge between cryptocurrencies and traditional payment systems, providing users with convenient and efficient payment solutions. This card is closely linked to a multi-currency wallet, allowing corporate or individual users to easily hold, convert, and use various mainstream cryptocurrencies such as USDT, BTC, ETH, USDC, and BGB (currently, the funding account is primarily topped up with USDT, with plans to gradually introduce more cryptocurrencies in the future). In actual payment processes, the Bitget Card can automatically convert cryptocurrencies into fiat currency based on real-time exchange rates, ensuring that users can smoothly complete payments at any merchant accepting Visa cards worldwide without worrying about cumbersome currency exchange procedures and exchange rate fluctuation risks, truly achieving seamless integration of cryptocurrency and fiat currency payments, providing users with great convenience. The emergence of the Bitget Card has had a significant impact on the corporate payment sector, not only simplifying corporate payment processes, allowing companies to use traditional currency for consumption in real-time without manually performing complex cryptocurrency and fiat currency conversion operations, but also greatly improving payment efficiency and capital utilization efficiency. Additionally, its strong cross-border payment capabilities make it easier for companies to expand and operate internationally without the hassle of opening and managing foreign currency accounts, effectively reducing operational costs and financial risks. Currently, the Bitget Card is widely accepted and recognized in over 180 countries and regions worldwide, providing strong support for the global development of enterprises. Furthermore, the Bitget Card has rich potential DeFi use cases, such as in supplier payments, where companies can directly use the card to pay suppliers in fiat currency, avoiding the cumbersome process of manually converting cryptocurrencies, thereby improving payment efficiency and stability in the supply chain; in travel expense reimbursements, employees can easily make business-related consumption payments during cross-border travel using the card, such as booking flights and hotel accommodations, without worrying about payment restrictions and fees, providing more convenient payment solutions for corporate cross-border business activities; in corporate reward mechanisms, companies can also utilize the cryptocurrency payment functions provided by the Bitget Card to issue cryptocurrency-based rewards to employees, who can then convert the cryptocurrency into fiat currency for consumption based on their needs or use it directly in scenarios that support cryptocurrency payments, bringing more innovation and flexibility to corporate employee incentive and welfare systems, further enhancing corporate competitiveness and attractiveness.

(5) Supply Chain and Trade Finance

Challenges in Traditional Supply Chain Finance: In traditional supply chain finance systems, suppliers often face long and complex payment cycles, with large amounts of capital locked up for extended periods, severely restricting their operational efficiency and cash flow capabilities, making it difficult to maintain normal production and business expansion activities. According to statistics, global enterprises face a trade financing demand of up to $2.5 trillion each year that cannot be effectively met due to the limitations of traditional financial institutions, becoming a bottleneck for global trade development and hindering the collaborative development of industrial chains and stable economic growth.

PayFi's Solution: PayFi introduces a decentralized platform to provide innovative solutions for invoice financing issues in supply chain finance. In this model, suppliers can leverage the advantages of blockchain technology to tokenize their invoices and quickly achieve financing on the decentralized platform, instantly obtaining financial support and greatly improving liquidity. Meanwhile, buyers can continue to settle payments according to the original payment schedule without changing their traditional payment habits and financial processes, achieving a balance of interests and collaborative development between buyers and sellers, providing strong guarantees for the efficient operation of supply chain finance.

Industry Innovation Cases

- Isle Finance: Deeply engaged in the on-chain credit market for supply chain finance, Isle Finance's platform can accurately connect high-credit buyers with liquidity providers, helping enterprises obtain financing more quickly. It cleverly utilizes blockchain technology to rigorously verify real-world assets (RWAs) and implements early payment strategies for buyers (especially those with low credit ratings), significantly enhancing the liquidity and security of the entire supply chain, laying a solid foundation for the stable development of supply chain finance. Isle Finance actively promotes reverse factoring business through its platform, not only significantly accelerating payment speeds for enterprises but also greatly optimizing cash flow. This blockchain-based innovative solution allows enterprises to flexibly offer early payment discounts, creating a highly stable and attractive return in the supply chain finance sector while also broadening the channels for enterprises to obtain liquidity, injecting strong momentum into their sustainable development.

(6) Stablecoin Payment Platforms

Example: Agora

Business Content: A meticulously crafted U.S. Digital Dollar (AUSD), backed by cash, U.S. Treasury bonds, and full support from overnight repurchase agreements. The platform is dedicated to leveraging blockchain technology to enable broader and more convenient circulation of the dollar globally, particularly focusing on regions underserved by traditional financial systems, fully embodying the concept of financial inclusion and opening up a new path for the public to access stable and globally recognized currency more easily.

Impact: It has significantly advanced the democratization of dollar access, aligning closely with PayFi's grand vision of expanding financial inclusion. It fully utilizes the technological advantages of blockchain to build a decentralized and easily accessible financial system, allowing individuals and businesses to benefit from dollar-backed financial instruments, with particularly notable results in regions like Argentina and Southeast Asia, providing strong support for local economic development and financial stability.

Achievements: Successfully launched the stablecoin AUSD, initially issued on Ethereum and later expanded to the Avalanche network. Remarkably, within just a few weeks of its issuance, the minting volume surpassed $20 million. Today, the platform is steadily advancing its global strategy for the digital dollar, continuously expanding into international markets while steadfastly adhering to the development strategy of financial inclusion and regulatory compliance, gradually establishing a good reputation and influence in the stablecoin sector.

Example: PayPal

Business Content: Officially launched PayPal USD (PYUSD) in August 2024, initially on the Ethereum blockchain, and successfully expanded to Solana in May 2024. The design of this stablecoin aims to fully integrate the advantages of both blockchains to achieve a fast, low-cost digital payment experience. Especially after expanding to Solana, PYUSD's usability in various commercial and DeFi application scenarios has significantly increased due to its excellent transaction speed and low fees, providing users with a more efficient and convenient payment option.

Impact: With its speed and cost-effectiveness, it is expected to become a strong alternative to traditional payment systems, significantly enhancing global payment efficiency. It successfully enables seamless transfers across different platforms (including PayPal and Venmo), allowing users to easily hold and transfer stablecoins while fully leveraging the technological advantages of blockchain, bringing more convenience and innovative experiences to users' digital asset management and payment transactions.

Achievements: After expanding to Solana, PYUSD's market adoption rate has shown rapid growth, with its market capitalization quickly rising and successfully surpassing $500 million. This significant achievement highlights its deep integration and wide recognition across centralized and decentralized platforms, marking a major milestone in PayPal's exploration of the stablecoin sector and laying a solid foundation for its future development in digital payments.

Example: Bridge (Acquired by Stripe)

Business Content: Bridge, a platform focused on stablecoin payments, has always aimed to simplify cross-border digital payments. Through convenient API interfaces, it enables easy integration of stablecoin-based payments, providing low-cost, high-efficiency cross-border transaction solutions for global users. Before being acquired by Stripe, Bridge had already achieved significant results in e-commerce platform integration, successfully helping merchants seamlessly connect and efficiently handle stablecoin payment operations anywhere in the world, greatly expanding the application scope of stablecoins in the commercial sector.

Impact: Recently acquired by the American payment giant Stripe, this significant event undoubtedly marks a key milestone for stablecoins' integration into mainstream financial services. With Stripe's robust infrastructure and extensive market network, Bridge can further expand its business coverage and enhance its capabilities, aiming to provide global enterprises with more convenient and efficient stablecoin payment and settlement services. This move aligns closely with PayFi's grand vision of promoting financial inclusion and seamless cross-border transactions, accelerating the global adoption of digital currencies. Leveraging Stripe's existing advantages and Bridge's expertise in stablecoin technology, it is expected to foster the widespread application and deep integration of blockchain-supported payment methods in mainstream financial channels, injecting new vitality into the innovative development of global financial payments.

Achievements: In August 2024, Bridge's payment volume annualized run rate successfully surpassed $5 billion, achieving remarkable results. Throughout its development, Bridge has established close partnerships with numerous industry-leading companies, such as Coinbase and SpaceX, and continues to provide high-quality payment services to these enterprises, accumulating rich practical experience and a good market reputation in the stablecoin payment sector, becoming one of the important forces driving industry development.

Conclusion

Overall, PayFi is not a completely new concept. The problems it aims to solve have already existed in traditional financial systems, and there are corresponding solutions. However, this does not mean that PayFi lacks value, as traditional solutions are still not perfect. By addressing the core inefficiencies of the global payment system and leveraging the transformative potential of blockchain, PayFi is expected to unlock unprecedented liquidity and promote financial inclusivity. As more companies innovate in this field, the vision of creating a fully decentralized financial ecosystem for instant, secure, and borderless payments is increasingly coming to fruition. Now is the time to embrace the PayFi revolution and shape the future of global finance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。