One type of stablecoin startup aims to become a partner to traditional financial participants, while another type leans towards building a fully decentralized stablecoin infrastructure.

Written by: YB

Translated by: Luffy, Foresight News

In May 2021, Byrne Hobart wrote an excellent article titled “Stripe and the Solid State Economy” where he articulated a point:

Cars, Excel spreadsheets, vacuum tube computers, attempts to implement bad recursive programs, and efforts to win in real-time strategy games, if they fail, are almost always for the same reason: they have a lot of moving parts, and the more moving parts there are, the easier it is for things to go wrong.

He pointed out that Stripe is a valuable company because it seamlessly combines various business functions required for online payments.

However, the problem is that Stripe's utility is limited to e-commerce, constrained by the institutional framework of the global financial system.

It turns out that there is no 'one' global payment system. Some countries have multiple payment systems, some of which overlap in certain ways, and participating in these systems requires government approval, bank permissions, technological development, and ongoing compliance and maintenance costs.

In other words, the difficulty of global payments arises from the weak network effects between currencies. Those in the cryptocurrency space know: this is precisely the main value pillar of DeFi.

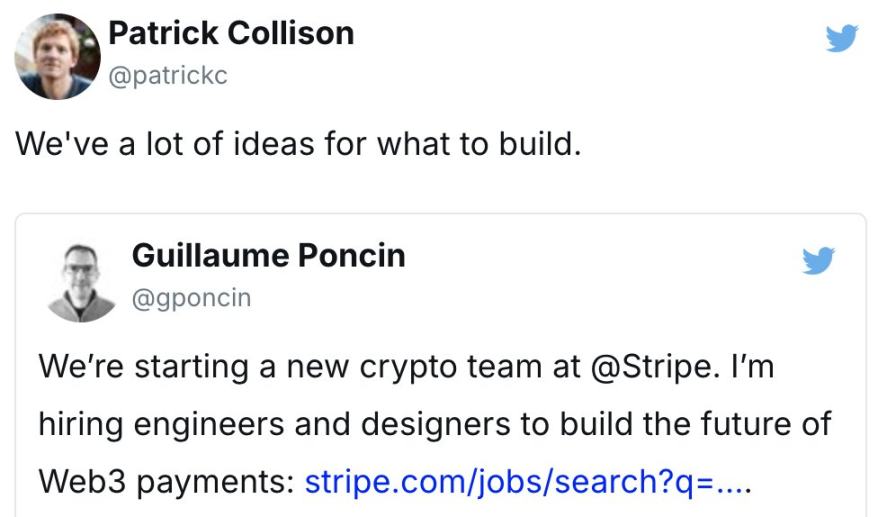

So why am I bringing this up? Because Twitter is currently buzzing with joy over Stripe's $1 billion acquisition of Bridge.

Celebration is warranted… this is a victory for cryptocurrency! The Collison brothers are betting on the crypto industry, sending a signal to other participants in the fintech space.

This is the largest acquisition in cryptocurrency history. Following closely are Coinbase (which acquired Bison Trails for $475 million in 2021) and Binance (which acquired Coinmarketcap for $400 million in 2020).

What caught me off guard about this news was not the acquisition itself, but my complete unawareness of the scale of the stablecoin ecosystem, which far exceeds the familiar figures of Circle (USDC) and Bitfinex (USDT).

In most cases, Bridge wasn't even on people's radar. For the past 2.5 years, they have been quietly exploring the stablecoin space, trying to figure out where they could best fit in.

Bridge's co-founders Zach and Sean ultimately found Stablecoin Orchestration as the answer, which is just a fancy way of saying their API suite can easily convert between stablecoins and fiat currencies, and vice versa.

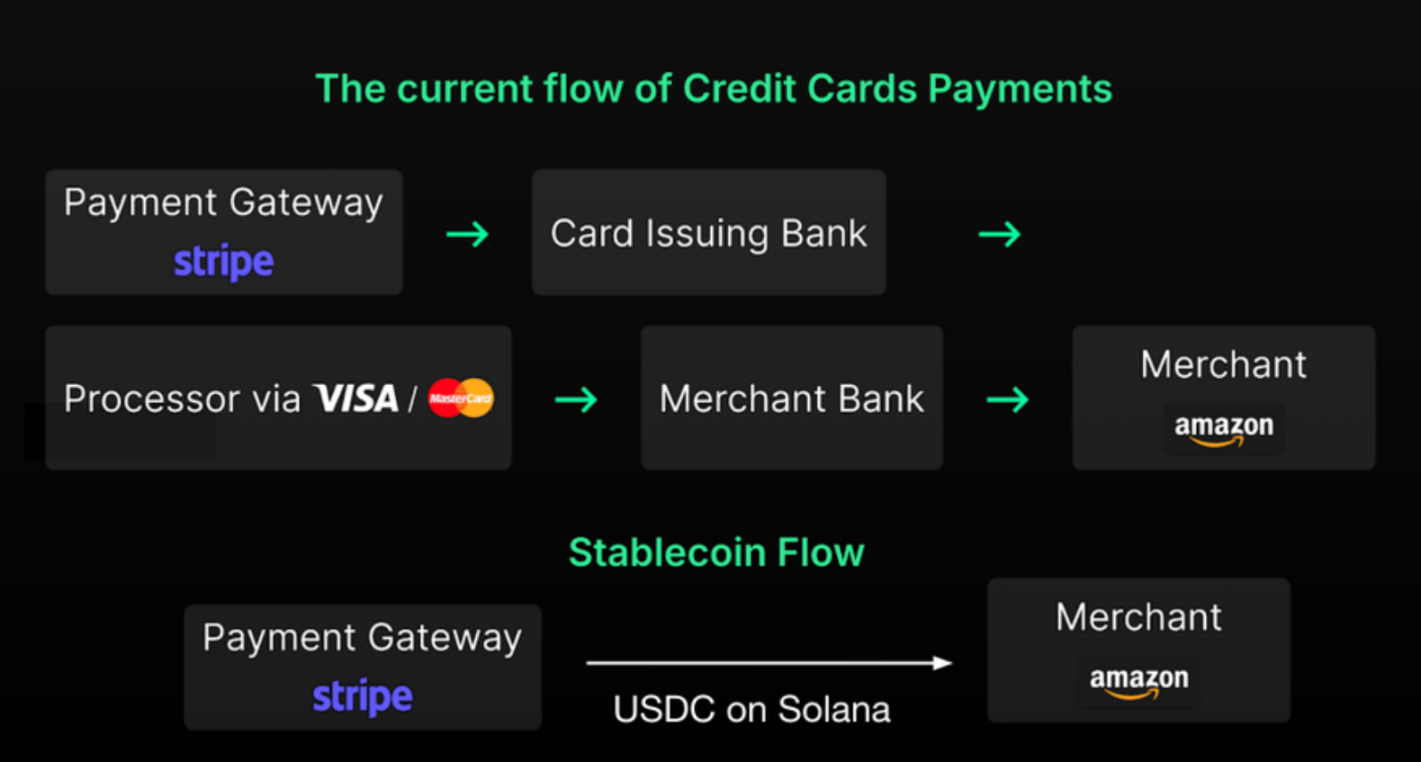

So why was this acquisition a natural fit for Stripe? Because Bridge enables them to eliminate excessive moving parts and streamline their payment processes.

But what does this mean? What impact does this acquisition have on other traditional finance and stablecoin startups?

Traditional Finance Enters the Scene

When using Stripe, most people are unaware that the product is handling processes among various stakeholders: banks, payment networks, and SWIFT for global transfers, among others.

But as Byrne mentioned, Stripe merely makes online payments feasible.

Stripe belongs to an interesting class of value-creating companies that provide services to make certain processes run the way you imagine, even if you've never really tried.

However, these intermediaries not only add transfer and settlement delays, making Stripe's processes inefficient, but they also take a cut from the value chain.

This issue is not unique to Stripe; PayPal faces the same problem, which may be a primary reason they launched their own stablecoin, PYUSD, last August.

By integrating stablecoins, these fintech companies are taking a step closer to capturing the entire online payment value chain.

As I mentioned above, payment companies like PayPal and Stripe work with existing banks to hold user funds. But by using stablecoins, they gain greater autonomy over the value of transactions on their networks.

In a report by Delphi Digital on the moat of crypto products, this passage explains the financial incentives:

… by allowing users to hold pyUSD through PayPal's payment front-end (like Venmo), PayPal effectively becomes a bank. PayPal can then receive user funds and deposit them in the treasury to earn returns. This not only allows PayPal to compress payment fees to zero but also gives them the ability to pay users rebates or some returns on idle pyUSD balances. This is a crushing advantage over other Web2 payment application competitors.

They are positioning themselves as a bank, which is a primary motivation for fintech giants. From a business perspective, this may be more important than faster transaction and settlement speeds.

Now, the interesting point to note is that PayPal and Stripe have taken different approaches.

PayPal decided to issue its own stablecoin, which means they are focusing on fund management. Stripe is betting on the conversion layer, indicating they are focusing on stablecoin infrastructure. They chose their respective paths because it fits their current tech stack.

From a higher-dimensional perspective, Stripe is a payment API company, while Bridge directly integrates this concept. Stripe only needs to integrate Bridge's stablecoin API into their own developer documentation.

PayPal thrives through front-end services like Venmo, leveraging a large retail user base. Thus, their crypto team naturally focuses on optimizing how to manage user balances and leverage that capital. Issuing their own stablecoin, PYUSD, allows PayPal to handle funds more effectively.

In my view, both companies will inevitably verticalize the entire stablecoin stack. Providing internal tools for stablecoin issuance, fund management, debit cards, crypto wallets, etc., is crucial. This seems like a no-brainer, as having a complete internal stack will enable companies to provide the best user experience and capture a larger share of the payment value chain.

In other words, don't be surprised to see Stripe launch its own smart wallet and crypto debit card.

Additionally, it's worth noting that token issuance is a cash cow for stablecoins. For example, Tether generated more profit in Q4 2022 than BlackRock. Therefore, as Stripe explores the maze of stablecoin concepts with its users, they will eventually launch a stablecoin to help their merchants onboard quickly and incentivize the use of their ecosystem's native stablecoin.

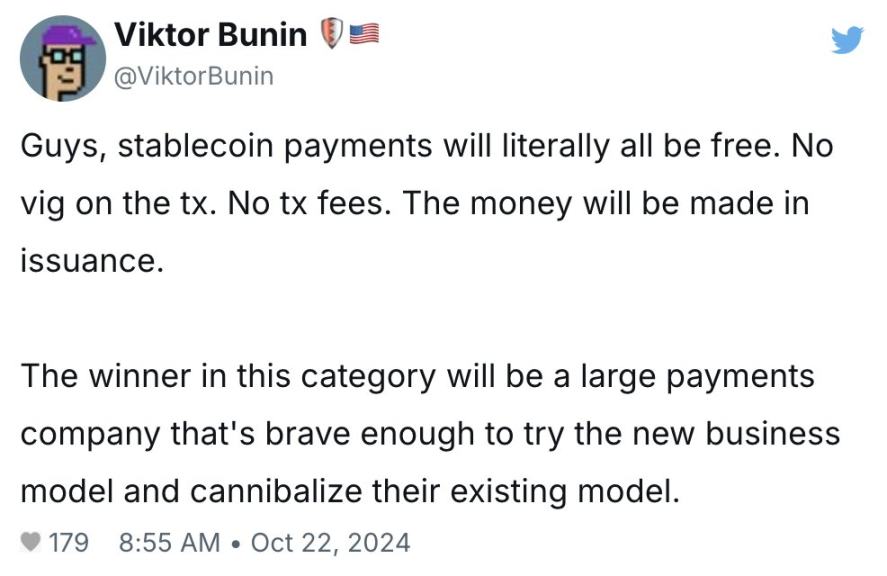

Both Stripe and PayPal have significant global influence and will seek to integrate stablecoin infrastructure into their existing networks. As Viktor mentioned above, in the next five years, companies that "eat into existing models" ahead of other market participants will reap substantial rewards.

Now, you might be wondering: if Stripe and PayPal fully commit to a stablecoin strategy, isn't that a huge threat to payment networks like Visa and Mastercard?

Indeed, it is. That's why Visa and Mastercard have already begun crafting their own playbooks to avoid missing out on the stablecoin revolution. For instance, Visa became the first payment network to accept USDC in 2020, while Mastercard launched its own crypto credit card service.

But I suspect that Stripe's acquisition of Bridge has accelerated the stablecoin strategies of these large traditional finance/fintech companies' crypto teams.

As for banks? To be honest, I'm not sure what their response strategy will be. It's clear that stablecoins undermine their position as facilitators of international payments and custodians of user deposits. But their advantage lies in regulatory compliance, and they may lean towards the rise of CBDCs?

For example, the BRICS nations just announced that they are currently launching their own digital currencies to reduce reliance on the dollar. Clearly, banks will seize the opportunity to formulate their own CBDC strategies to compete for this new market share.

Regardless of what the responses from these different traditional financial stakeholders will be, the overarching theme remains consistent: stablecoins have entered the financial hall.

The question now is, which large institutions will open their arms to embrace the new members of the financial system and quickly become friends with stablecoins?

To some extent, many different participants in traditional finance are starting to look very similar, as they all want to use stablecoins to provide full-stack financial services (payments, banking, card services, etc.).

At this point, we have outlined the impact of stablecoins on all fintech participants, but what will the new entrants of crypto-native stablecoins look like?

If you had to choose one, TradFi or DeFi?

Based on my previous research, founders in the stablecoin vertical need to choose their target audience:

- Traditional finance/Web3 tech companies

- On-chain cryptocurrency adopters

The first is clearly the target of Stripe's acquisition of Bridge; the second hints at the upcoming long-tail effect of DeFi-native stablecoin infrastructure. But what exactly is the distinction between the two?

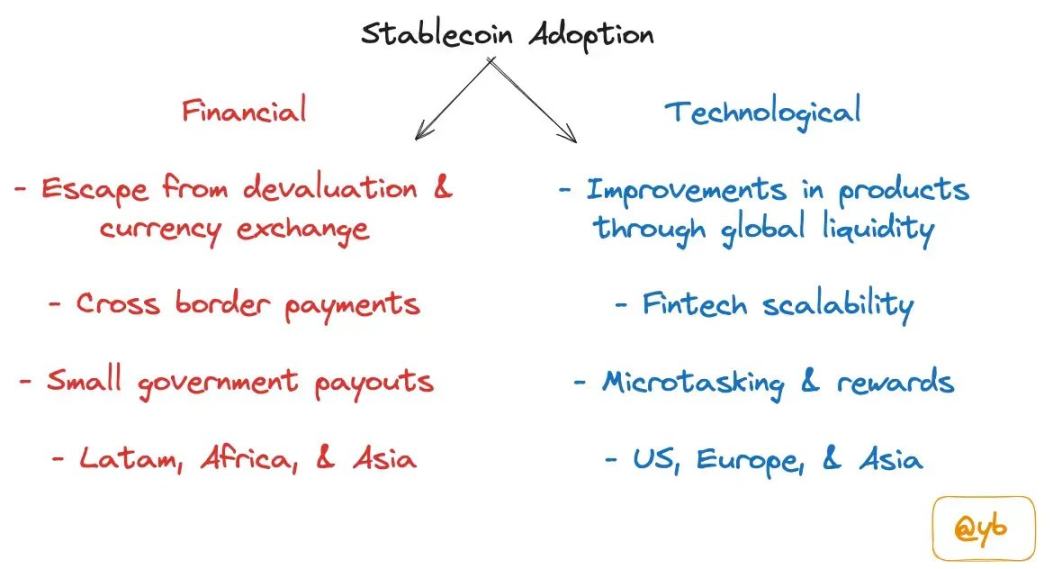

The scale of the stablecoin ecosystem goes far beyond replacing fintech payment services. As I mentioned in my article on stablecoin adoption, it is a dual approach. On one hand, it is dedicated to improving existing financial rails; on the other hand, it uses stablecoins to enhance cryptocurrency products like Polymarket, Bountycaster, Uniswap, Aave, etc.

One type of startup aims to be a plug-in for traditional financial participants, seeking to find more powerful partners, such as Paxos, Ondo Finance, Brale, Agora, Coinflow, and Sphere.

The other type of startup leans towards a fully decentralized stablecoin infrastructure stack, including Prerna, Gnosis Pay, Based App, and Picnic. These companies aim to be direct competitors to products like Stripe and PayPal. They cater to a more crypto-friendly audience and help enhance the on-chain experience through applications that support stablecoins.

That said, I believe founders should consider a stablecoin barbell strategy. Are we catering to traditional financial companies that will inevitably want to enter the stablecoin space? Or are we building stablecoin infrastructure for DeFi applications, attempting new experiments that make no sense to Stripe and PayPal?

In my view, companies that try to double-dip will either be defeated by traditional financial players with distribution moats or be outperformed by DeFi players optimizing their products for unique on-chain functionalities.

Today's post is to share some initial thoughts after hearing about the Bridge acquisition, but I have yet to find meaningful answers to the following questions:

- Where are the moats in the stablecoin stack?

- How will other Web2 fintech participants get involved?

- If another acquisition occurs, who will it be?

In the coming months, developments in the stablecoin space will become increasingly interesting.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。