The era of applications has arrived, and blockchain will thus generate a more powerful non-sovereign digital value storage than ever before.

Author: Ryan Watkins

Translated by: Deep Tide TechFlow

It is widely believed that, aside from Bitcoin and stablecoins, there are no other valuable applications in the industry. It is said that the driving force of the last cycle came entirely from speculation, with almost no progress since the crash in 2022. The industry has become oversaturated with unused infrastructure, and venture capitalists funding this infrastructure may suffer losses due to misallocation of capital.

The latter part of this viewpoint does hold some truth, as the market begins to punish blind infrastructure investments, while long-term winners are emerging based on the crypto economy. However, the former part, which claims that there are few applications relative to infrastructure and that there has been almost no progress since the last cycle, appears inaccurate once we observe the data.

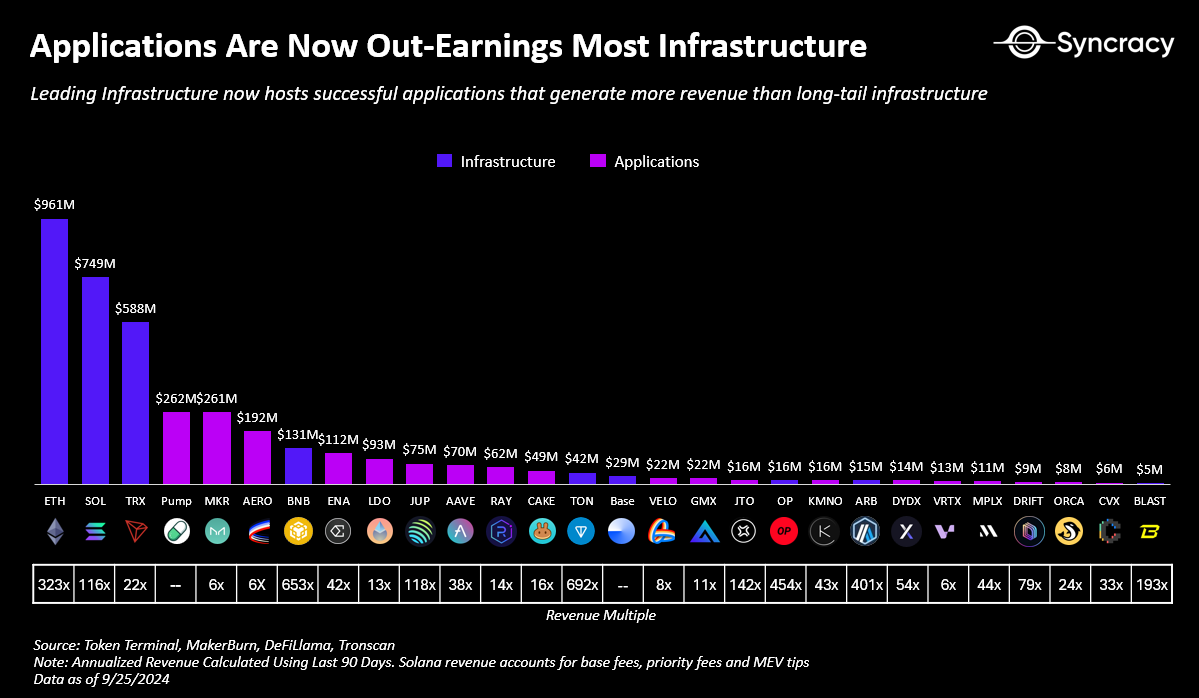

In fact, the era of applications has arrived, and many applications' revenues have surpassed that of infrastructure. Leading platforms like Ethereum and Solana host a multitude of applications that generate tens of millions to hundreds of millions of dollars in revenue each year, growing at triple-digit percentages. However, despite these impressive numbers, the trading prices of applications remain significantly lower than that of infrastructure, with the latter's average revenue multiple being about 300 times that of applications. While infrastructure assets at the center of the smart contract ecosystem, such as ETH and SOL, may maintain a premium for value storage, non-monetary infrastructure assets, such as L2 tokens, may see their multiples compress over time.

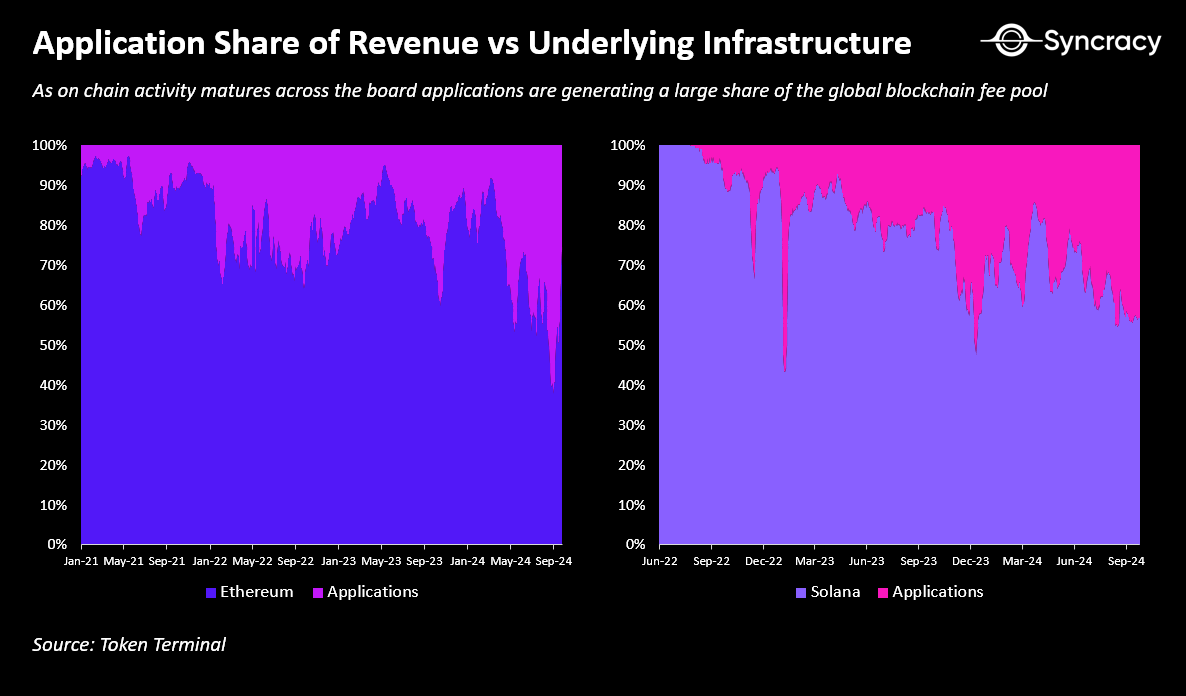

Applications are capturing a larger share of the total global blockchain fees and are exceeding most infrastructure assets in revenue, which may mark a turning point for future trends. Data from the two major application ecosystems, Ethereum and Solana, has shown that applications are gradually capturing a portion of the market share of the underlying platforms in terms of revenue. As applications continue to vie for a larger share of economic benefits and vertically integrate to better control user experience, this trend may accelerate. Even Solana applications, which pride themselves on Solana's synchronous composability, are shifting some operations off-chain, leveraging secondlayers and sidechains for scalability.

The Rise of Fat Applications

Is the rollapp hypothesis inevitable? As applications strive to overcome the limitations of a single global state machine in efficiently processing all on-chain transactions, cross-blockchain modularity seems imperative. For example, while Solana performs excellently in terms of performance, it began to encounter bottlenecks in April this year when only a few million users were trading memecoins daily. Although Firedancer may help, it remains unclear whether it can elevate performance to a level capable of supporting billions of active users daily, including AI agents and enterprises. As mentioned earlier, the modularization process of Solana has already begun.

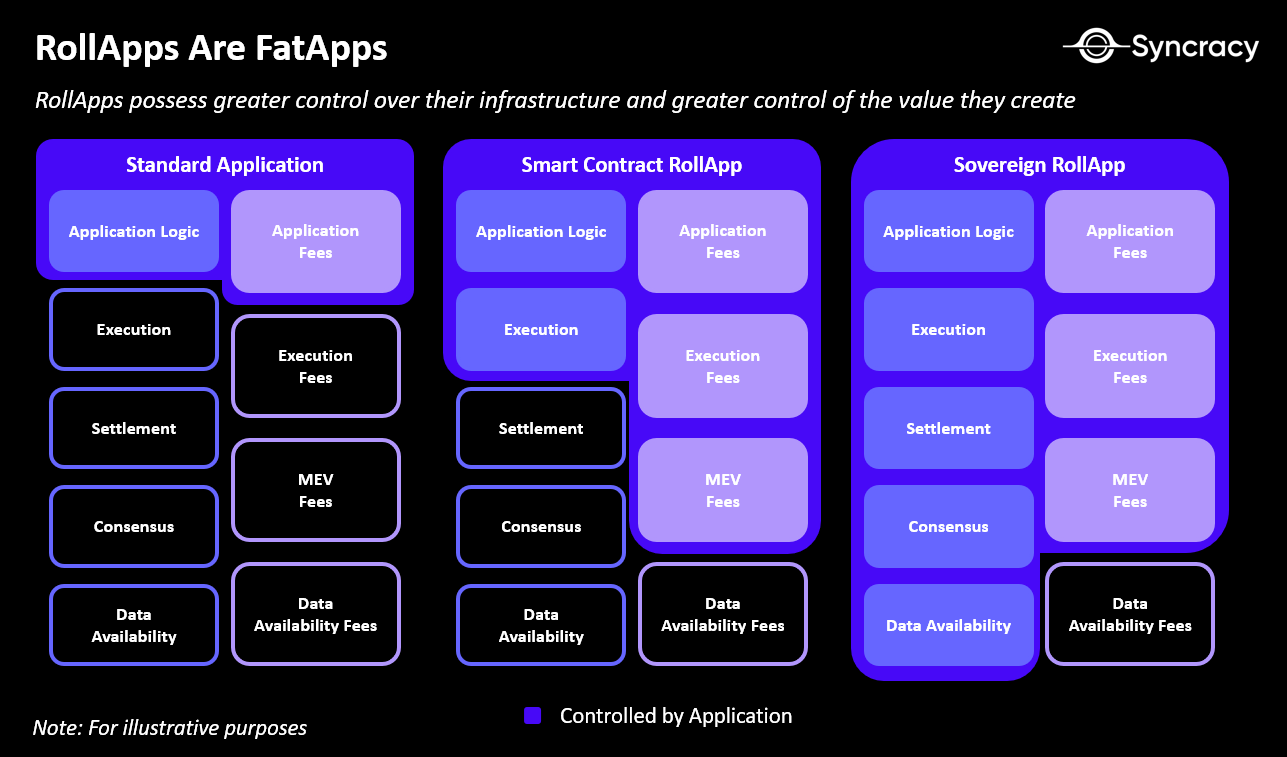

The key question is to what extent this transformation will occur and how many applications will ultimately shift operations off-chain. Running the entire global financial system on a single server—this is the fundamental assumption of any integrated blockchain—requires full nodes to operate in hyperscale data centers, which nearly makes it impossible for end users to independently verify the integrity of the chain. This would undermine a fundamental feature of global scalable blockchains: ensuring clear property rights and resisting manipulation and attacks. In contrast, Rollups allow applications to distribute these bandwidth demands across independent sets of ordering nodes while ensuring end-user verification through data availability sampling at the base layer. Furthermore, as applications scale and establish close ties with users, they may demand maximum flexibility from their underlying infrastructure to better meet user needs.

This is already happening on Ethereum, the most mature on-chain economy. Leading applications like Uniswap, Aave, and Maker are actively developing their own Rollups. These applications are not only pursuing scalability but are also driving features such as custom execution environments, alternative economic models (like native yields), enhanced access controls (like permissioned deployments), and customized transaction ordering mechanisms functions. Through these efforts, applications are not only enhancing user value and reducing operational costs but are also gaining greater economic control over their underlying infrastructure. Chain abstraction and smart wallets will make this application-centric world more seamless and gradually reduce friction between different blockchain spaces.

In the short term, next-generation data availability providers like Celestia and Eigen will be key drivers of this trend, providing applications with greater scale, interoperability, and flexibility while ensuring low-cost verifiability. However, in the long run, every blockchain aspiring to be the foundation of a global financial system will need to scale bandwidth and data availability while ensuring low-cost end-user verification. For instance, while Solana is conceptually integrated, there are already teams working on achieving light client verification, zk compression, and data availability sampling to achieve this goal.

The focus is not on specific scaling technologies or blockchain architectures. Token extensions, co-processors, and ephemeral rollups are sufficient to allow integrated blockchains to scale and provide customization for applications without compromising their atomic composability. Regardless, future trends point to applications continuing to pursue greater economic control and technical flexibility. The benefits gained by applications exceeding those of their infrastructure seem inevitable.

The Future of Blockchain Value Capture

The next question to focus on is how value will be distributed between applications and infrastructure as applications gradually gain more economic control in the coming years. Will this change become a turning point, allowing applications to have an impact similar to that of infrastructure in the coming years? According to Syncracy's perspective, while applications will gradually capture a larger share of global blockchain fees, infrastructure (L1s) may still generate greater returns for a few participants.

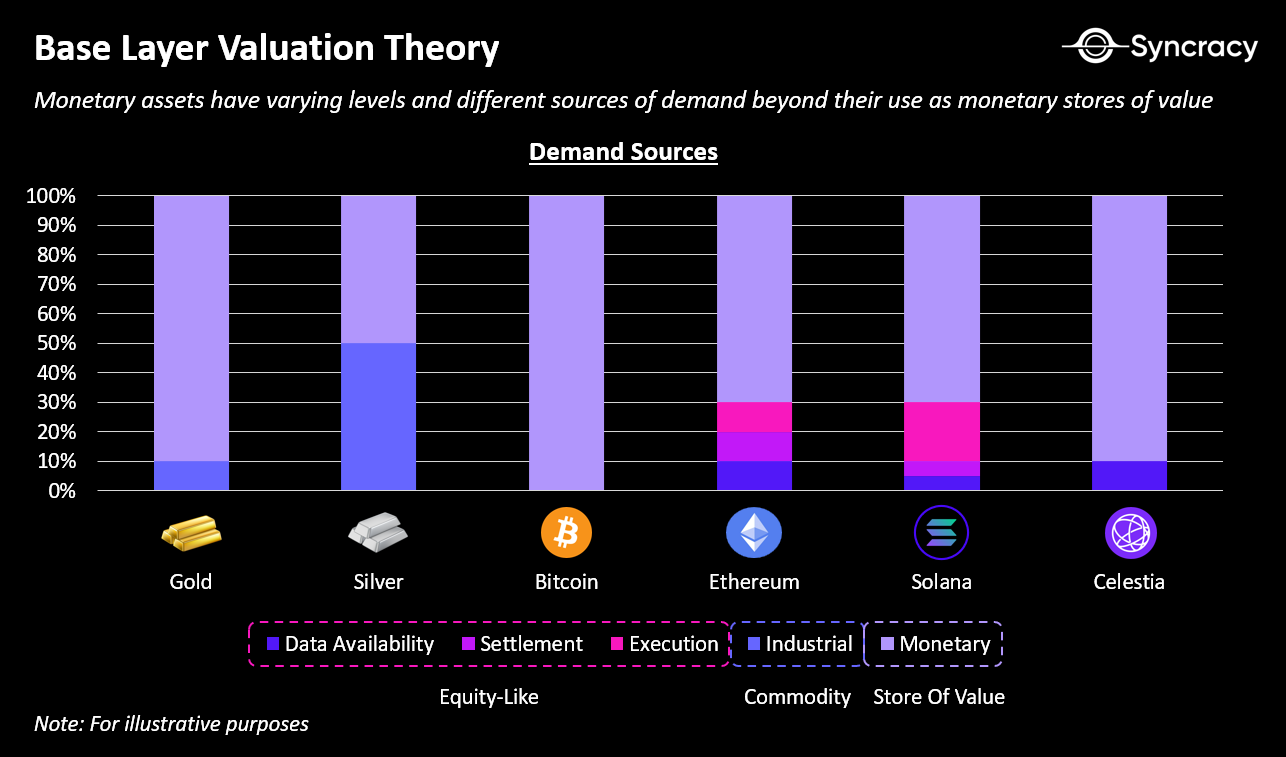

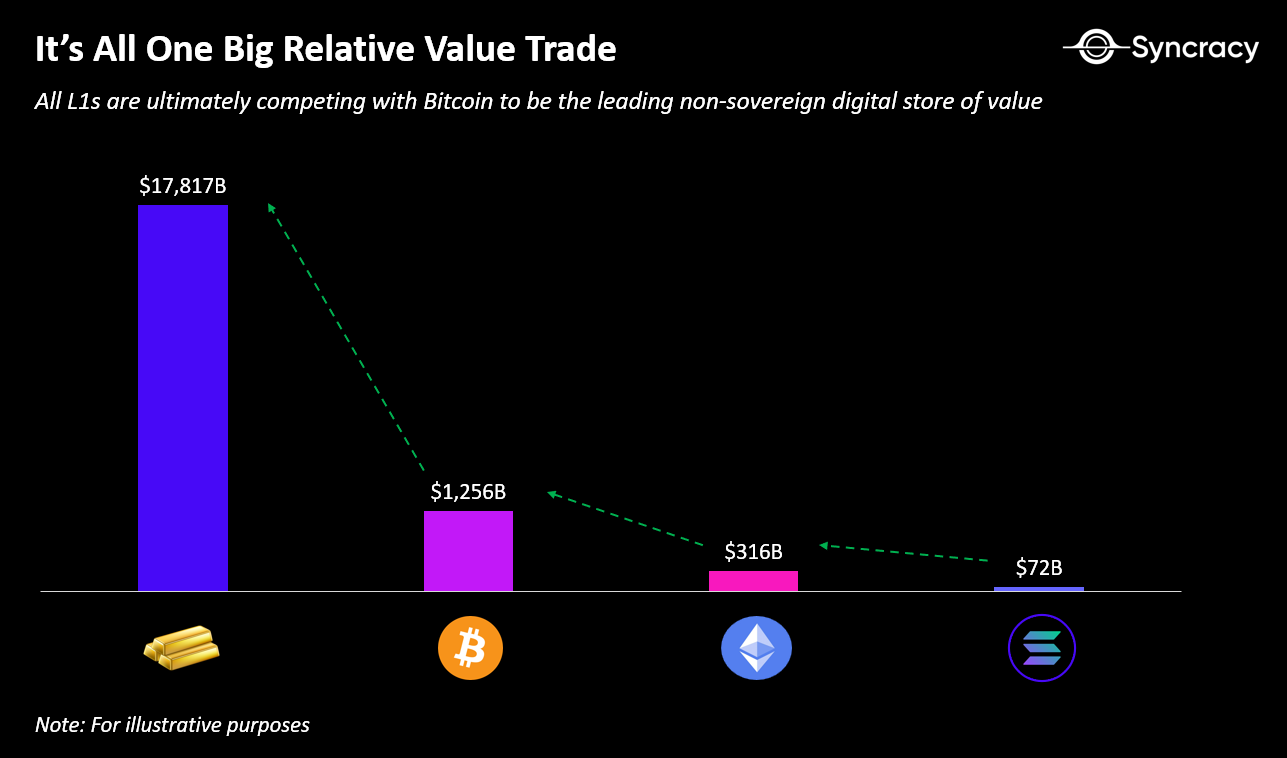

The core argument of this viewpoint is that, in the long run, foundational layer assets like BTC, ETH, and SOL will compete as non-sovereign digital value storage, which is the largest market in the crypto economy. While Bitcoin is often likened to gold and other L1 assets to stocks, this distinction is more narrative than substantive. Essentially, all native blockchain assets share common characteristics: they are non-sovereign, anti-seizure, and can be transferred digitally across borders. These characteristics are crucial for any blockchain aiming to establish a digital economy independent of state control.

The main difference lies in the global popularization strategy. Bitcoin directly challenges central banks by attempting to replace fiat currency and become the dominant global store of value. In contrast, L1s like Ethereum and Solana are dedicated to establishing a parallel economy in cyberspace, creating natural demand for ETH and SOL as they develop. This situation is already occurring. In addition to serving as a medium of exchange (gas fee payments) and a unit of account (NFT pricing), ETH and SOL are also the primary stores of value within their respective economies. As proof-of-stake assets, they directly capture fees generated from on-chain activities and maximum extractable value (MEV), providing the lowest counterparty risk and serving as the highest quality collateral on-chain. In contrast, BTC, as a proof-of-work asset, does not offer staking or fee yields, operating purely as a commodity currency.

While the strategy of building a parallel economy is ambitious, there is little likelihood of achieving this goal, but it may ultimately prove easier to compete in parallel with national economies than to compete directly. In fact, the approaches of Ethereum and Solana resemble historical methods nations have used to vie for reserve currency status: first establishing economic influence, then encouraging others to use your currency for trade and investment.

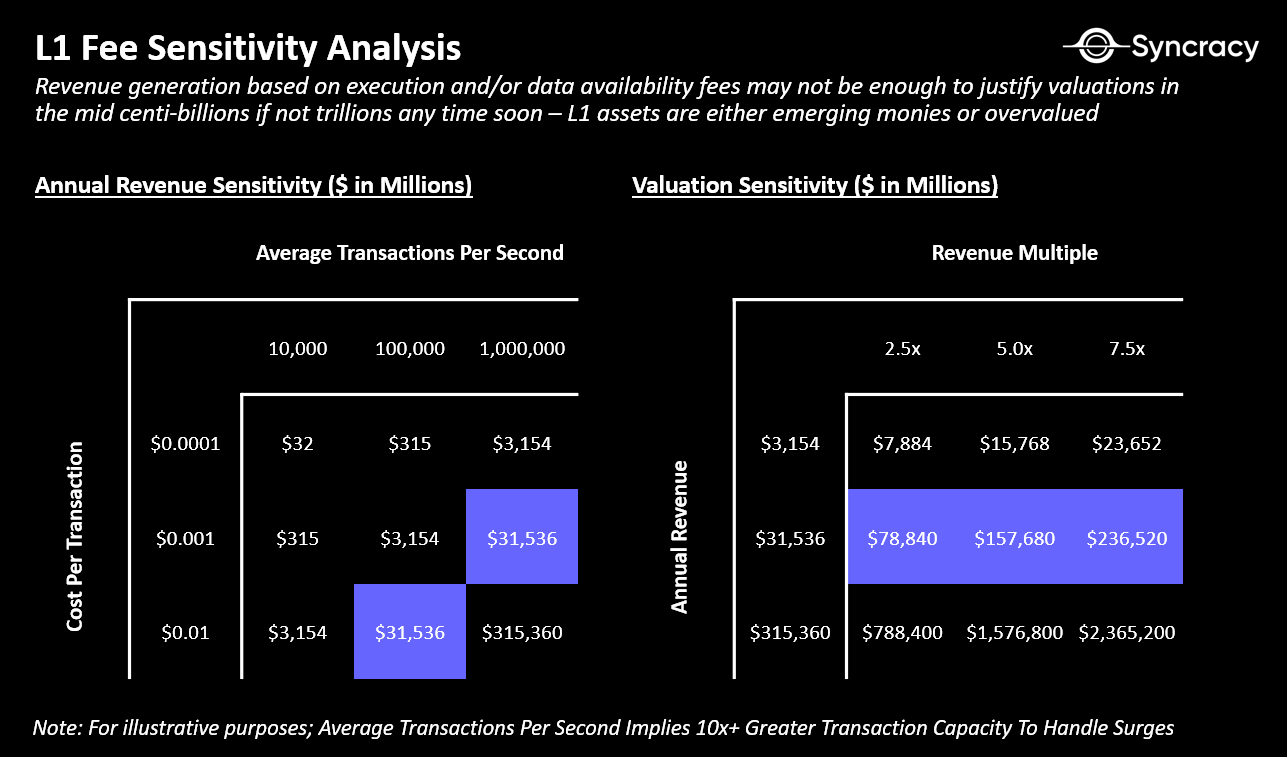

Take MEV as an example; it is unlikely to become a sufficiently large industry to support current valuations, and its proportion in on-chain activities is expected to decrease over time, being absorbed more by applications. The closest analogy to MEV in traditional finance is high-frequency trading (HFT), which has a global revenue estimated between 10 billion and 20 billion dollars. Moreover, current blockchains may have overearned on MEV, and as wallet infrastructure and order routing improve, MEV earnings may decrease, while applications are also working to internalize and minimize MEV. Can we really expect MEV revenue on a blockchain to exceed the global HFT industry and be entirely owned by validators?

Similarly, while execution and data availability fees are attractive sources of revenue, they may still be insufficient to support valuations in the tens or even hundreds of billions. To achieve this, trading volume needs to grow exponentially while fees remain low enough to facilitate mainstream adoption, a process that could take a decade.

Note: Visa's processing capacity is up to 65,000 tps, but typically averages around 2,000 tps.

So, how can sufficient value be provided to pay validators to maintain their basic services? Blockchains can offer a tax-like permanent subsidy through monetary inflation to sustain their operations. In other words, asset holders will lose a small portion of their wealth over time to subsidize validators who provide abundant block space, which in turn provides value to applications, driving the growth of the blockchain's underlying assets.

A more pessimistic view worth considering is that blockchain valuations should be based on fees, but as applications gain more economic control, these fees may not support high valuations in the long term. This situation is not without precedent—during the internet boom of the 1990s, telecom companies attracted massive infrastructure investments, and ultimately many companies became mere commodities. While companies like AT&T and Verizon adapted and survived, most of the value shifted to applications built on this infrastructure, such as Google, Amazon, and Facebook. In the crypto economy, this pattern may repeat: blockchains provide infrastructure, but the application layer captures more value. However, at the current early stage of the crypto economy, this remains a significant relative value competition—BTC wants to surpass gold, ETH wants to surpass BTC, and SOL aims for ETH.

The Era of Applications, The Era of Cryptocurrency

Overall, the crypto economy is undergoing a significant transformation from speculative experiments to revenue-generating businesses and active on-chain economies, bringing real monetary value to blockchain-native assets. While current activity may seem small, it is showing exponential growth as systems scale and user experiences improve. At Syncracy, we believe that years from now, looking back at this period will be interesting, wondering why anyone questioned the value of this field, as many important trends have already become evident.

The era of applications has arrived, and blockchain will thus generate a more powerful non-sovereign digital value storage than ever before.

Special thanks to Chris Burniske, Logan Jastremski, Mason Nystrom, Jonathan Moore, Rui Shang, and Kel Eleje for their feedback and discussions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。