The high-performance blockchain represented by Solana may completely reform the traditional financial market.

Author: OSL

Is blockchain really a disruptor of the traditional financial system, or a catalyst for TradFi to leap forward?

The answer to the question may not be either/or. On the one hand, the emergence of blockchain technology has indeed brought significant impact to the traditional financial system. It not only has the potential to eliminate the cumbersome intermediary links in traditional finance and reduce transaction costs, but also the smart contract function can improve transaction efficiency, reduce human errors and fraud risks, making it potentially disruptive to the traditional financial system to a certain extent.

At the same time, blockchain can also support traditional finance in achieving more efficient and secure solutions, such as in cross-border payments, securities trading, supply chain finance, etc., helping traditional finance to achieve digital transformation, improve service quality and competitiveness, thus becoming a catalyst for the leap forward of traditional finance.

However, this requires a blockchain infrastructure layer that is capable of nurturing killer applications. At the Solana Breakpoint conference, the Solana validator client Firedancer developed by Jump Crypto was also announced to be launched on the mainnet (non-voting mode), with an internal test reaching 1 million TPS, far exceeding Solana's current theoretical limit of tens of thousands of TPS. This breakthrough seems to be sufficient to meet the needs of all high-frequency trading applications, providing more powerful technical support for the application of blockchain in the traditional financial field.

Great winds start from small ripples. In the long run, as a representative of high-performance public chains, Solana is expected to solve the "last mile" of the integration of traditional finance and blockchain, bringing new imagination space to TradFi.

Web3's New Direction for Traditional Finance

Before that, we can ask a question: What has been the most successful crypto financial product globally in the past 5 years?

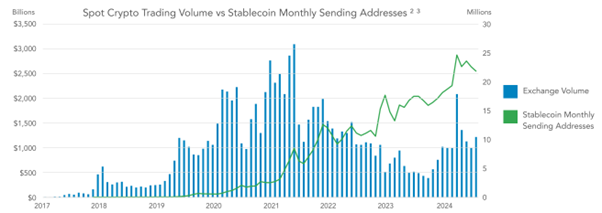

The answer is not difficult to guess. It is neither the on-chain financial innovations such as Uniswap that ignited DeFi Summer, nor the digital artworks such as CryptoPunks that sparked the NFT craze, but the stablecoins that everyone has long been accustomed to.

Yes, outside of DeFi, NFT, and other games with large user bases, stablecoins targeting ordinary users have become one of the widely accepted use cases for crypto/non-crypto users. The number of on-chain accounts for the TRC20 version alone has exceeded 40 million, truly making blockchain and the crypto economy no longer a celebration for a few, greatly expanding and deepening the user base of the crypto economy.

According to the report "Stablecoins: The Emerging Market Story," stablecoin adoption has expanded beyond serving only cryptocurrency users and trading scenarios. In the first half of 2024, about $2.62 trillion was settled through stablecoins, with an annualized scale reaching $5.28 trillion, covering a wider range of financial scenario demands such as currency exchange, commodity payments, remittances, and salary payments.

The reason is simple. Stablecoins provide an excellent entry point for users who have demand for cross-border transactions and payments in the traditional financial system. Blockchain-based payments greatly reduce transaction costs and improve the overall efficiency of cross-border transactions, not only reducing delays, but also solving the complexity and high cost issues associated with the traditional financial system, making it more convenient for both enterprises and individuals to conduct cross-border payments and improve their reliability.

In essence, USDT and other global payment services based on cryptocurrencies have even become a necessary option for "benefit unnoticed, but difficult to survive without." This is also a true portrayal of the current integration of the traditional financial system with Web3:

In the long process of development, although the traditional financial system has established a relatively complete architecture and standards, it has gradually revealed some limitations when facing the rapid development of globalization and the impact of emerging technologies, such as high transaction fees in cross-border transactions, long settlement periods, and complex regulatory requirements, all of which have to some extent hindered the efficient circulation of the economy.

The decentralized, efficient, and convenient technological concept represented by Web3 provides new ideas and directions for the transformation of the traditional financial system.

Solana is Accelerating its Penetration into TradFi

As a high-performance blockchain platform, Solana's high throughput, low latency, and scalability give it a huge advantage in handling financial transactions, meeting the needs of traditional financial institutions for efficient, secure, and reliable transaction processing systems.

From the data perspective, Solana's first wave of growth came from the promotion of the Solana Foundation's Breakpoint annual conference in 2023. Before October 2023, the number of daily active users measuring Solana's ecosystem activity had been hovering between 80,000 and 100,000.

The Breakpoint conference in late October to November 2023 stimulated the first phase of growth, and then the JTO airdrop and the listing of BONK on Coinbase further promoted this growth, causing it to soar more than 5 times to over 500,000 users.

Since the beginning of 2024, Solana has been accelerating its penetration into TradFi in the rapidly developing financial technology field today, bringing new changes and opportunities to the financial industry with its unique advantages.

The Underlying Logic of Solana for PayFi

PayFi is a typical example, as the name suggests, it is to create diversified application scenarios and functional services (Fi) around the behavior of "currency payment" (Pay).

Solana Foundation Chair Lily Liu's explanation is also straightforward: "The motivation of PayFi is to realize the initial vision of Bitcoin payments. PayFi is not DeFi, but it creates new financial primitives around the time value of currency."

Currently, PayFi on Solana has not been fully deployed and is still in a blue ocean. Lily Liu also provides many examples to the community of the usage scenarios it can cover, such as:

- Buy Now Pay Never: Unlike the common installment payment model, it involves depositing the purchase amount into a DeFi product for lending and interest, using the interest to pay for the purchase cost, sacrificing cash flow. For example, a user buys a $1000 TV and then deposits $10,000 into a DeFi lending product. Over time, the interest generated from this deposit gradually increases, and when it reaches $1000, the system automatically uses the interest to pay for the TV and returns the remaining deposit to the user.

- Creator Monetization: For example, a painter creates a painting expected to sell for $5000, but the payment will take two months. The painter can use PayFi to discount the expected income from the painting at a price of $4500, allowing the painter to obtain funds in advance for purchasing painting materials, living expenses, etc., without waiting for a long payment period.

- Account Receivable: A small business provides a batch of goods to a customer with an accounts receivable of $20,000. However, the customer's payment cycle is long, causing cash flow constraints for the business. The business can pledge this accounts receivable to a receivables financing company and obtain $18,000 in cash, ensuring timely access to funds for paying employee salaries, purchasing raw materials, etc., and ensuring the normal operation of the business without being affected by the speed of customer payments.

In addition, one can also imagine implementing automatic "daily pay" or even hourly pay for work, or paying by the minute or second when watching videos or listening to music. What kind of scenario would that be?

In general, with the programmability of smart contracts, Solana's high performance and low transaction costs can meet the high-frequency, small-value flow payment scenarios that traditional financial settlement systems cannot achieve—previously, due to the high gas fees and performance bottlenecks of Ethereum, previous attempts at flow payments have been limited.

Comprehensive Optimization of Traditional Financial Trading Systems

In addition, in the traditional financial market, large trading volumes and high speed requirements are common characteristics, and Solana's high throughput can easily handle large-scale trading demands, transferring trading to the chain for more efficient and decentralized processing.

The most direct demand is in the securities trading market, where a large number of financial products such as stocks and bonds are traded every day. Traditional trading systems may experience congestion during peak periods, leading to trading delays. Solana's high performance allows it to process millions or even tens of millions of transactions in a short period of time, ensuring timely execution of trades.

Especially, once Firedancer is fully deployed, it means that Solana's peak throughput can reach hundreds of thousands of transactions, far exceeding the processing capacity of traditional financial systems, providing more efficient trading processing solutions for traditional financial institutions, reducing transaction waiting times, and improving market liquidity.

At the same time, in financial trading, time is money. Low latency is crucial for fast decision-making and trade execution, and Solana's low latency allows trades to be confirmed within milliseconds, providing traders with a real-time trading experience.

For example, in the foreign exchange market, where exchange rates fluctuate rapidly, traders need to obtain market information and make decisions in a timely manner, and Solana's low latency can ensure that traders complete trades in the shortest time possible, avoiding missing the best trading opportunities due to delays. Low latency also helps reduce market risks and improve trading security.

Scalability to Meet the Growth Needs of Financial Businesses

As the financial market continues to develop, traditional financial institutions face system pressure from business growth. Solana's scalability allows it to easily handle growing trading demands and business scale.

For example, with the rise of the digital currency market, more and more traditional financial institutions are entering this field, and Solana can provide stable and reliable blockchain infrastructure for these institutions to support the trading, storage, and management of digital currencies. At the same time, Solana can also integrate with traditional financial systems to achieve cross-chain transactions and asset transfers, providing more opportunities for business innovation for financial institutions.

Currently, DeFi projects on Solana such as PYUSD provide new business models and revenue sources for traditional financial institutions, as well as higher-yield savings products and convenient lending services for customers: Since the launch of PYUSD on Solana, it has grown by 271%, with PYUSD on Solana accounting for 88% of this growth.

From this perspective, through integration with Solana DeFi, traditional financial institutions can improve their competitiveness and meet customer demands for diversified financial services.

Supply Chain Finance and Asset Tokenization

Solana's blockchain technology can provide transparent and traceable transaction records for supply chain finance, reducing credit risks. For example, in international trade, Solana can record the transportation, warehousing, and trading information of goods, ensuring that all parties can timely understand the status of goods and the flow of funds. This helps improve supply chain efficiency, reduce financing costs, and provide better financing channels for small and medium-sized enterprises.

In addition, according to BCG's research, the market for asset tokenization could reach $16 trillion by 2030, equivalent to 10% of global GDP. Solana can tokenize traditional financial assets such as real estate and artworks, digitize assets, and increase liquidity, reducing investment thresholds and increasing asset liquidity and value.

Cross-Border Trade Settlement

In a previous article, "Revisiting Crypto Trading: A New Solution for Liquidity Revolution in the Traditional TradFi System," several inherent problems in the traditional cross-border payment system were summarized:

- First, the entire process involves multiple intermediary banks, making the settlement time potentially extended to several days (T+N). In the current era of real-time trading, this undoubtedly causes significant efficiency waste.

- Second, each intermediary bank involved in the transaction charges fees, greatly increasing the total cost for the remitter. For businesses that rely on timely payments to effectively manage cash flow and individuals remitting money to cross-border family members, these delays and costs are almost unbearable.

- Furthermore, the complex and diverse regulatory environments in different jurisdictions pose challenges for traditional cross-border payments, and the unpredictable risk of exchange rate fluctuations during the long transaction period further exacerbates these difficulties.

In short, the traditional interbank payment process has many problems, and the market urgently needs innovative solutions that can provide faster, more cost-effective, and more reliable cross-border payment options to support the speed and scale of global trade, and blockchain-based cross-border payment settlement solutions are already providing better choices.

Solana has a competitive advantage among various blockchain solutions, not just making interbank transfers faster. Its low latency, high throughput, combined with the programmability of smart contracts, will completely change the circulation of currency, allowing for more diverse forms of transactions between individuals and merchants, as well as between merchants, supply chains, and financial institutions—quantifying everyone's economic behavior precisely in the form of flow payments, achieving real-time automatic payments, settlements, and other unique Web3 financial payment paradigms.

Conclusion

In conclusion, Solana is accelerating its penetration into the traditional financial field with its advantages of high throughput, low latency, and scalability, bringing new changes and opportunities to the financial industry. With the continuous development of technology and the widespread application of Solana, it is expected to become an important driving force for the digital transformation of traditional financial institutions.

Just recently, OSL also officially launched Solana (SOL) trading for professional investors, aiming to provide valuable investment opportunities for investors.

As the Web3 industry continues to develop, we will undoubtedly see Solana bring more and better solutions to the traditional financial system and the world, and it is hoped to continue to be the main narrative of the next bull market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。