Author: Wenser; Editor: Hao Fangzhou

Produced by Odaily Planet Daily (ID: o-daily)

In December 2017, when the market value of the cryptocurrency industry reached 500 billion US dollars, Ethereum co-founder Vitalik raised a series of "industry questions" (https://x.com/VitalikButerin/status/940744724431982594), mentioning key issues including banking services, anti-censorship commercial transactions, practical use cases for Dapps, actual interest rates, anti-inflation, and payment channels. In the end, he believed that despite some progress in these areas, they fell far short of expectations compared to market value data.

Today, the cryptocurrency market value, after surpassing 3 trillion US dollars in November 2021, has now fallen to around 2.4 trillion US dollars. Mass adoption is still a distant prospect, VC coins are criticized as "high FDV, low circulation" "blood-sucking machines" in the fluctuating market, and different tracks such as L1, DeFi, GameFi, NFT, SocialFi, DAO, Infra, L2 have taken turns to rise and then fall. Meme coins, which started in 2013, returned to the cryptocurrency stage in 2023 and continued to shine in 2024 after the approval of Bitcoin spot ETF and Ethereum spot ETF.

Looking back, the cryptocurrency industry has grown from the roots of Bitcoin and gradually developed into a "towering tree" with many branches. In front of this towering tree, there may be another cold winter, or perhaps another warm spring. In this still small but fertile "decentralized land," there are always new lights of ideals and wealth miracles waiting for us.

Odaily Planet Daily will briefly review and analyze the past venture capital cycles in the cryptocurrency industry in this series of articles. Although it is inevitable to miss some details, it can also serve as a supplement to the perspective for readers' reference.

Bitcoin Innovation Plan: Starting with Ethereum

After experiencing the Bitcoin pioneering period from 2013 to 2015, Bitcoin gradually became the stage for mining machine manufacturers and leading exchanges, and the market's ups and downs called for "another round of innovative diffusion."

When it comes to the venture capital cycle from 2016 to 2018, Ethereum is an unavoidable focal point. It is precisely because of its emergence and subsequent success that it established another "industry monument" in the cryptocurrency industry, and thus opened the first wave of "crazy enthusiasm" in the industry—ICO (Initial Coin Offering). Countless projects obtained varying amounts of initial funding through this, and the cryptocurrency industry quickly entered a "chaotic development period" with a mix of idealists, scammers, robbers, and thieves coexisting, and sentiments and greed intersecting. The industry's wilderness is always like this, with lies and truths intertwined, and innovation and scams just a step away.

Cryptocurrency's New Beginning: Greatness Cannot Be Planned

On July 22, 2014, the Ethereum ICO began, with a fundraising price of 1 BTC exchangeable for 2000 ETH, without permission, VC, or lock-up. In the end, this ICO raised over 18 million US dollars in the form of Bitcoin, with a single ETH priced at around 0.3 US dollars.

It is worth mentioning that Ethereum co-founder Vitalik was only 20 years old at the time. The idea of Ethereum originated from a white paper he sent to his friends at the end of 2013, which mentioned "I propose to design a new type of Bitcoin. This new Bitcoin will be based on a universal programming language and can be used to create various applications, such as social, trading, games, etc." These things have all come true today, once again proving his amazing foresight for the development trend of the cryptocurrency industry.

Photo of Vitalik playing with an IBM computer when he was young

In addition, one of the important reasons Vitalik entered the cryptocurrency industry is said to be the deletion of the "Life Tap" skill of the Warlock game character he loved in the World of Warcraft by the game developer Blizzard. Since then, the world has lost a loyal World of Warcraft player, but gained a decentralized believer.

In December of the same year, Xiao Feng, CEO of Wanxiang Blockchain Lab and partner of Distributed Capital, accidentally learned about Vitalik and specifically introduced Ethereum in a speech, which also laid the groundwork for "Shanghai's upgrade of Ethereum." According to Xiao Feng in an interview (https://www.odaily.news/post/5186633), "Ethereum went live in July 2015. Before the mainnet went live, the tokens held by the foundation and other official organizations were locked, with about 18 million US dollars in the account. After spending a certain amount, there was still money in the account. I remember there should have been 3 million US dollars in the account at that time. After all, the mainnet had not yet gone live, and people would ask if this money was enough. In fact, there was no performance crisis at that time. Some people would still ask, can this money support the mainnet going live? If not, what should we do? It just so happened that Vitalik was in Shanghai at the time and happened to come to our office. I heard that he was in a meeting last night, and voices from all sides were asking him how to explain it, but he did not answer on the spot.

I heard about this at the time, and it was not for investment, but for a great cause, to help this young man.

Our idea at the time was very simple. First, we could provide 500,000 US dollars in cash, and second, we also told the community that after providing 500,000 US dollars, we could continue to support. Subsequently, after we signed a donation agreement with the Ethereum Foundation and transferred the money to them, the Ethereum Foundation promised to give us the tokens at the price we donated when their tokens could be unlocked on the mainnet. Our idea at the time was to support them. In case the mainnet did not go live, it didn't matter. We considered it as supporting a great idea and did not think about it from an investment perspective." Nevertheless, Vitalik mentioned in a later interview, "The 500,000 US dollars from Wanxiang became Ethereum's lifeline."

Perhaps, as the saying goes, "greatness cannot be planned." Ethereum's development received support from Xiao Feng and the Wanxiang Group, simply because the latter "wanted to help young people like Vitalik realize a great idea." It may sound simple, but the cryptocurrency industry at that time, after experiencing the bear market baptism of 2013, indeed urgently needed a "new benchmark" to rebuild industry confidence, and Ethereum came at the right time.

On July 30, 2015, the first phase version of Ethereum, Frontier, was released, and the first Ethereum block was mined. The Ethereum blockchain network, adhering to the vision of the "world computer," officially began its operation.

Although Ethereum suffered a market value evaporation of up to 500 million US dollars due to the attack on The DAO (the world's first DAO organization, which lost 60 million US dollars' worth of Ethereum due to an attack after completing a 150 million US dollar crowdfunding) in June of the following year, it still successfully completed a hard fork upgrade and smoothly weathered this crisis with the support of leaders like Vitalik, early founding members of Ethereum including Gavin Wood, and the global Ethereum community, including Chinese cryptocurrency mining and capital institutions.

Cryptocurrency's Further Development: VC Coins Were Once Meme Coins

On May 19, 2017, the price of Ethereum broke through the $100 mark for the first time, which also meant that early Ethereum investors achieved an astonishing return rate of over 300 times (although this date would later become one of the "darkest moments" in the cryptocurrency industry).

Once again, it proved the correctness of investing in Ethereum and laid the foundation for the "ICO craze" in the cryptocurrency industry to be reignited.

In June 2017, Binance initiated the ICO of its platform token BNB. By July 2, the ICO had ended, raising a total of $15 million worth of digital assets. On September 1, Binance announced a $15 million financing from Black Hole Capital and Pantera Capital.

In August 2017, Binance's platform opened its ICO for the first time, and 500 million TRX tokens were sold at a price of about $0.01 within 53 seconds. Subsequently, TRON ICOs were launched on platforms such as RenRenICO and ICO365. According to insiders, TRON raised about 7,000 bitcoins in this ICO, worth about $200 million at the time.

In September 2017, Cardano (ADA, reportedly named after Ada Lovelace, the daughter of the famous poet and mathematician Byron, known as the first programmer in human history) raised over $62 million through a two-year ICO, with the token being sold at $0.0024 each and completing the TGE at $0.02 in October.

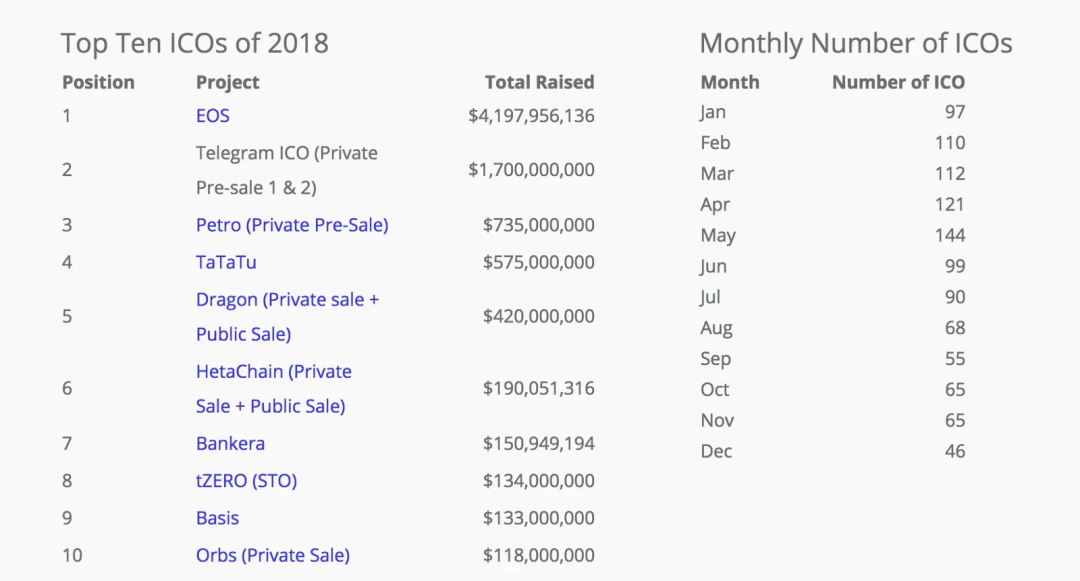

Top 10 ICO projects in 2017

The increasingly enthusiastic ICO activities were accompanied by a plethora of false projects such as "white paper first" and "air coin speculation," which became the catalyst for regulatory intervention.

On September 4, 2017, the People's Bank of China, in conjunction with seven departments, issued the "Announcement on Preventing the Risks of Token Issuance Financing," declaring ICOs as illegal activities, known as the "9/4 Event." While facing regulatory pressure from various countries around the world, the cryptocurrency industry continued its development. Binance, in particular, swiftly completed its transfer from Shanghai to Japan and began gradually removing users from related regions, laying a solid foundation for becoming the "world's largest cryptocurrency exchange."

However, looking at the fundraising methods in the cryptocurrency industry at that time, the "value coins" now sought after by major VC and other investment institutions could also be considered meme coins to some extent, due to their relatively decentralized fundraising methods, low issuance prices, and token names and symbols with meme properties.

Additionally, according to the "2017 China Internet Finance Investment and Financing Analysis Report" (https://www.odaily.news/post/5126806), the number of equity financing cases in the blockchain field increased from 4 in 2016 to 29 in 2017, a staggering 625% increase. In terms of total market value, according to Coinmarketcap data, the global daily market value of digital currencies exceeded $600 billion at the end of December 2017, with a total of 1,334 digital currencies.

On January 17, 2018, Binance's registered users exceeded 6 million, with over 97% of users being international, covering over 180 countries worldwide. Soon, Binance's trading volume surpassed that of Huobi and OKCoin (the predecessor of OKEx), becoming the world's largest cryptocurrency trading platform. From then on, Binance, OKCoin, and Huobi formed a tripartite balance of power, and the investment landscape created by the exchange's venture capital departments was about to unfold, attracting more and more attention as the exchange's influence continued to grow.

It is worth noting that the chaos of ICOs also triggered "regulatory attention" globally at the time. In early 2018, Gibraltar (https://www.odaily.news/post/5119070) announced the launch of the world's first ICO regulatory regulations, which also attracted close attention from regulatory agencies in the UK and Singapore. The Swiss Financial Market Supervisory Authority set three categories of ICO digital tokens, with asset-type digital tokens considered as securities. In Russia (https://www.odaily.news/post/5119543), government departments proposed that the nominal capital of ICO project initiators should be at least 100 million rubles. Meanwhile, the United States adopted existing securities regulations to regulate ICO events.

This was clearly necessary, as a Bloomberg report in July 2018 indicated that about 78% of ICO projects were identified as scams before trading. By July 2018, popular high-quality projects accounted for 70% of ICO funds (in USD). The subsequent emergence of IE0, ID0, and various fundraising and asset issuance methods can be seen as variations or updates of ICOs to some extent.

Cryptocurrency Trends: Public Chains Become Investment Hotspots

In 2018, thanks to founder BM's "halo effect" and the flow of funds and investors from China brought by early Bitcoin "evangelists" like Li Xiaolai, the EOS project raised $185 million in the first five days before its ICO. After the launch of the "election of 21 super nodes" by EOS holders, various representative figures and capital behind them, including Xuemanzi, Baorun Gongqinwang, Laomao, Yilihua, and Antpool, all announced their high-profile entry into the EOS node election, bringing high market attention and liquidity to EOS. Ultimately, on June 2 of that year, EOS successfully concluded its year-long ICO with an impressive fundraising of $4.2 billion.

Top 10 ICO projects in 2018

As BKFund's managing partner and director of Distributed Capital's strategic management department, Xu Chaoyi, mentioned in an interview with 36Kr in 2018 (https://www.odaily.news/post/5126806), "In 2018, BKFund's primary focus in the blockchain primary market was on industry public chains in the first tier, followed by industry vertical public chains in the second tier. Specific vertical applications could only rank in the third tier, leaning more towards traditional internet applications migrating to blockchain networks." He also candidly explained the logic behind this investment preference: "In the blockchain industry, the highest valuations are for the underlying protocol layer or public chains, while the valuations of the platform layer above are lower. The imagination and valuation of the business layer above the vertical industry will be much lower."

On the one hand, this is due to the early stage of development in the cryptocurrency industry, with a significant gap in infrastructure construction. On the other hand, to a large extent, it is also because of Ethereum's "pearls in front," with countless individuals and capital institutions entering the market, wanting to emulate the high returns obtained by Xiao Feng and Wanxiang due to their strong support for Ethereum, and "invest in the next Ethereum." This is the obsession of countless people at that time and one of the reasons why projects like Cosmos and Polkadot were highly sought after later.

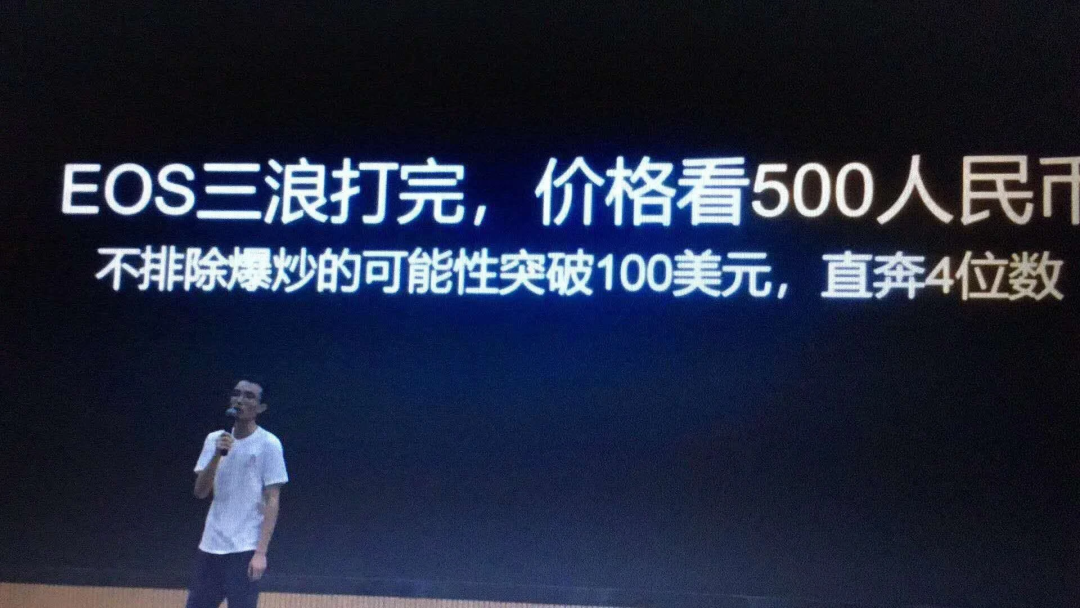

However, it is clear that the idea that "after three waves, EOS is expected to break through $1,000" was just a fantasy of the market bubble period. The cost of this fantasy was heavy, even brutal, as the subsequent price trend of EOS told the story: "The market does not move according to individual will."

Classic statement of the three waves of EOS

After experiencing a new high in market capitalization, breaking through $850 billion at the beginning of the year, the cryptocurrency industry once again entered a new round of "shakeout." Bitcoin dropped from over $18,000 at the beginning of the year to around $3,200 at the end of the year, with a decline of about 82% during the year. Ethereum, which was nearly $1,500 at the beginning of the year, briefly dropped below $100 and reached a low of around $83. The transition of the bull and bear market cycles and the test of market positions are constantly unfolding in the cryptocurrency industry.

Despite the arrival of the crypto winter not being as abrupt as imagined, the first half of 2018 saw a "slightly hot" trend in investment and financing in the blockchain field. According to Securities Daily, the first half of 2018 saw a surge in investment and financing activities in the blockchain field, with a total of 222 financing deals. The United States and China accounted for 179 of these deals, totaling 80.6% of the global total. Although China had 141 financing deals in the blockchain field, far exceeding the 38 deals in the United States, the financing amounts were similar, at $6.4 billion and $6.7 billion, respectively. In terms of financing stages, seed/angel round financing in the blockchain field accounted for 107 deals, or 48.2% of all rounds, with a total financing amount of $1.6 billion, accounting for only 10% of all rounds. In terms of financing projects by country, China had 73 seed/angel, 9 Pre-A, and 16 A round financing events, while the United States had 18 seed/angel, 0 Pre-A, and 6 A round financing events.

The Wave of Change: DeFi Summer, GameFi Summer, NFT Summer

As time entered 2019, the investment and financing in the cryptocurrency industry tended towards rationality. Specifically, the financing scale decreased by nearly 40% compared to 2018, with a total of 653 financing events and a total financing amount of nearly $4.7 billion (about 32.9 billion RMB). In addition, there were 35 public mergers and acquisitions in 2019, with a total acquisition amount exceeding $3 billion.

Overall, the cryptocurrency industry in 2019 seemed to be in a transitional phase of "continuing the past and opening the future." Although investment and financing were relatively active, they were mainly concentrated in the field of digital assets represented by exchanges and financial applications. In February, the exchange Kraken received a $100 million investment. In October, A.TOP Asia Exchange received an investment of 50,000 bitcoins from Potato, which was even ranked first in the total financing amount among the disclosed projects (note: this financing news was questioned by the market). Indian payment giant PhonePe received investments of $101 million and 4.05 billion rupees in July and October, respectively. In addition, payment companies Rapyd and Ripple also received investments of $100 million and $200 million, respectively, in the second half of the year. Overall, exchanges accounted for 129 financing deals, or 20% of the total financing events, making it the "most frequent financing category" of the year, with a total financing amount of about $2.22 billion, accounting for about 40% of the total financing amount for the year.

In terms of investment institutions, 2019 was also a "year of transformation." Overseas investment institutions gradually competed with Chinese investment institutions, with the U.S. investment institution Digital Currency Group being the most active with 14 investments. Even the U.S. cryptocurrency exchange Coinbase, established in 2012, and its subsidiary Coinbase Ventures, established in 2018, jointly ranked at the forefront of the list of institutions with 6 investments each. This also laid the groundwork for the next wave of the DeFi trend.

2019 Institutional Investment Data Ranking

Starting from 2020, the "era wave" of cryptocurrencies will attract global attention with different tracks rising one after another, creating a dynamic environment for the entire world.

DeFi Summer: Liquidity Mining as an Industry Paradigm

After the emergence of Ethereum, a long-standing question was, "What can Ethereum do?" While the consensus value of Bitcoin continued to rise with its spread, people had higher and more diverse demands for the practicality of the "cryptocurrency 2.0 system," including Ethereum.

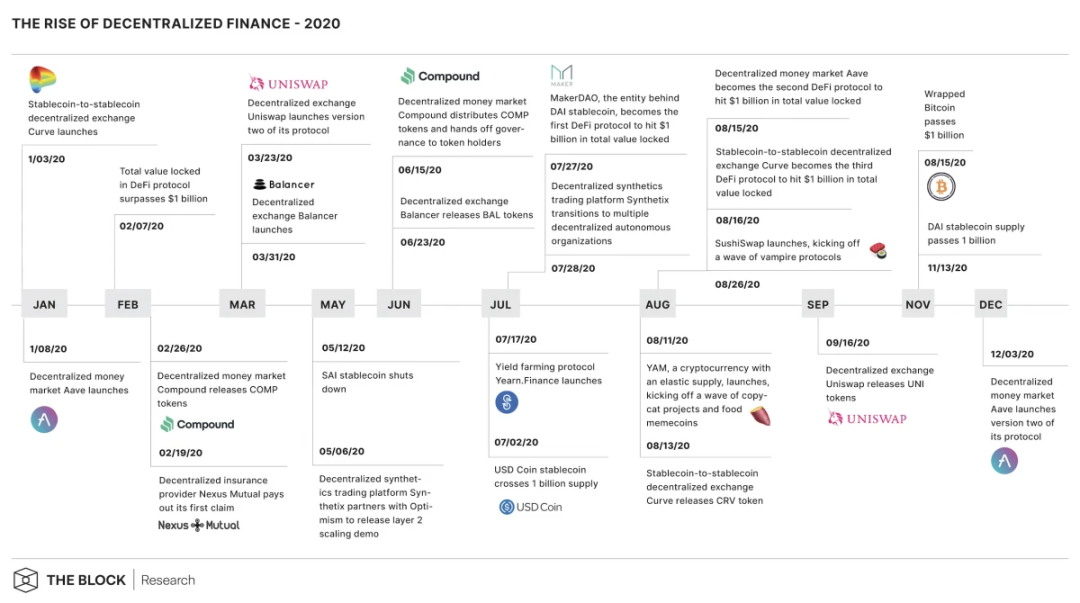

Despite the market cooling off in March 2020, the highly active participation of Compound and Aave (formerly ETHLend) in the money market business, as well as the exchange business of platforms like Curve, SushiSwap, Uniswap, and 1inch, led to the quiet arrival of DeFi Summer.

The concept of "liquidity mining" proposed by Synthetix (SNX) in July 2019 was truly realized through the issuance of governance token COMP by the Compound Protocol. Yearn Finance's governance token YFI became the first crypto asset in history to surpass the price of Bitcoin, gradually popularizing the concept of "yield farming." The concept of staking officially took the stage and gradually became a major industry paradigm.

Users could earn protocol native tokens by providing liquidity to DeFi protocols, sparking a new wave of "cryptocurrency issuance craze." Many projects needed to consider attracting users and increasing liquidity through tokens, making token issuance one of the most effective competitive strategies in the market.

After all, the pursuit of wealth is the unforgettable "original intention" of every player in the cryptocurrency industry.

2020 DeFi Milestones

(https://www.theblock.co/linked/89271/here-are-some-of-the-biggest-defi-events-in-2020)

According to industry data (https://www.odaily.news/post/5164636), global cryptocurrency investment and financing continued to grow rapidly in 2020, with a total of 434 investment and financing events throughout the year, and multiple projects completing multiple rounds of financing. The total disclosed financing amount for the year reached $3.566 billion (excluding acquisitions).

According to Arcane Research, the total value locked (TVL) in DeFi increased by about 2,100% throughout the year, and the number of unique addresses increased tenfold. Perhaps due to ample market liquidity support or the intensification of competition brought about by the arrival of DeFi Summer, the total financing amount for DeFi projects experienced a breakthrough, reaching approximately $278 million, accounting for only 7.80% of the total financing amount in the cryptocurrency industry. The average financing amount for individual DeFi projects was only $4.8 million, making it the weakest financing capability among all sub-sectors. The $50 million financing completed by the cryptocurrency lending company BlockFi in August of that year was the highest single financing amount in DeFi for the year.

Looking back one year after DeFi Summer (https://www.okx.com/zh-hans/learn/defi-summer-cn), with TVL increasing by 58 times, the number of users increasing nearly 140 times, the total borrowing amount increasing by over 3474.1%, and the highest increase in DEX trading volume reaching 382.5 times, the impact of DeFi on the entire cryptocurrency industry was comprehensive and far-reaching. In addition, Polkadot (DOT) also raised approximately $43 million through an ICO that year, becoming another "star public chain."

GameFi & NFT Summer: The "Gold Rush" Led by Axie Infinity and the "Blue Chip NFT Craze" Led by Opensea

As we entered 2021, the events that had a significant impact on the industry can be mainly categorized into three types:

First, in the traditional financial market, Coinbase successfully went public on the US stock market with the stock code COIN, signaling a commitment to "compliance to the end." Roblox also debuted on the NASDAQ stock market, igniting the concept of the "metaverse," and Facebook directly renamed itself Meta.

Second, in the cryptocurrency industry, the "FTX Group" (including FTX Exchange, the cryptocurrency quantitative trading firm Alameda Research, and a series of investment projects including Solana) gradually emerged as a new force in the cryptocurrency exchange sector. FTX Exchange briefly rose to the position of the "second-largest exchange" in the industry but also sowed the seeds of its downfall for 2022.

Third, in terms of specific project tracks, the "gold rush" brought by GameFi Summer led by Axie Infinity and the gaming guild YGG, as well as the NFT Summer led by blue-chip NFTs such as BAYC, CryptoPunks, and the NFT trading platform Opensea (which continued until May 2022, marked by the sale of 10,000 ETH worth of Gas by Otherside), were the major events.

In addition, "Web3" entered people's field of vision in a more popular and inclusive manner and gradually gained popularity with the strong promotion by Ethereum co-founder Gavin Wood, Polkadot founder Chris Dxion, and a16z investor Chris Dixon, becoming the latest synonym for the "cryptocurrency industry."

Furthermore, Solana, founded in 2017 by former engineers from Qualcomm, Intel, and Dropbox, and using the "Proof of History (PoH)" mechanism as a tool to improve network efficiency, also shone brightly this year. After raising $25 million in funding from private placements and ICOs, it received an additional $40 million from OKX and MEXC in March (https://cointelegraph.com/news/solana-raises-40-million-in-strategic-investments-from-okex-mxc-exchanges). In June, it secured $314.15 million in a private token sale led by Andreessen Horowitz and Polychain Capital, with participation from institutions and individuals including 1kx, Alameda Research, Blockchange Ventures, CMS Holdings, Coinfund, CoinShares, Collab Currency, MGNR (Memetic Capital), Multicoin Capital, ParaFi Capital, Sino Global Capital, Jump Trading, and Boys Noize (https://solana.com/news/solana-labs-completes-a-314-15m-private-token-sale-led-by-andreessen-horowitz-and-polychain-capital), as it was touted as the "next Ethereum killer" due to its claimed "far superior TPS operational efficiency."

Multicoin Capital, as a deeply involved investor in Solana, also reaped thousands of times in investment returns. However, as time entered 2022, the market would tell everyone a truth: "Achieving something can also become your lesson," and the intuitive result of path dependence is that "profit and loss are two sides of the same coin."

The NFT game Axie Infinity, which made waves and drove the "gold rush" in Southeast Asia, saw its parent company Sky Mavis complete a $7.5 million financing round in May, led by Libertus Capital, with participation from Blocktower Capital, Konvoy Ventures, Collab Currency, Derek Schloss, Stephen McKeon, and Mark Cuban, among others. The next round of financing (https://www.odaily.news/newsflash/281143) would have to wait until April 2022, but the financing amount would increase significantly to $150 million. Founded in 2017, Axie Infinity had previously achieved the milestone of "AXS token listed on Binance" in early November 2020 as the "most active blockchain game," with only about 7,000 monthly active users at the time. A few months later, it had become synonymous with the "GameFi industry" and successfully created the so-called "Play-To-Earn" (P2E) model, laying the foundation for the emergence of subsequent projects like STEPN.

As for BAYC at the time, despite its impressive performance due to the endorsement of sports and entertainment stars including Stephen Curry and Snoop Dogg, with the floor price briefly surpassing 55 ETH, as the main character of "NFT Summer," it had not yet secured financing.

In that year, the absolute protagonist in the NFT field was Opensea. After completing a $2 million seed round of financing in 2018 and a $21 million strategic round of financing in 2019, in March 2021, Opensea completed a $23 million Series A financing round led by a16z, with participation from the Cultural Leadership Fund, as well as angel investors such as Ron Conway, Mark Cuban, Tim Ferriss, Belinda Johnson, Naval Ravikant, and Ben Silberman. In July, it once again completed a $100 million Series B financing round led by a16z, with a post-investment valuation of $1.5 billion. This was still several months away from the peak of the "NFT bubble," and Opensea would continue to perform.

According to Footprint Analytics (https://www.odaily.news/post/5175751), there were a total of 1,045 financing events in 2021, with a total financing amount of $30.27 billion, representing an increase of nearly 790% compared to 2020. In terms of specific project financing, stock brokerage firm Robinhood, exchange FTX, and application service platform Revolut ranked as the top three in the CeFi sector. In the DeFi sector, decentralized autonomous organization BitDAO, asset trading platform FalconX, and decentralized aggregator exchange 1inch ranked as the top three.

It is worth mentioning that DAO organizations received great attention at this time, with Seed Club, Bankless DAO, and FWB being seen as benchmark organizations for DAOs, but ultimately to some extent, they were "falsified" by the market.

In November 2021, the cryptocurrency industry's market capitalization finally surpassed $3 trillion amid a surge, ushering in another bull market after the "5.19" baptism of that year, and a new narrative was about to unfold. More stories of venture capital cycles were still ongoing.

Cryptocurrency Industry Market Cap Surpasses $3 Trillion

Summary: Each generation has its own legends, and each version has its masters

Looking back at the journey of the cryptocurrency venture capital cycle from 2016 to 2021, each stage, each bull and bear market, and each cycle has its own "main theme" and "version answer." The projects and roles that have ridden the waves are numerous, with some achieving success and then retiring, some disappearing without a trace, some still active to this day, and some still searching for their "wealth code."

In the upcoming Part 2, covering the years 2022 to 2024, we will continue to track the people, events, and developments in the wave of the cryptocurrency industry's venture capital cycle. We aim to summarize past experiences and lessons for the venture capital industry while providing readers and friends with valuable insights and information. If anyone wishes to engage in discussions, please feel free to contact us. More perspectives and information are always welcome.

Goodbye for now, until the next part of our series on the evolution of the cryptocurrency venture capital cycle.

References

A Decade of Blockchain Turbulence

https://www.odaily.news/post/5134263

How To DeFi: Advanced

https://nigdaemon.gitbook.io/how-to-defi-advanced-zhogn-wen-b/di-1-zhang-defi-kuai-zhao#defi-summer-2020-su-cheng-defi-xia-tian

Ethereum 2.0: Struggles for Interests and Power

https://www.odaily.news/post/5160035

The Last Miners: A Comprehensive Review of Ethereum's 8-Year Mining History

https://www.odaily.news/post/5181758

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。