On March 31, 2026, the FTX Recovery Trust officially launched the fourth round of creditor distributions totaling about $2.2 billion. As funds are gradually deposited into accounts within 1 to 3 working days through channels such as BitGo, Kraken, and Payoneer, this most famous bankruptcy case in crypto history seems to be heading towards a seemingly satisfactory conclusion.

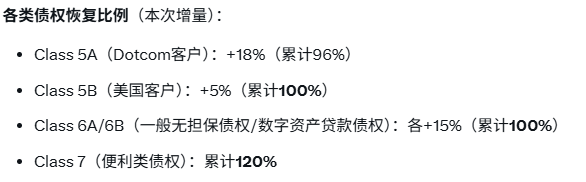

On the surface, this is a victory for Web3 infrastructure. Compared to Lehman Brothers, which took 14 years and Enron, which took 11 years to liquidate, FTX achieved an astonishingly high recovery rate in just over three years — US customers (Class 5B) achieved a total of 100% recovery, Convenience Class creditors even reached a 120% overpayment rate, and Class 5A reached about 96%. The transparency, traceability, and extremely high liquidity efficiency of on-chain assets allowed the speed of bankruptcy liquidation to far exceed that of the traditional financial system.

However, behind the glamorous data of "120% overpayment" lies an extremely cruel invisible wealth transfer occurring in the cryptocurrency market. When we analyze the flow of this $2.2 billion in funds, we find that the biggest beneficiaries of this distribution are no longer the desperate and tearful original FTX users from November 2022, but rather traditional financial distressed asset funds that are well-versed in the cycle rules. The crypto collapse case may be invisibly completing an epic "blood transfusion" for traditional finance.

To understand the essence of this wealth transfer, it is first necessary to clarify the valuation benchmark in bankruptcy court. In FTX's liquidation framework, all payouts are strictly pegged to the fiat currency-based prices of cryptocurrency at the time FTX filed for bankruptcy in November 2022.

This is a snapshot of an extremely low price!

At that time, the price of Bitcoin was only $16,871. This means that if a user held 10 BTC before the FTX collapse, their legal debt size would be firmly locked at about $168,710. Today, when they receive 100% or even 120% of the "overpayment," the absolute amount they get back is approximately between $168,000 to $200,000. However, in the real market at the end of March 2026, the market value of 10 BTC has reached about $670,000.

The original cryptocurrency asset holders are reclaiming "collapse price dollars," rather than the appreciation profits of the assets themselves. This large price difference (over $400,000 in missed opportunity costs) is actually the "implicit missed opportunity tax" that original creditors pay to obtain fiat currency liquidity. The bankruptcy reorganization process legally protects the integrity of the dollar-pegged payouts but, in fact, deprives crypto native users of the Beta returns they should have earned during the subsequent three-year recovery cycle. This seemingly fair statutory full payment is, for investors who believe in crypto-based assets, akin to a second systemic plunder.

If the original users' missed opportunity is the helplessness of bankruptcy law, then the prosperity of the secondary claim market is the ultimate manifestation of capital's bloodthirsty nature.

The biggest beneficiaries of this $2.2 billion distribution are the "discount creditors" who have been active in the over-the-counter market between 2023 and 2024.

Looking back to 2023, the market was in a deep bear phase with the prospects of FTX's restructuring unclear. A large number of retail and small to medium-sized institutional creditors faced extreme liquidity exhaustion, being forced to sell their claims at discounted prices in the secondary market. At that time, Hedge funds, family offices, and specialized distressed asset investment funds on Wall Street massively acquired these claims at extremely low prices of 30 to 40 cents on the dollar (30%-40% of face value).

This formed a classic "bankruptcy arbitrage" chain:

TradFi institutions bought $1 of claims for 30 cents at the extremely pessimistic emotional bottom. As FTX enriched its fiat treasury through the sale of its held crypto assets (such as massive amounts of SOL) and in the market recovery had finalized the restructuring scheme with a payout rate of 100% to 120% in dollar terms, this meant that those distressed asset buyers lurking during the trough achieved nearly risk-free, unleveraged absolute returns of 200% to 300% in dollars within just over two years.

In the past, few people systematically tracked the true identities of these "second-hand creditors" and the subsequent flow of their funds. However, this $2.2 billion centralized release provides an excellent observation window. The essence of this arbitrage capital is that it is driven by fiat currency-based returns, and its genes are fundamentally different from the crypto native community.

When these immense profits are realized, the fate of this capital will most likely not be to re-enter the cryptocurrency secondary market to purchase high-priced Bitcoin or Ethereum, but to flow directly into the TradFi market, such as purchasing US Treasury bills (T-bills), high-yield corporate bonds, or investing in the next traditional macro-arbitrage target.

The extreme fluctuations and collapses in the crypto market have essentially created a massive pool of cheap assets; while traditional financial capital, leveraging its size and time tolerance advantages, has completed low-level harvesting in this pool, ultimately permanently extracting huge fiat profits from the crypto ecosystem. This is not just a change of chips, but also a dimensional strike on liquidity levels.

$2.2 billion liquidity test: cold returns and market pressure under "extreme fear."

In the narrative of retail investors, the $2.2 billion distribution is often interpreted as "a boon from the heavens," a significant liquidity injection into the crypto market. However, the reactions of professional traders on social media like Twitter are unusually lukewarm, even wary. Current market sentiment is in an extremely tense state, with the Fear & Greed index dropping to 11, signifying "extreme fear"; coupled with complex geopolitical pressures, this $2.2 billion may not only fail to become the fuel for market recovery but may instead exacerbate short-term market fluctuations.

Historical data provide the coldest evidence. Reviewing the previous three rounds of creditor distributions by FTX, on-chain analysis shows that only about 30% to 40% of the funds will flow back into cryptocurrency trading platforms within 30 days and be converted into spot purchasing power. This low flow rate is destined by two main reasons:

Firstly, for those original retail investors who held on to their claims and did not sell, after three and a half years of torment, the pressure of living expenses and their distrust of centralized exchanges have reached a peak. When they receive fiat currency through Payoneer or compliant channels, their primary concern is to improve their liquidity in real life, rather than to re-bet on high-risk assets in the current "extreme fear" market sentiment. The comments from the Chinese crypto community are particularly pragmatic: "What everyone urgently needs is real-world liquidity; this doesn’t count as good news."

Screenshot from the Chinese sector of the platform X — Yuan Zhang

Secondly, as mentioned earlier, a significant proportion of the secondary market claim-buying institutions do not have investment mandates to go long in cryptocurrencies. For this part of the capital, the day of the $2.2 billion distribution is precisely their "liquidation withdrawal day."

Thus, the argument that "the $200 million of fresh capital (assuming only 10% flows back and buys in) encounters maximum fear" is likely to evolve into a catalyst for short-term pullback. The market will not only fail to gain the expected incremental funds for support but will also have to bear the liquidity vacuum created by some profit-taking positions exiting completely.

The fourth round of distribution from FTX presents a thought-provoking proposition for cryptocurrency financial practitioners: in a highly transparent yet barrier-free decentralized network, how can native wealth accumulation resist the systematic arbitrage of massive external capital at the cycle bottom?

When retail investors are forced to surrender their blood-soaked chips during a prolonged bear market, only to ultimately nourish the balance sheets of Wall Street, the so-called "financial democratization" of cryptocurrencies may still require a much longer evolution and reconstruction.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。