From the development of the liquidity mining model of DeFi protocols to the adoption of centralized elements.

Author: DeSpread Research

Disclaimer: The content of this report reflects the views of the respective authors, is for reference only, and does not constitute advice to buy or sell tokens or use protocols. Any content in this report does not constitute investment advice and should not be understood as investment advice.

1. Introduction

Decentralized Finance (DeFi) is a new form of finance aimed at achieving trustless transactions through blockchain and smart contracts, increasing opportunities for regions lacking financial infrastructure to access financial services, and disrupting traditional financial systems by enhancing transparency and efficiency. The origin of DeFi can be traced back to the development of Bitcoin by Satoshi Nakamoto during the global financial crisis in 2008.

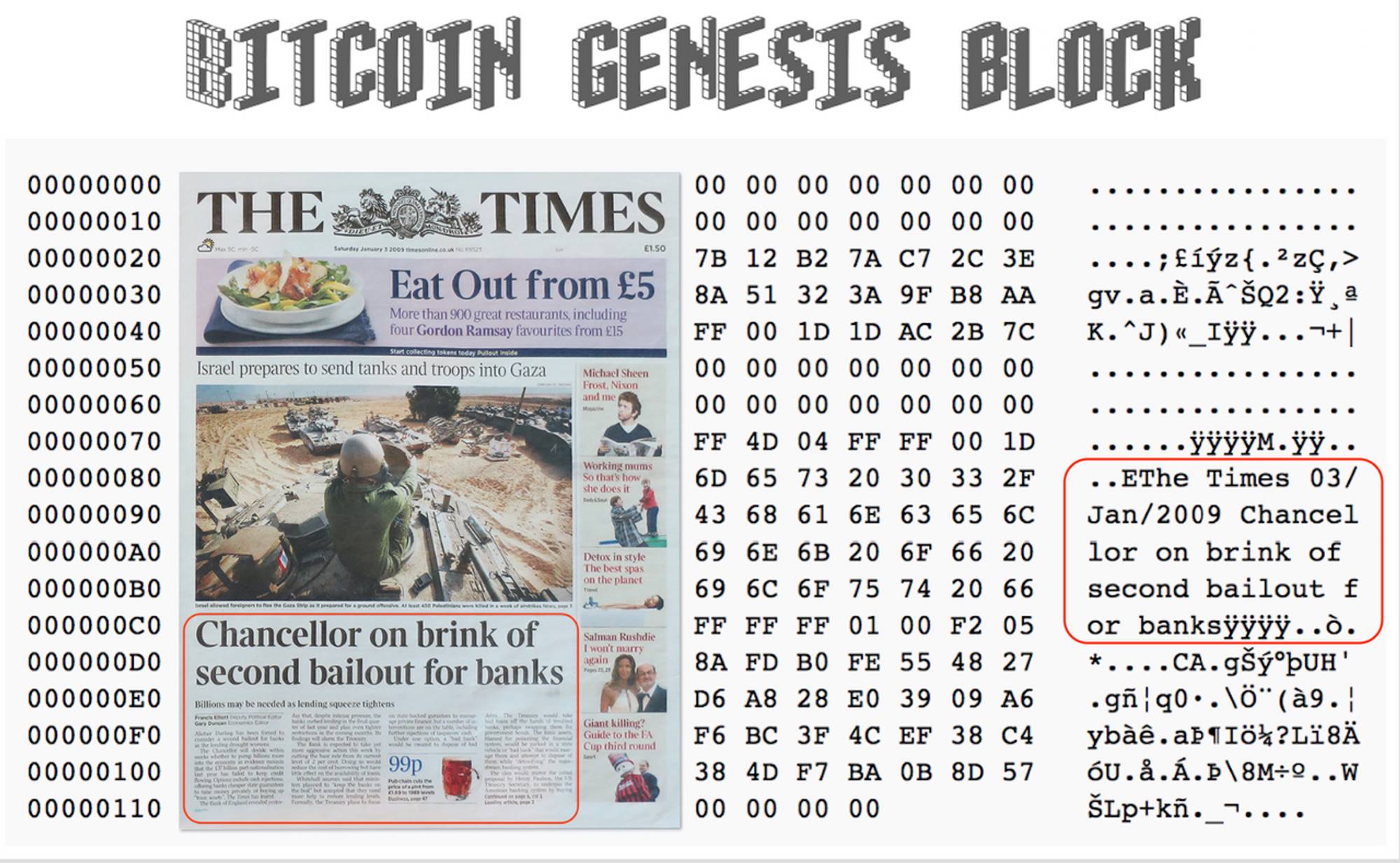

During the 2008 global financial crisis, Satoshi Nakamoto was concerned about the repeated news of bank failures and government bailouts of banks. He believed that over-reliance on trusted institutions, lack of transparency, and inefficiency were fundamental problems of centralized financial systems. To address this issue, Satoshi Nakamoto developed Bitcoin, a system that provides value transfer and payments in a decentralized environment. In the genesis block of Bitcoin, Satoshi Nakamoto included the message "The Times 03/Jan/2009 Chancellor on brink of second bailout for banks," indicating the problems Bitcoin aimed to solve and the demand for decentralized finance.

Bitcoin genesis block and London Times front page, source: phuzion7 steemit

Subsequently, the emergence of Ethereum in 2015 and the introduction of smart contracts gave rise to a series of DeFi protocols. Until now, these protocols have been providing financial services such as token exchange and lending without intermediaries, based on the "decentralized finance" concept proposed by Satoshi Nakamoto, and have been continuously undergoing large-scale experimentation and research. These protocols have formed a vast ecosystem through the ability to combine and connect like "MoneyLego," and have achieved a wide range of financial transactions in a decentralized form that Bitcoin could not provide, opening up the possibility of replacing trusted institutions in traditional financial systems with blockchain.

However, so far, the rapid growth of liquidity in the DeFi market mostly comes from the yield provided to liquidity providers by various protocols, rather than from decentralization or financial system innovation. In particular, these protocols have effectively attracted many users by providing various incentives beyond traditional finance through their token economies, known as "Yield Farming," and have played a significant role in bringing liquidity into the DeFi market.

As users increasingly focus on higher yields, the revenue models of DeFi protocols have evolved from the initial design based on the core value of "providing intermediary-free financial services" to meeting the market demand for "continuously providing users with stable and high returns." Recently, some protocols have even emerged that borrow centralized elements, distributing revenue to users by using real-world assets as collateral or executing trades through centralized exchanges.

In this article, we will explore the various mechanisms and evolutionary processes of DeFi and gain a deep understanding of the challenges faced by these DeFi protocols in partially adopting centralized elements.

2. Liquidity Mining and DeFi Summer

Early DeFi protocols on the Ethereum network focused on implementing traditional financial systems on the blockchain. Therefore, early DeFi protocols, in addition to changing the transaction environment on the blockchain and removing service providers, were no different from traditional finance in terms of generating income and structure.

Decentralized Exchanges (DEX): Similar to currency exchanges and stock exchanges, income is generated through transaction fees. Users receive a certain percentage of fees from each token transaction, which is distributed to liquidity providers.

Lending Protocols: Similar to banks, income is generated from the interest rate difference between depositors and borrowers or collateral. Depositors provide assets to the protocol and receive interest, while borrowers provide collateral to borrow and pay interest.

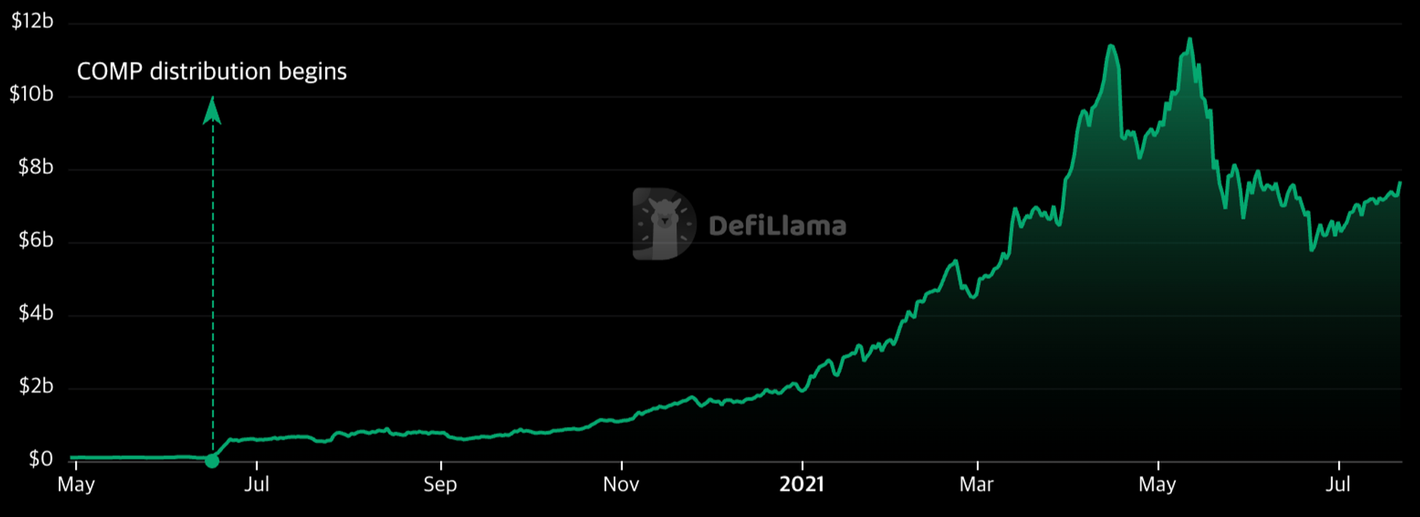

Subsequently, in June 2020, the most representative lending protocol Compound launched the Liquidity Mining activity, attracting liquidity in the market before and after the Bitcoin halving by issuing governance token $COMP and distributing it to liquidity providers and borrowers, leading to a significant increase in liquidity and lending demand on Compound.

Compound TVL changes, source: Defi Llama

Under the initiative of Compound, DeFi protocols began to change from the trend of simply distributing protocol income to liquidity providers. Other early DeFi projects such as Aave and Uniswap also started to issue their own tokens to pay rewards in addition to protocol income. Since then, the DeFi ecosystem has seen a large influx of users and liquidity, leading to the well-known "DeFi Summer" across the entire Ethereum network.

3. Limitations of Liquidity Mining and Improvement of Token Economy

Liquidity mining has provided strong incentives for service providers and users to use services, greatly increasing the liquidity of DeFi protocols and expanding the user base. However, the additional income generated through liquidity mining in the early stages has several limitations.

The utility of the issued tokens is limited to governance, lacking a buying factor.

A decrease in token price leads to a decrease in liquidity mining rates.

These limitations make it difficult to sustain the liquidity and user traffic attracted through liquidity mining in the long term. Subsequent DeFi protocols have attempted to establish token economic models that enable them to provide additional income to liquidity providers beyond protocol income and sustain the introduction of liquidity into the protocol in the long term. Many protocols link the value of their tokens to protocol income and provide continuous incentives to token holders, thereby enhancing the stability and sustainability of the protocol.

Curve Finance and Olympus DAO are the two best examples in this regard.

3.1. Curve Finance

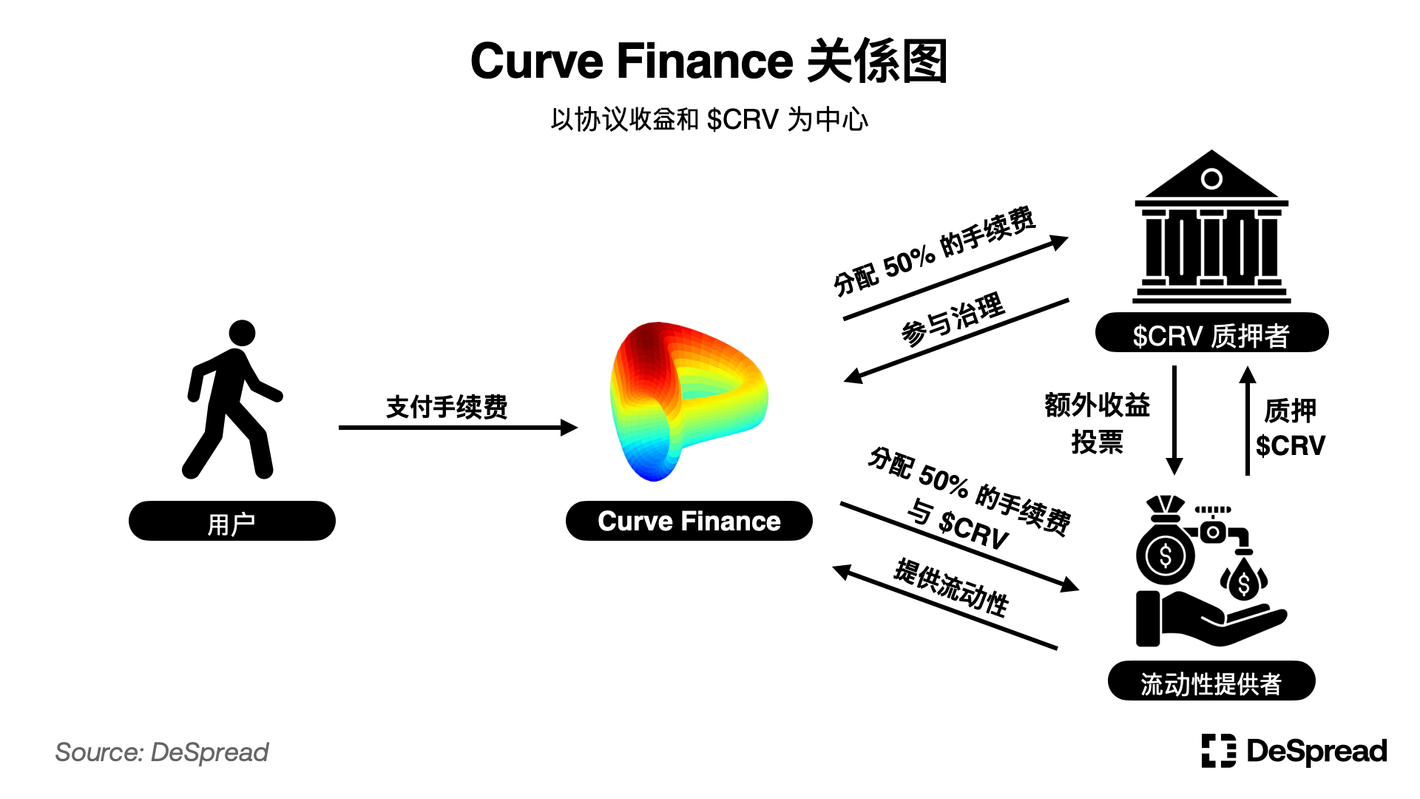

Curve Finance is a DEX that provides low slippage trading for stablecoins. Curve rewards liquidity providers with its own token $CRV and a portion of the trading fees taken from the liquidity pools as liquidity mining rewards. However, Curve Finance has improved the sustainability of liquidity mining by introducing the "veTokenomics" system.

Liquidity providers only receive 50% of the trading fees and do not sell the $CRV obtained from liquidity mining on the market. Instead, they deposit it into Curve Finance for a set period (up to 4 years) and receive $veCRV.

Holders of $veCRV can earn 50% of the trading fees generated by Curve Finance and further increase liquidity mining rewards by participating in voting for the liquidity pools.

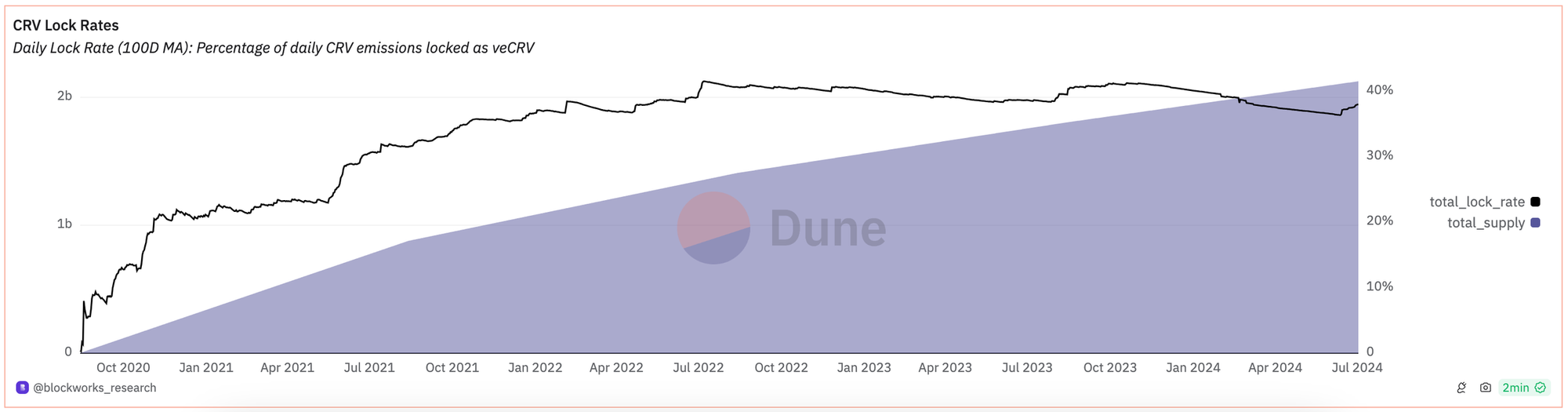

Curve Finance allows liquidity providers to lock up the $CRV tokens they receive for a long time, thereby reducing selling pressure. Additionally, by introducing voting, specific liquidity pools can receive additional rewards, increasing the demand for projects hoping to provide liquidity to Curve Finance to purchase and hold $CRV in the market.

As a result of these effects, the lock-up ratio of $CRV tokens has rapidly increased, reaching 40% within a year and a half, and has been maintained to this day.

Source: @blockworks_research Dune Dashboard

This mechanism of Curve Finance is considered a good attempt, not only to provide high returns to ensure short-term liquidity, but also to pursue sustainability by closely integrating its token with the protocol's operation, becoming an inspiration for the token economic models of many subsequent DeFi protocols.

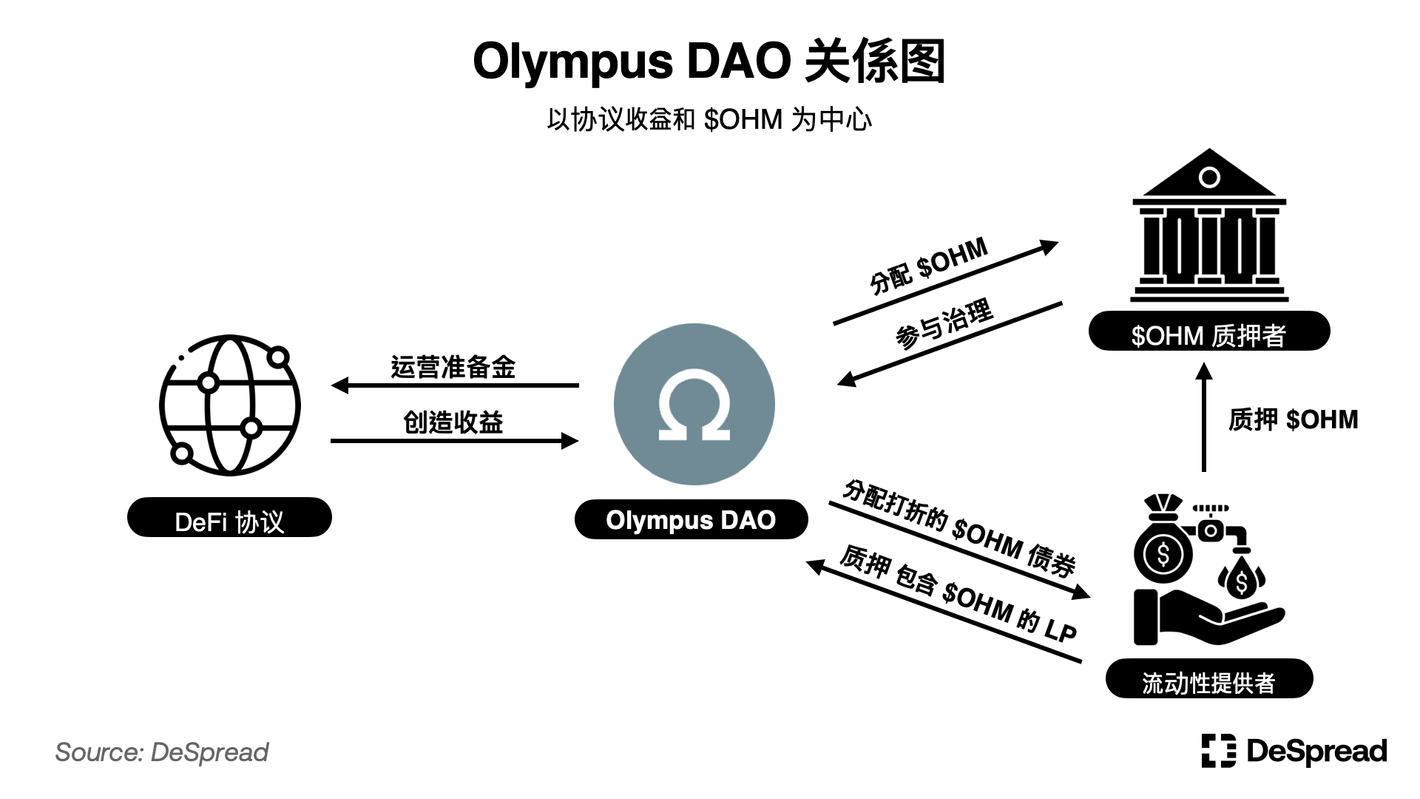

3.2. Olympus DAO

Olympus DAO is a protocol aimed at creating on-chain reserves. Olympus DAO accepts user liquidity deposits to establish and manage reserves, and issues its protocol token $OHM in proportion to the reserves. In the process of issuing $OHM, Olympus DAO introduces a unique mechanism called "bonding," allowing users to deposit LP tokens containing $OHM and issue bonds corresponding to $OHM.

Users can deposit LP tokens consisting of single assets (such as Ethereum, stablecoins, or OHM-asset pairs) and receive discounted OHM bonds as a reward. Olympus DAO will manage these assets through governance to generate income.

By staking $OHM on Olympus DAO, $OHM holders receive a portion of the protocol's reserve growth in the form of $OHM tokens.

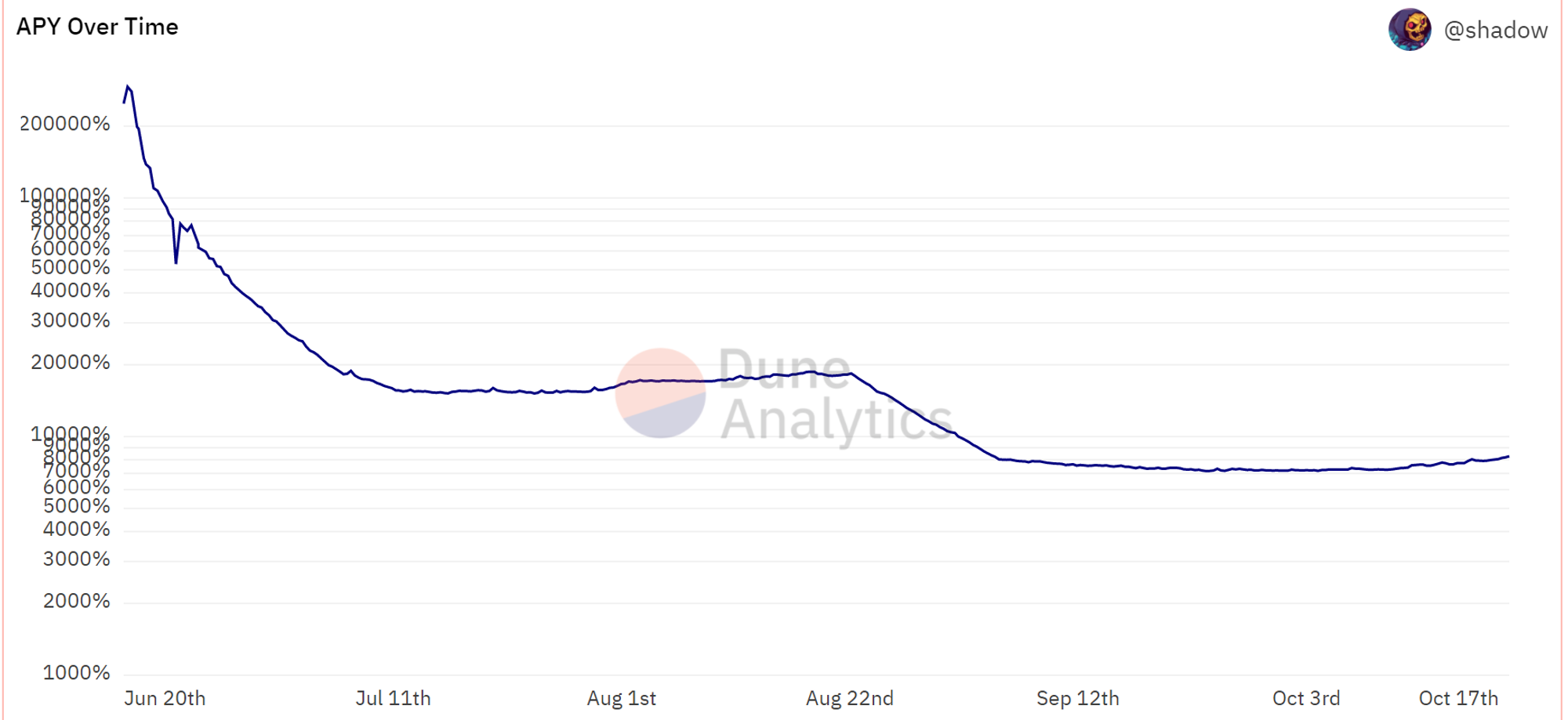

Through the above mechanism, Olympus DAO provides ample $OHM to the market while directly holding LP tokens with ownership of the liquidity pools to prevent traditional liquidity providers from easily withdrawing liquidity for short-term gains. In the early stages of the protocol, a large amount of liquidity flowed in and increased reserves. During the process of issuing more $OHM to pay holders, the annual percentage yield (APY) exceeded 7,000% and lasted for about six months.

Source: @shadow Dune Dashboard

These high annual yields incentivized users to continue depositing assets into Olympus DAO's treasury to mint $OHM, leading to the launch of many DeFi protocols adopting Olympus DAO's mechanism in 2021.

4. Rise of DeFi Bear Market and Real Yield

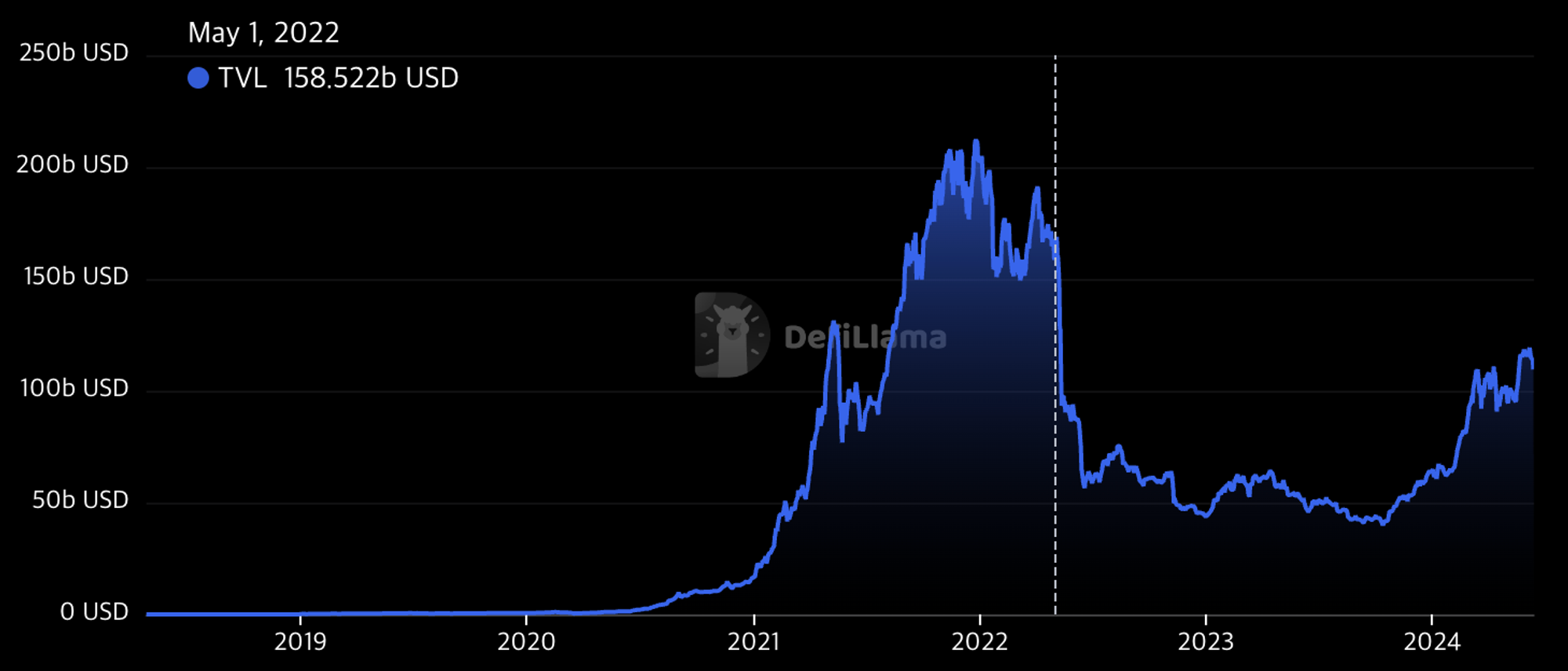

The rise of DeFi protocols led to an unprecedented high total value locked (TVL) in the DeFi market in November 2021. However, the market subsequently entered a correction phase, with a gradual decrease in liquidity inflow, and ultimately, the collapse of the Terra-Luna ecosystem in May 2022 led to a full-fledged bear market. This reduced the overall market liquidity, not only dampening investor sentiment but also impacting early and second-generation DeFi protocols such as Curve Finance and Olympus DAO.

Source: Defi Llama

While the token economic models adopted by these protocols to some extent overcame the limitations of their tokens' lack of utility, the issue of the token's value affecting liquidity provider rates still exists, especially in an environment of constantly changing market conditions and significantly reduced investor sentiment. The income of these protocols cannot keep up with the continuous inflation of the tokens, showing structural limitations of these protocols.

Therefore, the decrease in token value and protocol income accelerated the outflow of assets deposited in the protocols, leading to a vicious cycle, making it difficult for the protocols to generate stable income and provide attractive rates for users. In this situation, DeFi protocols that can significantly limit the inflation rate of their tokens while generating sustainable income for the protocol, known as "Real Yield" DeFi protocols, have become a new focus.

4.1. GMX

One of the most famous Real Yield DeFi protocols is the GMX protocol, a decentralized perpetual contract exchange based on the Arbitrum and Avalanche networks.

The GMX protocol has two tokens, $GLP and $GMX, with the following operating mechanisms.

Liquidity providers deposit assets such as $ETH, $BTC, $USDC, $USDT into GMX and receive $GLP tokens as proof of providing liquidity, while $GLP holders can receive 70% of the income generated by the GMX protocol.

$GMX is the governance token of the GMX protocol, and stakers of $GMX receive discounts on GMX trading fees and linearly receive 30% of the income generated by the GMX protocol within a year. ```

The GMX protocol does not provide additional rewards through token inflation, but chooses to allocate a portion of the protocol's generated income to its token holders. This approach provides clear incentives for users to buy and hold $GMX, ensuring that token holders do not sell the tokens for profit and do not face inflation devaluation issues in a market downturn.

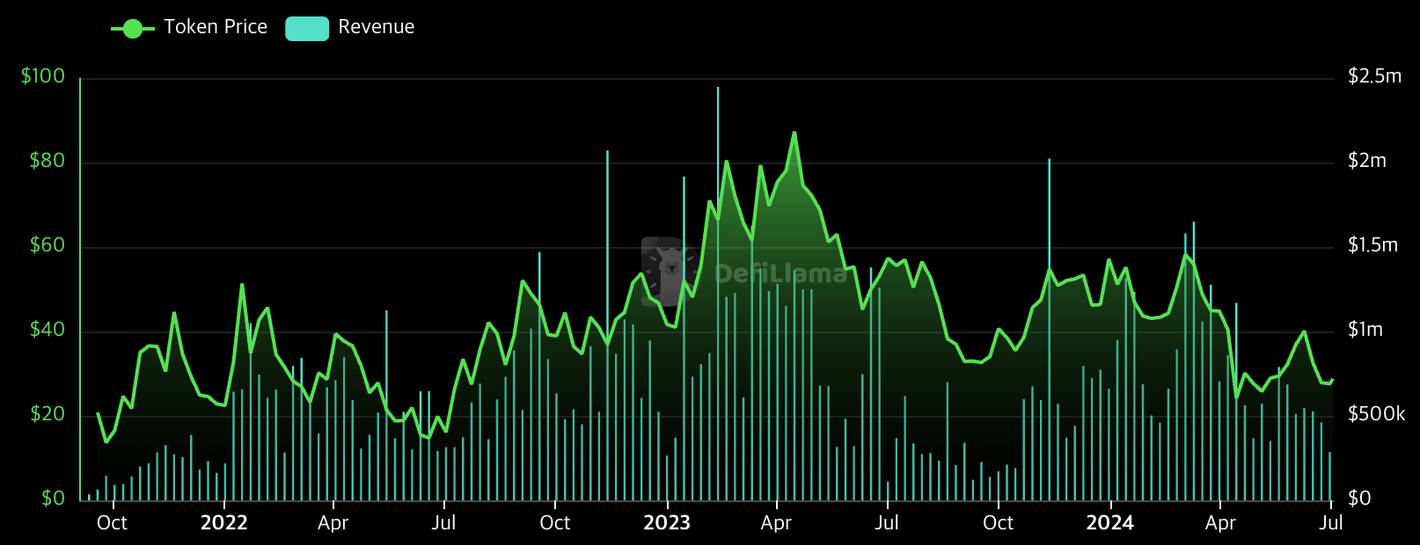

By observing the income of the GMX protocol and the fluctuation of the $GMX token price, it can be seen that the value of the $GMX token fluctuates with the income of the GMX protocol.

GMX Protocol Income and Token Price Trend, Source: Defi Llama

However, compared to traditional protocols, this structure allocates a portion of the fees that liquidity providers deserve to governance token holders, which is somewhat disadvantageous to liquidity providers and not ideal for attracting initial liquidity. Additionally, when distributing the governance token $GMX, the GMX protocol focuses on airdropping to DeFi users on Arbitrum and Avalanche, aiming to promote the GMX protocol to potential users, rather than quickly gaining liquidity through liquidity mining activities.

Nevertheless, the GMX protocol is currently the protocol with the highest TVL among derivative DeFi protocols and is one of the platforms that has maintained its TVL after the bear market following the Luna-Terra incident.

GMX Protocol TVL Trend, Source: Defi Llama

Compared to other DeFi protocols, despite the structural disadvantage to liquidity providers, the GMX protocol continues to perform well for several reasons:

It emerged as a decentralized perpetual contract exchange during the peak of the Arbitrum network, leading to the capture of liquidity and user traffic within Arbitrum.

After the bankruptcy of FTX in December 2022, there was a decrease in confidence in centralized exchanges, leading to an increased demand for on-chain exchanges.

The GMX protocol is able to somewhat offset its structural disadvantages based on these external factors, making it difficult for subsequent DeFi protocols to replicate the structure of the GMX protocol while attracting liquidity and users.

On the other hand, the early decentralized exchange Uniswap is discussing the introduction of a Fee Switch mechanism to distribute protocol income to holders of the $UNI token previously distributed through liquidity mining and liquidity providers. This indicates that Uniswap is also considering transitioning to a real yield DeFi protocol. However, this is only possible because Uniswap, as one of the earliest projects, has already gained enough liquidity and trading volume.

From the cases of the GMX protocol and Uniswap, it can be observed that adopting real yield, distributing protocol income to both liquidity providers and token holders, should be carefully considered based on the maturity of the protocol and its position in the market. Under this model, ensuring liquidity is the most important challenge, which is also why early projects have not widely adopted it.

5. RWA: Integrating Traditional Financial Instruments into DeFi

In the continued bear market, attracting limited liquidity through token economics while ensuring the sustainability of protocol income remains the biggest challenge for DeFi protocols.

In September 2022, after Ethereum transitioned from proof of work (PoW) to proof of stake (PoS) through The Merge update, there have been protocols assisting users in participating in Ethereum staking to allocate interest to users. This change made Ethereum's 3% interest the most basic default rate, forcing emerging DeFi protocols to increase sustainable returns to attract liquidity and maintain the protocol's environment.

In this context, protocols based on Real World Assets (RWA) began to emerge. These protocols naturally became an alternative in the DeFi ecosystem that can provide sustainable returns by linking traditional financial instruments to the blockchain and generating income outside the blockchain environment.

RWA refers to the tokenization of any traditional financial instrument on the blockchain, allowing users to use real-world assets in the on-chain environment, and these protocols can benefit in the following ways:

Transparently recording asset ownership and transaction history compared to traditional systems.

Increasing the inclusivity of financial services without geographical, status, and other criteria.

Providing flexible and efficient trading forms, such as micro-splits or integration with DeFi protocols.

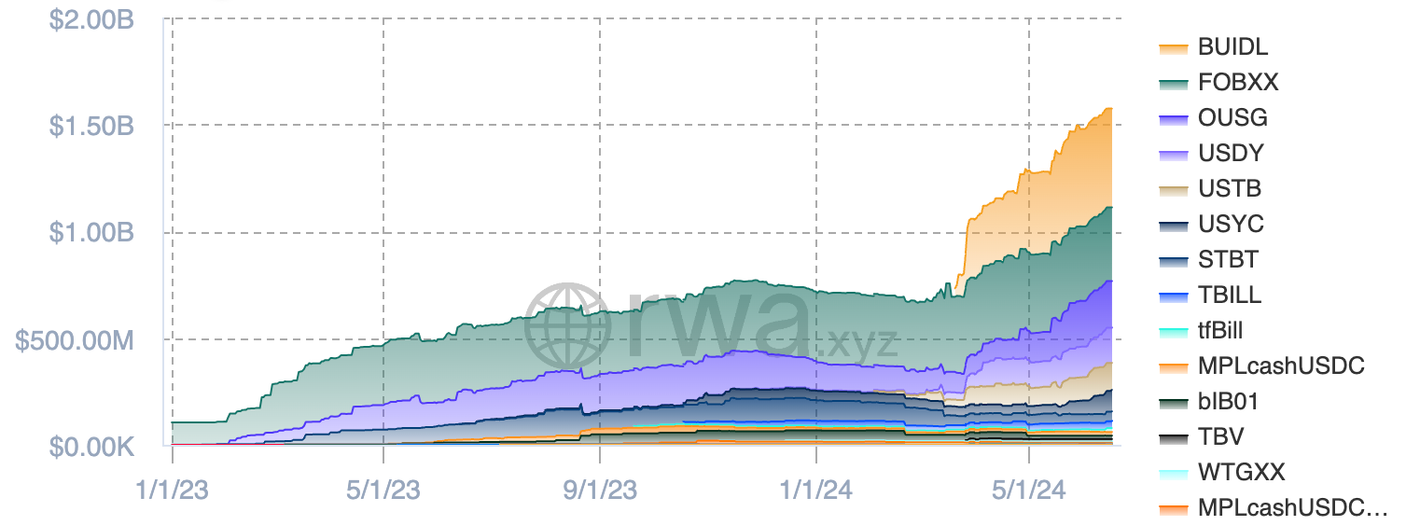

These advantages have led to a wide range of RWA cases, including bonds, stocks, real estate, and unsecured credit loans. The tokenization of U.S. Treasury bonds is particularly noteworthy, meeting users' demand for stable value and returns.

Currently, there are approximately $1.57 billion worth of tokenized U.S. Treasury bond assets on-chain, and with global asset management companies such as BlackRock and Franklin Templeton entering this field, RWA has become an important part of the DeFi market.

Market Value Trend of Tokenized U.S. Treasury Bonds, Source: rwa.xyz

Next, we will provide an example of a DeFi protocol that provides returns to users using the RWA model.

5.1. Goldfinch

Goldfinch is a lending protocol that has been pioneering the integration of DeFi with traditional financial products since July 2020. The protocol provides unsecured cryptocurrency loans to real-world businesses around the world based on its proprietary credit scoring system, with most borrowers located in developing countries in Asia, Africa, and South America. The total funds lent out and operational funds currently amount to approximately $76 million.

Goldfinch has two different loan pools.

Junior Pool: Established when borrowers apply for loans and pass the verification process. Verified entities such as professional investment institutions and credit analysts deposit funds into the pool to lend to these borrowers. If there is a default, the funds in the junior loan pool will be used first to cover the losses.

Senior Pool: Positions from individual pools are diversified across all junior loan pools, with the condition of prioritizing the protection of principal, and the returns paid are lower than those of the junior loan pool.

After completing the KYC process, users can deposit $USDC into the senior loan pool to receive a share of the income generated by Goldfinch through credit collateralized lending, while also receiving $FIDU tokens as proof of providing liquidity. When users want to withdraw, they can only deposit $FIDU and receive a return of $USDC if there is idle capital in the senior loan pool. If there is no idle capital in the senior loan pool, users can still sell $FIDU on a DEX to achieve the same effect. Conversely, users can also buy $FIDU tokens on a DEX and receive income generated by Goldfinch without undergoing KYC.

During its initial launch, Goldfinch distributed its governance token $GFI through liquidity mining, attracting a large amount of liquidity. Even after the end of liquidity mining activities and the Luna-Terra incident, when the market entered a downturn, Goldfinch continued to receive stable net income from external sources, providing liquidity providers with a stable expected interest rate of about 8%.

However, from August 2023 to the present, Goldfinch has experienced three defaults, exposing issues such as poor credit assessment and lack of up-to-date loan information, casting doubt on the sustainability of the protocol. In response, liquidity providers have started selling their $FIDU tokens on the market. Considering the income the protocol can generate, the price of $FIDU should rise. However, as of June 2024, the value of $FIDU is still at $0.6, down from $1.

5.2. MakerDAO

MakerDAO is an early Collateralized Debt Position (CDP) protocol in the Ethereum DeFi ecosystem, aimed at issuing and providing users with stablecoins collateralized with stable value, to cope with the volatile cryptocurrency market.

Users can collateralize virtual assets such as Ethereum with MakerDAO and receive $DAI in return. MakerDAO continuously monitors the fluctuation in the value of collateral assets to measure the collateralization ratio and liquidates collateral assets when the collateralization ratio falls below a certain level to maintain a stable reserve.

MakerDAO has two main revenue models:

Stability Fee: Fees paid by users who deposit collateral and issue and borrow $DAI.

Liquidation Fee: Fees charged when collateral assets of $DAI issuers are forcibly liquidated due to their value falling below a certain level.

MakerDAO has a mechanism to incentivize $DAI holders, using these fees to pay interest to users who deposit $DAI into MakerDAO's savings system "DSR contract," and using any remaining capital to purchase and burn MakerDAO's governance token $MKR to incentivize $MKR holders.

5.2.1. Endgame and RWA Introduction

In May 2022, MakerDAO co-founder Rune Christensen proposed the "Endgame" plan, representing the true decentralization of MakerDAO governance and operations, and the long-term vision for DAI stability.

For more information on "Endgame," please refer to the Endgame series published by DeSpread.

As mentioned in Endgame, one of the key challenges to ensuring the stability of $DAI is to diversify the collateral assets, which are currently primarily based on $ETH. MakerDAO has announced plans to introduce RWA as collateral assets to achieve the following advantages:

RWA has price fluctuation characteristics different from crypto assets, allowing for portfolio diversification.

RWA supported by real-world assets helps reduce friction with regulatory authorities and gain the trust of institutional investors.

RWA strengthens the connection between the MakerDAO protocol and the real economy, ensuring long-term stability and growth of $DAI outside the blockchain.

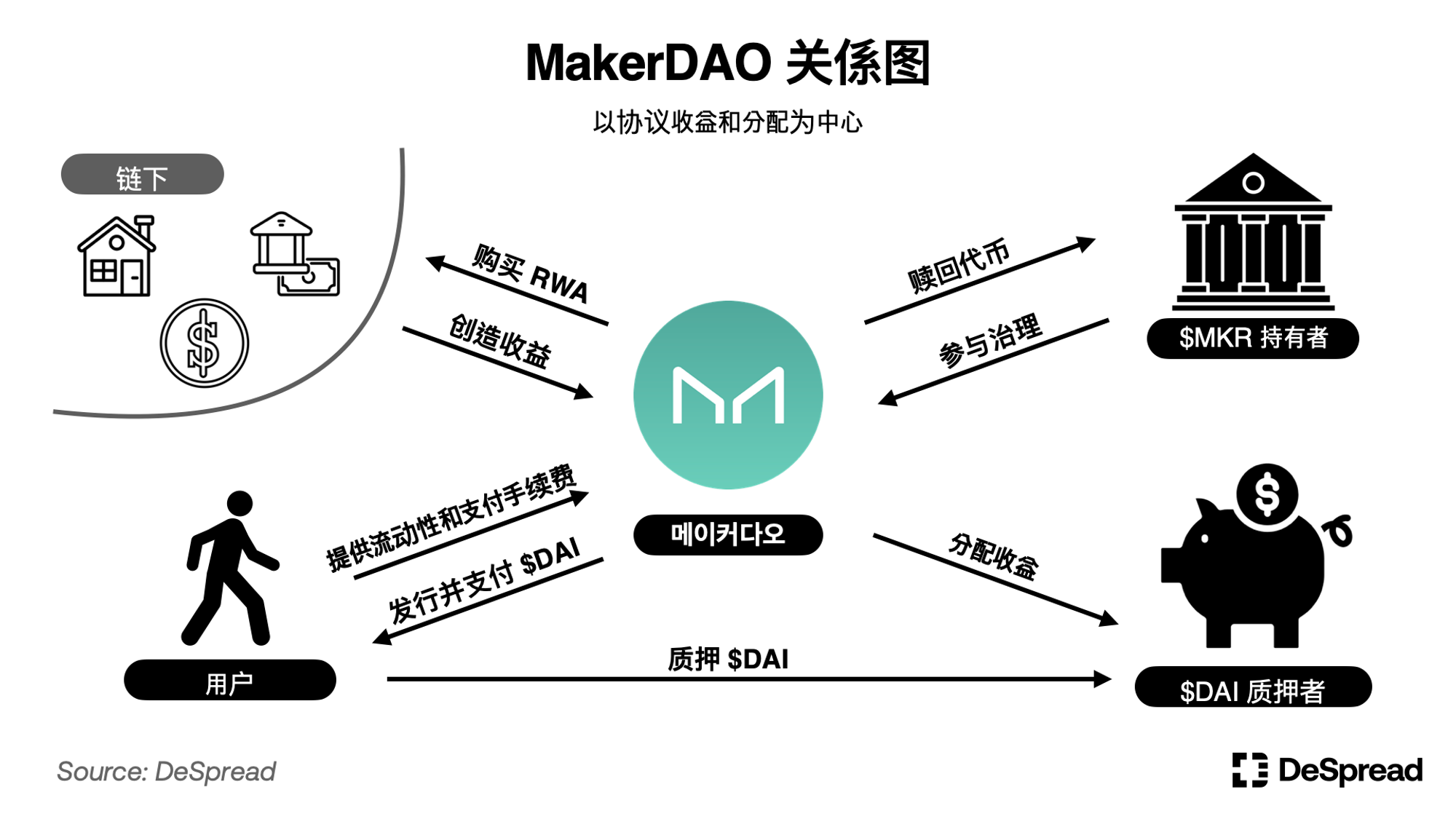

After the Endgame proposal was approved, MakerDAO's relationship diagram is as follows.

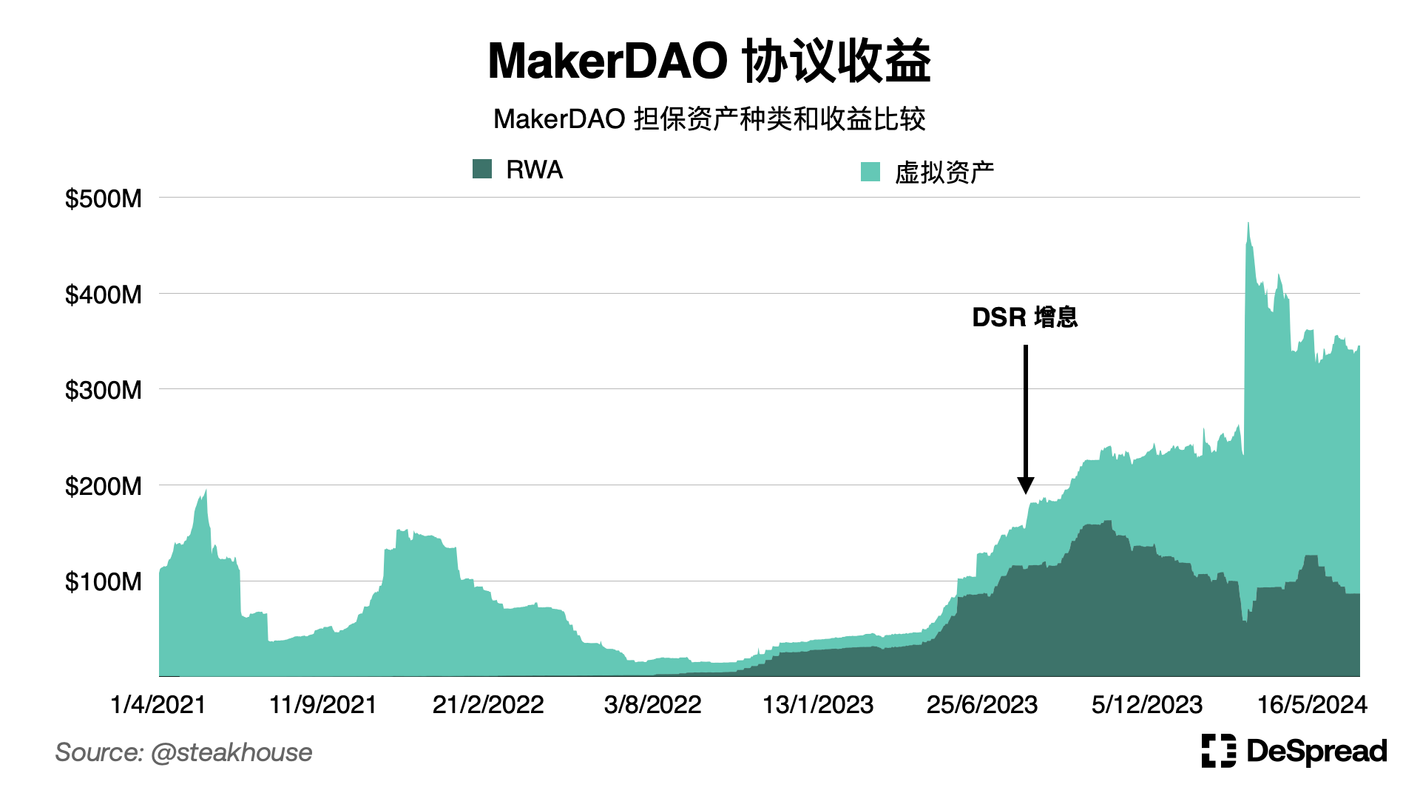

After the Endgame proposal was approved, MakerDAO diversified its portfolio by introducing various forms of RWA, including short-term U.S. Treasury bonds, real estate-backed loans, tokenized real estate, and credit-backed assets. As the income generated through RWA is determined by factors such as government bond rates and off-chain lending rates, MakerDAO has reduced its exposure to cryptocurrency market fluctuations through the integration of RWA and gained a stable source of returns.

As a result, in 2023, despite the entire DeFi ecosystem experiencing a bear market, MakerDAO's RWA-backed assets continued to generate stable income, accounting for 70% of the protocol's total income. Based on this income, MakerDAO was able to increase and maintain the DSR interest rate from 1% to 5%, effectively supporting the demand for $DAI.

In this way, MakerDAO, starting as a protocol that issues stablecoins collateralized with on-chain assets, has diversified its income sources through engagement with real-world finance, strengthened its connection with the real economy, and ensured the sustainability and long-term growth of the protocol, making MakerDAO a leading RWA protocol and pointing to a new direction for the integration of traditional finance and DeFi.

6. Arbitrage Trading: Utilizing CEX Liquidity Attempts

In the fourth quarter of 2023, with the expected approval of a Bitcoin spot ETF, external liquidity began flowing into the market after nearly two years of stagnation. This prompted the DeFi ecosystem to move away from traditional passive management structures and use the incoming liquidity and its own token incentive mechanisms to provide higher interest rates to attract new liquidity.

Unlike early projects, these protocols did not engage in the popular liquidity mining at the beginning. Instead, they used a model of distributing rewards based on points to increase the interval between the period of attracting liquidity and the airdrop, allowing the team to better manage the circulation of their tokens.

Some protocols also quickly attracted a large amount of liquidity through the "restaking" model, using tokens that had already been staked with other protocols as collateral assets to compound risk and generate additional income.

Although the cryptocurrency market has experienced a recovery after the Luna-Terra crisis, the high barrier to entry into the on-chain environment has resulted in most of the market's liquidity and user traffic still being concentrated in CEX rather than DeFi protocols.

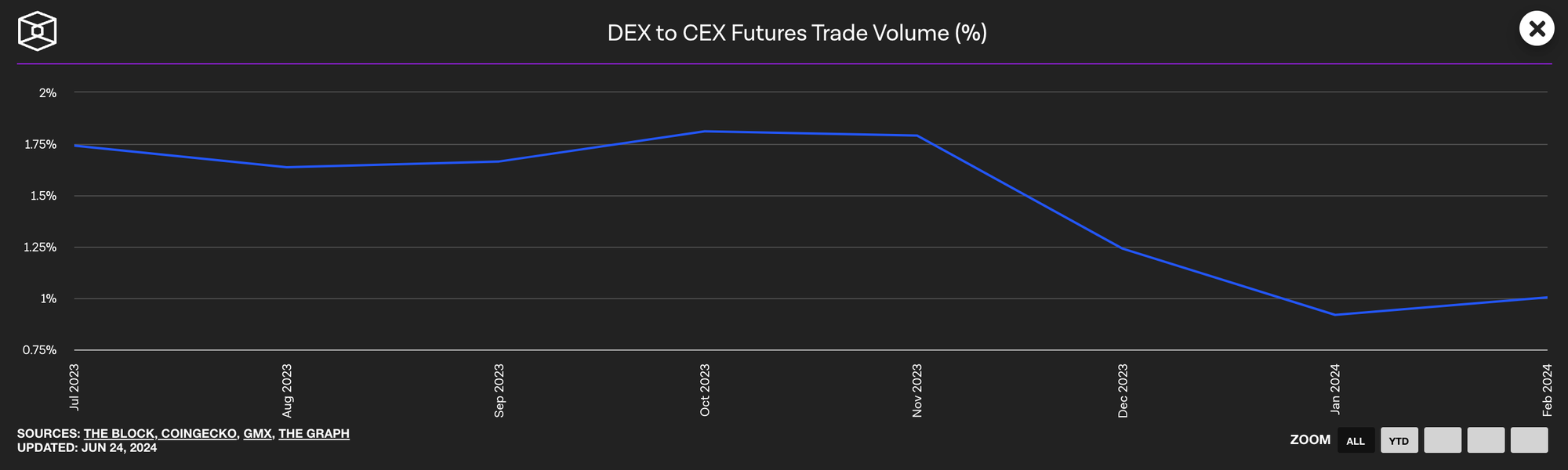

Especially, CEX provides users with a more familiar and simple trading environment, leading to a temporary decrease in the trading volume of on-chain perpetual contract exchanges to about 1% of the CEX futures trading volume. This environment has driven the rise of Basis Trading model protocols that utilize the trading volume and traffic on CEX to create additional income.

Comparison of futures trading volume between CEX and DEX, Source: The Block

The Basis Trading model uses assets deposited by users to create positions and generate income by capturing price differences between spot and futures or between futures of the same asset on CEX, and distributes it to liquidity providers. Compared to the RWA model, which generates income directly from traditional finance, the advantage of these models is less regulation, allowing for more freedom in building protocol structures and adopting more aggressive market strategies.

In the past, virtual asset custody companies such as Celsius and BlockFi also leveraged the leverage of liquidity providers' assets deposited on CEX to create and distribute income. However, due to opaque fund management and over-leveraged investments, Celsius went bankrupt after the market crash in 2022, and the custody company's model of managing deposited assets lost credibility in the market and gradually disappeared.

Therefore, the protocols based on the Basis Trading model that have emerged in recent years are striving to operate more transparently than traditional custody institutions and have set up various mechanisms to supplement their credibility and stability.

Next, we will explore some protocols that provide income to users through Basis Trading.

6.1. Ethena

Ethena is a protocol that issues the USD synthetic asset $USDe with a value of 1 USD. Ethena uses CEX futures to hedge its collateral assets to ensure that the collateralization ratio does not fluctuate with the value of the collateral assets, maintaining a Delta Neutral state. The protocol can issue USD equivalent to the collateral assets without being affected by market fluctuations.

The assets deposited by users on Ethena are distributed in the form of $BTC, $ETH, interest-bearing Ethereum LST tokens, and $USDT through Off-Exchange Settlement (OES) providers. Subsequently, Ethena hedges its holding of $BTC and $ETH spot collateral assets by opening short positions equivalent to them on CEX to maintain a Delta Neutral state for the held assets.

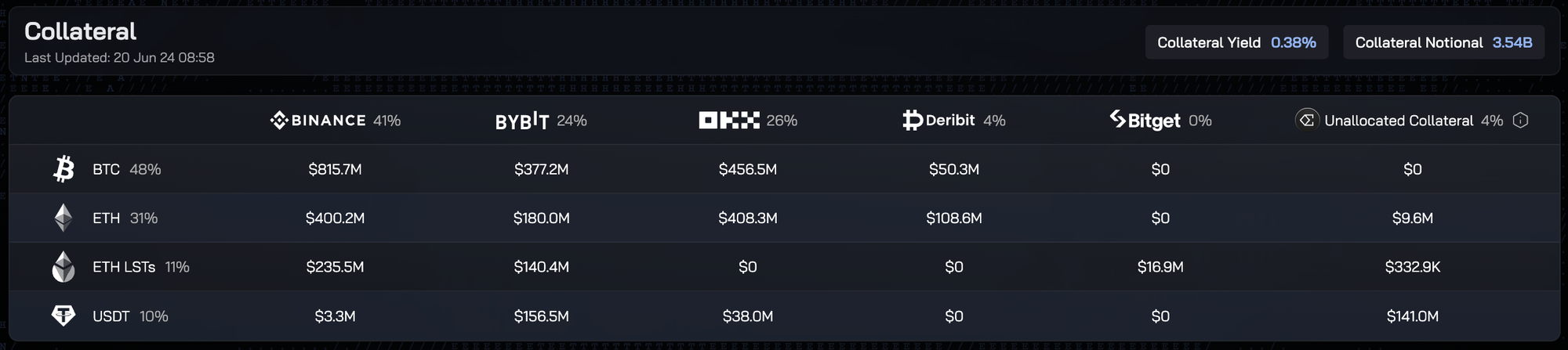

Collateral asset ratio of Ethena, Source: Ethena

During the process of collateralizing USDe, Ethena can receive two types of returns:

LST Interest: Interest generated from Ethereum validation rewards, with an annual interest rate maintained at over 3% and increasing with the increase in Ethereum ecosystem activity. This income can provide a return of about 0.4% per year for the total spot collateral assets.

Funding Fee: Fees paid by users holding overheated positions to users holding opposite positions, used to bridge the gap between spot and futures prices on CEX (considering that there is no limit to long positions and they are at a disadvantage compared to short positions, long users pay 0.01% as the basic funding fee every 8 hours to short users). Currently, Ethereum futures short positions can earn an 8% fee per year based on the unrealized positions.

In addition to distributing the income generated from Basis Trading to $USDe holders, Ethena is also conducting a second airdrop of the governance token $ENA. In this process, Ethena distributes more points to holders than to $USDe stakers to ensure that protocol income is concentrated in a small number of stakers, resulting in a staking rate of 17% for $USDe in June 20, 2024.

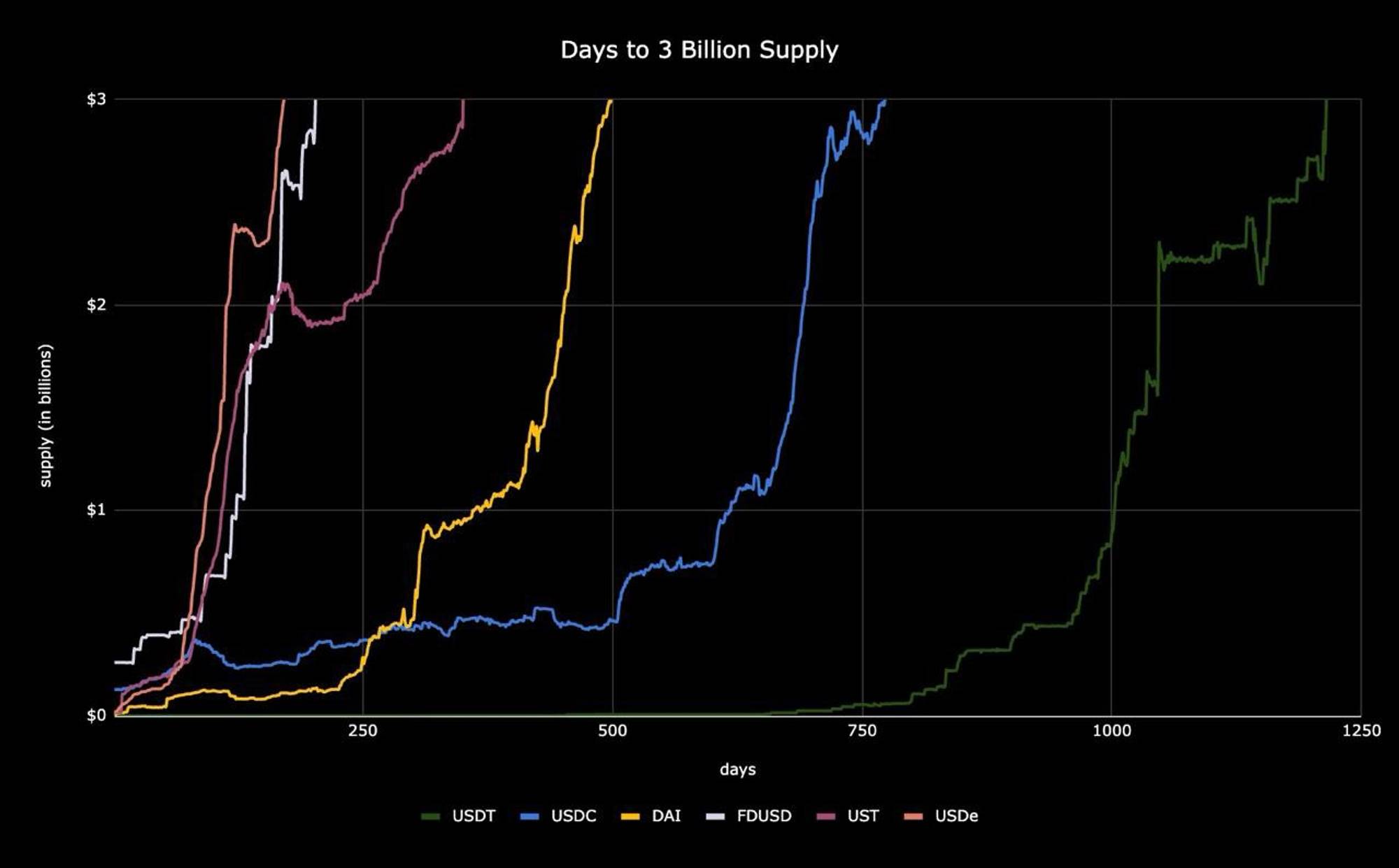

Furthermore, by announcing future plans to provide more airdrops to $ENA stakers, Ethena aims to alleviate selling pressure on $ENA and attract initial liquidity for $ENA. Through these efforts, approximately $3.6 billion of $USDe has been issued to date, making it the stablecoin with the fastest market capitalization reaching $3 billion.

Time taken for stablecoin to reach a market capitalization of $3 billion, Source: @leptokurtic_ on Twitter

6.1.1. Limitations and Roadmap

Although Ethena has achieved some success in rapidly gaining initial liquidity, it faces the following limitations from a sustainability perspective:

Once the points activity ends, the demand for Ethena will decrease, leading to a reduction in staking income.

The interest from the funding fee is variable and fluctuates with market conditions, especially when short positions increase during a bear market, there is a possibility of a decrease.

Currently, the only reason to stake $ENA in Ethena is to earn additional $ENA, so $ENA may face significant selling pressure after the airdrop activity.

To prevent the loss of liquidity for $USDe and $ENA, a collaboration with the staking protocol Symbiotic has recently been announced as the first step to increase the utility of both tokens, by staking $USDe and $ENA on a PoS intermediate protocol that requires secure budgets to earn additional income.

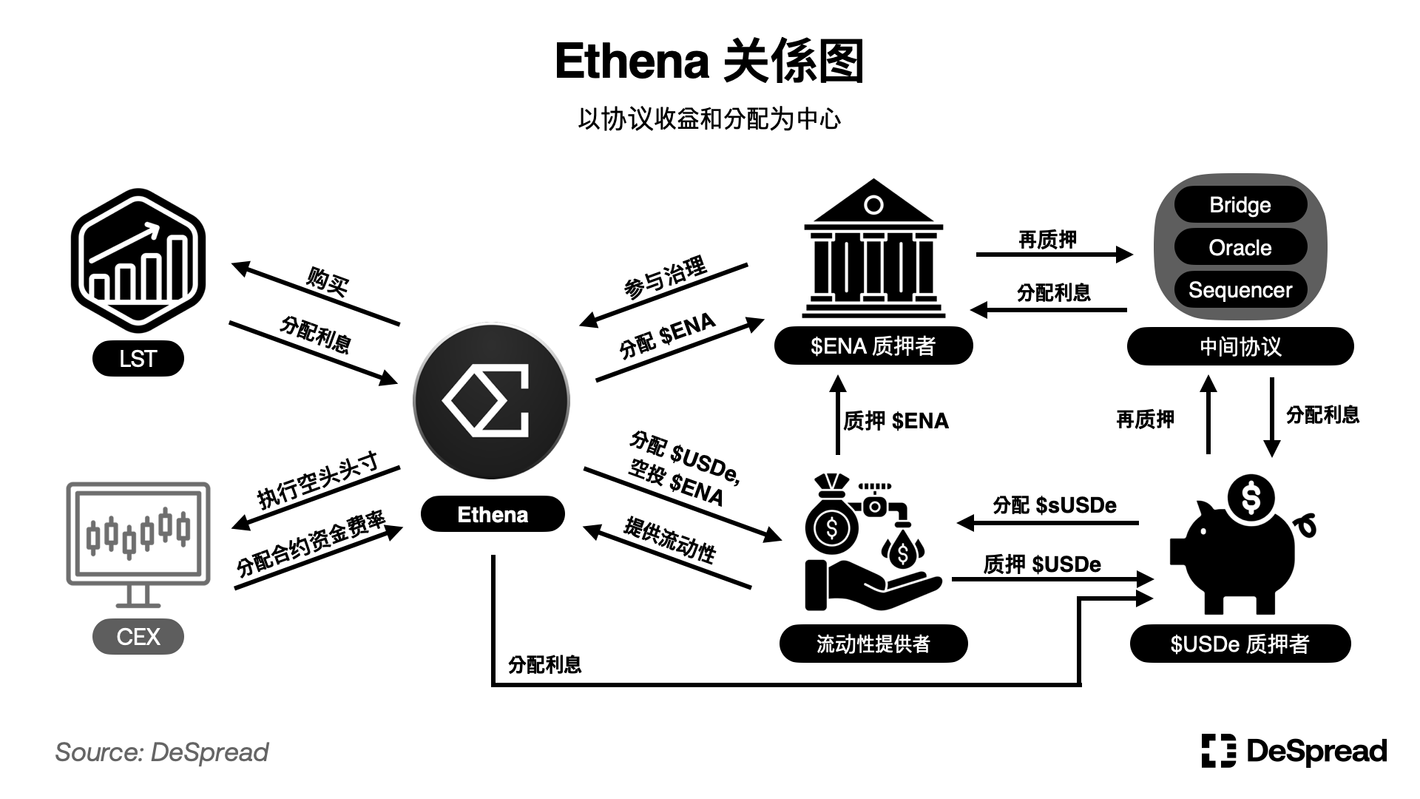

The following is the current relationship of Ethena.

Ethena is addressing the transparency issues of existing asset custody institutions, primarily by publicly disclosing the wallet addresses of OES providers and releasing reports proving the holdings and positions of assets. Furthermore, Ethena plans to use ZK technology to verify all assets held by OES providers in real-time, further enhancing transparency.

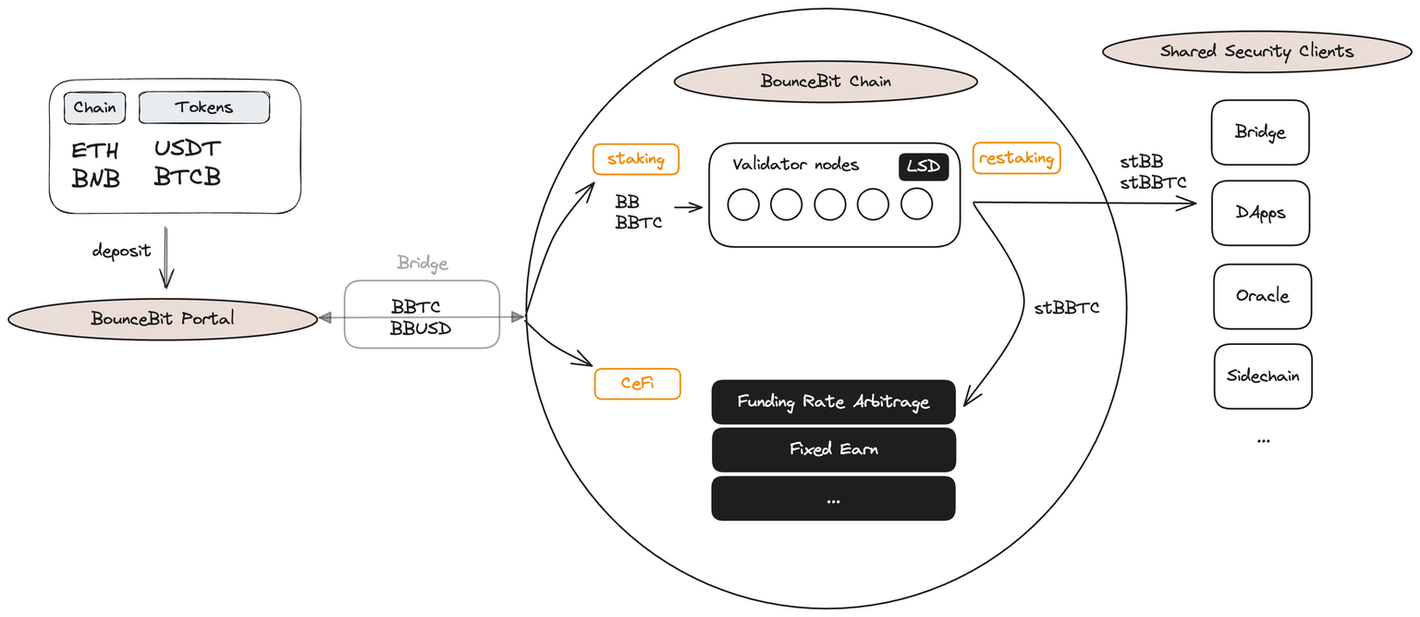

6.2. BounceBit

BounceBit is a PoS-based L1 network that operates Delta Neutral positions on centralized exchanges (CEX) using assets bridged by users to generate additional income. Since June 2024, users can bridge two types of assets from other networks to BounceBit, including $BTCB and $USDT.

The assets bridged by users will be used for Basis Trading on CEX by asset management entities, and BounceBit will pay users the available liquid custody tokens $BBTC and $BBUSD on the network as collateral proof in a 1:1 ratio. Users can use the received $BBTC to stake with BounceBit's native token $BB to assist in network validation work, and stakers will receive proof-of-stake liquidity tokens $stBBTC and $stBB, as well as interest paid in $BB.

Users can also further earn additional income by restaking $stBBTC on Shared Security Clients (SSC) in collaboration with BounceBit, or deposit it into the Premium Yield Generation Vault to receive the income generated from BounceBit's Basis Trading. Currently, the feature to restake with SSC has not been opened, and additional income can only be obtained through the Premium Yield Generation Vault.

BounceBit user fund flow diagram, Source: BounceBit Docs

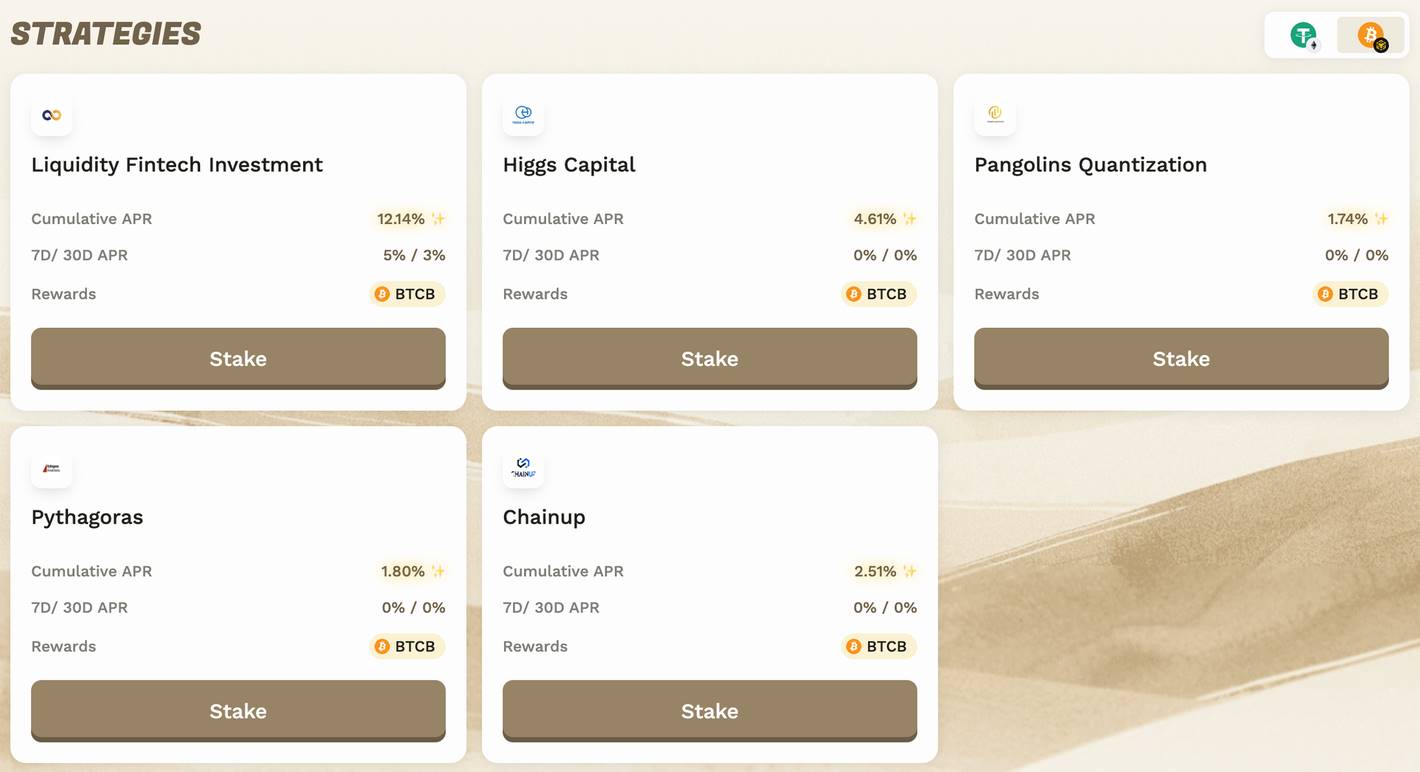

When users deposit assets into the Premium Yield Generation Vault, they can choose from five asset management institutions collaborating with BounceBit to receive profits. These asset management institutions use the MirrorX feature to execute trades on CEX without actually depositing the assets into CEX. BounceBit also regularly publishes asset status reports to ensure the stability and transparency of bridged assets.

BounceBit Premium Yield Generation Vault collaborating institutions, Source: BounceBit

Currently, BounceBit offers a maximum yield of 16%, including 4% network staking interest and a 12% Premium Yield Generation Vault yield, which is quite high for assets based on BTC. However, the sustainability of these yields remains to be observed, as staking interest fluctuates with the price of $BB, and the yield from Basis Trading depends on market conditions.

Compared to the DeFi ecosystem, protocols adopting this emerging Basis Trading model use the trading volume and liquidity on CEX to generate stable income, constituting a key part of protocol income stability. Furthermore, these protocols also provide additional income to users through active DeFi protocol strategies such as the liquidity of staked assets (to facilitate use on other protocols) and issuing their own tokens.

7. Conclusion

In this article, we have explored the evolution of the yield model in the DeFi ecosystem and also understood how protocols maintain income and liquidity through elements such as RWA and Basis Trading. Considering that RWA and Basis Trading models are still in the early adoption stage, we can expect their influence in the DeFi ecosystem to grow.

Although RWA and Basis Trading models borrow elements from centralized systems, their common goal is to bring assets and liquidity from outside the DeFi ecosystem into DeFi protocols. As on-ramp and off-ramp solutions develop to a certain extent in the future and changes focus on cross-chain interoperability, these centralized elements will be replaced, improving the convenience for users in the DeFi ecosystem and leading to the continuous emergence of innovative DeFi protocols based on the increase in blockchain usage.

While these centralized elements currently dominate the DeFi ecosystem, it is contradictory to Satoshi Nakamoto's creation of Bitcoin to solve traditional financial problems. However, considering that the modern financial system has developed based on capital efficiency, it can be explained that it is natural for DeFi as a new form of finance to undergo this transformation.

As DeFi moves towards centralization, we will continue to see the emergence of protocols that prioritize decentralization principles, such as stablecoin protocols Reflexer that are not pegged to the US dollar and have independent price formation systems. These protocols will complement those that introduce centralized elements, creating a balance in the DeFi ecosystem.

We can expect a more mature and efficient financial system, and we can look forward to how blockchain finance, represented by "DeFi," will change and be defined in the future.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。