Author: Chris Powers

Translation: Luccy, BlockBeats

Editor's Note: DeFi researcher Chris Powers explores the new trend in the lending field - modular lending, and provides examples of the potential of modular lending in addressing market challenges and providing better services.

Chris Powers compares traditional DeFi lending leaders (MakerDAO, Aave, and Compound) with several major modular lending projects, including Morpho, Euler, and Gearbox, pointing out the prevalence of modular lending in the DeFi world and emphasizing its positive impact on risk management and value flow.

In the business and technology fields, there is an ancient concept: "There are only two ways to make money in business: bundling and unbundling." This is not only true in traditional industries, but it is more evident in the world of cryptocurrencies and DeFi due to its permissionless nature. In this article, we will explore the surge in modular lending trends (and those who have already entered the post-modular era), and discuss how it is disrupting the mainstream of DeFi lending. With the emergence of unbundling, new market structures have formed new value flows - who will benefit the most?

- Chris

There has been a huge unbundling at the core base layer, where Ethereum previously had only one solution for execution, settlement, and data availability. However, it has adopted a more modular approach, providing specialized solutions for each core element of the blockchain.

The DeFi lending sector is also playing out the same drama. The initially successful products were those that were all-encompassing. Although the initial three DeFi lending platforms - MakerDAO, Aave, and Compound - had many active parts, they all operated under predefined structures set by their respective core teams. However, today, the growth of DeFi lending comes from a new batch of projects that are splitting the core functions of lending protocols.

These projects are creating independent markets, minimizing governance, separating risk management, relaxing oracle responsibilities, and eliminating other single dependencies. Other projects are creating user-friendly bundled products, combining multiple DeFi building blocks to provide more comprehensive lending products.

This new drive to unbundle DeFi lending has become a meme for modular lending. We at Dose of DeFi love memes, but we also see new projects (and their investors) trying to hype up new market topics rather than because of potential innovation (look at DeFi 2.0).

Our view: Hype is not fiction. DeFi lending will undergo a transformation similar to the core technology layer - just like Ethereum, new modular protocols are emerging, such as Celestia, while existing leading companies are adjusting their roadmaps to become more modular.

In the short term, major competitors are opening up different paths. New modular lending projects such as Morpho, Euler, Ajna, and Credit Guild have been successful, while MakerDAO is moving towards a more decentralized SubDAO model. In addition, the recently announced Aave v4 is also moving towards a modular direction, echoing the architecture shift of Ethereum. The paths being opened up now may determine the long-term accumulation of value in the DeFi lending stack.

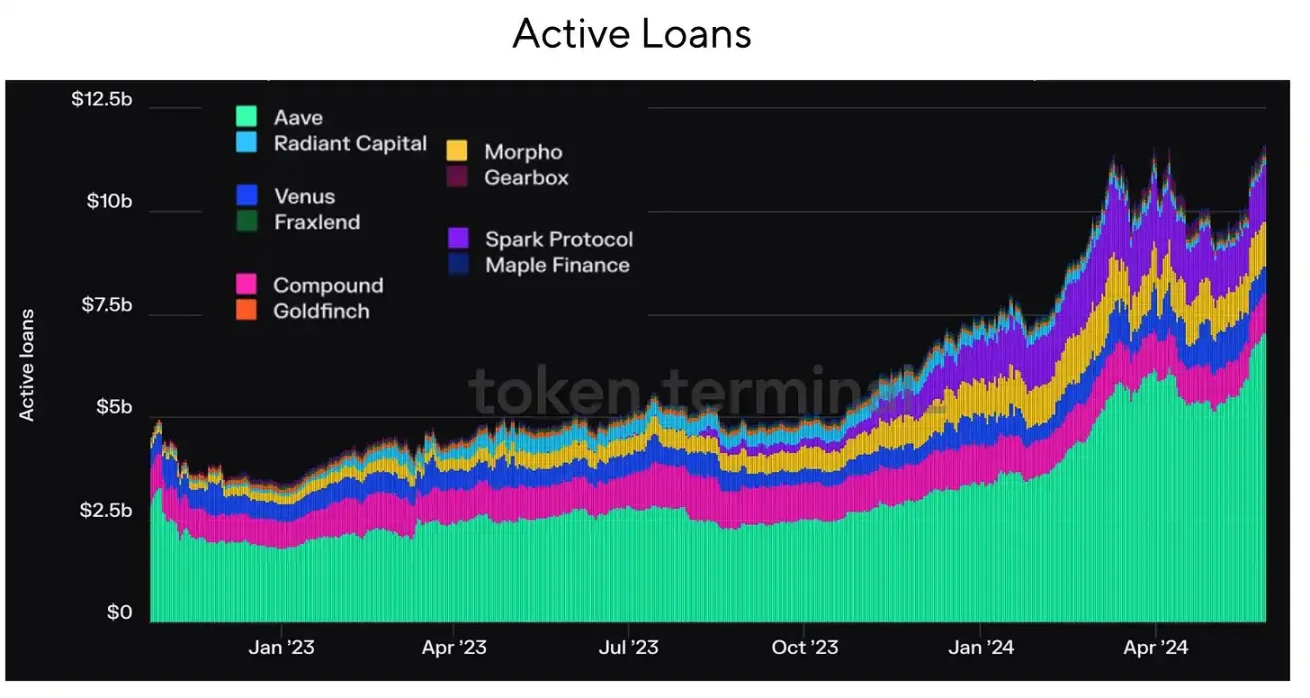

According to Token Terminal data, there has always been a question about whether MakerDAO belongs to the encrypted DeFi lending market share or the stablecoin market. However, with the success of Spark Protocol and the growth of MakerDAO's RWA (Real World Assets), this will no longer be a problem in the future.

Why Choose Modularization?

There are usually two approaches to building complex systems. One strategy is to focus on the end-user experience, ensuring that complexity does not affect usability. This means controlling the entire technology stack (as Apple does through integrated hardware and software).

The other strategy is to have multiple participants build various components of the system. In this approach, the central designer of the complex system focuses on creating interoperable core standards, relying on the market for innovation. This can be seen in core internet protocols, where the protocols remain unchanged, and applications and businesses based on TCP/IP drive innovation on the internet.

This analogy can also be applied to the economy, where the government is seen as the base layer, similar to TCP/IP, ensuring interoperability through the rule of law and social cohesion, while economic development occurs in the private sector built on top of the governance layer. These two approaches are not always applicable, and many companies, protocols, and economies operate somewhere between the two.

Breakdown Analysis

Supporters of modular lending theory believe that DeFi innovation will be driven by achieving specialization in every part of the lending stack, rather than just focusing on the end-user experience.

One key reason is to eliminate single dependencies. Lending protocols need close risk monitoring, as a small issue can lead to catastrophic losses, so building redundancy mechanisms is crucial. Single-structured lending protocols typically introduce multiple oracles to prevent the failure of one, but modular lending applies this hedging method to every layer of the lending stack.

For each DeFi loan, we can identify five key components that are necessary but adjustable:

- Loan assets

- Collateral assets

- Oracle

- Loan-to-Value ratio (LTV)

- Interest rate model

These components must be closely monitored to ensure the platform's solvency and prevent the accumulation of bad debts due to rapid price changes (we can also add a liquidation system to the above five components).

For Aave, Maker, and Compound, the token governance mechanism makes decisions for all assets and users. Initially, all assets were combined and shared the risk of the entire system. But even single-structured lending protocols quickly began creating separate markets for each asset to isolate risk.

Understanding the Key Modular Participants

Isolating markets is not the only way to make your lending protocol more modular. True innovation is happening in new protocols that rethink the essential components of the lending stack.

The biggest player in the modular world is Morpho, Euler, and Gearbox:

Morpho is currently the clear leader in modular lending, although it seems to have recently felt uncomfortable with this label, trying to become "non-modular, non-single-structured, but aggregated." Its total locked value (TVL) is 18 billion, undoubtedly ranking it at the forefront of the DeFi lending industry, but its ambition is to become the largest. Morpho Blue is its main lending stack, where a vault can be created without permission, tuned according to desired parameters. Governance only allows modifications to a few components - currently five different components - without specifying what these components should be. This is configured by the vault owner (usually a DeFi risk manager). Another major layer of Morpho is MetaMorpho, which aims to be an aggregated liquidity layer for passive lenders. This is a section particularly focused on the end-user experience. It is similar to Uniswap in the DEX on Ethereum, and also has Uniswap X for efficient trading routes.

Euler launched its v1 version in 2022, generating over $200 million in open contracts, but a hack almost depleted all protocol funds (although they were later returned). Now, it is preparing to launch v2 and re-enter the mature modular lending ecosystem as a major participant. Euler v2 has two key components. One is the Euler Vault Kit (EVK), a framework for creating ERC4626-compatible vaults with additional lending functionality, allowing it to function as a passive lending pool. The other is the Ethereum Vault Connector (EVC), an EVM primitive primarily implementing multi-vault collateral, where multiple vaults can use collateral provided by one vault. The v2 is planned to be launched in the second or third quarter.

Gearbox provides a user-centric explicit framework, allowing users to easily set positions without much supervision, regardless of their skills or knowledge level. Its main innovation is the "credit account," which is a list that allows the operation and whitelisting of assets valued in borrowed assets. It is essentially an independent lending pool, similar to Euler's vault, but different in that Gearbox's credit account combines a user's collateral and borrowed funds in one place. Like MetaMorpho, Gearbox demonstrates that there can be a layer focused on bundling for end-users in the modular world.

Unbundle, then Rebundle

Specializing in parts of the lending stack provides an opportunity to build alternative systems that may target specific niche markets or future growth drivers. Some leading proponents adopting this approach include:

Credit Guild intends to enter the established pooled lending market through a trust-minimized governance model. Existing participants like Aave have very strict governance parameters, which often lead to apathy among small token holders, as their votes seem to have little impact. Credit Guild disrupts this dynamic by introducing an optimistic, veto-based governance framework that specifies various statutory threshold numbers and delays for different parameter changes, combined with a risk response approach to handle unforeseen consequences.

Starport aims for cross-chain development. It has implemented a basic framework for integrating different types of EVM-compatible lending protocols. It handles data availability and term execution through two core components:

- Starport contracts, responsible for loan initiation (term definition) and refinancing (term updates). It stores data for protocols built on the Starport core and provides this data when needed.

- Custody contracts, primarily holding collateral initiated by borrowers on Starport and ensuring debt settlement and closure according to the terms defined in the initiated protocol, stored in the Starport contracts.

Ajna has a truly permissionless, oracle-less pooled lending model with no governance at any level. The pool is set up with specific pairs of quoted/collateral assets provided by lenders/borrowers, allowing users to assess asset demand and allocate capital. Ajna's oracle-less design comes from lenders being able to determine lending rates by specifying the amount of collateral assets each borrower's quoted token should be backed by. This is particularly attractive for long-tail assets, similar to what Uniswap v2 did for small tokens.

If You Can't Beat Them, Join Them

The lending space has attracted a large number of newcomers and reignited the drive for the largest DeFi protocols to launch new lending products:

Aave v4, announced just last month, is very similar to Euler v2. Previously, Aave's fervent supporter Marc "Chainsaw" Zeller had stated that due to the modular nature of Aave v3, it would be the final version of Aave. Its soft liquidation mechanism was pioneered by Llammalend (see below); its unified liquidity layer is also similar to Euler v2's EVC. While most upcoming upgrades are not novel, they have not been widely tested in a highly liquid protocol (which Aave already is). Aave's success in winning market share on every chain is incredible. Its moat may not be deep, but it is wide, giving Aave a very strong tailwind.

Curve, or more colloquially known as Llammalend, is a series of isolated, one-way (non-borrowable collateral) lending markets, where crvUSD (already minted), Curve's native stablecoin, is used as collateral or debt assets. This allows it to leverage Curve's expertise in automated market maker (AMM) design to provide unique lending market opportunities. Curve has operated in a unique way in the DeFi space, but it has been effective for them. In addition to Uniswap, Curve has carved out an important niche in the decentralized exchange (DEX) market and has made people rethink their token economics through the success of the veCRV model. Llammalend seems to be another chapter in the Curve story:

Its most interesting feature is its risk management and liquidation logic, based on Curve's LLAMMA system, capable of achieving "soft liquidation."

LLAMMA is implemented as a market-making contract, encouraging arbitrage between isolated lending market assets and the external market.

Similar to concentrated liquidity automated market makers (clAMM, such as Uniswap v3), LLAMMA evenly deposits a borrower's collateral within a specified price range (referred to as an interval), where prices deviate significantly from the oracle price, to ensure there is always an incentive for arbitrage.

In this way, when the price of collateral assets falls outside the interval, the system can automatically convert some collateral assets into crvUSD (soft liquidation). While this method may lower the overall health of the loan, it is much better than full liquidation, especially considering explicit support for long-tail assets.

Since 2019, Curve founder Michael Egorov has invalidated over-engineered criticisms.

Both Curve and Aave place a strong emphasis on the development of their stablecoins. This is a very effective long-term strategy that can bring substantial income. Both are emulating MakerDAO's approach. MakerDAO has not given up on DeFi lending and has launched the independent brand Spark. Despite the lack of native token incentives (yet), Spark has performed exceptionally well over the past year. Stablecoins and massive currency creation capabilities (credit is indeed a powerful drug) present a huge long-term opportunity. However, unlike lending, stablecoins require on-chain governance or off-chain centralized entities. For Curve and Aave, this path is reasonable as they have some of the oldest and most active token governance (second only to MakerDAO).

What Compound is up to is currently unclear. It used to be a leader in the DeFi space, kicking off DeFi summer and establishing the concept of yield farming. Apparently, regulatory issues have limited the activity of its core team and investors, leading to a decrease in its market share. However, like Aave's wide but shallow moat, Compound still has $1 billion in outstanding loans and extensive governance distribution. Recently, development has continued outside the Compound Labs team. It is uncertain which markets it should focus on - perhaps large blue-chip markets, especially if it can gain some regulatory advantages.

Accrued Value

The top three in DeFi lending (Maker, Aave, Compound) are adjusting their strategies to adapt to the shift towards modular lending architecture. Lending against cryptocurrency collateral used to be a good business, but when your collateral is on-chain, the market becomes more efficient, squeezing profits.

This does not mean there are no opportunities in an efficient market structure, just that no one can monopolize their position and extract rent.

The new modular market structure provides more permissionless value capture opportunities for private enterprises like risk managers and venture capitalists. This makes risk management more practical and directly translates into better opportunities, as economic losses would severely impact the reputation of vault administrators.

The recent Gauntlet-Morpho incident is a good example of this, which occurred during the uncoupling process of ezETH.

During the uncoupling, the mature risk manager Gauntlet operated an ezETH vault and suffered losses. However, due to clearer and more isolated risks, most users of other metamorpho vaults were unaffected, and Gauntlet needed to provide a post-assessment and take responsibility.

Gauntlet initially launched the vault because it believed it had a more promising future on Morpho, where it could directly charge fees, rather than providing risk management consulting services to Aave governance (the latter is more focused on politics than risk analysis - you try tasting or drinking "Chainsaw").

Just this week, Morpho founder Paul Frambot revealed that a smaller risk management firm, Re7Capital, also a company with excellent research newsletters, as the manager of the Morpho vault, achieved an annualized on-chain income of $500,000. While not huge, this indicates that you can build a financial firm on DeFi (not just a wild yield farm). This does raise some long-term regulatory issues, but this is commonplace in today's cryptocurrency world. Furthermore, this will not prevent risk managers from becoming one of the biggest beneficiaries of future modular lending.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。