Original Author: Hosseeb, Dragonfly Managing partner

Translation: Zen, PANews

Is the market structure broken? Are VCs too greedy? Is this a manipulation game targeting retail investors?

Every theory I've seen about this issue seems to be wrong, but I will let the data speak.

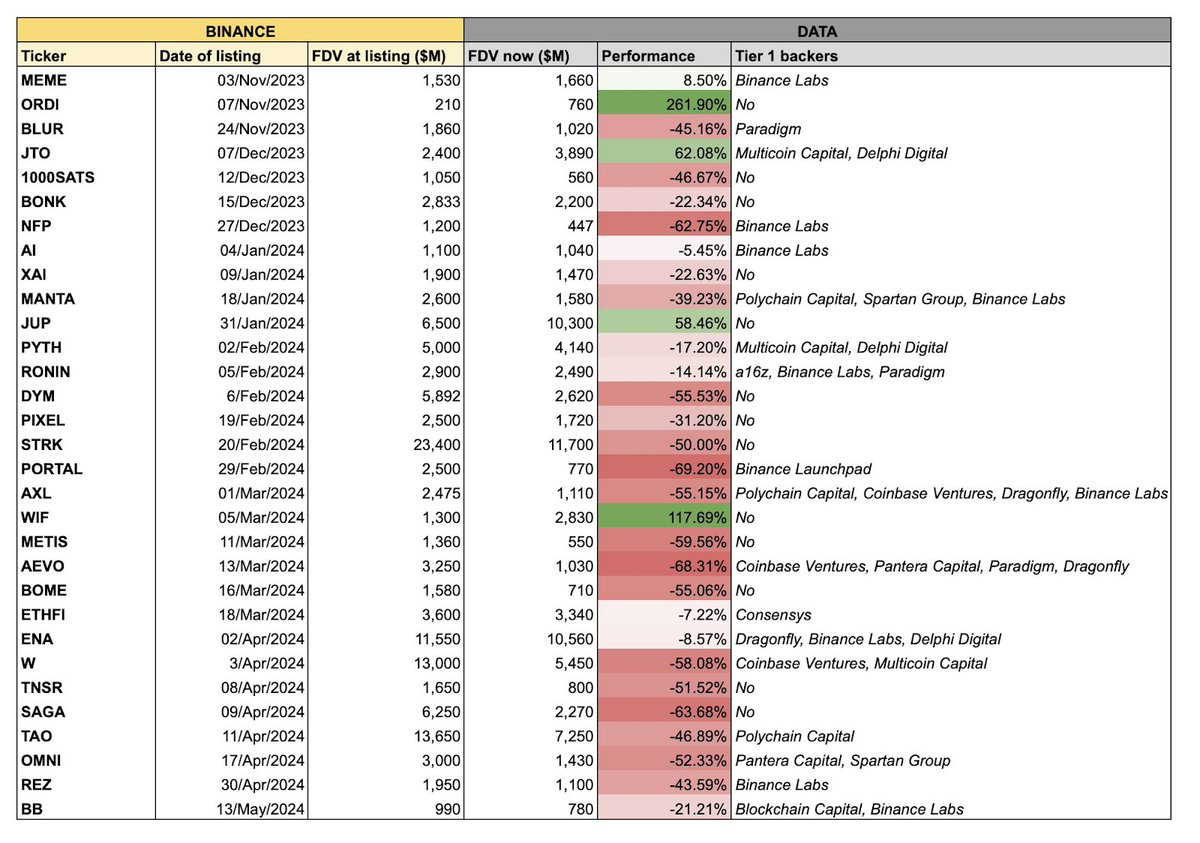

A table recently made by user @tradetheflow on X has been widely circulated, showing that a batch of tokens listed on Binance in the past six months have not performed well. Most people mock these tokens as "overvalued, low circulation" tokens, meaning they have a high fully diluted valuation (FDV) but a low initial circulating supply.

I have plotted these tokens into candlestick charts and removed the labels, as well as excluded all tokens explicitly labeled as "memecoins," as well as tokens like RON and AXL that had TGEs before being listed on Binance.

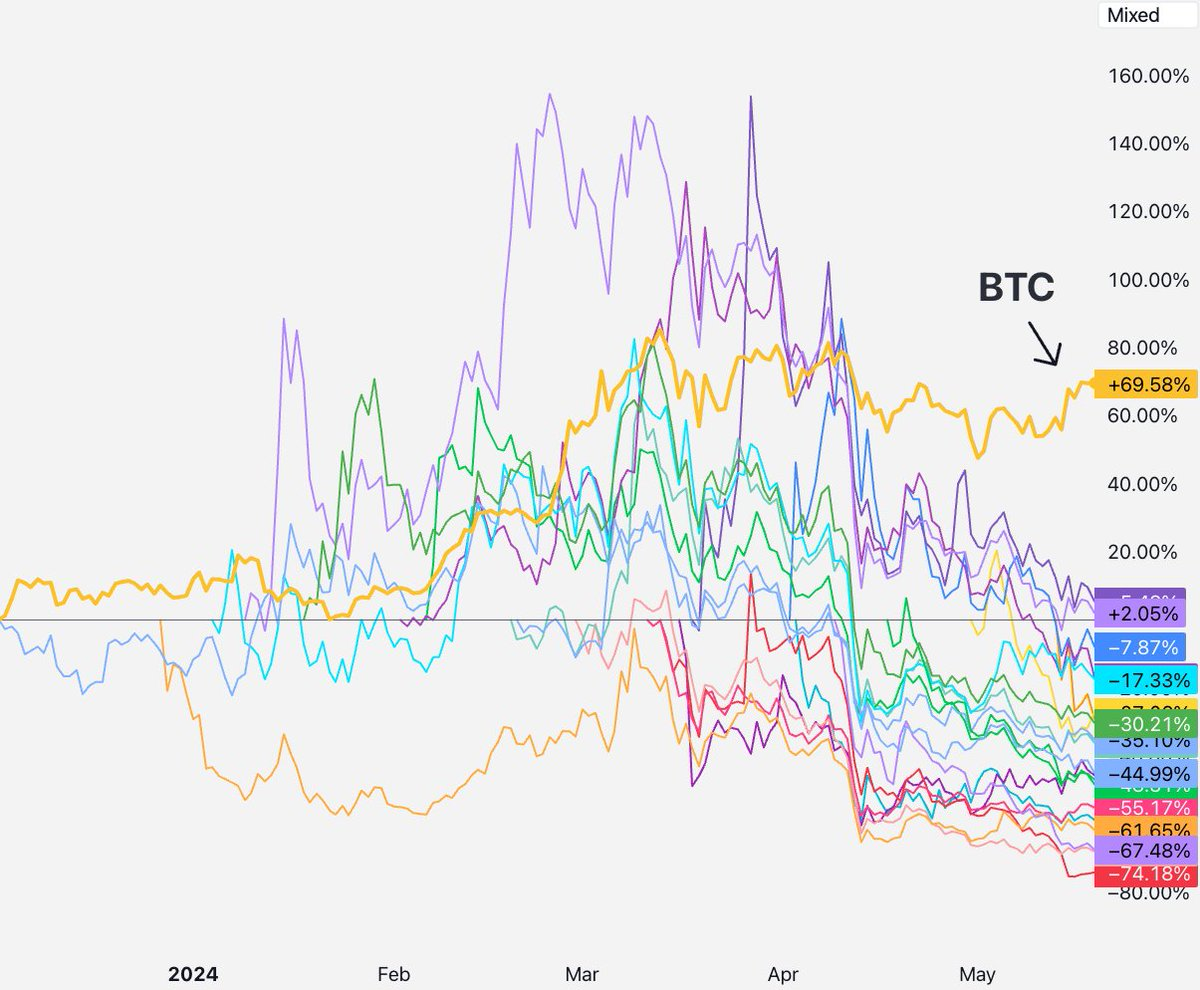

Almost all of these "low circulation, high FDV" tokens listed on Binance have been on a downward trend. Everyone has their own views on the market structure issue. The three most popular arguments are:

1) VCs/KOLs are dumping on retail investors

2) Retail investors are abandoning these tokens and turning to memecoins

3) The supply is too low to facilitate meaningful price discovery

All of these arguments are reasonable! Let's see if they hold true. But for the sake of science, we need a null hypothesis to refute. Our null hypothesis here should be: these assets have all repriced, but there are no deeper market structure issues (classic "more sellers than buyers"). Based on this, we will examine each viewpoint one by one.

Viewpoint One: VCs/KOLs Dumping on Retail Investors

If this is true, what would we see? We should see tokens with short-term lockups dropping faster than other tokens, and projects with long-term lockups or no KOLs should perform well. (Liquidity perpetual contracts may also be another way for this dumping to occur.)

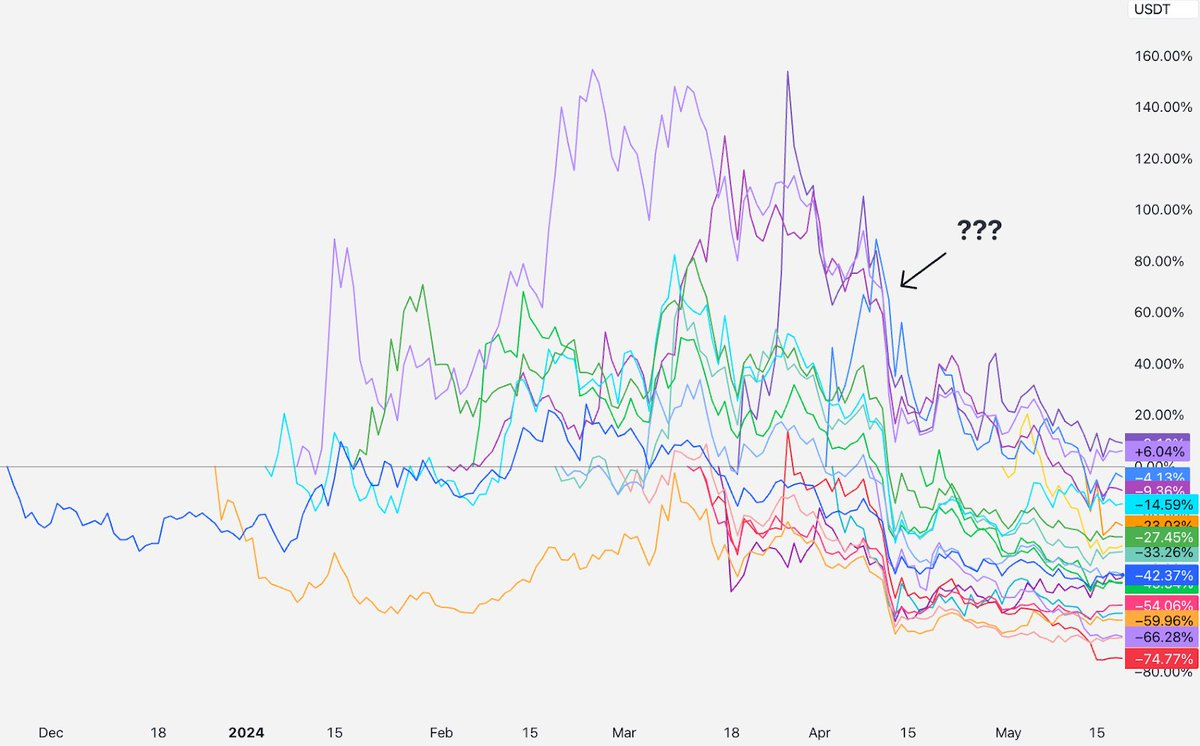

So what do we see in the data?

Therefore, from listing to early April, these tokens actually performed well. Some were priced higher than the listing price, some lower, but most were concentrated around zero. Before that, there seemed to be no dumping by VCs or KOLs.

Then in mid-April, everything started to decline together. Despite these projects listing at different times and having different VCs and KOLs, did they all unlock in mid-April and start dumping on retail investors?

As a venture capitalist, I must confess, there are definitely some VCs dumping on retail investors—some VCs do not lock up, they hedge OTC, and some even violate their lockup period. But these are low-grade VCs, most teams working with these VCs will not list on top-tier exchanges. Every top-tier VC you can think of has at least a 1-year cliff and multi-year lockups. Under SEC Rule 144a, anyone under SEC regulation must have a 1-year cliff. Furthermore, for large VCs like us, our positions are too large to hedge OTC, and we are often bound by contractual obligations not to do so.

So why does this story not make sense: every one of these tokens is less than a year from TGE, meaning venture capitalists with a 1-year lockup are still locked. So for some tokens, dumping by investors/KOLs may be real—there will always be some bad actors in projects. But if all tokens are declining at the same time, this theory cannot explain that.

Viewpoint Two: Retail Investors Abandoning These Tokens and Turning to Memecoins

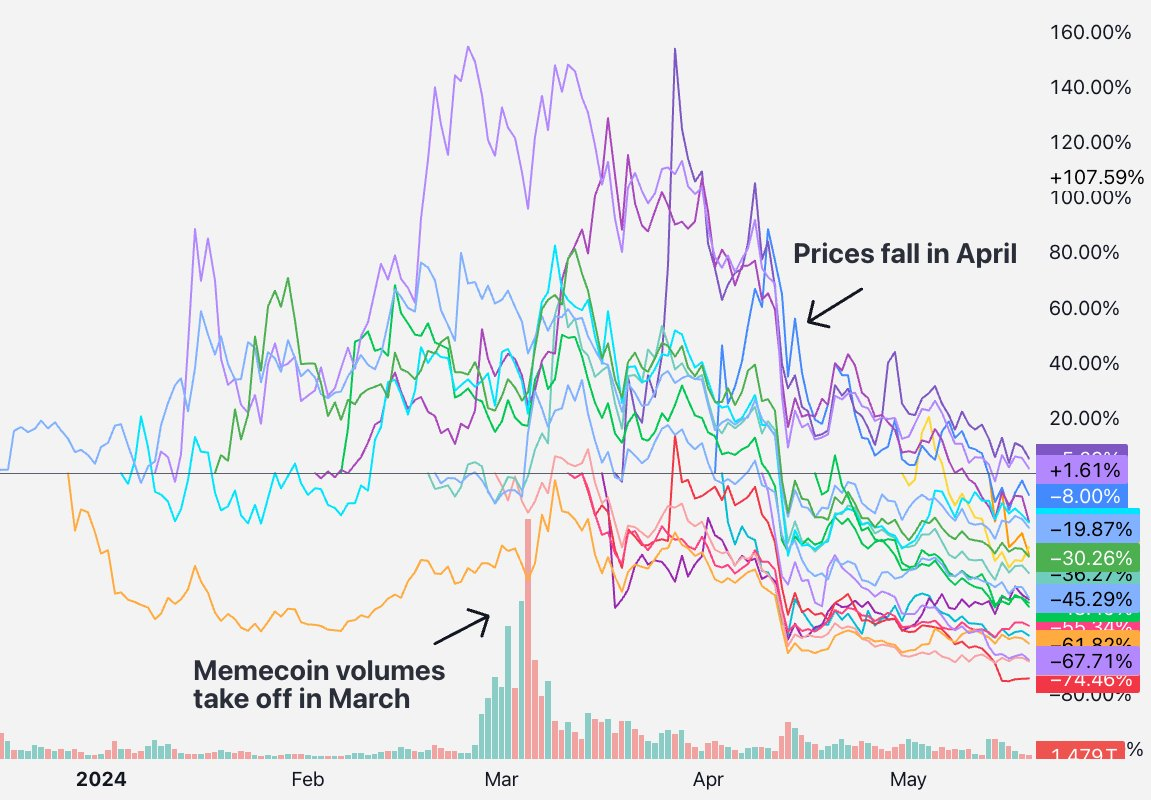

If this is true, what we should see is: the prices of these new tokens dropping, while retail investors turn to buying memecoins.

However, this is not the case:

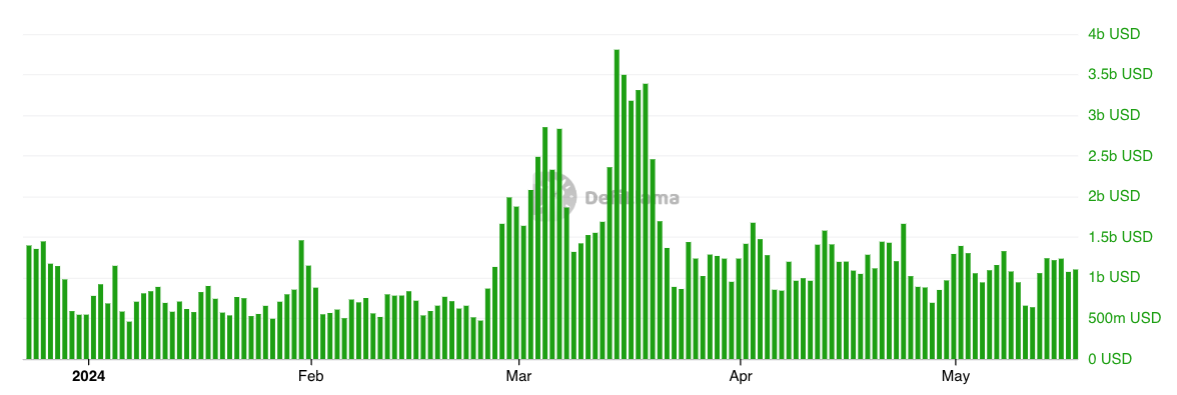

By comparing the trading volume of SHIB token with this basket of tokens, we find that the timing does not match. The memecoin frenzy peaked in March, but this basket of tokens started to decline a month and a half later in April.

The trading volume on Solana DEX also confirms this—memecoins had their surge in early March before the decline in April.

Therefore, this theory also does not align with the data. There is no widespread shift of funds from this basket of tokens to memecoins. People are trading memecoins, but they are also trading new tokens, and the trading volume does not show a clear trend.

The issue is not with the trading volume, but with the asset prices.

Nevertheless, many people are trying to spread the idea that retail investors are abandoning real projects and mainly turning to buying memecoins. On Binance's Coingecko page, about 14.3% of the top 50 tokens by trading volume are memecoins pairs. Memecoins do not dominate the cryptocurrency market. Yes, financial nihilism exists and is very prominent on social media. But most people in the world still buy VC tokens because they believe in some kind of technological narrative, regardless of its correctness.

So, perhaps the fact is not that retail investors are turning from VC tokens to memecoins, but there is a sub-theory here: VCs have too many of these projects, which is also why retail investors are giving up. They may have realized around mid-April that these are all deceptive VC tokens, with teams+VCs owning 30-50% of the token supply. This must have been the last straw.

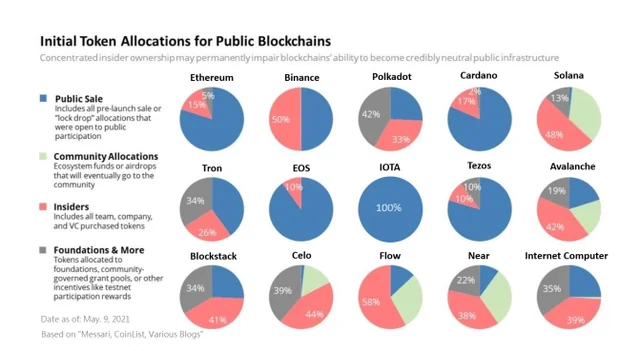

However, comparing the snapshots of token distribution from 2017-2020, look at the red shaded portion—that is the proportion owned by insiders (teams+investors). SOL 48%, AVAX 42%, BNB 50%, STX 41%, NEAR 38%, and so on. The situation today is basically the same. So if the theory is "tokens that were not VC tokens before are now," then this also does not align with the statistical data. Capital-intensive projects always have over-ownership by teams and investors at launch, regardless of the cycle. These "VC tokens" have also been successful after full unlocking.

As a general matter, if this thing happened in the previous cycle, then it cannot explain the unique phenomenon happening now. Therefore, the claim that "retail investors are abandoning these tokens and only buying memecoins" sounds reasonable and is a clever viewpoint, but it cannot explain these data.

Viewpoint Three: Insufficient Supply for Price Discovery

This is the most common viewpoint I have seen, it sounds reasonable and not so sensational. However, Binance Research once published a good report to address this issue:

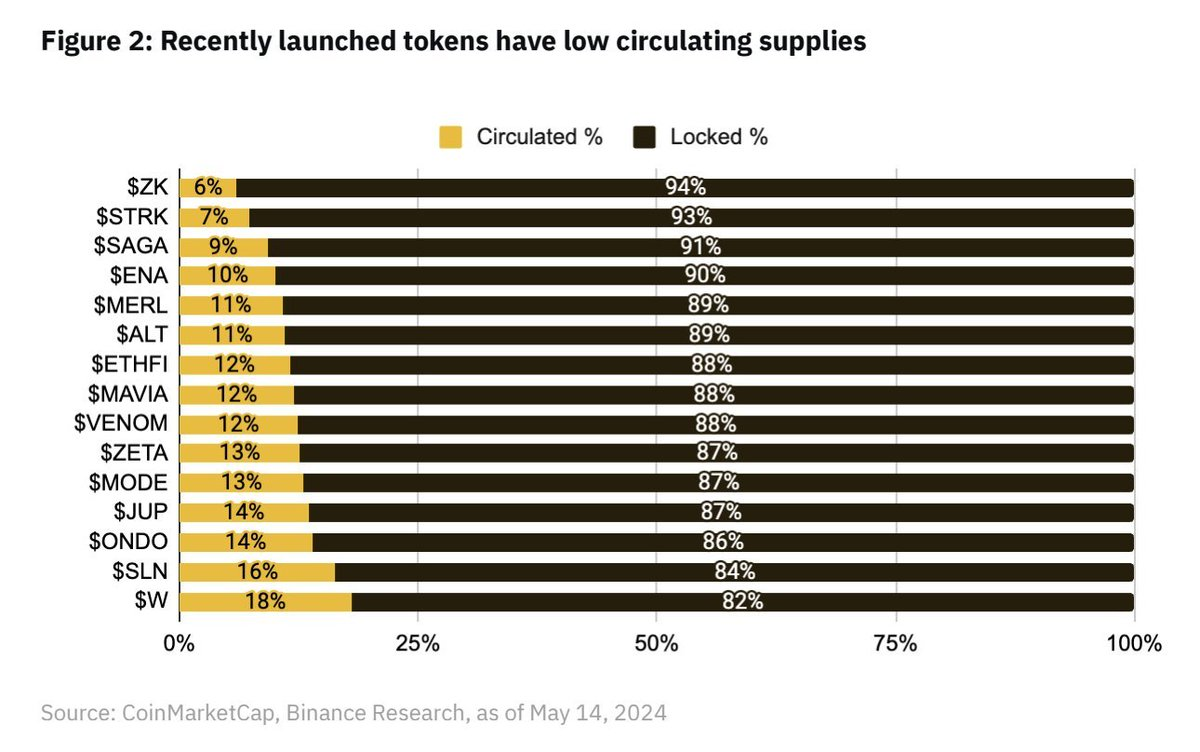

The average circulation of the tokens in the above table is about 13%, which is obviously very low, lower than the tokens in the past.

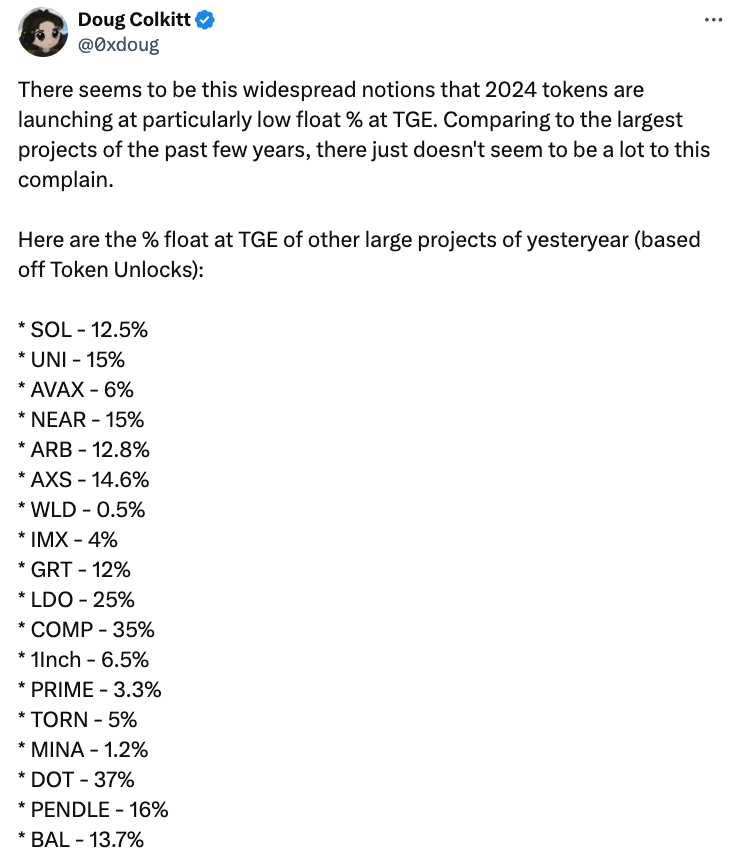

According to the data provided by user @0xdoug on X, the average circulation of tokens in the previous cycle was also 13%.

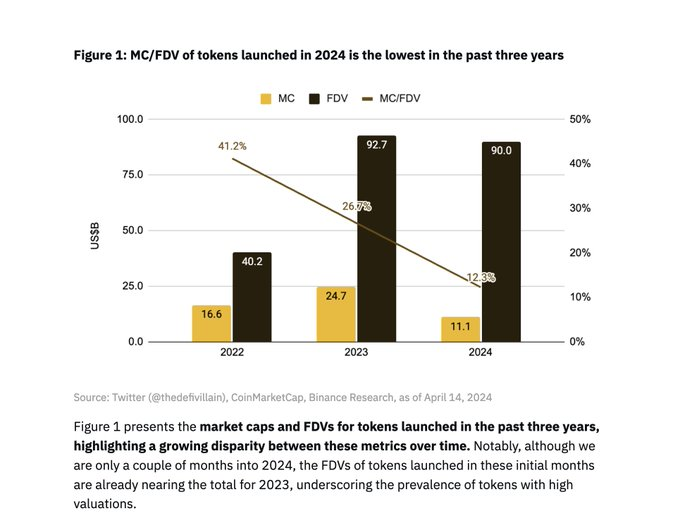

It should be noted that the same Binance research report also had another widely circulated chart, which indicated that the average circulation of tokens listed in 2022 was 41% at launch.

However, this information is not accurate. I looked at the projects listed on Binance in 2022: OSMO, MAGIC, APT, GMX, STG, OP, LDO, MOB, NEXO, GAL, BSW, APE, KDA, GMT, ASTR, ALPINE, WOO, ANC, ACA, API3, LOKA, GLMR, ACH, IMX. Among them, IMX, OP, and APE are similar to the latest batch of tokens we are comparing. IMX had a first-day circulation of 10%, APE had a first-day circulation of 27% (but 10% of it is APE's reserve, so it can be rounded to a circulation of 17%), and OP had a first-day circulation of 5%.

On the other hand, although LDO and OSMO had unlock percentages of 55% and 46% respectively, these had been running for over a year before being listed on Binance, so comparing these listings with the latest first-day listed tokens is foolish. If I were to guess, these are not projects that were first-day listed on Binance, and random project tokens like NEXO or ALPINE may be the reason for their crazy high numbers. I think Binance Research may not have clarified the true trend of token TGEs, and their results are essentially the trend of the types of tokens listed on Binance each year.

You might agree that a 13% circulation supply is similar to the previous cycle. But this is still too low for meaningful price discovery. So, does the stock market not have this problem? According to the data provided by user @0xdoug, the median first-day circulation for IPOs in 2023 was 12.8%.

To be honest, an extremely low circulation supply is definitely a problem. WLD is a particularly severe example, with a circulation supply of only 2%. FIL and ICP also had extremely low circulation at launch, leading to very ugly price charts. But in this batch of Binance tokens, most are within historically normal ranges for first-day circulation supply.

Furthermore, if this theory is correct, you should see the tokens with the lowest circulation being punished, and tokens with higher circulation should perform well. But we have not seen a strong correlation. They are all declining. So, while the theory of a lack of price discovery sounds convincing, it is not convincing after looking at the data.

How to Get Out of the Current Predicament?

Everyone is complaining, but only a few have proposed real solutions.

Many people suggest restarting ICOs. However, have we forgotten how ICOs ruthlessly dumped after listing, and retail investors were heavily exploited? Additionally, ICOs are illegal almost everywhere, so I don't think this is a serious suggestion.

Kyle Samani (Founder of Multicoin) believes that investors and teams should unlock 100% immediately. However, this is impossible for U.S. investors, and according to Rule 144a (which would exacerbate the "VC dumping" problem). Furthermore, I think we learned in 2017 that team unlocks are a good idea.

Investment firm Arca believes that tokens should have custodians like traditional IPOs. But token issuance is more similar to direct listings, where they just list on exchanges, have some market makers, and that's it. I think it's fine, but I lean towards a simpler market structure and fewer intermediaries.

@reganbozman (Lattice Fund) suggests that projects should list at a lower price to allow retail investors to buy in earlier and gain some upside. I understand the intent, but I don't think this will work. Artificially pricing below the market clearing price only means that those trading in the first few minutes on Binance will capture mispricing. We have seen this in many NFT launches and IDOs. Artificially undervaluing your listing price only benefits a few traders who execute large orders in the first 10 minutes. If the market believes your value is X, in a free market, you will be worth X by the end of the day.

Many people suggest that teams should do larger-scale airdrops, which I think is reasonable! We usually encourage teams to provide more supply on the first day to improve decentralization and price discovery. That being said, I don't think it's wise to do absurdly large-scale airdrops just for circulation supply—doing a large-scale airdrop on the first day just for the sake of getting a huge circulation supply and then having to rely on token giveaways when competing with other projects in the future is not a wise choice. No one wants to be one of those projects that has to reissue tokens a few years later due to financial stress.

As a venture capitalist, we hope that token prices will be truly reflected within a year. We don't make money by price appreciation, but by DPI (deployed capital interest) returns, which means we eventually have to convert our tokens into cash. We can't eat paper gains, and we won't market-price our unlocked tokens (I think anyone who does that is crazy). Tokens soaring after we unlock and then crashing is actually a bad look for VC funds. This makes limited partners think this asset class is fake—looks good on paper, but bad in practice. We don't want that, we prefer assets to gradually and steadily appreciate, which is what most people want.

So are these high valuations sustainable? I don't know. The current prices are obviously jaw-dropping compared to when projects like ETH, SOL, NEAR, and AVAX were first listed. Cryptocurrency is much larger now, and the market potential and chances of success for crypto protocols are clearly greater than in the past.

@0xdoug (Founder of ambient finance) made a good point: if you calculate the FDV of the old meme coins in ETH, you will get numbers very close to the current FDV we see. @Cobie also expressed a similar point in his recent article. We won't go back to the days when the FDV of L1 was only $40 million, because everyone sees how big the market is now.

A lot of this frustration actually boils down to: cryptocurrency has risen sharply in the past 5 years. The prices of startups are determined based on comparable peers, so all numbers will be larger. That's the fact.

It's easy to criticize others' solutions, but to be honest, I don't have any brilliant solutions either. The free market will solve this problem on its own. If tokens decline, then the prices of other tokens will be repriced lower, exchanges will push teams to list at lower FDVs, traders will only buy at lower prices, VCs will pass this message to founders. Price signals will eventually spread through the public market, B-round prices will be lowered due to comparisons, which will make A-round investors feel ashamed, and ultimately affect seed investors. Price signals will always eventually spread.

When there is a real market failure, you may need some clever market intervention. But the free market knows how to correct mispricing—just adjust the price. Those who have lost money, whether VCs or retail investors, don't need people like me to think or debate on Twitter. They have internalized the lesson and are willing to buy these tokens at lower prices. That's why all these tokens are trading at lower FDVs, and future token trades will be priced accordingly. This situation has happened many times before, it just takes some time.

Who's to Blame for the Market Downturn in April?

Now let's uncover the truth like in "Scooby-Doo." What caused all the coins to drop in April? The culprit: the Middle East.

In the first few months, these coins mostly remained stable after listing, until mid-April. Suddenly, Iran and Israel started threatening to start World War III, and the market was in chaos. Although Bitcoin recovered, these coins did not. So why are these coins still falling? My explanation is: these new projects were all considered "high-risk new coins." In April, interest in this "high-risk new coin" basket decreased and did not recover. The market decided not to buy them anymore.

The market can be very fickle at times. But if this "high-risk new coin" basket had risen 50% during this time instead of falling 50%, would you also argue that there is a problem with the token market structure? That would also be a mispricing, just in the opposite direction. Mispricing is mispricing, and the market will eventually correct it. If you want to help—sell at crazy prices and buy at better prices. If the market is wrong, this is how it corrects itself. No need to do anything else.

When people lose money, everyone wants to know whose fault it is. Is it the founders? VCs? KOLs? Exchanges? Market makers? Traders? I think the best answer is no one (I also accept everyone). But thinking about market mispricing from anyone's perspective is not an effective framework. So I will analyze from the perspective of what people can do better in this new market system.

Venture Capital: Listen to the market's voice, slow down. Show price discipline. Encourage founders to be realistic about valuations. Don't mark locked tokens at market prices (almost all top VCs I know hold their locked tokens at a significant discount to market prices). If you find yourself thinking "this trade can't possibly lose money," you might regret that trade.

Exchanges: List tokens at lower prices. Consider using open auctions to price first-day tokens, rather than as the final round of VC. And adhere to the following principles when listing: tokens need to have a lock-up period following market standards; project teams and all their investors have non-hedging contractual obligations. Additionally, do better in showing FDV charts to retail investors and educate them about token unlocks.

Project Teams: Strive to release more tokens on the first day, less than 10% of token supply is too little. Of course, healthy airdrops should be conducted, don't be too afraid of undervaluing FDV on the first day. Building a healthy community with the best price chart is a gradual upward process. If you are a team whose token price is falling, don't worry. You are not alone. Remember: AVAX dropped by about 24% in the two months after listing, SOL dropped by about 35% in the two months after listing, NEAR dropped by about 47% in the two months after listing. You'll be fine. Focus on building something to be proud of and keep moving forward. The market will eventually solve the problem.

As for the anonymous: be careful of single-cause explanations. The market is complex and sometimes falls. Doubt anyone who claims to know the exact reason. Do your own research, don't invest in anything you're not willing to lose.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。