Since 2013, the U.S. government's policy has been clear that developers and users of cryptocurrency wallets are not considered money transmitters. However, the recent decision by the Department of Justice to prosecute wallet developers for unlicensed money transmission came as a surprise, especially considering that these developers do not actually control the assets protected by their software.

Federal prosecutors have presented this unprecedented interpretation in two recent cases: the publicized lawsuit against Samourai Wallet on April 26 and the opposition to the exclusion of evidence in the Tornado Cash case involving Roman Storm, also announced on the same day. Additionally, the FBI has issued a warning to cryptocurrency wallet users, stating that if they do not transfer funds to regulated entities, they may risk losing these funds due to criminal seizures and investigations.

I. Brief Review of Existing Money Transmission Policies and Detailed Summary of Recent Events

The United States has a series of federal laws governing anti-money laundering (AML) regulations for money transmitters, primarily based on the Bank Secrecy Act and its amendments. These laws define the category of "financial institutions" and authorize the Secretary of the Treasury to redefine this category as needed. Therefore, the implementing rules under the Bank Secrecy Act actually specify who must or must not register as a money transmitter or other financial institution, comply with the "know your customer" (KYC) principle, submit reports to the government, and implement other anti-money laundering controls.

These regulations define money transmitters as:

- Anyone providing money transmission services, where "money transmission services" are defined as "the acceptance of currency, funds, or other value that substitutes for currency from one person and the transmission of currency, funds, or other value that substitutes for currency to another location or person";

- Any other person involved in the transfer of funds.

In the context of cryptocurrency, there is some ambiguity regarding whether cryptocurrency qualifies as "currency, funds, or other value that substitutes for currency." If cryptocurrency is considered "funds," then "anyone involved in the transfer" becomes a money transmitter. If cryptocurrency is considered "currency," or "other value that substitutes for currency," then anyone "accepting" and "transmitting" cryptocurrency becomes a money transmitter. According to a direct interpretation of the regulations, cryptocurrency is considered a substitute for traditional currency. Therefore, if someone commercially accepts and transmits another person's cryptocurrency, they are considered a money transmitter. In other words, if someone actually controls another person's cryptocurrency and uses that control to transfer the cryptocurrency to another person or location, they are a money transmitter. This law has been in place before the emergence of cryptocurrency and has never been modified or overturned by Congress, the courts, or regulations.

The minor ambiguity about whether cryptocurrency qualifies as currency, funds, or other value that substitutes for currency will be resolved by FinCEN in the early history of cryptocurrency regulation.

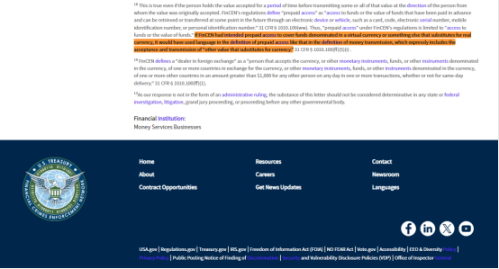

In 2013, FinCEN issued its first "virtual currency" guidance. In this guidance, FinCEN confirmed that cryptocurrency (referred to as virtual currency) is "value that substitutes for currency," not "funds" or "currency" itself (hence the term "virtual currency"). In a footnote, it also explicitly stated that virtual currency is not considered "funds" because such a definition would trigger certain prepaid access rules, which FinCEN believed did not apply to cryptocurrency activities.

FinCEN further explained that merely using virtual currency does not make a user a money transmitter, and in a subsequent administrative ruling, it was found that software developers are also not money transmitters: "The mere production and distribution of software itself does not constitute acceptance and transmission of value, even if the software is designed to facilitate the sale of virtual currency."

Furthermore, in 2019, FinCEN issued additional guidance explicitly stating that partial control over virtual currency is not sufficient to classify wallet developers as money transmitters, as those participating in transactions and holding the currency need to request additional verification and do not have complete independent control over these values.

This guidance requires only companies providing custodial cryptocurrency services to be licensed and subject to federal money transmission regulations. The law has always been clear: non-custodial cryptocurrency developers are not money transmitters.

II. Details and Points of Contention in the Cases

On April 26, 2024, a complaint was made public, accusing Samourai Wallet (a Bitcoin wallet that enhances user privacy through CoinJoin transactions) developers of illegal money transmission and other charges. In this discussion, we will not address the money laundering conspiracy charges, as they depend on specific facts and may not be based on the developers providing custodial rather than non-custodial services. The defendant may have operated a centralized server to coordinate CoinJoin transactions, as alleged in the complaint. However, based on our current understanding, Samourai Wallet did not give developers or any third party independent control over the Bitcoin protected by the wallet software. According to a direct interpretation of the regulations, especially considering FinCEN's guidance and administrative ruling, Samourai Wallet developers do not have "complete independent control" over any user funds, and therefore do not fall within the definition of money transmitters.

In the case of Roman Storm's Tornado Cash, the prosecution responded to the previously filed motion to dismiss. They discussed a law called "Section 1960," which states that operating an unlicensed money transmission business is illegal. The prosecution's response emphasized that the definition of this law is much broader than what is typically discussed.

Their main argument is that as long as the Tornado Cash software is used to request deposits or withdrawals, it results in the movement of cryptocurrency on the Ethereum blockchain, and therefore they believe the developers of Tornado Cash should be held responsible. This broadens the scope of liability, implying that, according to this logic, almost all cryptocurrency wallets and smart contracts are engaged in money transmission businesses, and all developers could be involved in illegal money transmission.

In terms of regulatory definitions, the prosecution's response disregards all previous guidance, interpreting "funds" in the law very broadly, simply defining it as anyone involved in the transfer. They even likened this to parcel delivery, attempting to show that control of funds is not a necessary condition. This interpretation overlooks FinCEN's previous explicit statement that virtual currency does not qualify as "funds," which is quite absurd.

If Tornado Cash is considered a parcel service, it is clearly not serving only criminals. Furthermore, the prosecution's analogy actually proves the opposite of what they intend to prove. A courier service that cannot access the contents of the packages is clearly not a money transmission service. First, if you cannot open the package, how do you know what's inside? If you are told it's just a box of canned goods being transported and you cannot open the box, how could you be guilty of operating an unlicensed money transmission business? Secondly, the Financial Crimes Enforcement Network (FinCEN) explicitly states that armored car services exclusively for the secure transport of money are not considered money transmission services!

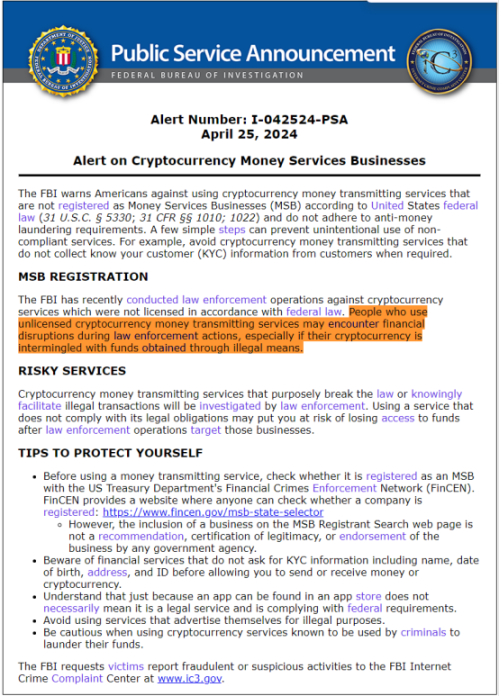

Meanwhile, the Federal Bureau of Investigation (FBI) issued a warning about cryptocurrency wallets. The announcement reminds Americans not to use cryptocurrency transmission services that are not registered as money services businesses (MSBs) under U.S. federal law. The FBI also provides the official FinCEN tool for users to check if a company is registered as an MSB.

Given the lawsuits against Tornado Cash and Samourai Wallet, if the Department of Justice's position is that any action that moves cryptocurrency on the Ethereum blockchain from one place to another (as argued in Tornado Cash's defense) constitutes money transmission, then every cryptocurrency wallet is a money transmitter, whether it is software running on your phone, on your Trezor or Ledger hardware wallet, or on Coinbase's servers, and all would need to register as money services businesses. Among these, only Coinbase is registered. Considering the recent lawsuits, this is a precedent that should be of concern to many wallet companies in the industry, including some decentralized wallet providers.

It is still unclear whether the Department of Justice intentionally changed its long-standing policy through criminal enforcement, or if there is a serious disconnect between the Department of Justice and the Financial Crimes Enforcement Network (FinCEN). However, this approach undoubtedly undermines the rule of law in the United States. On a side note, whether it's the passage of the TikTok case or the recent controversial "Anti-Semitism Awareness Act," we can feel the internal division within the United States.

III. Uncertainty Leads to Withdrawal of Cryptocurrency Wallets from the U.S. Market

Paris-based Bitcoin company Acinq stated that recent announcements by U.S. authorities have raised questions about whether self-custody wallet providers, Lightning service providers, and even Lightning nodes can be considered money services businesses and subject to such regulation due to regulatory uncertainty. As a result, they will delist their popular Lightning Network wallet, Phoenix, from U.S. app stores, advising users to close channels and transfer funds before terminating access on May 3, 2023.

One day later, zkSNACKs announced the closure of access to its privacy-focused Wasabi wallet in the United States and stated in a statement on April 27 that "due to recent announcements by U.S. authorities, zkSNACKs now strictly prohibits the use of its services by U.S. users."

IV. Questions

1. If a wallet is not targeting U.S. users, does it still need to obtain a license and register?

If a cryptocurrency wallet or service explicitly does not target U.S. users and ensures that U.S. users cannot access its services, it generally does not need to obtain a U.S. money transmission license or register as a money services business (MSB). U.S. laws and regulations primarily apply to businesses operating in the U.S. or serving U.S. residents.

However, even if a service does not directly target U.S. users, if it operates through the U.S. financial system or if U.S. users find ways to use the service, it may still attract the attention of U.S. regulatory authorities. Therefore, completely avoiding the risk of U.S. law may be challenging, especially in a globalized and internet environment.

To mitigate potential legal risks, non-U.S. cryptocurrency service providers should take measures to ensure that their services are not accessed or used by U.S. users. This may include geoblocking, IP address filtering, and explicitly stating in the terms of service that the service is not provided to U.S. residents.

2. If it's not possible to completely prevent U.S. users from using the service, what is the prudent approach?

- Register as a Money Services Business (MSB):

- Individuals or companies providing money transmission services must register as a Money Services Business (MSB) in accordance with the requirements of the Financial Crimes Enforcement Network (FinCEN) of the U.S. Department of the Treasury. This includes submitting necessary registration forms and updating any significant changes.

- Compliance with the Bank Secrecy Act (BSA) regulations:

- Businesses registered as MSBs must comply with the regulations of the Bank Secrecy Act and its amendments, including but not limited to anti-money laundering (AML) regulations and the submission of suspicious activity reports (SARs).

- Implementation of Know Your Customer (KYC) procedures:

- Money transmission services need to implement KYC procedures, which are customer identity verification processes aimed at preventing identity theft, financial fraud, and money laundering activities.

- Obtain State-Level Licenses (MTL License):

- In addition to federal registration, most states require money transmission services to obtain state-level licenses. Specific requirements may vary by state, so applications for the appropriate licenses should be made based on the specific state of operation.

- Maintenance of Compliance Records and Reporting:

- Compliance with all record-keeping requirements and regular reporting to FinCEN of large transactions and suspicious activities. These records may need to be provided during reviews or examinations.

- Capital and Insurance Requirements:

- Depending on the scale of operations and types of transactions, there may be requirements to meet certain capital reserves and insurance coverage to ensure the security of customer funds.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。