Do not listen to bad advice from venture capitalists, consultants, or anyone else.

Written by: Regan Bozman

Translated by: DeepTechFlow

The current token issuance structure promotes a "only fall, no rise" pattern, and the token price will be severely hit under this pattern.

Tokens are issued with a high FDV, gradually depleting as a result of airdrop recipients selling, and then collapsing with VC unlocks.

Some thoughts on how to break the current pattern

Mike Zajko always describes the worst-case trajectory of a team's token as an ICP chart. If your token price looks like this, you're in trouble in the long run.

Reflexivity can be a wonderful thing for protocols, as price increases can help catalyze a true community/developer ecosystem.

But the reverse is also true, and it can be very cruel.

Before I go further, let's quickly define a few things. Token supply has two main indicators:

Circulating supply: Tokens in circulation

Fully diluted supply: Maximum number of tokens

Circulating supply increases over time until it equals the fully diluted supply.

For example, if team tokens are locked at TGE (token generation event), when they start vesting in the 12th month, they will be added to the circulating supply. They always form part of the fully diluted supply.

Market cap = circulating token supply * price, fully diluted valuation (FDV) = fully diluted supply * price.

Market cap is a measure of demand, while FDV is only a measure of supply.

Market cap is the total value of public demand, and it rises and falls with price changes, assuming good liquidity, making it a reliable indicator.

FDV increases with market cap because both indicators are based on the current market token price. However, an increase in market cap does not necessarily mean additional demand for these locked tokens.

Holders of locked tokens may actually be willing to sell at much lower prices, so FDV may not be a very accurate measure of the true network value.

There is a saying that FDV (fully diluted valuation) is actually a meme, because the FDV of some tokens trades very wildly (e.g., Worldcoin's FDV is $50 billion).

This may make sense for retail investors, as FDV may not be that important if you are trading frequently in these assets, unless you are stuck at unlock.

But FDV is absolutely important for VCs, as they are the ones holding the locked tokens! Currently, the vast majority of VC financing agreements have a one-year lockup period, followed by expiration over the next 18-36 months.

VCs should value assets based on expected FDV over 3-4 years, as this is a true reflection of what they can return to LPs, but unfortunately, this is not how this market operates.

So what is the current paradigm I am talking about?

Tokens issued with high FDV

20% of token supply in circulation

No public token sales

Large-scale airdrops

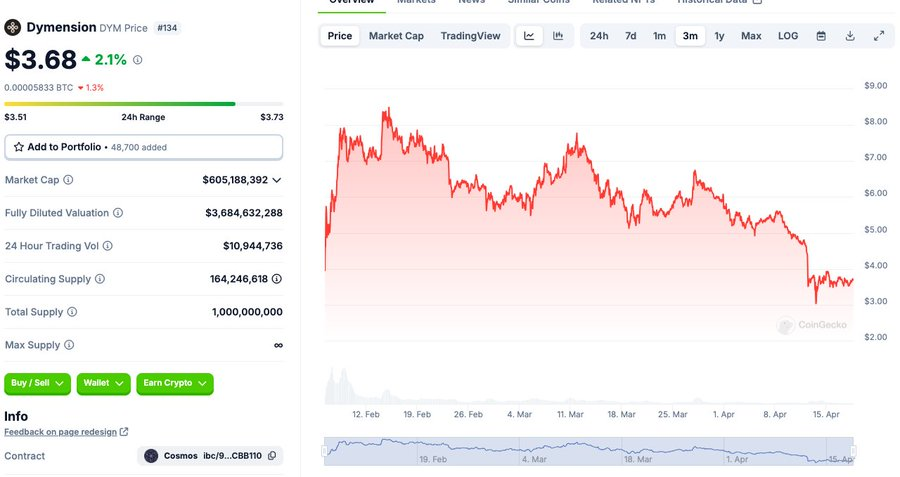

Dymension is an example, launched with an FDV as high as $8 billion, 16% in circulation, no public sales, and airdrops worth up to 9 figures.

Why is this happening?

I believe once the airdrop paradigm starts, it becomes a way to increase the dollar value of airdrops without adding more tokens.

And it enhances the pride of the team and venture capitalists.

Yes, VCs and teams can sell locked tokens, but I am not sure how much demand there is for locked tokens, so I am not sure how common this situation is.

But the above ways are not always how these projects start! Today, most dominant L1 (layer 1 blockchain)

Issuance is less than $1 billion FDV

Unlocking is generally similar, but vesting periods are usually shorter

Retail can buy at relatively lower prices ($500 million FDV)

No airdrops

Take NEAR as an example, with 20% in circulation at launch, but community sales start vesting immediately, 50% in circulation within 1 year, and an FDV of $500 million to $800 million at launch.

SOL initially had about 20% in circulation, but about 75% within a year. The initial FDV was between $300 million and $500 million.

You could buy $SOL for less than $5 for many months.

$LINK was issued at a valuation of hundreds of millions of FDV, and in the first 18 months of trading, FDV was usually below $1 billion.

These tokens all have strong communities and solid token holder bases, and their costs are relatively low. What are these legendary crypto communities we always talk about?

Forgive me for being blunt: Community means making money with your net friends. In the cryptocurrency field, there are few strong communities that are not making money.

Remember the ICP chart, do you really think there is a strong ICP community? Absolutely not.

What will happen next?

The price of tokens only rises when there are more buyers than sellers.

So who are the buyers in today's market? Definitely not institutional investors!

Yes, there are some liquidity funds, and there are some cryptocurrency venture capital funds buying tokens, but there really isn't much capital flowing into the liquidity market.

Setting aside ETH/BTC, the absolute largest annual inflow of funds is only $10 billion to $15 billion.

Just this week, we have seen the issuance of three tokens with a total supply exceeding $5 billion, with no chance for enough institutional bids to absorb the supply in the market.

Ultimately, all the end buyers of these tokens are retail investors.

But the problem is, retail investors have very limited interest in high-valuation, low-circulating supply tokens. There are two existing problems:

First, these tokens are expensive. No one thinks it's a good deal to buy something with a ten-figure FDV

Second, through these large airdrops, retail investors can get tokens for free! So why would they buy more?

The most anticipated token release this year

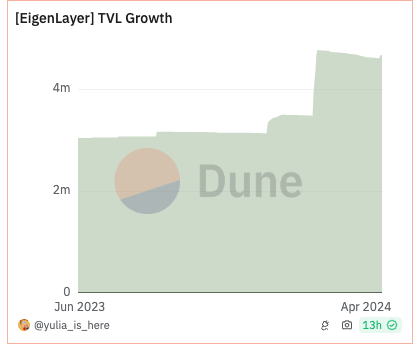

EigenLayer may be issued at a valuation of over $10 billion FDV. I bet that at least most knowledgeable ETH holders are already farming Eigenlayer.

Over 3% of ETH has already been deposited, and an ecosystem worth over $5 billion has formed around the airdrop narrative.

Logically, if you want Eigenlayer's airdrop, you probably already own ETH.

If you have ETH, you are likely using it now to earn Eigen tokens! So a large part of potential buyers will get tokens for free

Of course, people can go buy more, and there will obviously be some non-zero buying behavior, but I am skeptical of it being a huge market.

I personally have a fair amount of ETH in various LRT or Eigen, hoping to get a substantial airdrop.

If it's a $20 billion FDV, would I buy more? The answer is obviously no.

So what is the other buyer market?

Retail investors want to get involved in Eigenlayer, but for various reasons cannot buy the tokens. Obviously, the number of buyers is not zero, but I don't believe there are large numbers of retail investors willing to buy $EIGEN at a $25 billion FDV.

So, we have established that the audience for buyers is limited.

What about sellers?

If your FDV is high enough, VCs will obviously sell!

If you've gone from a $100 million seed round to a $200 billion FDV, it's very reasonable to take the money off the table!

Retail investors are aware of this dynamic and are tracking it! Token unlocks are verifiable, click here to learn more.

Are airdrop participants selling? I haven't seen a lot of data on the sales ratio in this round of airdrops, but there is an obvious psychological concept that the value you place on something you get for free is lower than something you buy.

Most airdrops are also based on the nominal value of the assets you deposit/stake, so they make up a small proportion of your portfolio. For example, if you deposit 1 ETH in Eigen, you might get tokens worth 0.05-0.01 ETH, so it doesn't make much sense for most airdrop hunters.

So this is why we are in a paradigm of only going down, I'm not trying to pick faults with these projects. I don't know what they are doing, I think they are all well-intentioned, and Eigen is a novel product.

How to break free from this pattern?

I believe the following three ways are needed to break free from the current pattern:

Linear unlocking

Public token sales

Create cool stuff

6MV has done some great research, often finding that smaller unlocking events have less impact on price than larger events.

I think the right direction should be to have 20-25% of tokens in circulation at TGE, with a linear unlocking over 36 months.

Additionally, there should be public token sales. Let retail investors buy your project on a large scale, the demand for Near's token sale was so high that it crashed the CoinList website twice.

It's obvious that there is a lot of demand even before the TGE! Allowing the community to accumulate tokens worth $5-25K outside of airdrops will buy more loyalty.

Finally, it's about creating cool stuff. Projects that have performed well in this cycle are often super innovative, like Ethena or Jito. I don't know if this applies to the rest of the cycle, but intuitively, it might be the case.

Perhaps retail investors are tired of being pushed the tenth parallel DA (data availability) modular solution.

Venture capitalists can complain about meme coins causing them trouble, but if they think the market structure of previous cycles will continue forever, then the problem is actually with them.

I am still highly bullish, we are actively deploying. This is not a macro view of the market.

This is a warning, buying into the current token issuance structure clearly will not lead to long-term success.

For the past decade, I have been bringing these protocols to market and have witnessed dozens of times which protocols work and which do not.

Do not listen to bad advice from venture capitalists, consultants, or anyone else, they are trying to tell you that buying at the highest FDV is wise.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。