Author: 0xmiddle

Preface: The landscape of multiple chains and the flourishing development of Layer2 have brought more choices to users and developers, but it has also led to a serious fragmentation of liquidity. How can users fully utilize global liquidity to optimize the trading experience? How can developers of multi-chain applications deploy and guide liquidity to maximize utility? This article will list various industry solutions and analyze their advantages, disadvantages, and development trends.

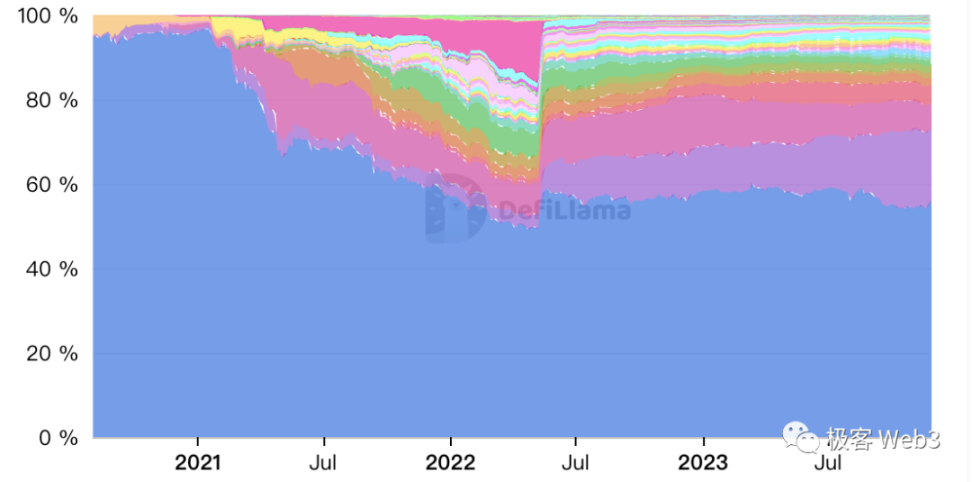

Main Text: Today's Crypto is a chaotic world composed of multiple chains. Previously, Ethereum gathered the majority of liquidity and DeFi applications in the crypto world, but now its TVL share has dropped to below 60% and continues to decline.

Some EVM-compatible chains and new public chains are still continuously eroding market share. Faced with this situation, Ethereum is also undergoing self-revolution to improve performance and ecological capacity. Various Layer2 solutions have become the biggest competitors of new public chains, once again snatching assets and users from Alt chains.

Image Source: defillama.com/chains, the blue part represents Ethereum's TVL market share

This world of multi-chains and L2 coexistence provides more possibilities for dApps and DeFi financial innovation. dApps do not have to be built on the expensive and congested Ethereum mainnet, avoiding limiting their adoption rates due to gas fees. While Layer2 brings high performance, it can still interact with assets within Layer1 and even the entire EVM ecosystem. dApps can even choose to independently build exclusive L2 application chains.

It is foreseeable that the decentralization of applications and liquidity will intensify in the future, bringing new challenges to developers and users.

For users, regardless of which chain they trade on, they can hardly mobilize global liquidity, leading to higher price impact, making large transactions easily affected by insufficient liquidity. Some assets may not even have liquidity on certain chains, forcing users to cross to other chains to trade.

From the perspective of developers, in order to cater to users on different chains, they need to guide liquidity on different chains, which brings additional costs. If limited liquidity is guided to different chains, it will make the liquidity of all chains thin, deteriorating the trading experience. However, if some chains are abandoned, it will also mean giving up some users and business income.

Faced with the dilemma of liquidity fragmentation, some solutions attempt to start from the user's perspective, allowing users to efficiently utilize liquidity on different chains as much as possible during transactions to reduce trading slippage. In general, there are two ways—Liquidity Router and Trading Agency.

Liquidity Router

Liquidity Router is manifested as applications similar to trade aggregators. When users conduct transactions in these applications, the system does not only use local liquidity to complete the transaction for the user, but also searches for the optimal trading path from different chains. Liquidity Router can serve local transactions as well as cross-chain transactions.

We will use Chainhop and Chainge Finance as examples to illustrate how Liquidity Router works. Both are cross-chain exchange aggregators.

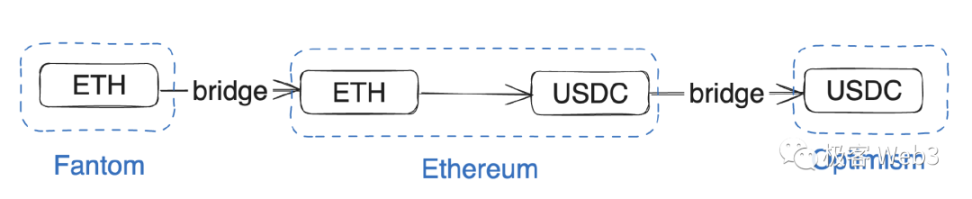

On ChainHop, if a user wants to exchange asset A on chain X for asset B on chain Y, but the primary liquidity of A/B is on chain Z, Chainge Finance will execute multi-hop transactions to help the user send asset A to chain Z, exchange it for asset B, and then send it to chain Y. Through this "multi-hop" method, although gas expenditure is increased, it still provides users with a more optimal trading result overall.

For example, when a user requests to exchange a large amount of ETH on Fantom for USDC on Optimism, Chainhop will first bridge the ETH to Ethereum, then complete the ETH-USDC exchange on Ethereum (usually with much smaller price impact), and finally bridge the USDC to Optimism.

Chainge Finance goes further by supporting the splitting of orders among liquidity pools on multiple chains to complete the transaction together. For example, if a user needs to exchange a large amount of ETH on the Fusion chain for USDT on the Tron chain, the system may split it between Ethereum and Polygon, complete the exchanges separately, and then transfer the USDT to the Tron chain for the user.

Through the "multi-hop" and "order splitting" mechanisms, the "Liquidity Router" method can more intelligently utilize the dispersed liquidity on multiple chains to complete transactions for users, effectively reducing the overall price impact.

Trading Agency

Trading Agency refers to helping users complete transactions after they submit a transaction request. The trading agency forms a bidding market, where users can choose the agency that can provide the best price to execute the transaction. This method is somewhat similar to an order book, but the difference is that these trading agencies do not necessarily pre-reserve their own liquidity. Instead, they can help users find the best trading path and complete the transaction after receiving the order, earning a commission from it. In this process, the trading agency can even fully utilize liquidity in CEX as long as it can provide a better price for users, regardless of the available liquidity location.

Similar to the Liquidity Router solution, the Trading Agency solution can also provide both local trading services and cross-chain trading services for users.

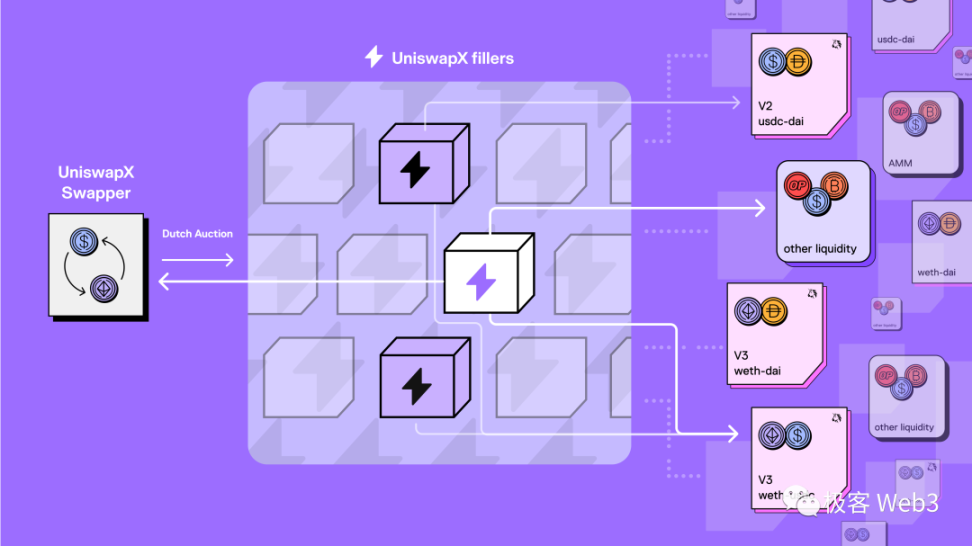

A typical case using this approach is Uniswap X. Uniswap X is a new product released by Uniswap Labs in July 2023. In the official description, Uniswap X is a new type of permissionless, open-source, Dutch auction-based aggregation trading protocol that provides services for users across AMMs and other liquidity sources, with advantages such as no gas, no slippage, and resistance to MEV.

The trading agency in Uniswap X is called "Filler." After a user initiates a transaction request through Uniswap X, it will be responded to by a Filler. Fillers compete with each other, and the system determines who will take the order through a Dutch auction. The winning Filler will help the user complete the exchange. In short, Uniswap X allows numerous Fillers to provide users with the best execution price through bidding, and Fillers gain a competitive advantage by finding better trading paths.

Image Source: Uniswap X Official Introduction

Throughout the process, Gas is paid by the Filler, so users experience a gas-free transaction. As for the risks of MEV attacks and slippage, they are also transferred to the Filler, and users can obtain a "what you see is what you get" trading experience.

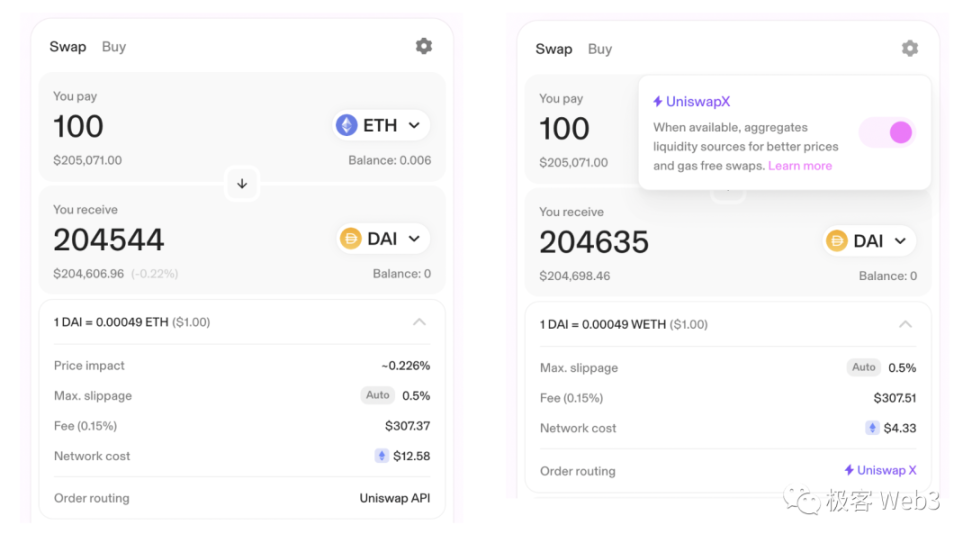

The Uniswap website interface already has a button to enable Uniswap X, which users can manually activate by clicking the gear icon in the upper right corner. Currently, it only supports the Ethereum network.

Now, whether it is the "Liquidity Router" or "Trading Agency" model, the core is to focus on delivering the best execution price to users, hiding the complex process, and being replaced by smart algorithms or bidding markets. This way, there is actually a more fashionable and more appropriate concept to describe it, which is the "Intent Layer". Whether it is liquidity routing or trading agency, they can be considered as different forms of Intent Solver. Of course, the Intent-Centric narrative is very grand and includes many other aspects.

How to Deploy Liquidity Better?

Above, we discussed how to help users better utilize liquidity across multiple chains. So from the perspective of liquidity deployers and guides, that is, the DeFi project side, how can the efficiency of liquidity utilization be improved?

For DeFi projects, liquidity is their core, and even liquidity is the service provided by DeFi projects themselves. Fragmented liquidity will prevent each part of the liquidity from achieving maximum utility, and the overall liquidity efficiency will be at a low level, hindering the establishment of its competitive advantage. Concentrating liquidity on one chain will also mean losing users and opportunities on other chains.

There are two feasible approaches to improve this problem.

The first approach is SLAMM (Shared Liquidity AMM), which sets up a role called "Predictor" responsible for predicting the distribution of trading volume in the future and based on this, scheduling liquidity in advance. The closer the predictor's prediction is to the actual situation, the more rewards the predictor will receive.

Ideally, the predictor can transfer liquidity from other chains to a certain chain before the trading volume explodes on that chain, to prevent insufficient liquidity from causing transaction failures. It can also transfer surplus liquidity to where it is needed before the trading volume on a certain chain decreases, to avoid wasting liquidity.

However, this approach has significant drawbacks. Firstly, even with reasonable scheduling, each chain still cannot use global liquidity. Secondly, changes in trading volume are often unpredictable, and predictors lack the basis to make reasonable predictions and schedules. Thirdly, users have to pay fees to the predictor.

Although SLAMM has been proposed for over a year, so far, the author has not seen any practical cases of SLAMM, indicating that developers do not favor this approach.

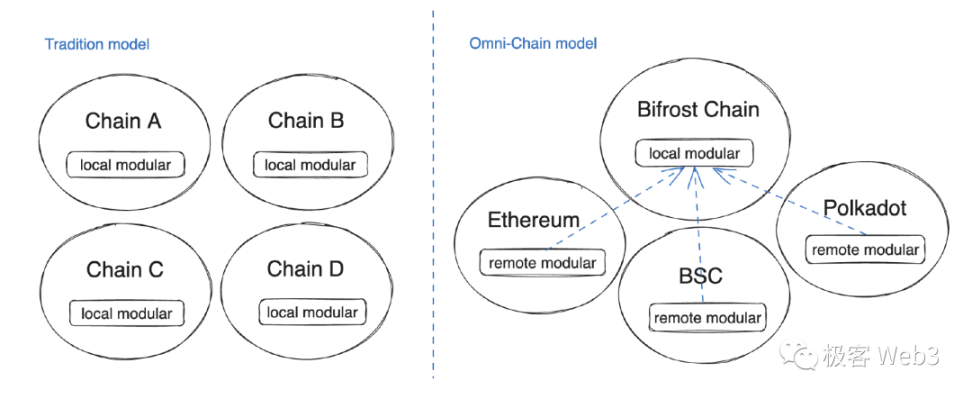

Remote Access to Liquidity

This is a simpler approach. DeFi projects deploy and guide all liquidity on one chain and provide remote access modules on other chains. When users initiate transaction requests on other chains, they actually use liquidity remotely through cross-chain methods.

This approach has many advantages, including:

- Users access global liquidity on any chain

- Liquidity deployment and guidance become simple, with no allocation and scheduling issues

- Better cross-chain integrations, applications on other chains can also use the project's global liquidity through remote access. For example, lending projects can use global liquidity remotely for liquidation, reducing slippage during liquidation.

The Bifrost project of the cross-chain LSD is practicing this approach, as mentioned by the author 0xmiddle in the previous work "The Future of Cross-Chain Bridges: Full Interoperability of Multiple Chains, the Decline of Liquidity Bridges". In fact, this is not just a liquidity deployment method, but a new application architecture. We can describe it as a "headquarters + branch" structure.

In this structure, applications do not need to deploy instances on all chains, but only deploy the core module (headquarters) on one chain, and deploy a lightweight remote module (branch) on other chains. Users from any other chain access the application remotely and receive services through cross-chain methods.

In other words, not only liquidity, but also the main part of the application is unified on one chain.

Of course, this model also has challenges. During remote access, cross-chain bridges are required, and executing two cross-chain transfers (one each way) will incur additional costs. If the cross-chain bridge infrastructure is not secure enough, there will be additional risks in such operations.

But what the author sees is that the cross-chain bridge infrastructure is constantly developing and improving, and a new generation of more secure cross-chain bridges is emerging. The impression of insecurity caused by cross-chain bridges will be dispelled. You can refer to the author's article "The Collapse of Multichain May Become an Opportunity for the Transformation of Cross-Chain Bridges" for more information.

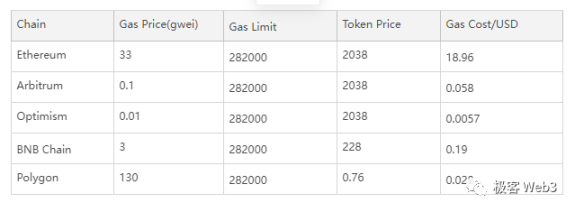

Let's analyze the cost of cross-chain asset transfers. This cost is divided into two parts: first, the Protocol Fee charged by the cross-chain bridge for maintaining Bridge Nodes and Relayers, which is generally minimal and can even be fully subsidized by some cross-chain bridges, such as Wormhole and Zetachain; second, the Gas fee generated during the cross-chain process, which is the main part.

Compared to local exchanges, remote exchanges will incur an additional cost of approximately 282,000 Gas (using EVM as an example). This Gas fee on Arbitrum, Polygon, BSC, and Optimism is generally between $0.005 and $0.2, although this price fluctuates with network congestion and token price fluctuations, it is within an acceptable range. Ethereum L1 is a bit more expensive and may require special treatment.

Table Note: Data captured on November 30, 2023;

Price data source: coincarp.com;

Gas price data source: gasnow.io, bscscan.com/gastracker

Regarding the calculation of Gas fees:

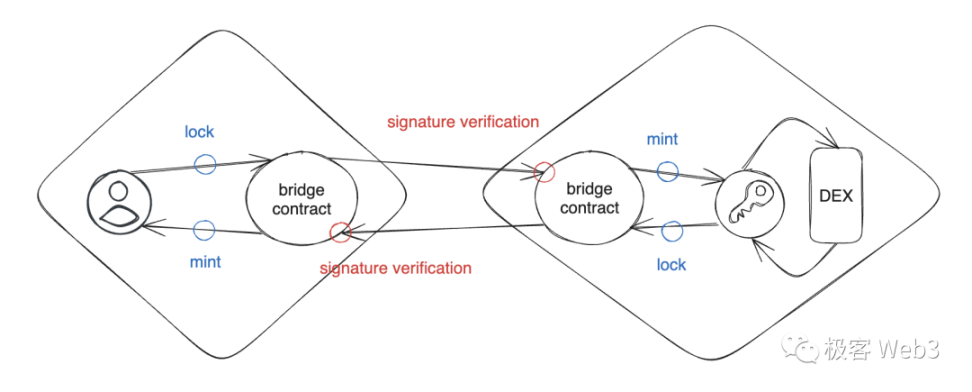

A single cross-chain token transfer includes one transaction on the source chain and one on the target chain, totaling 2 Token Transfers (which may be lock-mint, burn-unlock, or burn-mint). The Gas fee for a single ERC20 token transfer is generally 60,000 Gas, so for two transfers, it is 120,000 Gas.

In addition, there is a cost for signature verification during cross-chain transfers. The purpose of signature verification is to confirm that the cross-chain message has been confirmed by Bridge Nodes. Bridge Nodes can use MPC technology for joint signature, and the signature formed is a single signature, no different from a regular address signature. The Gas required to verify this signature is also no different from verifying a regular address signature, approximately 21,000 Gas (for more information on the application of MPC technology in cross-chain bridges, you can refer to this article).

Therefore, the Gas fee for a single cross-chain transfer can be considered as:

120,000 + 21,000 Gas = 141,000 Gas, and the Gas fee for two round-trip cross-chain transfers is 282,000 Gas.

Image Note: The example in the image is for lock-mint, but in fact, there are also burn-unlock and burn-mint scenarios for asset transfers.

So, from a cost perspective, we can also conclude that the cost of cross-chain interoperability is not significant compared to the challenges caused by liquidity fragmentation. The remote liquidity call mode is more feasible than the dynamic scheduling mode.

Viewpoints and Conclusion

Above, we have explained the reasons for the emergence of a multi-chain landscape and its inevitability, and through examining the industry's existing explorations, we have opened up ways to address the issue of fragmented liquidity.

In summary, there are two main points. Firstly, new trading methods centered around intent, including liquidity routing and trading agencies, are helping users better utilize liquidity across multiple chains and reduce trading losses.

Secondly, DeFi applications are also pursuing higher efficiency through better liquidity deployment. Dynamic liquidity solutions are better than static ones, but with the maturity of cross-chain infrastructure, "single-chain liquidity deployment + remote call" is a more promising solution.

In the future multi-chain liquidity landscape, the main liquidity of most assets will be concentrated on one chain, and remote exchanges will become the norm. Stablecoins (USDT, USDC, and even in a sense, ETH) are exceptions, as they will be distributed across various chains and serve as mediators for cross-chain asset exchanges.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。